JHVEPhoto/iStock Editorial through Getty Photographs

Thesis

Intel (NASDAQ:INTC) is endeavor a capital-intensive endeavor that many traders are doubting. The corporate has grow to be operationally unprofitable as its enterprise has been negatively impacted by inner and exterior elements. Whereas the outlook might seem bleak at this juncture, traders ought to maintain a watch out for enhancements within the basic story. There’ll doubtless come a time when Intel is a horny funding relative to friends. In our opinion, that day will not be at present.

The Foundry Gamble and IDM 2.0

Intel has embarked upon an costly quest to construct out and enhance its foundry capability the world over in a plan often known as IDM 2.0. The corporate is closely taking part in up its strategic significance to Western provide chains so as to acquire authorities help and obtain authorities cash. You possibly can learn the latest updates on IDM 2.0 right here.

Intel Foundry Companies [IFS] is Intel’s enterprise unit that may fabricate semiconductors for out of doors corporations. It is a shift in path from Intel’s primarily inner foundry operations and it stays to be seen how successfully Intel will be capable of compete on this space. The foundry enterprise is notoriously capital-intensive and there’s a lot of collaboration that goes on between the foundry and its design prospects. Intel lacks the strong testing/packaging/manufacturing infrastructure that exists in Taiwan, and economies of scale will likely be tough to come back by. The corporate is a competitor to many corporations which are potential prospects of their foundry division, which can maintain them from using IFS as a result of they do not wish to fund a competitor.

Monetary Difficulties

Intel is at present unprofitable on an working foundation and is experiencing a continued decline in income. That is typically a recipe for catastrophe, however because of the cyclical nature of the trade, some traders are prepared to provide the corporate the good thing about the doubt. We view the monetary scenario as being dismal, particularly given how a lot funding will likely be required for them to catch up in design and manufacturing whereas additionally constructing out IFS.

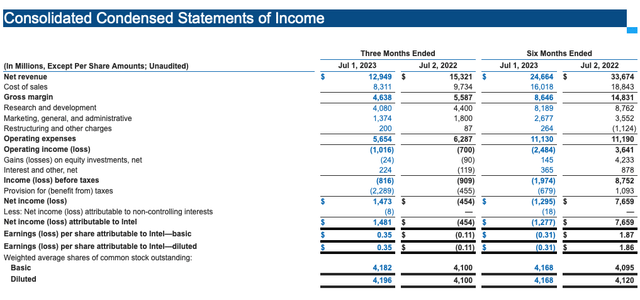

Earnings Assertion (Intel’s Quarterly Earnings Report)

The corporate is going through huge capex necessities tied to its foundry buildout, with web capex growing dramatically yr over yr. They’ve wanted to extend their debt to fund these expenditures as their working money flows have declined significantly. Absent a significant turnaround in working money movement, the corporate will doubtless must borrow much more cash over the subsequent couple of years. That is an unattractive prospect given the place rates of interest are in the meanwhile.

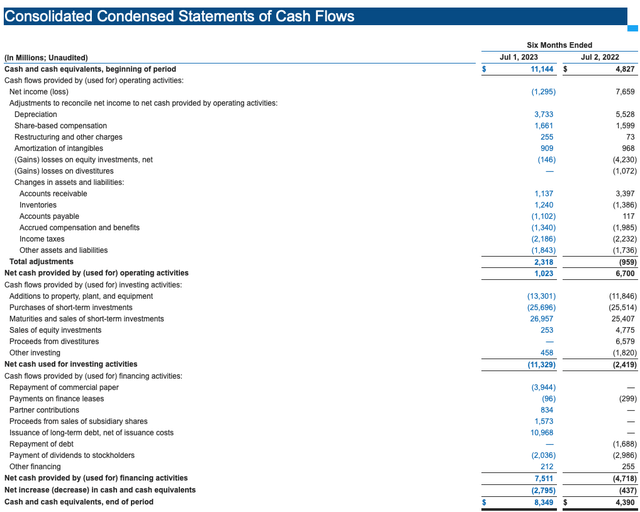

Assertion of Money Flows (Intel’s Quarterly Earnings Report)

What Might Go Proper

The bull case surrounding Intel depends on two issues going at the very least partially proper. The primary is the corporate wants to enhance its competitiveness on the logic entrance. NVIDIA (NVDA) is at present demolishing the competitors however there’s an urge for food for a substitute for Nvidia’s GPUs in HPC, and Intel can meet the market want in the event that they play their playing cards proper. It will take not solely time but additionally endurance from the corporate.

The second factor that should go proper is Intel must create and develop a financially viable foundry operation, which is not any simple job given their competitors in TSMC (TSM). Whereas some traders might doubt Intel’s IFS journey, we consider that the transfer is prudent and helps to future-proof the corporate. There may be the potential for the x86 ecosystem to proceed to lose recognition and for GPUs and CPUs to get replaced by ASICs/SOCs for HPC purposes. Intel’s prospects might choose to design their very own chips as a substitute of buying from Intel. This could be devastating for the corporate until they will earn money from fabricating the chips of their former prospects. The foundry enterprise will not be a straightforward one, however it’s one which Intel can achieve over the long run. The battle will likely be lengthy and arduous, and we consider that the majority traders do not really grasp how robust it is going to be. The monetary rewards will doubtless be far out sooner or later even when IFS and IDM 2.Zero are successful. The inventory might have a chronic interval of stagnation as traders who anticipated a fast turnaround throw within the towel and the extended danger elements maintain a lid on investor urge for food.

What to Look ahead to In Q3

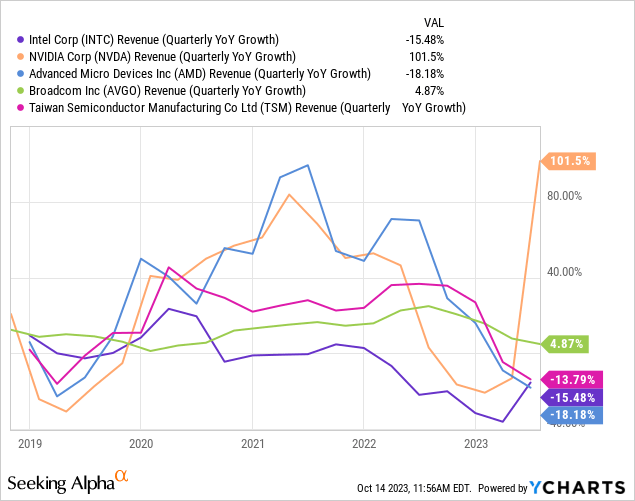

Intel is ready to report its Q3 earnings on October 26. Some key metrics to be careful for are their profitability and money movement. If these metrics proceed to worsen it might sign that the turnaround will take even longer than anticipated. It might additionally sign that Intel might grow to be financially challenged and must tackle extra debt. On the convention name, traders ought to hear for progress on design and manufacturing. Bullish traders would really like Intel to speak that they’ve a pipeline of aggressive designs and that they’re taking the best steps to create helpful foundry capability. This stuff are the important thing to the basic thesis, and in the event that they nonetheless seem like behind in these areas then traders ought to low cost their valuation for the corporate. Will probably be helpful to check the outcomes from Intel in opposition to corporations resembling AMD and Nvidia to get a gauge of how far behind Intel is, and the way a lot of their weak spot is macro-related versus how a lot weak spot is firm-specific.

Worth Motion and Valuation

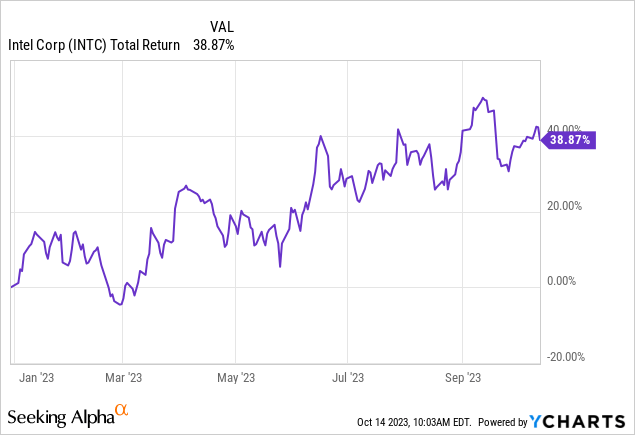

Intel has been on a pleasant run in 2023, with the inventory returning almost 40%. Going ahead the corporate might want to execute nicely on IFS and enhance its competitiveness in logic. If they will obtain this, the inventory’s upward momentum seems more likely to proceed.

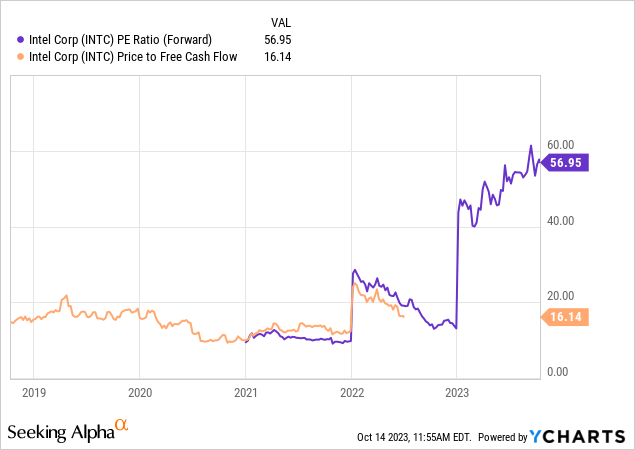

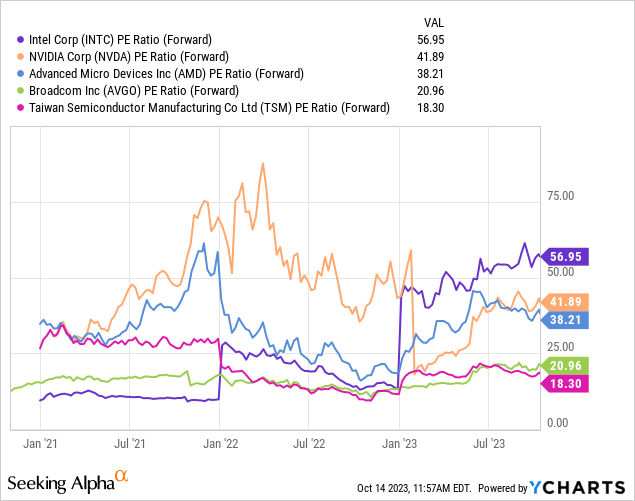

Intel is at present free money movement detrimental and has a ahead PE ratio of almost 57. It is a excessive value to pay for a corporation that’s experiencing a dramatic decline in income and profitability whereas additionally going through growing capex necessities.

Intel is not the one firm within the semiconductor trade experiencing a decline in income. That being mentioned, Intel has confronted rising issues inside its enterprise for a number of years now. For that motive, traders are typically extra skeptical of Intel re-accelerating income development than for corporations resembling AMD (AMD) or TSMC.

Regardless of the numerous weak spot of their enterprise Intel is buying and selling on the highest ahead PE of any of the businesses listed on the chart. This appears extremely optimistic and alerts that traders could also be in search of a faster turnaround from Intel than is realistically potential. It appears cheap to anticipate Intel to commerce at a valuation someplace between TSMC and AMD, which in the meanwhile would lead to a a lot decrease share value.

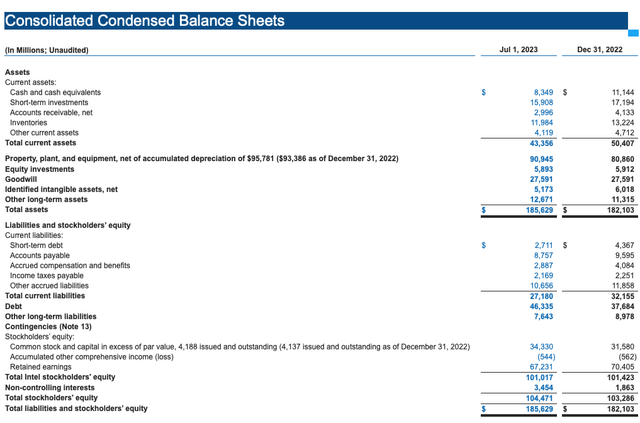

Intel has taken on extra debt to fund its foundry capability buildout. Their stability sheet continues to be in good condition however loads depends on how nicely IFS goes and the way environment friendly their capex goes ahead.

Stability Sheet (Intel’s Quarterly Earnings Report)

The basic thesis for Intel revolves across the firm’s capability to proper the ship and repair its operations. We consider that the present valuation will not be compelling and would await the corporate to make appreciable progress earlier than investing. Traders do not must seize 100% of the transfer to earn money and there’s a lot to be mentioned for avoiding turnaround tales till they really make the turnaround.

Dangers

Some dangers to the bullish thesis are the potential for his or her design models to fall behind the competitors and for his or her semiconductor gross sales to stay in a relative droop attributable to a troublesome macro surroundings.

Whereas some traders view an hostile geopolitical occasion involving Taiwan as being good for Intel, the corporate depends closely on Taiwan for a part of its provide chain and China is a big finish market. For these causes, the online impact of a China/Taiwan battle would doubtless be very detrimental for Intel.

The most important danger to the bearish thesis is the potential for Intel to execute on its bold design and manufacturing targets. This could exhibit the success of IDM 2.Zero and permit Intel to not solely earn money from chip design but additionally develop into the foundry enterprise. This could subsequently enhance their earnings whereas serving to to de-risk the enterprise. Intel’s design and manufacturing targets are operationally difficult and we’ve our doubts, however they’re definitely inside the realm of chance.

We view the general danger/reward as being unattractive presently. That being mentioned, Intel is an organization that’s value having on an investor’s watchlist.

Key Takeaway

Intel is an organization that pulls many worth and contrarian traders. Regardless of how tempting the funding could seem, we consider that staying on the sidelines is the perfect plan of action. The corporate has loads to show and traders do not lose a dime by ready for the basic image to enhance. If they will return to working profitability and present indicators of success in design and IFS we might flip extra bullish on the corporate. For now, we are going to watch and wait.

Thanks for taking the time to learn this text!

Right this moment’s query is: When you might solely decide one, would you moderately put money into Intel, AMD, or Nvidia at this juncture and why?

Tell us your ideas within the feedback beneath.