CleanCore Options has filed for an preliminary public providing with the Securities and Change Fee.

The Omaha, Neb.-based maker of cleansing merchandise mentioned Tuesday it might supply 1.5 million shares of Class B widespread inventory, priced between $four and $6 a share.

The corporate expects web proceeds of about $6.1 million based mostly on the assumed worth of $5, which it plans to make use of for paying down debt, analysis and growth and for basic company functions.

CleanCore will apply to record on the New York Inventory Change American beneath an unspecified ticker.

The corporate produces enhanced aqueous ozone resolution, which has ozone fuel infused into it and can be utilized for cleansing.

Within the yr ended June 30, CleanCore reported $2.65 million in income and a lack of $541,611.

CleanCore Chief Government and Chairman Matthew Atkinson controls all the excellent Class A typical inventory, which has 10 votes per share. Massive shareholders of Class B widespread inventory embody Lisa Roskens of Burlington Capital and Clayton Adams, one of many firm’s founders.

Unity Software program Inc. stated late Monday that John Riccitiello will retire as president, chief govt and chairman of the game-engine and ad-monetization firm he took public on the peak of the COVID pandemic.

Unity U, -1.49% appointed James Whitehurst as interim CEO; Roelof Botha, lead unbiased director of Unity’s board, has been appointed chairman. The board stated it might provoke a seek for a brand new CEO.

Lately, Unity drew hearth from sport builders and needed to alter a charge rollout for its sport engine.

Riccitiello, who will depart the corporate altogether, “will proceed to advise Unity to make sure a clean transition.” Unity shares declined as a lot as 2.5% after hours, following a 1.5% decline within the common session to shut at $29.70.

The corporate additionally reaffirmed its third-quarter outlook. Again in August, Unity forecast income of $540 million to $550 million, citing a flat game-ads market and a continued smooth market in China.

Analysts surveyed by FactSet, on the time, had estimated income of $549 million, and now forecast $555 million.

Unity went public again in September 2020, opening at $75 after pricing at $52 a share.

At Monday’s shut, Unity shares have been up 3.9% 12 months thus far, whereas the S&P 500 index SPX is up 12.9%, and the tech-heavy Nasdaq Composite COMP is up 28.8%.

The US reviews September CPI on October 12, and the primary decline in three months within the year-over-year fee is anticipated. Nonetheless, the value motion itself might overshadow not solely the CPI however different high-frequency knowledge within the week forward. US grew greater than twice the variety of jobs in September, as economists anticipated. US rates of interest and the greenback jumped initially, and shares had been dumped. After which they reversed. Many narratives shall be spun to elucidate the value motion. Whereas we couldn’t have anticipated the 336ok enhance in nonfarm payrolls or the 119ok upward revision within the earlier two months, we did acknowledge that greenback was drained. That the greenback and US charges had been unable to maintain the upside momentum is what one would count on if the market had already discounted a powerful Q3 US economic system. The Atlanta Fed’s GDP tracker nonetheless has it heading in the right direction for almost 5% progress.

China’s mainland markets will re-open from the prolonged nationwide vacation. Recall the backdrop. Disappointing financial exercise spurred many modest measures from Beijing and the PBOC utilizing comfortable and formal energy. It seems to have begun producing some outcomes, particularly for big companies. The offshore yuan is barely weaker than the place it was when onshore yuan final traded. The deflationary forces mirrored within the detrimental CPI have eased, and there may be scope for added measures to assist the economic system. A major growth for the reason that vacation started is a pointy 11-12% drop in oil costs, seemingly fueled by considerations of weakening demand.

United States: A partial federal authorities shutdown has been prevented, via persevering with resolutions till November 17. It’s far sufficient option to push it towards the sides of traders’ radar screens. That stated, the machinations within the Home appear to bolster the probabilities that the dodged bullet strikes. US job progress re-accelerated in September and with a 336ok enhance in nonfarm payrolls, nearly twice the median forecast within the Bloomberg and Dow Jones surveys (~170ok). But, the greenback’s momentum was not sustained after the employment report, and the spike in yields was retraced, with settlements close to the center of the session. A element that has not acquired a lot consideration is that with the seasonal changes, the BLS knowledge confirmed the third consecutive lack of full-time positions. Nonetheless, the greenback’s incapacity to maintain upside momentum on the favor optics is a market inform and would assist our priors of the greenback forming a excessive.

With the employment knowledge out of the way in which, consideration turns to the inflation gauges. Producer costs aren’t the story. In August, producer costs had risen 1.6% year-over-year, the best in 4 months. A 0.3% enhance in September will maintain the 12-month tempo regular. The core fee might agency a little bit from 2.2% in August. The actual curiosity is client costs. After the year-over-year fee rose in July and August, a small dip is anticipated in September (3.6% vs. 3.7%). That permits for a 0.3% enhance in September after an energy-flattered 0.6% enhance in August. A 0.3% enhance implies that the core fee will sluggish to 4.0%-4.1% from 4.3% in August. It might be the bottom studying since September 2021. The minutes from the September FOMC assembly are due on October 11. This was the assembly that was a hawkish maintain, with a majority of Fed officers seeing one other hike as doubtless applicable right here in This fall and decreasing the variety of cuts that could be wanted subsequent yr to 2 from 4. The comfortable touchdown situation that was endorsed is in line with the “increased for longer” mantra. On the similar time, there may be nice uncertainty, and it might be clearer within the minutes than within the public discourse. We be aware that on the eve of final month’s Fed’s choice, the 2-year be aware settled at 5.09%. It completed final week at 5.08%. The implied yield of the June 2024 Fed funds futures contract is about 5.23%, down a few foundation factors since earlier than the Fed met in September.

The Greenback Index peaked on October Three close to 107.35. Earlier than the stronger-than-expected jobs knowledge, it had eased to about 106.25. It rallied to nearly 107.00, which is a couple of (61.8%) retracement of the week’s decline. But, the momentum was not sustained, and Greenback Index was bought to a brand new low close to 105.95. After buying and selling on either side of Thursday’s vary, the Greenback Index closed beneath the low (~106.30). The Greenback Index’s momentum indicators are flagging. Nonetheless, a break of 105.80 would lend credence to concepts {that a} prime is being solid.

China: Mainland markets re-open after a six-session vacation. Throughout the mainland vacation, the greenback traded in opposition to the offshore yuan between about CNH7.2810 and CNH7.3315. Chinese language officers will be anticipated to proceed to lean in opposition to the wind in in search of to average the yuan’s decline. On the similar time, its concern doesn’t appear adequate to have materials clear intervention as Japan is seemingly contemplating. Nor do considerations in regards to the alternate fee eclipse the will to place the financial restoration on extra strong footing. China is anticipated to report new lending figures. Non-bank lending was notably sturdy in August (CNY1.77 billion, or a little bit greater than half of the month’s combination financing. China will even report September commerce figures. The commerce surplus via August is little modified yr over yr at about $553 billion (within the January-August 2022 interval, China’s commerce surplus was ~$549 billion). Exports have been falling on a year-over-year foundation starting final October, with the exception in March and April. Imports have been falling starting final October as nicely, and its sole exception was February. Whereas China’s commerce figures are politically delicate, the monetary markets might put extra emphasis on the inflation reviews. Recall that in August, China reported its first optimistic year-over-year CPI since Might, and that was 0.1% – a rounding error. It might be disappointing if it didn’t speed up in September. The tempo of deflation in producer costs slowed from -6.4% in June to -3.0% in August. It seems as if the nook has been turned and the deflation section is ending. Nonetheless, the takeaway is that worth pressures don’t stand in the way in which of extra financial easing by the PBOC. The greenback settled close to CNH7.3095 earlier than the weekend, in contrast with CNH7.2950 when the mainland markets started the prolonged nationwide vacation.

Japan: The primary focus is on the Japanese official intervention within the overseas alternate market and within the authorities bond market. It’s not clear whether or not there was materials intervention final week the greenback was round JPY150, however the BOJ’s unscheduled bond shopping for, and new purchases had been additionally pre-announced final week. It doesn’t look sustainable for the BOJ to attempt to cap bond yields and put a flooring beneath the yen on the similar time. Japan has three knowledge reviews within the coming day, and neither often elicits a market response. First is the August present account. It sometimes deteriorates in August. It had risen to JPY2.77 trillion in July, the biggest surplus since March 2022. Within the first seven months of the yr, Japan’s present account surplus was about JPY10.Eight trillion (~$78 billion), in contrast with JPY8.1 trillion within the January-July 2022 interval. Japan’s present account surplus will not be pushed by commerce. Japan has recorded a JPY5.1 trillion commerce deficit (balance-of-payments phrases) via July this yr. It had a JPY6.Eight trillion deficit in the identical interval final yr. Second is September’s PPI. It has fallen each month this yr. It peaked at 10.6% final December, and in August was at 3.2%. Final September’s 0.9% bounce will more than likely get replaced with a decrease quantity, permitting the year-over-year tempo to proceed to say no. Third, Japan reviews August core equipment orders. They fell 1.1% in July to carry the year-over-year decline to 13%. Higher August and September knowledge are anticipated.

The response to the US jobs knowledge noticed 10-year Treasury yield rise to a brand new excessive barely shy of 4.89%. This noticed the greenback rise to just about JPY149.55, the best for the reason that JPY150 degree was pierced on October 3. Though the greenback closed barely decrease on the week to finish a four-week surge, it’s not clear a significant prime is in place. A detailed beneath the 20-day shifting common close to JPY148.40, which the dollar has not completed since late July, could be an encouraging signal.

Eurozone: The financial diary is gentle within the days forward. There are two reviews of be aware: the ECB’s inflation survey and August industrial output. The median one-year inflation outlook fell from 5.0% on the finish of final yr to three.4% in June, the place it remained in July. The three-year median expectation fell from 3.0% final December to 2.3% in June, earlier than ticking as much as 2.40% in July. Rising oil costs and a weaker euro may raise survey outcomes due October 11. The manufacturing PMI warns that industrial output might not have recovered a lot from the 1.1% drop in July. The euro traded on either side of Thursday’s vary forward of the weekend and recorded session highs of $1.06 after the US jobs knowledge. It settled above Thursday’s excessive (~$1.0550) to publish a bullish exterior up day. A transfer above the $1.0600-10 space is required to raise the technical tone.

UK: The information spotlight of the week forward would be the August GDP and particulars. The economic system unexpectedly contracted by 0.5% in July (-0.2% anticipated), and this has renewed fears of recession. Final month, the BOE decreased its Q3 progress forecast to 0.1% from the 0.4% projection made in August. In July, all the principle sectors of the UK economic system weakened: industrial manufacturing, providers, and development, whereas the commerce deficit fell (to GBP3.45 billion from GBP4.79 billion in June). Sterling’s worth motion has change into considerably extra constructive. A key reversal was recorded on October Four as sterling fell to a brand new six-month low (~$1.2035) earlier than rallying again and shutting above the October Three excessive (~$1.2100). It hesitated close to $1.2200, however follow-through shopping for after the US jobs knowledge lifted was a brand new excessive for the week (~$1.2260). The momentum indicators have turned increased. The following technical hurdle is the $1.2280-1.2310 space. Overcoming it will strengthen the conviction {that a} backside has been solid.

Canada: Canada’s financial knowledge had been combined, however the Canadian greenback was not a match for the dollar, which rose to about CAD1.3785, the best degree since March. The September manufacturing PMI (47.5 vs. 48.0) and the Ivey PMI (53.1vs. 53.5) softened, however quite than document a commerce deficit in August, Canada reported a (small) commerce surplus and the July deficit was halved. Extra importantly, the September employment knowledge was higher than anticipated, with nearly 64ok jobs created (median forecast in Bloomberg’s survey was for 20ok). Unemployment was regular at 5.5%, not rising as economists projected, and the wage fee unexpectedly ticked as much as 5.3% from 5.2% (the median forecast was for a slight decline). Canada reviews August constructing permits and September present house gross sales within the coming days, however they don’t seem to be sometimes market movers. The weak spot of the Canadian greenback appears extreme. If a US greenback excessive is in place, as we suspect, we search for a near-term check at CAD1.3645 after which CAD1.3600.

Australia: A number of non-public surveys are due within the coming days. They embrace Westpac’s client confidence, NAB’s enterprise confidence, and the CBA’s family spending survey. Maybe crucial survey is the October 11 Melbourne Institute’s measure of inflation expectations. It had fallen from 5.6% in January to 4.6% in April, however recovered again to five.2% Might via July. It declined again to 4.6% in September. The Australian greenback posted an outdoor up day earlier than the weekend, buying and selling on either side of Thursday’s vary and shutting above its excessive. It entered a band of resistance that extends from about $0.6390 to $0.6420. A extra formidable impediment is $0.6500. The Aussie has not closed above in two months.

Mexico: The peso has fallen for the previous three weeks, which is the longest shedding streak of the yr. In actual fact, there has not been an extended shedding streak since September-October 2021. Nonetheless, it doesn’t look like particular to Mexico, besides maybe the positioning. The chance-off atmosphere of a relentless rise in US rates of interest and the greenback proved an excessive amount of. The dollar surge to nearly MXN18.49 forward of the weekend, its highest degree in nearly seven months. It has settled above the 200-day shifting common for the primary time in a little bit over a yr. The greenback’s momentum indicators are getting stretched, and though they haven’t turned down, the greenback’s surge could also be over. Preliminary assist could also be seen round MXN18.00-05, and a break of the MXN17.80 may usher in new peso consumers. Mexico reviews September CPI on October 9. It has been slowing uninterruptedly since January’s 7.91% year-over-year fee. It stood at 4.64% in August and eased to round 4.5%. The core fee is stickier. It peaked at 8.51% final November and was at 6.08% in August. It might have slowed to round 5.75% final month. Mexico reviews August industrial manufacturing on October 12. The survey knowledge warns that July’s positive aspects of 0.5% (0.8% for manufacturing) will not be repeated. The central financial institution is on maintain, with the in a single day fee at 11.25%. The swaps market sees virtually no likelihood of a minimize this yr and fewer than a 30% likelihood of a minimize in six months.

Unique Submit

Editor’s Observe: The abstract bullets for this text had been chosen by In search of Alpha editors.

Editor’s Observe: This text covers a number of microcap shares. Please concentrate on the dangers related to these shares.

Taylor Swift continues to pay dividends for the NFL.

The Swift-NFL saga, which incorporates her rumored romantic relationship with Kansas Metropolis Chiefs tight finish Travis Kelce and her appearances at two NFL video games has created a complete equal model worth of $122 million, in response to information supplied to MarketWatch from Apex Advertising and marketing, an organization that focuses on promoting and branding companies.

The equal model worth metric measures worth throughout all social media, TV, radio, digital information and print information. The $122 million determine was from Sept. 24, the day earlier than Swift’s first Chiefs sport, to Oct. 6. Swift was proven on digital camera yelling in pleasure when Kelce scored a landing because the Chiefs dominated the Bears 41-10 that evening, and the 2 had been seen leaving the sport collectively in a now-viral clip.

See additionally: AMC inventory surges as Taylor Swift live performance crosses $100 million upfront ticket gross sales

Swift’s influence on the NFL these previous couple of weeks can’t be overstated, however it will possibly partially be measured. The singer songwriter attended the Chiefs-Jets sport final Sunday evening, which set season-high viewership numbers, together with an enormous increase from feminine followers.

Swift’s new public friendship and rumored relationship with Kelce was additionally doubtless associated to the 400% improve in Kelce-related NFL jersey gross sales final month. And his Instagram followers depend jumped from 2.7 million to three.9 million as of Friday, though nonetheless a lot decrease than Swift’s spectacular 273 million followers on the Meta-owned META, +3.49% platform.

The “New Heights with Jason and Travis Kelce” podcast, that includes Kelce and his brother, is No. 1 on Apple’s podcast charts too.

The NFL’s bio on X, the platform previously often called Twitter, not too long ago learn “NFL (Taylor’s Model)” alongside a photograph of Swift and Travis Kelce’s mother, Donna Kelce, watching a Chiefs sport. Kelce stated he thinks the NFL could also be “overdoing it” with all the Swift protection, however the league disagrees.

“We regularly change our bios and profile imagery based mostly on what’s taking place in and round our video games, in addition to culturally,” the NFL wrote in an announcement Wednesday. “The Taylor Swift and Travis Kelce information has been a pop cultural second we’ve leaned into in actual time, because it’s an intersection of sport and leisure, and we’ve seen an unbelievable quantity of positivity across the sport.”

See additionally: Need to watch each NFL sport this season? Right here’s how a lot it’s going to value you.

It has been a tough stretch for the Gold Juniors Index (GDXJ), with the sector discovering itself down ~31% from its Might highs regardless of a comparatively delicate decline within the gold worth. This efficiency is much more irritating when trying on the 3-year return, with the GDXJ down almost 55% since Q3 2020 in a interval when the gold worth is comparatively flat, which has some buyers scratching their heads. Sadly, it isn’t this easy, and whereas the gold worth has held its floor above $1,800/ozoutside of transient excursions beneath this stage, margins have clobbered, affected by rising labor, gasoline, and consumables prices. The end result? A 35% plus decline in margins sector-wide from peak ranges in Q3 2020, and as much as 75% declines in margins for higher-cost producers.

On the time of the Fortuna Silver Mines Inc. (NYSE:FSM) acquisition of Roxgold in 2021, there was cause to be fairly optimistic concerning the firm’s future, on condition that it was including a sub $850/ozall-in sustaining price [AISC] mine that will assist its consolidated prices, pulling its company-wide AISC again beneath $1,150/oz. Nevertheless, two years of inflationary pressures have thrown a wrench in these plans, and Seguela is now trying like a $1,000/ozAISC mine, on condition that the 2021 AISC projections did not embrace company G&A and we have seen important inflation over the previous two years. And with Seguela being a ~$1,000/ozAISC mine and the remainder of its operations having prices above $1,500/ozon common on a gold-equivalent foundation, the outlook for margins is far weaker.

That stated, for issues that Fortuna can management, it is value commending the corporate for bringing this asset into manufacturing on schedule and price range, and the primary quarter out of Seguela was definitely spectacular, properly exceeding my expectations of 26,000 to 28,000 ounces. And whereas these grades had been properly above the common reserve grades over the mine life and will not final, it was good to see some optimistic grade reconciliation even when a comparatively small pattern of whole tonnes relative to the mine life, and with the higher than anticipated grades partially offset by fewer tonnes.

On this replace, we’ll take a look at the Q3 manufacturing outcomes and whether or not the inventory is lastly providing a margin of security after important outperformance previously few years.

Seguela Mine Operations – Firm Web site

All figures are in United States {Dollars} except in any other case famous.

Q3 Manufacturing & H2 Outlook

Fortuna Silver Mines (“Fortuna”) launched its Q3 outcomes this week, reporting quarterly manufacturing of ~94,800 ounces of gold and ~1.68 million ounces of silver, translating to a 43% and eight% decline from the year-ago interval. The sharp improve in gold manufacturing was helped by one other strong quarter out of Yaramoko, which benefited from above-average head grades within the interval, however the main contributor was Seguela, which got here out of the gate sturdy with ~31,500 ounces of gold produced in its first full quarter.

Sadly, the strong outcomes out of those two mines had been offset by one other gentle quarter at San Jose with lower than ~1.Four million ounces of gold produced, and an extra decline in manufacturing at its Lindero Mine in Argentina, with decrease grades leading to a 30% decline in manufacturing to only ~20,900 ounces. The end result was that regardless of the addition of a brand new mine, gold manufacturing was solely up 15% to ~116,000 gold-equivalent ounces from This autumn 2021, regardless of a ~60% improve within the share rely associated to the Roxgold acquisition.

Gold-equivalent ounce manufacturing comparisons use a relentless 80 to 1 gold/silver ratio.

Digging into the outcomes just a little nearer, we will see that Seguela moved as much as the #2 spot by way of quarterly output, simply behind Yaramoko, which had an abnormally sturdy quarter with its grades coming in ~15% above anticipated life-of-mine grades at 7.73 grams per tonne of gold. In the meantime, Lindero and San Jose have seen a continued decline in quarterly manufacturing, with Lindero’s manufacturing peaking in This autumn 2021 at ~36,000 ounces and set to settle at a decrease stage of ~25,000 ounces per quarter sooner or later. Lastly, Caylloma introduced up the yr with ~300,000 ounces of silver, however this can be a comparatively insignificant asset, particularly with decrease zinc costs than final yr weighing on prices due to decreased by-product credit.

So, what led to the spectacular efficiency at Seguela?

Whereas Seguela is definitely an outstanding asset with above-average open-pit grades, the Q3 efficiency was a lot better than I anticipated, with ~502,000 tonnes mined at 3.48 grams per tonne of gold at a low strip ratio of two.Three to 1.0. These higher than anticipated grades mixed with throughput charges above nameplate capability (plant throughput was 174 tonnes per hour in September, 13% above nameplate capability) helped the asset to ship properly above my estimates of 27,000 ounces of gold in Q3, and Fortuna famous that grades have reconciled properly since mining started, with the 6 p.c dip in anticipated tonnes greater than offset by a 29% improve in grades. As proven beneath, increased grades had been definitely to be anticipated from Antenna Stage 1, with an expectation of ~1.5 million tonnes at 3.Zero grams per tonne of gold from this primary section of the undertaking.

That stated, this can be a important outperformance. Whereas it is encouraging, I would not be banking on this stage of optimistic grade reconciliation sooner or later which bumped up the Q3 output.

Antenna Stage 1 – Grades & Tonnes – 2021 TR

That stated, buyers might be excited as a result of the plant is operating at properly above nameplate capability, suggesting this asset can run at nearer to 1.55 to 1.60 million tonnes every year, in step with ranges it anticipated to ramp as much as in 12 months Three in line with its preliminary mine plan. Assuming the asset can function at ~1.50 million tonnes subsequent yr with a mean grade of ~3.40 grams per tonne of gold for its first two years, the asset ought to produce upwards of 155,000 ounces every year, setting it as much as report new quarterly information nearer to 40,000 ounces over the subsequent a number of quarters. Therefore, there’s some upside to the manufacturing we simply witnessed at Seguela, and as famous in previous updates, there’s room to optimize this mine plan by pulling ahead high-grade ounces from Sunbird.

Though that is definitely thrilling, this is only one asset, and the fact is that whereas one of the best years are forward of Seguela, with a mean annual gold manufacturing profile of ~150,000 ounces from 2024 to 2027 at sub $1,050/ozAISC, one of the best years are behind the corporate at three of its different property, which embrace Lindero (previous its peak years of grade), Yaramoko (steadily declining throughput offsetting comparable grades), and San Jose, which continues to see declining grades and is struggling to switch its reserves.

So, whereas it is definitely optimistic to have this spectacular asset on-line and firing on all cylinders, Seguela is not any Fekola, which reworked B2Gold (BTG) in a single day right into a money move machine, so it is solely going to assist a lot from a money move standpoint when balancing this in opposition to declining manufacturing at its different property. And, as I’ve said beforehand, I’m not optimistic about reserve development at San Jose/Yaramoko, with sticky inflationary pressures probably contributing to rising cut-off grades and a better hurdle to including new reserves at these mines.

San Jose & Caylloma – AISC Margins – Firm Filings, Creator’s Chart

Lastly, it is value noting that whereas Seguela can have a powerful H2 with elevated grades and a full quarter of upper processing charges (~360,000 tonnes) in This autumn, the corporate is not getting any assist from the gold worth, and positively not from the silver worth. In reality, silver is again to plumbing its year-to-date lows and its margins had been already razor-thin at its silver property in Q2 regardless of a better silver worth. So, whereas there is no query that Fortuna’s gold enterprise can have a greater H2 with the advantage of a 3rd mine in Seguela, the silver phase can have one other tough half yr, particularly if silver cannot discover its footing quickly on condition that the corporate is up in opposition to comparable silver costs, increased consumables inflation, and a stronger Mexican Peso (regardless of the latest rebound) on a year-over-year foundation at its flagship silver mine, San Jose.

Valuation

Based mostly on ~310 million shares and a share worth of $2.84, Fortuna trades at a market cap of ~$880 million and an enterprise worth of ~$1.07 billion. This can be a very affordable valuation for a multi-mine producer that’s diversified throughout the Americas and in West Africa.

Nevertheless, it is essential to notice that two of the corporate’s mines have sub 4-year mine lives and a poor monitor file of reserve alternative, and one of many firm’s mines is comparatively insignificant (Caylloma). Therefore, though the corporate is a five-mine producer, its future appears to be like to be that of a three-mine producer, as San Jose and Yaramoko are prone to head offline by 2027. Which means whereas the corporate will see a big improve in income and money move in 2024 and 2025, these numbers should not run charges that may be relied upon post-2025 when Seguela sees a slight dip in manufacturing, San Jose probably heads offline, and Yaramoko additionally has a a lot much less important manufacturing profile, even when it may add some reserves at 55 Zone extensions.

Yaramoko LOMP – 2022 TR

Given this setup, I do not suppose it is honest to worth the inventory on a worth to money move foundation, and I feel a big weighting ought to be positioned on P/NAV vs. P/CF on condition that the ahead 10-year run charge will look a lot totally different from the elevated years of 2024/2025. Plus, whereas Fortuna is fast to level out that it stays discounted relative to friends on a P/CF and EV/EBITDA foundation in its most up-to-date presentation, these charts can deceive if one would not learn the nice print. And whereas the corporate does commerce at a reduction to its peer group, I might argue that it has conveniently chosen its peer group to incorporate three teams that profit from increased multiples on steadiness, together with:

1. Among the lowest-cost producers sector-wide like Lundin Gold (OTCQX:LUGDF), Alamos Gold (AGI), Dundee PM (OTCPK:DPMLF), and Centerra Gold (CGAU).

2. A number of Tier-1 jurisdiction producers like SSR Mining (SSRM), Wesdome Gold (OTCQX:WDOFF) and OceanaGold (OTCPK:OCANF).

3. The best-margin and solely giant Tier-1 jurisdiction silver producer: Hecla Mining (HL).

And with solely one West African producer within the peer group and Fortuna hardly being a silver producer – with the majority of its income from gold (and fewer silver income than its silver producer friends on steadiness) – it is no shock that this low cost is in place, because the peer group will not be lifelike in comparison with Fortuna’s portfolio.

FSM EV/EBITDA & P/CF A number of vs. “Friends” – Firm Presentation

The second level value making is that whereas there might need been an argument for utilizing a 5% low cost charge for Fortuna beforehand to calculate its web asset worth, it is onerous to justify utilizing this identical low cost charge at present when charges are a lot increased and over 50% of its web asset worth is tied to a Tier-Three ranked jurisdiction: West Africa. And even when we use a 5% low cost charge for its non-West African property and a 7% low cost charge for Seguela, Yaramoko and Diamba Sud, Fortuna’s estimated NPV is available in at ~$1.55 billion, with an estimated web asset worth of ~$1.11 billion after subtracting out estimated company G&A and web debt. If we divide this determine by 310 million totally diluted shares, Fortuna’s honest worth is available in at US$3.60, translating to a 26% upside from present ranges.

To be honest, I feel we should always assign some weighting to P/CF, and use what I consider to be extra conservative multiples of 5.5x ahead money move and 1.0x P/NAV and a 65/35% weighting (P/NAV vs. P/CF), I see a good worth for Fortuna of US$4.05. Nevertheless, I’m on the lookout for a minimal 40% low cost to honest worth to justify proudly owning small-cap producers based mostly primarily in Tier-2/Tier-Three ranked jurisdictions (Mexico, West Africa, Argentina, Peru). And after making use of this low cost, the best purchase zone for the inventory is available in at US$2.43 or decrease, barely decrease than my earlier low-risk purchase zone of US$2.60 which the inventory has rallied 7% from just lately. So, whereas FSM has undoubtedly develop into extra moderately valued, I proceed to see extra engaging bets elsewhere within the sector, and one might argue {that a} 7% low cost charge nonetheless is not low cost sufficient for West African gold mines within the present charge surroundings.

Abstract

Fortuna Silver Mines Inc. had a good manufacturing quarter, and the inventory continues to commerce at a really affordable valuation, particularly if it had been a diversified silver producer within the Americas. Nevertheless, with its silver publicity being a melting ice dice and its gold publicity predominantly coming from a jurisdiction the place low single-digit money move multiples should not uncommon, it is onerous to argue for any excessive undervaluation relative to its extra related friends like Perseus Mining (OTCPK:PMNXF) and Endeavour Mining (OTCQX:EDVMF).

In reality, Fortuna arguably appears to be like costly comparatively, buying and selling at ~3.2x ahead EV/EBITDA vs. Perseus at ~2.5x and Endeavour at ~3.6x regardless of these being bigger and higher-margin producers. That stated, if Fortuna Silver Mines Inc. shares had been to say no beneath US$2.44, it might drop right into a low-risk purchase zone. So, if I had been trying so as to add lengthy publicity and was snug proudly owning what’s develop into primarily a small-cap West African gold producer, FSM appears to be like like a sexy reward/danger wager beneath US$2.44.

Virtus Diversified Revenue & Convertible Fund (NYSE:ACV) is a bond fund that specialised is convertible bonds with a purpose to generate high-yield earnings for traders. After peaking on the finish of 2021 and promoting off for two years, the fund is lastly approaching a value vary the place it would make sense to begin constructing a place for long-term oriented traders who need to increase their earnings.

First, what are convertible bonds? They’re a subset of the company bond universe. They’re totally different from common bonds as a result of they normally convert to frequent inventory after an organization’s inventory value rises to a pre-agreed worth. These might be win-win for each issuing firms and investing establishments. Discover that I stated “establishments” as a result of it’s totally uncommon for retail traders to have the ability to purchase these bonds on account of them having giant minimal funding necessities. How are these win-win for each events? It permits firms to have the ability to borrow money at low rates of interest whereas permitting traders to take part upside in inventory whereas having fun with security of bonds on the identical time.

Since convertible bonds can convert to inventory at an agreed upon value, the traders of those bonds will profit from upside in frequent inventory as if they’re holding an choices contract. In the meantime, they’re nonetheless holding a bond so the danger of dropping their cash is minimal. For example an establishment buys convertible bonds for Firm A whose inventory at the moment trades at $80 and these convert to inventory if Firm A’s share value passes $100. If Firm A’s inventory climbs above $100, the traders holding the bond take part in upside and make a revenue. If Firm A’s inventory stays under $100, traders do not get to take part in upside however they nonetheless must receives a commission as a result of it is nonetheless a bond with obligations. The preliminary funding does not go away it doesn’t matter what except the corporate goes bankrupt and the chapter courtroom decides to wipe out its bond obligations which is tremendous uncommon.

If it is a win-win state of affairs, what is the catch? In any case there isn’t any such factor as risk-free or caveat-free funding. For the corporate issuing these bonds the largest catch is that their inventory can endure dilution. When convertible bonds convert into inventory, new shares must be created which can dilute the worth of present shares. Additionally, if the corporate is paying dividends, now it has to pay dividends on extra shares which might have an effect on their money stream state of affairs.

For the investor of convertible bonds, the largest catch is that they’ve to just accept a lot decrease rates of interest for the advantage of with the ability to take part in inventory upside. An organization’s common company bonds might yield 7-8% whereas the identical firm’s convertible bonds might yield solely 2-3%. Buyers of convertible bonds are accepting decrease charges in alternate for upside potential with out taking a danger within the inventory and struggling draw back.

Now allow us to take a look at ACV’s holdings. We’re seeing that the fund at the moment holds 313 positions. Apparently sufficient not all of the fund’s positions are bonds. Discover that it has shares in Alphabet (GOOGL) (GOOG), Microsoft (MSFT) and Apple (AAPL). It isn’t unusual for convertible bond funds to carry frequent inventory as a result of their convertible shares could convert into shares. Some funds will promote their bonds as quickly as they convert into shares and e-book their revenue whereas others will maintain these shares for some time in the event that they see upside. As a lot as I do know, Apple and Microsoft do not have convertible bonds since they’ve a credit standing of AAA to allow them to command very low charges as it’s. It appears just like the fund truly purchased these shares. Now, after we take a look at among the fund’s convertible bond holdings we see Zillow (Z) 2.75% bonds and Liberty 3.125% bonds. These firms do not have the very best credit score scores and it could be very tough if not unimaginable for these firms to have such low charges in the event that they have been issuing common debt as an alternative of convertible debt.

ACV High 10 Holdings (In search of Alpha)

Which brings us to our subsequent dialogue. The kinds of firms that sometimes situation convertible bonds are going to be both start-ups, turnaround tales, firms who do not have as a lot entry to liquidity or firms with weak credit score scores. For this reason it is not uncommon for a lot of of those convertible bonds to be referred to as “junk bonds” however not all are. Just some years in the past Tesla (TSLA) was making use of convertible bonds to boost money cheaply. Typically nice firms use these once they need to get entry to low cost credit score but it surely’s uncommon for an organization with AAA or AA ranking to utilize them. It appears like ACV tries to stability it out by preserving shares of firms like Apple and Microsoft which have very sturdy credit score scores.

Presently the fund sells for a NAV low cost of 5.14%. Earlier this 12 months the fund’s NAV low cost was approaching 10% however the hole appears to be closing now. Since convertible bonds correlate strongly with the efficiency of the inventory market, you will note a wider low cost when shares are on sale and there’s panic within the streets as in comparison with when the market is in a rallying mode. Traditionally this fund ought to commerce at a value very near its NAV and reductions like what you might be seeing at this time aren’t quite common.

Knowledge by YCharts

The fund was created in 2015 and it has been round for lower than a decade. After we take a look at the fund’s efficiency, it resulted in complete returns of 87% since inception. This appears spectacular however discover that the fund’s complete return was approaching 200% by late 2021 proper earlier than final 12 months’s bear market began. This reveals you that convertible bond funds can carry out very well if inventory markets carry out effectively however their efficiency will lag if shares begin underperforming. What we have been seeing since early 2022 is what I might name a double-whammy as a result of each shares and bonds acquired hit exhausting on the identical time which is traditionally very uncommon. Sometimes bonds are likely to outperform when shares underperform as a result of folks run to security of bonds but it surely hasn’t occurred final 12 months so this fund acquired hit twice when each inventory and bond costs dropped considerably without delay. It has been recovering although so we must wait and see.

Knowledge by YCharts

The fund pays a wealthy dividend yield of 12%. A lot of the dividends come from capital positive factors which is sensible as a result of a lot of the bonds held by the corporate yield lower than 5% and most of its inventory holdings yield 1% or much less. The fund has proven some dividend development in its historical past but it surely’s been extra pushed by outperformance of the inventory market than anything.

ACV Distribution Historical past (In search of Alpha)

Tech firms are likely to situation convertible bonds excess of another sector so this fund’s publicity goes to be obese in tech shares. The fund’s total efficiency and talent to distribute any positive factors will depend upon how effectively tech shares carry out so you’ll be able to take into account investing into this fund extra like an funding in Nasdaq fairly than the general inventory market. Buyers must be snug with the truth that tech shares are typically extra unstable but in addition remember that convertible bonds take part in upside however not draw back in inventory actions so your volatility might be extra restricted in nature except we now have a bond bear market coupled with a inventory bear market which could be very uncommon, however then once more we simply had one final 12 months.

I feel this fund is now value a glance particularly in case you are bullish in tech shares total. In case you are feeling bearish about shares basically, this won’t be the fund for you although.

Jerome Schneider: The Federal Reserve’s charge mountaineering cycle has led traders to learn inside the mounted earnings universe. Usually time, prime quality portfolios can produce yield on earnings of about 6.5%.

We imagine that there is a chance for lively portfolio administration inside the entrance finish of the yield curve. Particularly taking a look at prime quality securitized merchandise, self-liquidating property and property which profit from not essentially betting on rate of interest publicity within the close to time period.

At this cut-off date, it does three distinct issues: One, being in mounted earnings and particularly on the entrance finish of the yield curve permits traders to give attention to increased money yields, earn extra earnings within the face of uncertainty and financial prospects that aren’t essentially recognized outcomes.

Quantity two, if rates of interest ought to improve, it permits you to be slightly extra defensive by way of anticipating these charge will increase and extra importantly, shielding portfolios from market volatility that may exist from additional charge will increase.

And quantity three, ought to charges really lower as financial outlooks turn into extra clouded, you will really profit by having the ability to reposition in portfolios and prolong period or rate of interest publicity to reap the benefits of an financial outlook, which means that charges are going to be transferring decrease over the long run.

These three issues permit most optionality for traders to handle increased than anticipated money balances, extra importantly show to be lively by way of how they’re fascinated about these money balances on the sidelines after which earn above market premiums.

Transferring out of top quality money T-bills and cash markets is step one to this evaluation, and we view this as being not solely a chance set proper now, however for the rapid future, till we get extra readability on the financial outlook in addition to the Federal Reserve’s resolve to struggle inflation as we enter 2024.

Disclosure

This materials comprises the opinions of the supervisor and such opinions are topic to alter with out discover. This materials has been distributed for informational functions solely and shouldn’t be thought of as funding recommendation or a advice of any specific safety, technique or funding product. Info contained herein has been obtained from sources believed to be dependable, however not assured.

British style manufacturers have been below strain Tuesday, amid nervousness over a faltering U.Okay. client and slowing world development for luxurious labels.

Shares in Boohoo BOO, -9.72% stumbled 10% after the fast-fashion retailer mentioned it anticipated revenues to fall between 12% to 17% within the yr to the top of February as lively buyer numbers declined at double-digit charges.

The London-listed group, which owns the Debenhams and Karen Millen manufacturers, mentioned the decline in gross sales would harm income within the present monetary yr, with adjusted earnings earlier than curiosity, tax, depreciation and amortization falling from the earlier forecast vary of £69 million-£78 million to between £58 million and £70 million.

Boohoo shares hit a peak in 2020, amid COVID-induced pleasure over online-focused retailers, however have fallen about 90% since.

“Boohoo, the celebration’s on maintain for now – the net style retailer loved a spectacular run between its IPO in 2014 and 2021, turning into the epitome of quick style,” mentioned Aarin Chiekrie, fairness analyst at Hargreaves Lansdown. “However since then, the celebrations have been muted and efficiency has been lacklustre, to say the least.”

Nonetheless, Richard Hunter, head of markets at interactive investor, welcomed administration greedy the nettle on expenditure and mentioned some value headwinds have been fading. “Boohoo has change into extra related to purple flags somewhat than glad rags, however this newest replace a minimum of presents some glimmers of hope,” mentioned Hunter.

“The group has acknowledged that it must trim some fats, and has recognized £125 million of annual value financial savings over the following two years. On the identical time, with the provision chain easing and with decrease enter costs starting to filter by means of, boohoo has been in a position to move on some decrease costs to clients,” he added.

And Andrew Wade, analyst at Jefferies, rated Boohoo a purchase, although diminished his worth goal from 85p to 75p, stating: “We’re inspired by the group’s operational and strategic progress that ought to help a transparent restoration when the demand image improves. “

In the meantime, larger up the style worth vary, Burberry shares BRBY, -3.78% fell greater than 3% after UBS downgraded the inventory from impartial to promote and clipped its worth goal from 2,285p to 1,614p.

For the reason that appointment of Daniel Lee because the artistic director in September 2022, the market has had excessive hopes for the model’s new course, mentioned the united statesresearch group led by Zuzanna Pusz.

“Nonetheless, the suggestions on the brand new assortment appears muted,” wrote Pusz in a word. “Our discussions with chosen wholesalers recommend its worth level is just too excessive for the focused client, thus driving a discount in orders y/y, whereas among the social media traits additionally don’t recommend any ‘hype’ among the many shoppers.”

This muted response to “the brand new model aesthetics” mixed with what UBS phrases an more and more difficult sector context, implies that the turnaround could should be extra pricey to succeed, mentioned Pusz. “We imagine that consensus [earnings] estimates are too excessive,” she concludes.

Within the broader market, London’s FTSE 100 UK:UKX fell 0.1%, helped by banks however hindered by interest-rate delicate shares akin to utilities as bond yields continued to rise. The DAX DX:DAX in Frankfurt fell 0.8% to its lowest since March as utilities RWE RWE, -3.82% and E.ON EOAN, -3.07% each fell greater than 3%.

Funding grade company bond funds are usually a more sensible choice than high-yield bond funds in occasions of market turmoil. Nevertheless, final yr was a brutal yr for each varieties of funds because the Federal Reserve aggressively hiked the charge. Will this pattern proceed in the direction of the tip of 2023 and into 2024? On this article, we’ll analyze iShares 5-10 12 months Funding Grade Company Bond ETF (NASDAQ:IGIB) and supply our insights and proposals.

Funding Thesis

IGIB invests in funding grade company bonds in the US. The fund gives a sexy yield of 5.93% and has a high quality bond portfolio with low default charges. Nevertheless, an financial recession which will seemingly occur in early 2024 could set off a selloff. Lengthy-term earnings buyers ought to deal with this occasion as shopping for alternative to build up extra shares because the occasion will seemingly be non permanent. Over the long term, we anticipate each capital appreciation and stable curiosity incomes.

YCharts

Fund Evaluation

IGIB has carried out poorly since 2021

IGIB reached its historic peak through the pandemic due to the Federal Reserve’s quantitative easing financial coverage. Nevertheless, skyrocketing inflation began in late 2021 has induced the Federal Reserve to shortly reverse its financial coverage from easing to tightening.

Because of this, IGIB has declined by over 21% since its value peak reached in 2021. Its lack of 21.3% was not the worst, although. Its peer fund comparable to iShares 10+ 12 months Funding Grade Company Bond ETF (IGLB) suffered a a lot larger lack of 36.5%. The explanation for this larger lack of IGLB is as a result of longer length of the bonds in its portfolio. On the whole, the longer the length of the bond, the extra delicate its value is to the change of charge and vice versa. In distinction, shorter-term bond funds comparable to iShares 1-5 12 months Funding Grade Company Bond ETF (IGSB) have solely dropped by 9.7% attributable to its portfolio’s shorter length attribute.

YCharts

IGIB owns a portfolio of investment-grade company bonds

IGIB’s portfolio consists of practically 100% funding grade company bonds. As could be seen from the chart beneath, BBB rated and A rated bonds characterize about 52.4% and 41.3% of the portfolio respectively. These bonds have very low default charges. In truth, the default charge for 3-year and 10-year funding grade company bonds are solely 0.41% and 1.81% respectively. With a 30-day SEC yield of 5.93%, this yield is means increased than the default charges. Subsequently, default threat is sort of minimal.

iShares

Nevertheless, there may be draw back threat in an financial recession

Though, IGIB has a high-quality portfolio of funding grade company bonds, its near-term threat can’t be ignored. We imagine the Federal Reserve’s coverage of holding the speed elevated or increased, and for longer to fight persistent inflation, could finally trigger the U.S. economic system to fall right into a recession. The explanation that it has but to occur is as a result of financial coverage usually takes 6~12 months to propagate by means of the whole economic system. Subsequently, we could finally begin to really feel this influence in the direction of the tip of the yr or within the first half of 2024. If a recession reveals up, funding grade company bonds could fall even additional as buyers search protected haven in treasuries as an alternative. As could be seen from the chart beneath, IGIB’s fund value skilled adverse spikes amid the preliminary outbreak of the worldwide pandemic in 2020 and within the Nice Recession in 2008/2009. In distinction, its treasury fund peer iShares 7-10 12 months Treasury Bond ETF (IEF) didn’t expertise any decline throughout these two durations. The reason being as a result of buyers usually understand U.S. treasuries as risk-free belongings and have a tendency to rotate cash out of riskier belongings comparable to company bonds into treasuries.

YCharts

One other potential rationalization that IGIB tends to expertise a adverse spike in a recession is as a result of over 52% of IGIB’s portfolio is BBB-rated bonds. As we all know, BBB-rated bond is the lowest-rating bonds within the funding grade class and is extra susceptible in an financial recession than A, AA, or AAA bonds. In an financial recession, credit standing companies could downgrade some BBB-rated bonds to non-investment grade bonds. Because the market anticipates these downgrades to occur, bond costs could react beforehand and trigger a fall in IGIB’s fund value.

However, buyers ought to deal with this adverse spike as shopping for alternative

Regardless of the actual fact there tends to be a adverse spike for company bonds throughout an financial downturn, long-term buyers ought to embrace this volatility. As funding guru Warren Buffett usually says, “Be grasping when others are fearful,” long-term buyers ought to deal with this uncommon adverse spike as shopping for alternative. In truth, IGIB truly outperformed its treasury peer IEF in the long term. As could be seen from the chart beneath, IGIB’s 10-year whole return of 19.7% is clearly significantly better than the 7.6% return of IEF.

YCharts

Investor Takeaway

Whereas we could also be nearer to the tip of this charge hike cycle than the start of this yr, a recession will not be too far-off too. As we’ve mentioned in our article, there should be the opportunity of a adverse spike in IGIB’s fund value. Nevertheless, buyers mustn’t worry and as an alternative ought to deal with this as shopping for alternative. Because the Federal Reserve will often flip its financial coverage from tightening to loosening in an financial recession, we see potential capital features afterward. Subsequently, buyers will have the ability to earn each a stable curiosity earnings and a few capital features in the long term. Therefore, we imagine long-term earnings buyers ought to personal this fund.

Extra Disclosure: This isn’t monetary recommendation and that every one monetary investments carry dangers. Buyers are anticipated to hunt monetary recommendation from professionals earlier than making any funding.

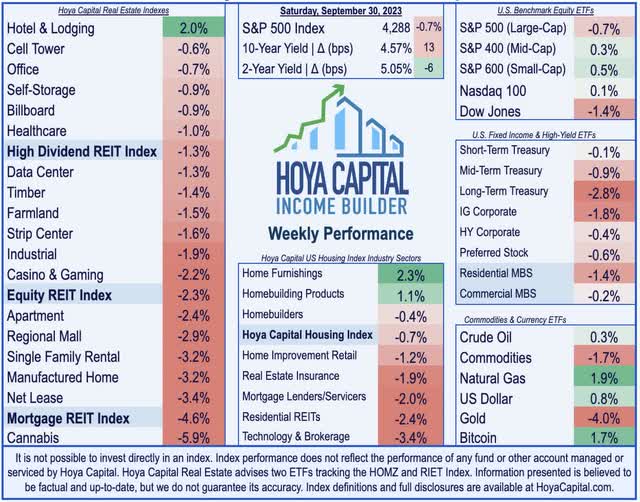

U.S. fairness markets declined for a fourth-straight week whereas benchmark curiosity continued an unabating resurgence to contemporary multi-decade highs as a possible looming authorities shutdown, lukewarm financial knowledge, and ongoing labor disputes added problems to current “increased for longer” considerations. Following a promising begin to the third quarter, optimism over a possible “comfortable touchdown” has been dimmed by resurgent oil costs – overwhelming fragile disinflationary tailwinds – and prompting central banks to face agency of their dedication to restrictive financial coverage.

Hoya Capital

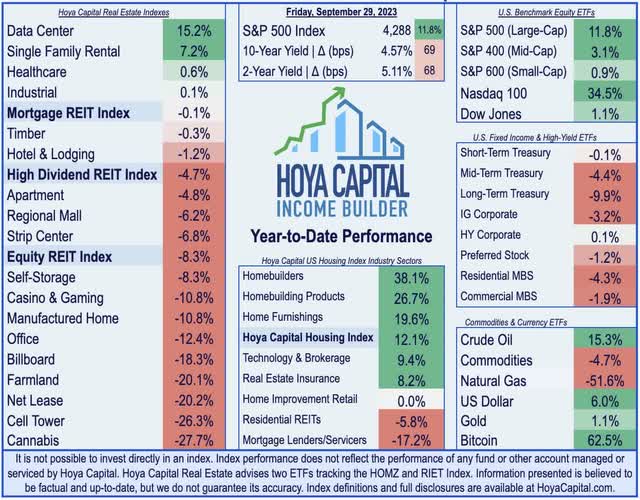

Posting its seventh weekly decline prior to now 9 weeks, the S&P 500 declined one other 0.7% on the week, ending the quarter close to its lowest-levels since early June. Nonetheless, the opposite main fairness benchmarks achieved modest positive aspects on the week, because the Mid-Cap 400 gained 0.3% whereas the Small-Cap 600 superior 0.5%. Following steep declines final week, actual property equities remained below stress amid concern {that a} “increased for longer” rate of interest surroundings will spell extra ache for personal actual property house owners and a few lesser-capitalized public REITs. The Fairness REIT Index declined one other 2.3% on the week, with 17-of-18 property sectors in detrimental territory, whereas the Mortgage REIT Index dipped by 4.6%. Homebuilders declined 0.4% as mortgage charges surged to contemporary 23-year highs, prompting a rate-driven slowdown that was already evident in sluggish New and Pending Residence Gross sales knowledge this week.

Hoya Capital

Optimistic catalysts have been more and more sparse in current weeks, lifting the Cboe Volatility Index (“VIX”) – also referred to as the Wall Road “worry gauge” – to the very best since late Might. Oil costs – a key supply of a lot of the current dismay – continued their ascent at present with Brent Crude hovering round $95/barrel as contemporary Division of Power (DoE) knowledge confirmed that inventories of the Strategic Petroleum Reserve remained close to 40-year low following a historically-large depletion in late 2022. Benchmark yields continued their ascent as effectively, with the 10-12 months Treasury Yield swelling one other 13 foundation factors to 4.57% – the very best end-of-week shut since 2007 – whereas the U.S. Greenback posted an 11th straight week of positive aspects. Complicating the financial outlook, a last-minute deal to keep away from a authorities shutdown appeared unlikely by Friday’s shut, whereas different carefully watched negotiations between the UAW and automakers additionally yielded restricted progress. Eight of the eleven GICS fairness sectors completed decrease on the week, with yield-sensitive sectors, together with Utilities (XLU) and Shopper Staples (XLP) dragging on the draw back.

Hoya Capital

Actual Property Financial Information

Beneath, we recap an important macroeconomic knowledge factors over this previous week affecting the residential and industrial actual property market.

Hoya Capital

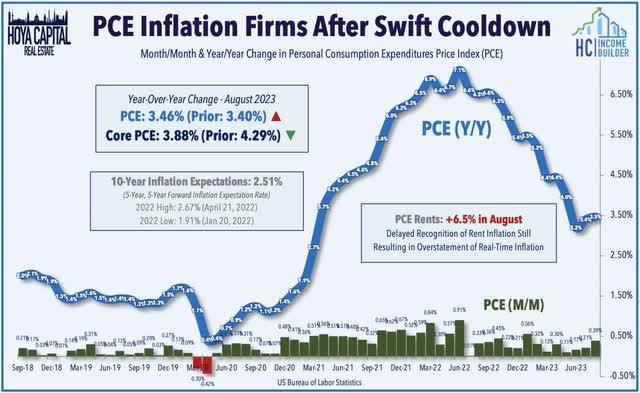

The closely-watched PCE Index this week supplied additional proof that resurgent oil costs have negated the once-promising disinflationary tailwinds. The Private Consumption Expenditures (PCE) Worth Index rose 0.39% in August – the very best month-over-month improve since January – which pulled the year-over-year improve to three.46%, a modest acceleration from July. In keeping with the traits noticed within the Shopper Worth Index, the Core metrics – which exclude vitality and meals costs – have remained on a promising development, which can develop into much more pronounced in months forward because the lagging shelter element begins to exert downward stress on these worth indices. The delayed recognition of shelter inflation has closely distorted the headline and core metrics since 2021, leading to a major understatement of inflation from mid-2021-2022 and an overstatement of inflation since mid-2022.

Hoya Capital

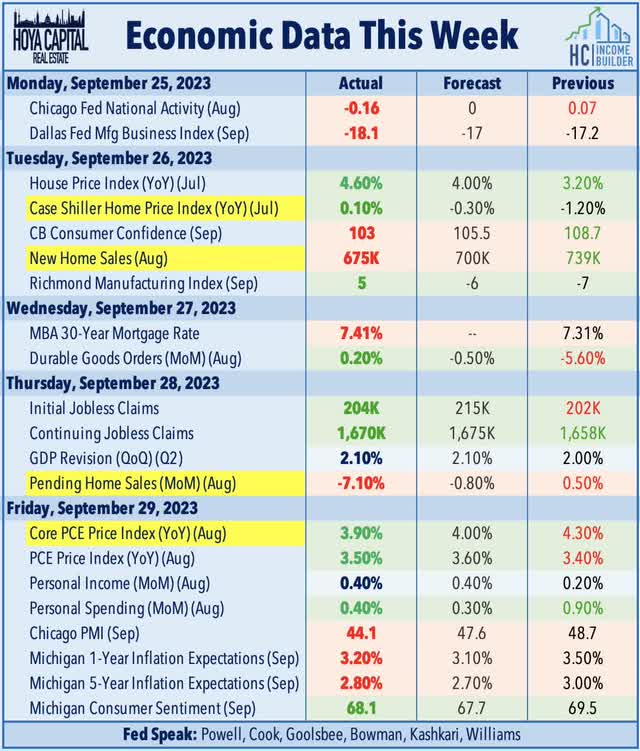

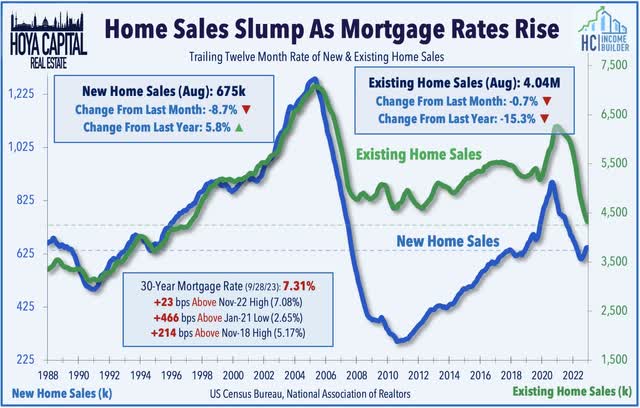

Pressured by a resurgence in mortgage charges to contemporary twenty-year highs, knowledge this previous week confirmed that housing market exercise has cooled as soon as once more over the previous two months following a modest revival in late Spring and early Summer season. New Residence Gross sales fell greater than anticipated in August, dipping 9% from final month to a seasonally adjusted annual charge of 675okay. Pending Residence Gross sales, in the meantime, posted a 7% decline from the prior month, slowing to the lowest-levels since 2020. Present Residence Gross sales knowledge final week confirmed that gross sales of beforehand owned houses dropped to the slowest July tempo since 2010, dipping to an annualized charge of 4.04 million, which was 15.3% decrease than a yr in the past. In line with Freddie Mac, the 30-year fixed-rate mortgage averaged 7.31% final week, which is now effectively above the prior November 2022 highs of seven.08%. Stock ranges have remained close to historic lows, nevertheless, with simply 1.1 million houses on the market on the finish of August, which is the bottom since 1999.

Hoya Capital

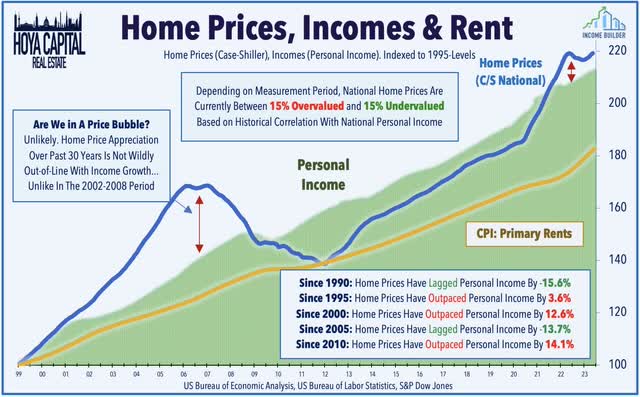

Restricted provide – leading to half from a “lock-in impact” on current householders – has supplied a ground for house values within the face of the stiff rate of interest headwinds, and has helped to usher in a interval of “normalization” in house costs after two years of unsustainable will increase in 2021 and 2022. This week, the Case Shiller Residence Worth Index confirmed that house costs had been roughly flat year-over-year in July, as costs rose modestly for a sixth straight month following a stretch of seven straight months of declines. The cooldown in house worth appreciation is welcome and critically essential to keep away from a speculative bubble that was starting to construct – and the longer-term ache that might consequence from a interval of considerably detrimental nationwide house worth appreciation. Nationwide house costs aren’t wildly out-of-line with private revenue development over long-term measurement intervals. Relying on the measurement interval, house costs are between 15% overvalued and 15% undervalued based mostly on historic correlation with private incomes, probably the most strong long-term predictor of worth traits throughout time intervals and areas.

Hoya Capital

Fairness REIT Week In Evaluation

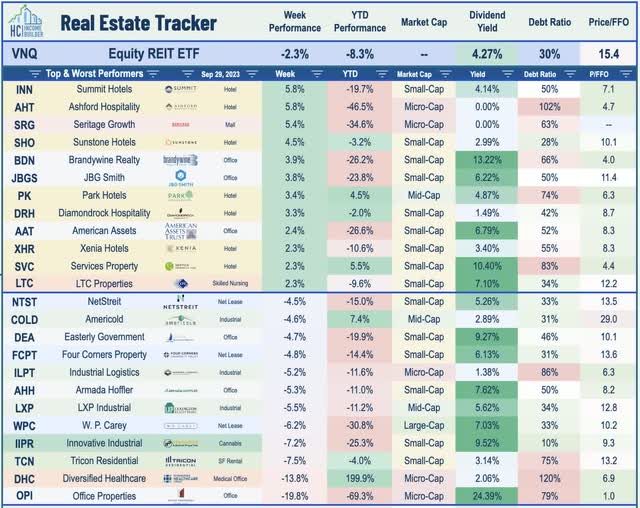

Finest & Worst Efficiency This Week Throughout the REIT Sector

Hoya Capital

Workplace: West Coast-focused Hudson Pacific Properties (HPP) gained 2% this week following a decision that ended the five-month Hollywood author’s strike. HPP is among the many largest house owners of Hollywood studio house – representing roughly 10% of its NOI – nearly all of that are operated below usage-based income fashions moderately than long-term leases. BTIG upgraded HPP to Purchase from Impartial, citing the ending of the strike, together with comparatively stable pricing on HPP’s current asset gross sales and enchancment in workplace utilization charges in a number of West Coast cities. NYC-focused SL Inexperienced (SLG) was additionally among the many leaders this week 4% after it introduced that One Madison Avenue secured its Short-term Certificates of Occupancy, finishing the event three months forward of schedule. SLG obtained $577.4M in money as the ultimate fairness cost from its three way partnership companions, which SLG used to repay company unsecured debt. The 27-story, 1.Four million-square-foot workplace tower is one in all two new “trophy” property in Midtown NYC developed by SLG prior to now a number of years, following the completion of One Vanderbilt in 2020. As famous in our workplace REIT report, the “flight to high quality” development has been evident in current quarters as renewing tenants search to make the most of the comfortable market to “commerce up” into higher-quality house, in step with our view that the workplace sector shares many parallels with the retail house within the mid-2010s.

Hoya Capital

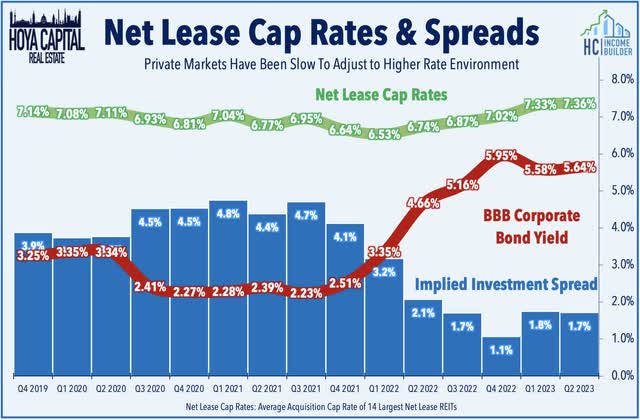

Internet Lease: W. P. Carey (WPC) remained below stress this week after extra analysts piled on the criticism of its announcement final week that it’s going to spin-off its workplace property right into a separate externally-managed REIT as a part of a “strategic exit from workplace” geared toward driving a “re-rating” of WPC’s inventory worth, which has traded at discounted valuations to similar-sized friends. This week, we revealed Internet Lease REITs: Preventing The Fed, which mentioned why these REITs have lagged in current months as traders come to grips with a possible “higher-for-longer” rate of interest surroundings. Thriving within the “decrease endlessly” surroundings, the business has been reluctant to acknowledge the higher-rate regime, preserving private-market values and cap charges stubbornly “sticky” and leading to compressed funding spreads. Regardless of the tighter funding spreads, acquisition exercise has slowed solely modestly for some REITs – who’ve paid top-dollar for current purchases – a technique that would show pricey if charges stay elevated. Sturdy stability sheets and restricted variable charge debt publicity had afforded these REITs the power to be affected person till the worth is correct, and whereas some REITs have exhibited prudence, others have plowed forward with a “enterprise as ordinary” method or made seemingly pointless pivots, placing in danger a long time of hard-fought progress.

Hoya Capital

Single-Household Rental: Invitation Houses (INVH) – which we personal within the Dividend Progress Portfolio – obtained a contemporary Wall Road ‘Purchase’ ranking by UBS, with analyst Michael Goldsmith citing the rising demand for SFR leases and a “lengthy runway” for development given the macroeconomic backdrop of a lingering housing scarcity, growing older millennials, and excessive price of house possession. UBS particularly likes INVH’s “infill product” – upper-end suburban neighborhoods – which it expects will see significantly restricted provide development, whereas its tenant base is positioned to soak up lease will increase. Among the best-performing property sectors this yr, Single-Household Rental REITs have rebounded because the dire predictions of a “arduous touchdown” in rental markets have been rebuffed in current months by steadying rental charges and robust occupancy traits seen throughout the foremost lease indexes. Whereas multifamily markets face provide headwinds over the subsequent yr, single-family builders have pulled again from an already traditionally supply-constrained single-family market, fundamentals that assist sustained inflation-beating lease development. These REITs have performed it protected – a privilege earned by way of disciplined stability sheet administration – however tighter financing circumstances will likely be a catalyst to drive additional market share positive aspects to bigger establishments which have entry to cheaper and deeper capital.

Hoya Capital

Healthcare: A pair of externally-managed REITs suggested by RMR Group – Diversified Healthcare (DHC) and Workplace Properties Revenue (OPI) – traded sharply decrease this week as each REITs introduced Board and C-suite shakeups after their merger proposal did not garner shareholder assist. OPI introduced the resignation and alternative of its Chief Monetary Officer and appointed Christopher Bilotto – presently its Chief Working Officer – as its new CEO. DHC, in the meantime, introduced the resignation of two of DHC’s Board members who served on the DHC Board’s particular committee in reference to DHC’s terminated merger plan and introduced that B. Riley Securities has been engaged as its monetary advisor to assist it consider choices to handle close to time period capital wants together with upcoming debt maturities. DHC additionally supplied a enterprise replace, highlighting a continued restoration in its Senior Housing Working Portfolio (“SHOP”). Comparable occupancy charges elevated to 79.3% in August – up 30 foundation factors from July – which was nonetheless 720 foundation factors beneath the pre-pandemic 2019 baseline of 86.5%. Larger rents have helped to offset a few of the relative occupancy declines, nevertheless, with DHC noting that comparable income was solely 7.6% beneath 2019-levels. Final week in Healthcare REITs: Restoration and Relapse, we famous that Senior Housing has emerged as a pacesetter in current quarters because the long-awaited post-pandemic occupancy restoration is lastly taking maintain, however different sub-sectors have regressed of late amid a mixture of macro and sector-specific headwinds.

Hoya Capital

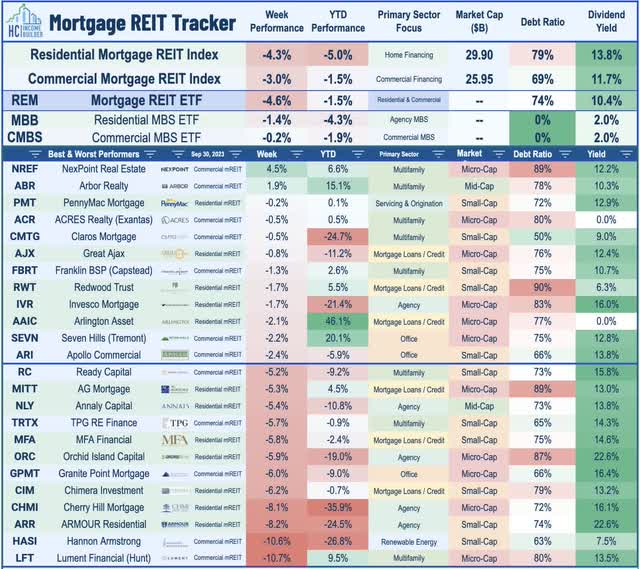

Mortgage REIT Week In Evaluation

Mortgage REITs had been below stress for a second week amid a rebound in rate of interest volatility, because the closely-watched MOVE Index jumped to one-month highs after calming to its lowest ranges of the yr in mid-September. The iShares Mortgage REIT ETF (REM) dipped 4.6% on the week, dragged on the draw back by sharp declines from a handful of agency-focused residential mREITs amid stress on residential mortgage-backed safety (“RMBS”) valuations, with Annaly Capital (NLY) and Armour Residential (ARR) among the many notable laggards. Newsflow was mild this week forward of the beginning of mREIT earnings season in mid-October. Invesco Mortgage (IVR) was among the many better-performers after it held its quarterly dividend regular at $0.40/share (16.0% dividend yield). In our Earnings Recap, we famous that mREITs stand on steadier floor with dividend protection after a comparatively stable slate of earnings outcomes exhibiting a modest improve in earnings per share.

Hoya Capital

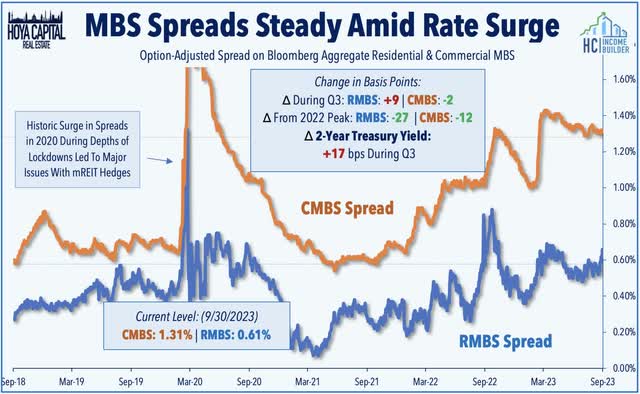

Guide Values had been in focus because the third-quarter wrapped up. Ellington Monetary (EFC) slipped 3% after it introduced that its e-book worth per share was $14.30 on the finish of August, down about 3% from the tip of Q2. Spreads on mortgage-backed bonds (“MBS spreads”) – an vital enter into Guide Worth fashions – trended increased within the ultimate two weeks of the quarter on the residential-side, however had been little modified for industrial MBS. Through the third-quarter, RMBS spreads widened by 9 foundation factors to 0.61%, whereas CMBS spreads narrowed by 2 foundation factors to 1.31%. Whereas MBS spreads had been typically regular in the course of the quarter, benchmark rates of interest – the opposite crucial enter affecting Guide Values – have elevated considerably throughout this era, with the 2-12 months Yield leaping by 17 foundation factors. The iShares MBS ETF (MBB) – an un-levered benchmark monitoring RMBS valuations – declined 3.7% in the course of the quarter, whereas the iShares CMBS ETF (CMBS) posted declines of 1.2%, indicating downward stress on mREIT Guide Values in Q3.

Hoya Capital

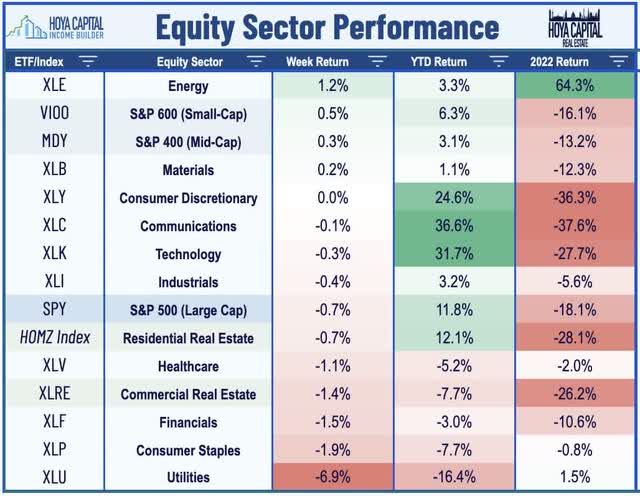

2023 Efficiency Recap & 2022 Evaluation

On the finish of the third quarter, the Fairness REIT Index is decrease by 8.3% on a worth return foundation for the yr (-5.9% on a complete return foundation), whereas the Mortgage REIT Index is decrease by 0.1% (+4.9% on a complete return foundation). This compares with the 11.8% achieve on the S&P 500 and the three.1% advance for the S&P Mid-Cap 400. Inside the actual property sector, 4-of-18 property sectors are in constructive territory on the yr, led by Information Middle, Single-Household Rental, Healthcare and Industrial REITs, whereas Internet Lease and Cell Tower REITs have lagged on the draw back. At 4.57%, the 10-12 months Treasury Yield has elevated by 69 foundation factors for the reason that begin of the yr – up sharply from its 2023 intra-day lows of three.26% in April – and now hovering at 15-year highs . Following the worst yr for bonds in a long time, the Bloomberg US Bond Index is decrease once more this yr, producing complete returns of -1.2% up to now. WTICrude Oil – maybe an important inflation enter – is increased by 15% this yr however stays roughly 15% beneath 2022 peaks.

Hoya Capital

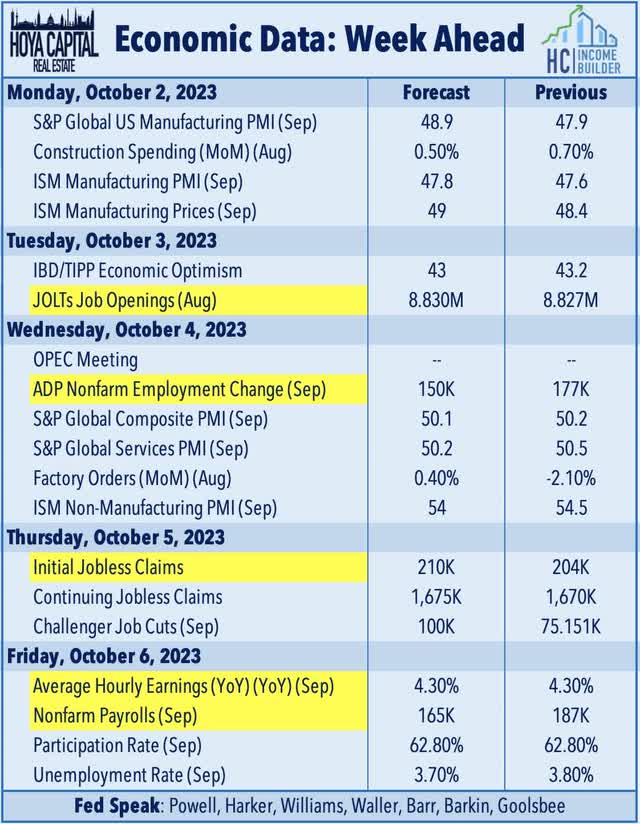

Financial Calendar In The Week Forward

Employment knowledge highlights one other crucial week of financial knowledge within the week forward – however a number of of the experiences could be delayed within the occasion of a authorities shutdown. The main report of the week – which might certainly be affected by a shutdown – comes on Friday with the BLS Nonfarm Payrolls, which is anticipated to indicate job development of 165okay in September, a moderation from the 187okay in August. The closely-watched Common Hourly Earnings collection throughout the payrolls report – which is the primary main inflation print for September – is anticipated to indicate a continued moderation in wage development to 4.3%. Wage development slowed to 4.28% final month, the slowest since June 2021. Earlier within the week, we’ll see JOLTS knowledge on Tuesday, ADP Payrolls knowledge on Wednesday, and Jobless Claims knowledge on Thursday – of which the ADP report could be the one launch unaffected by a shutdown. ‘Excellent news is unhealthy information’ will probably be the theme of those experiences as a number of Fed officers have pinned their selections to pivot away from aggressive financial tightening on a long-awaited cooldown in labor markets. We’ll even be watching Development Spending knowledge on Monday, the OPEC assembly on Wednesday, and Buying Managers’ Index (“PMI”) knowledge from each ISM and S&P.

Hoya Capital

For an in-depth evaluation of all actual property sectors, try all of our quarterly experiences:Residences,Homebuilders,Manufactured Housing,Pupil Housing,Single-Household Leases,Cell Towers,Casinos,Industrial,Information Middle,Malls,Healthcare, Internet Lease,Purchasing Facilities,Accommodations,Billboards, Workplace,Farmland,Storage,Timber,Mortgage, and Hashish.

Disclosure: Hoya Capital Actual Property advises two Trade-Traded Funds listed on the NYSE. Along with any lengthy positions listed beneath, Hoya Capital is lengthy all parts within the Hoya Capital Housing 100 Index and within the Hoya Capital Excessive Dividend Yield Index. Index definitions and a whole listing of holdings can be found on our web site.

Hoya Capital

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please pay attention to the dangers related to these shares.