Industria de Diseno Textil S.A. (OTCPK:IDEXY) Q1 2023 Earnings Convention Name June 7, 2023 3:00 AM ET

Firm Individuals

Marcos López – Capital Markets Director

Oscar Garcia Maceiras – CEO & Government Director

Ignacio Fernández – CFO

Convention Name Individuals

Geoff Lowery – Redburn

Anne Critchlow – Societe Generale

Georgina Johanan – JPMorgan

Nick Coulter – Citi

Richard Chamberlain – RBC

Marcos López

Good morning to all people. A heat welcome to all of these attending the presentation of Inditex’s Outcomes for the Interim Three months 2023. I’m Marcos López, Capital Markets Director. The presentation will probably be chaired by Inditex’s CEO, Oscar Garcia Maceiras, additionally with us is our CFO, Ignacio Fernández. The presentation will probably be adopted by a Q&A session, beginning with the questions obtained from the phone after which these obtained by way of the webcast platform.

Earlier than we begin, we’ll take the disclaimer as learn. Please, Oscar?

Oscar Garcia Maceiras

Good morning, and welcome to our outcomes presentation. It’s my pleasure to affix you at the moment. Within the first Three months of 2023, Inditex has continued its very sturdy working efficiency pushed very a lot by the creativity of our groups and the robust execution of our absolutely built-in enterprise mannequin. This efficiency depends on the 4 key pillars of our technique you might be very accustomed to.

Our distinctive trend proposition and optimize buyer expertise, our deal with sustainability and the expertise and dedication of our folks. These elements have propelled our aggressive differentiation.

Now we have had a really passable gross sales development of 13%. The execution of the enterprise mannequin has additionally been very sturdy with a wholesome gross margin and disciplined value administration. On the underside line, internet earnings elevated 54% to €1.17 billion. Our working efficiency locations us in a sound monetary place. Now we have generated important free money circulation.

The efficiency has continued within the second quarter. Retailer and on-line gross sales in fixed currencies between the first of Could and 4th of June grew 16%. Let me spotlight some key features for the yr so far marked by a powerful execution of the mannequin.

Our Spring/Summer season collections have been very nicely obtained by prospects. Gross sales in fixed foreign money elevated 15%, with a powerful development in shops and on-line. Gross sales have been constructive throughout all geographical areas in addition to in all of the ideas.

Our diversified presence in 213 markets with low market penetration permits us to get pleasure from important international development alternatives. Now we have full confidence within the capability to develop this enterprise as a result of our distinctive mannequin, which in flip is driving our rising differentiation.

I’ll hand you over to Ignacio to enter the headline numbers.

Ignacio Fernández

Thanks, Oscar. As you possibly can see in our launch, Inditex executed strongly within the interim Three months of 2023. Gross sales have progressed nicely, up plus 15%. Now we have managed the provision chain actively, and this has pushed a really wholesome gross margin.

Working bills have, in fact, been managed rigorously, leading to working leverage. Because of this, EBITDA grew 14% to €2.2 billion. Beneath this line are for comparability causes. It’s price noting the availability cost within the first quarter 2022 referring to operation within the Russian Federation and Ukraine for €216 million in that yr.

In any case, we’ve additionally seen very robust progress within the internet earnings line with a rise of 54% to €1.17 billion versus €760 million within the first quarter 2022. For full comparability, internet earnings ex provision within the first quarter 2022 would have been €940 million. We proceed producing important free money circulation, and this has taken our internet cap place to €10.5 billion.

Let me reiterate that gross sales have progressed very properly at plus 15%, reaching €7.6 billion. That is 15% in fixed foreign money. Gross sales development was robust each in shops and on-line. Moreover, gross sales have been constructive throughout all areas and ideas. Primarily based on present trade price, we count on a minus 2.5% foreign money affect on gross sales for the total yr 2023. Within the first quarter of 2023, gross revenue elevated 14% to succeed in €4.6 billion and clearly demonstrated a wholesome execution of the enterprise mannequin. The gross margin reached 60.5%.

Primarily based on present data, we count on a secure gross margin of plus, minus 50 foundation factors this fiscal yr. There was very rigorous management of working bills throughout all departments and enterprise areas.

Working bills elevated beneath gross sales development over the primary quarter of 2023. Together with all these expenses, working bills grew 150 foundation factors beneath gross sales development. Over the primary quarter of the yr, we skilled a strong working efficiency. Now we have additionally seen a normalization in provide chain situations which have returned to earlier ranges.

As a consequence of these elements, Inditex’s stock as of the 30th of April was 5% greater. As a aspect word, the end-of-the-period stock is taken into account to be of top of the range, whereas dedication ranges have remained just like final yr’s ranges. Because of the robust money circulation, the online cap place grew to €10.5 billion.

And now over to Marcos.

Marcos López

Thanks. Over the primary quarter of 2023, the group has had a strong efficiency throughout the board. We’re happy with execution over the interval. Now we have continued with enlargement and have opened shops in 17 completely different markets. The shop and on-line gross sales throughout all ideas have been sturdy. The efficiency has been robust in any respect ranges.

And now again to you, Oscar.

Oscar Garcia Maceiras

Thanks, Marcos. I wish to touch upon a few of the initiatives this season, which have been driving the rising ranges of differentiation we’re seeing at the moment.

In the beginning, our precedence stays to at all times enhance the attraction of our trend proposition. Creativity, innovation, design and high quality are the defining options of our collections and a key focus throughout all our groups.

A superb instance of that is Zara Lady Studio Capsule, the Zara Man Spring/Summer season Assortment, the Zara Children Swimwear Assortment, Zara Residence’s new Van Duysen drop, Pull&Bear’s Restricted Version, Massimo Dutti’s THE CAIRO DIARY Assortment, Bershka’s assortment for Spring/Summer season 2023, Stradivarius Welcome to the Countryside Assortment, and eventually, Oysho’s Linen Assortment.

By way of the client expertise, I wish to spotlight some key initiatives of 2023. Inditex began operations in Cambodia in Could with the opening of a Zara flagship retailer in Phnom Penh and the launch of on-line gross sales out there by way of zara.com/kh.

A key current venture has been the brand new retailer design for Zara created by our Architectural Studio that integrates organically essentially the most refined interiors with the practical and digital sections, the becoming rooms, self-checkout areas, click on&gather factors, in-store silos and inventory rooms. This new Zara retailer design is featured in openings, enlargements and relocations resembling Paris Champs Elysees, London Stratford, Miami Dadeland, Mumbai Phoenix Palladium and Johannesburg Sandton.

A key venture of the yr has been the third enlargement of the Zara retailer at London Stratford to five,500 sq. meters. Similar to all the opposite essential flagship shops just lately opened, it’s going to embody devoted areas for lingerie, sneakers and purses, the leggings [ph] assortment, the athletics assortment and newborns. It can additionally embody all of the options that enable an entire digital expertise.

And at last, the enlargement of the Zara retailer at Mumbai Palladium Phoenix. The shop extends over 2,500 sq. meters and can provide the newest trend with essentially the most up-to-date picture.

By way of buyer expertise, it is very important spotlight that the {hardware} to implement the brand new safety know-how, which eliminates the necessity for exhausting tags, will probably be accessible in all Zara shops globally by July. The intention is to launch a testing section within the 2023 Autumn/Winter season.

And now let’s cowl sustainability. As per the Sustainability Roadmap Objectives, Inditex is on monitor to ship upon the entire targets set for 2023 to 2025. Our technique is especially targeted on two pillars, innovation by way of our Sustainability Innovation Hub and circularity.

In 2022, Inditex made an funding in CIRC, the style know-how firm that recycles textile waste again into new fibers, aimed toward accelerating industrial-scale options in direction of circularity within the trend sector. In April 2023, Zara partnered with CIRC to launch a first-of-its-kind ladies’s capsule assortment made utilizing recycled polyester and lyocell derived from the separation of polycotton textile waste.

By way of circularity, the Zara Pre-Owned platform, at present accessible in the UK, will attain France, Germany and Spain within the second half of 2023. By this platform, we’ll proceed serving to our prospects to increase the life cycle of their Zara clothes by way of donation, restore or resale, and can contribute to the discount of waste.

One of many priorities of our folks technique is to advertise stimulating work environments the place the expansion and ongoing studying of our groups is inspired. Final yr, greater than 11,000 of our staff have been promoted. And on the finish of the primary quarter, there have been already greater than 2,700 individuals who have been promoted internally.

Now we have additionally invested nearly 600,000 hours of coaching on this similar interval as we’re satisfied that steady studying contributes to the non-public {and professional} growth of our folks.

Let me now transfer to the outlook for 2023. We stay on monitor to ship upon all of our long-term objectives. The expertise, dedication and keenness of our groups throughout the globe will at all times be key to our aggressive edge. We provide a novel trend proposition outlined by creativity, innovation, design and high quality. The continual optimization of the client expertise is vital to our strategy.

The energy of the absolutely built-in enterprise mannequin that’s working at full tempo has been clear in current occasions. Inditex operates in 213 markets with low share in a extremely fragmented sector, and we see loads of alternatives for each natural development and enlargement.

We see elevated gross sales productiveness in our shops going ahead and in addition count on the gross house development in 2023 to be round 3%. Optimization of shops is ongoing. We count on house contribution to gross sales to be constructive in 2023.

Steady gross margins have at all times been a key focus for us. We’re planning investments that can scale our capabilities, generate efficiencies and enhance our aggressive differentiation to the following degree. For 2023, we estimate atypical capital expenditure of round €1.6 billion.

A phrase on the dividend. As accepted in March 2023, the Board of Administrators will suggest to the Annual Basic Assembly a dividend for 2022 of €1.2. The dividend consists of two equal funds of €0.6 per share. The primary interim fee was made on the 2nd of Could 2023, and the ultimate dividend fee will probably be made on the 2nd of November 2023.

I wish to end with a short touch upon our present efficiency. Spring/Summer season collections proceed to be very nicely obtained by our prospects. Retailer and on-line gross sales in fixed foreign money between the first of Could and the 4th of June 2023 elevated 16%.

Thanks all for attending. That concludes our presentation for at the moment. We will probably be blissful to reply any questions you might have.

Query-and-Reply Session

Operator

[Operator Instructions] The primary query comes from Geoff Lowery from Redburn. Please go forward, Geoff.

Geoff Lowery

Sure. Good morning, staff. May you simply discuss your future view of house? Particularly, you have talked about 3% development this yr. Do you foresee a time sooner or later the place that quantity might speed up from right here given how fragmented the markets are and the way low your market shares are? Thanks.

Oscar Garcia Maceiras

Thanks, Geoff. Sure, for this yr, we’ve talked about two issues relating to house. First, that we have been anticipating 3% gross house development. There’ll at all times be some optimization progress right into a enterprise. And for this reason we talked about that we have been anticipating constructive house contribution for the enterprise within the yr, and that is very a lot what we count on going ahead.

What I wish to do with these numbers is to qualify that you’ve got seen the robust development throughout the board in shops and on-line, in all of the geographies, in all of the ideas. What we’ve been stressing over current years is that there’s very robust productiveness of the house. So given the truth that we see very selective robust development alternatives within the 213 markets wherein we function, we proceed to be very, very selective.

However I wish to come again to you one key message. It is rather a lot concerning the high quality of the house we open and the opportunity of that house to supply steady development with very robust productiveness greater than the house development quantity. For instance, you possibly can see that on this first quarter, a lot of the development got here by way of the – by way of like-for-likes.

So sure, we count on some constructive development coming ahead, nevertheless it’s very a lot the productiveness of our absolutely built-in retailer and on-line mannequin that can drive the expansion within the coming years.

Operator

Thanks. The following query comes from Anne Critchlow from Societe Generale. Please go forward, Anne.

Anne Critchlow

Good morning, all. Thanks for taking my query. I simply puzzled which product areas at Zara have been performing the strongest at current, whether or not it is vacation put on or tailoring or event? What are you seeing? Thanks.

Oscar Garcia Maceiras

Once more, Anne, good morning. This hyperlinks very a lot to my earlier reply. As we’ve talked about within the presentation, the standard of the gross sales of the corporate has been very, very robust. We have certified that’s all channels, each in shops and on-line, we have seen a really robust development is in all geographies. There’s not one geography that’s mainly rising extra or in a really completely different approach to others. And all of the ideas have had a really robust efficiency this quarter.

So I wish to spotlight two elements. It’s totally a lot the creativity of our groups, the trouble they make by way of having the fitting high quality, the fitting design, the fitting innovation, all the fitting merchandise on the proper time; after which the execution and the flexibleness of our enterprise mannequin which can be driving this outperformance.

Operator

The following query comes from Georgina Johanan from JPMorgan. Go forward, Georgina.

Georgina Johanan

Hello, good morning. Thanks for taking my questions. My query is simply on the gross margin, which was, in fact, an amazing efficiency within the quarter. Simply being conscious that FX was in all probability fairly a fabric drag within the quarter. I imply I assume my first query is, might you affirm that?

After which maybe simply assist us perceive, is it form of provide chain normalization by way of exterior elements and freight, et cetera, that was offsetting that? Or is it form of – or is it extra about inside initiatives and the Inditex enterprise mannequin, please? Thanks.

Oscar Garcia Maceiras

Effectively, once more, I will mix this with what I discussed at the start. The principle purpose behind the robust gross margin this quarter is the execution. that within the gross margin, there are numerous, many elements. We are able to discuss markups, markdowns, foreign money, combine, et cetera, et cetera. However given the robust development in gross sales at 13%, that is the primary driver.

As I discussed, what may be very, very related on this first quarter is the consistency of the execution throughout the board. And that is, once more, why the gross margin has been – has had this constructive efficiency on this first quarter.

Operator

The following query comes from Nick Coulter at Citi. Go forward, Nick.

Nick Coulter

Thanks, James. And good morning. Thanks for the presentation. Apologies, a non-operational query, if I’ll, on the finance earnings. Ought to we count on that internet constructive to proceed? Or are there non-recurring elements or risky elements that we have to take into account for the remainder of the yr? Thanks.

Oscar Garcia Maceiras

By way of the monetary earnings, Nick, as you’ve talked about, on this first quarter, we’ve a constructive evolution, which is the results of the yields [ph] we are actually attaining within the treasury. Clearly, the state of affairs has modified versus the earlier yr, and it’s best to count on one thing related for the approaching quarters.

Operator

The following query comes from Richard Chamberlain at RBC. Go forward, Richard.

Richard Chamberlain

Thanks, James. Morning, everybody. I puzzled if you happen to might simply contact on the brand new safety tech, eliminating using exhausting tags that you’re bringing in later this yr. When do you count on that to begin to have a constructive gross sales affect? And can that be rolled out to different codecs, different banners subsequent yr? Thanks.

Marcos López

Thanks, Richard. Effectively, as you recognize, buyer expertise is without doubt one of the key pillars for our enterprise mannequin. And we take into account that with this new know-how, we’ll eradicate exhausting tags, we’ll enhance the expertise of consumers in our shops.

We’re making good progress with the venture, as we’ve already talked about. First step is having the {hardware} within the shops, and that is anticipated to be absolutely rolled out in Zara by July. Subsequent step will probably be inserting the alarms within the clothes, and this may begin throughout the Autumn/Winter assortment. We’re working very intently with our suppliers with this function. And naturally, this venture will probably be deployed in the remainder of our codecs going ahead.

Operator

We’ll now proceed to the webcast platform. I had a few questions right here at the moment on the webcast platform.

Q – Unknown Analyst

The primary of which is, are you able to please remark – present some touch upon the expansion in Spain, please?

Oscar Garcia Maceiras

Effectively, thanks. Effectively, as Marcos has already mentioned, we’re very pleased with our efficiency this quarter. This efficiency has been constructive in all key geographical areas, in all ideas, each on-line and in retailer, and this continues over the second quarter.

And this case is, in fact, additionally predictable to our efficiency in Spain. Now we have continued to be very energetic right here. Some examples of essential initiatives undertaken just lately are our Zara shops in Plaza de España [ph] in Madrid or Juan de Austria in Valencia or our new flagship Pull&Bear retailer in Gran Vía in Madrid.

New thrilling initiatives will open within the coming months, resembling our new Zara retailer in Plaza Duque [ph] in Seville. And due to the optimization course of, our present presence in Spain is with greater, higher and nicer shops in tremendous prime areas.

Q – Unknown Analyst

The following query pertains to market particularly. Are there any feedback you possibly can present maybe on China or the USA?

Oscar Garcia Maceiras

Effectively, the concept – the primary concept that we’re very blissful about our efficiency is predicable for the U.S. and for China as nicely. that, as an example, within the U.S., we see important alternatives for selective development within the coming years with a number of initiatives already introduced. And within the case of China, we take into account that trend urge for food continues to be robust there. Chinese language prospects demand trend and are very pleased with our proposition. So China will stay in addition to one among our core markets.

Q – Unknown Analyst

Thanks, Oscar. And the following query pertains to development ambitions. Are you able to present just a little bit extra element on development ambitions and maybe just a little bit extra element on the corporate’s coverage to take it to the following degree?

Oscar Garcia Maceiras

Effectively, thanks. Effectively, I’d say that we’ve already lined this extensively throughout the presentation. However to summarize and to share the primary concepts, our mannequin is at present working at full tempo. We proceed to focus our consideration on strengthening the primary pillars of that mannequin that’s absolutely built-in.

And with this in thoughts, we take into account that the essential issue is our folks. I wish to spotlight that the expertise, the fervour, the dedication of our folks each single day and in each retailer, in each logistics heart, in each workplace world wide, is the primary driver of our efficiency quarter after quarter.

These similar elements are critically pushing us to the following degree by rising the extent of economic differentiation and pursuing development alternatives throughout all markets and throughout every of the ideas.

Operator

Thanks, Oscar. That concludes the webcast questions and the Q&A session.

Oscar Garcia Maceiras

Thanks to all of these taking part within the presentation at the moment. For any extra questions you might have, please get in contact with our Capital Markets division. And we’ll welcome you again in September for the primary half 2023 outcomes.

Scammers seem like focusing on mourners nationwide with cellphone calls impersonating funeral-home employees, in accordance with native media experiences and shopper advisories.

Grieving folks in Georgia and California have advised native media retailers in latest months that they had been contacted by scammers who posed as funeral-home employees and requested cost referring to preparations for the dying of a liked one. Enterprise leaders have additionally warned customers of the mounting development in West Virginia and Louisiana.

Within the Georgia case, a lady despatched a faux funeral-home employee $1,200 by means of Zelle the day earlier than her father’s funeral was scheduled to happen earlier than realizing her mistake, in accordance with Fox 5 Atlanta. In the meantime, CBS 8 in California reported on a distinct girl who was focused within the days after her husband’s dying, however didn’t pay the $49.90 the caller mentioned she owed for “an insurance coverage factor.”

“To benefit from a household that’s grieving the dying of a liked one is deplorable — the bottom of the low,” Jessica Koth, a spokesperson for the Nationwide Funeral Administrators Affiliation, advised MarketWatch in an e mail. The group has inspired its members to warn households they’ve served about this rip-off and remind them of their funeral dwelling’s billing practices, Koth added.

The NFDA mentioned in an alert final month that scammers had been utilizing lately revealed obituaries to pose as funeral-home employees members and name households claiming they owed some amount of cash for a service. In an replace to that alert, the group added that scammers had been additionally calling households to say they owed an instantaneous deposit to their pre-need account — an account used as a method of arranging a funeral forward of 1’s dying — or “the funeral dwelling can’t assure that the service will happen.”

Most lately, Forest Park Funeral Residence and Cemeteries mentioned in a Fb publish Friday that its Shreveport, La., enterprise had heard from a number of funeral administrators who’d mentioned scammers had been posing as workers and calling households utilizing cremation, funeral and cemetery providers. One among its personal clients had even been contacted a number of instances.

“Thankfully, they did NOT present any data and referred to as us instantly,” the funeral dwelling wrote within the publish, advising customers to be cautious of callers claiming to be funeral-home workers who want private or monetary data.

“Refuse cost and NEVER disclose bank card numbers, banking data, social safety numbers or a date of delivery,” the funeral dwelling mentioned. “Inform the caller you’ll follow-up straight with the funeral dwelling or cemetery and finish the decision. Be at liberty to finish the decision with out clarification if it seems suspicious or to be a rip-off. If potential, take down the caller’s data (together with title, title, cellphone quantity, and e mail tackle), and report this to police and to your funeral director or cemetery employees member.”

DonsESLAdventure/iStock Editorial by way of Getty Photos

Chicken World’s (NYSE:BRDS) go-public story has turn into a traditional story of how SPACs turned the harbinger of wealth destruction in opposition to initially buoyant expectations of progress. The Los Angeles-based firm is down by 88% over the past 12 months and has fallen 54% in 2023 alone. The decline has been relentless, led by an unprofitable enterprise that has turn into solely at odds with the present market risk-off sentiment. Bears, who type the 12% brief curiosity, have a Chapter 11 submitting in view as Chicken faces a dearth of liquidity and consecutive quarters of excessive money burn that has left it with a few quarters of money runway as of the top of its fiscal 2023 first quarter. To be clear right here, Chicken is hurtling in direction of a chapter submitting and its frequent shares needs to be averted.

Knowledge by YCharts

While Chicken simply initiated a 25-for-1 reverse inventory break up to keep up compliance with NYSE minimal itemizing guidelines, the corporate has been hit with one other non-compliance discover with its present market cap at $30 million being beneath the requirement for a $50 million market cap. This varieties a core danger for present shareholders as a reverse inventory break up doesn’t enhance market cap so the one near-term treatment to regain compliance would both be a basic led rally or a broader inventory market rally that the corporate’s commons are in a position to take part in. With the market pricing in a roughly 75% likelihood of the FOMC pausing charge hikes at their June 14th assembly, Chicken may very well be handed an eleventh-hour salvo in opposition to its shares being moved to over-the-counter buying and selling.

Price Cuts Are Aggressive However Do not Go Far Sufficient

Chicken’s fiscal 2023 first-quarter earnings noticed income are available in at $29.5 million, a 16.5% decline over its year-ago comp and a miss by $33.95 million on consensus estimates. There was a drop in income throughout all their income phase with revenues from sharing seeing a $1.66 million drop year-over-year and with product gross sales collapsing by 92.6% over the identical timeframe following the corporate’s choice to exit their retail enterprise final 12 months. This exit positively impacted gross revenue margins which got here in at $5 million throughout the first quarter, up from simply $820,000 within the year-ago comp. Critically, while Chicken was in a position to understand a 20.5% discount in the price of sharing versus the 16.5% decline in sharing income, the exit from their retail enterprise did the heavy lifting for gross revenue margins coming in at 17.2% throughout the first quarter.

Chicken World Fiscal 2023 First Quarter 10-Q

Chicken has been aggressive in reducing again its operational price base. Basic and administrative bills fell to $31.6 million from $84.6 million within the year-ago interval with the corporate additionally decreasing its promoting and advertising bills by 61.7% and reducing again on R&D by $3.5 million throughout the first quarter versus the year-ago comp. These mixed initiatives noticed complete working bills fall by round 60% to $40.55 million from $100.2 million. Nevertheless, it was not sufficient with internet loss coming in at $44.Three million throughout the first quarter, round 150% of income and 148% of the corporate’s present market cap.

Requiem For A Very 21st Century Mode Of Transport

A Chapter 11 submitting is a comparatively easy affair and is without doubt one of the choices out there to firms whose liabilities and obligations are in extra of what their enterprise can meet. Chicken’s money burn from operations got here in at $21.7 million throughout the first quarter, down from $42.6 million within the year-ago comp however nonetheless at an extreme and unsustainable stage. For some context, the corporate’s money and equivalents together with restricted money on the finish of the primary quarter stood at $18.Three million.

Critically, Chicken’s money place in opposition to its present money burn profile leaves the corporate with a brief money runway. In fact, the scenario is fluid and Chicken remains to be taking aggressive steps to scale back its money burn so future quarters ought to see a decreased charge of outflows. Bears also needs to watch out with Chicken guiding for constructive free money flows by the top of fiscal 2023 with a goal of decreasing its general working bills to a ceiling of $100 million by means of 2023, down from $290.2 million in 2022. The corporate’s administration can be bullish and bought round 1.5 million shares in Could, highlighting what they thought was a mismatch between the corporate’s present valuation and their constructive free money stream steering. On a full-year foundation, Chicken now thinks it will probably generate constructive free money stream within the vary of $5 million to $10 million.

Nevertheless, I might be skeptical about investing based mostly on this steering. Turning the present money burn to constructive money flows will probably be troublesome in opposition to a tepid money place. Shares are to be averted with a complete debt place of $110.eight million as of the top of the quarter being a excessive mountain to climb for an organization nonetheless dropping such massive sums even after aggressive price cuts.

Editor’s Be aware: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.

Writer’s Notice: This text was printed to iREIT on Alpha in Mid-Might of 2023.

Expensive subscribers,

Safehold (NYSE:SAFE) is an fascinating REIT. We very not too long ago had an replace article by Brad Thomas concerning the firm, which you will discover right here. He showcased his numerous returns over totally different durations of time – constructive from 2018, destructive since 2021, and considerably constructive, although underperforming, since April of 2023.

My very own final piece on SAFE was printed again in October of final yr. I’ve a modest place within the enterprise, and I am going to clarify to you right here why I am shopping for extra – some comparable causes to Brad, but in addition another concerns.

Let’s get going.

SAFE stays fantastically secure – here is why and why I am at a “BUY”

SAFE is not the simplest REIT to know and requires some in-depth studying earlier than you understand what to anticipate and what the corporate does.

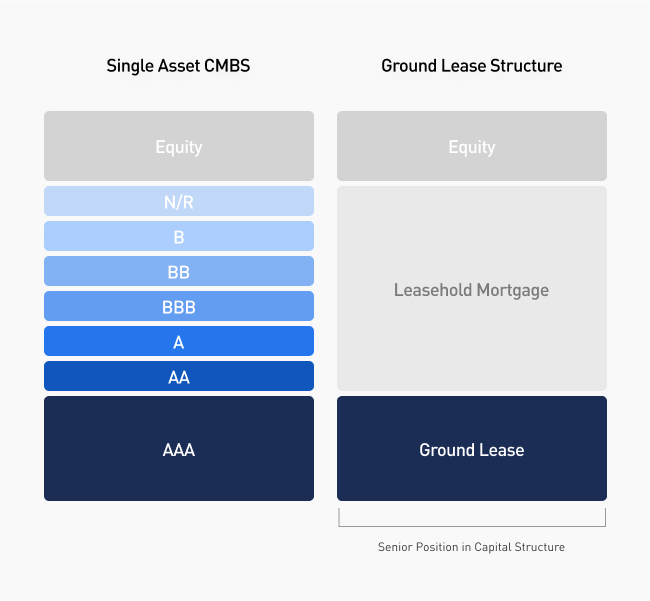

It is a “Land lease REIT”. Not lots of them on the market, however that is what Safehold does and the enterprise it is in. SAFE is New York-based, it is externally managed (extra on that later), and comes with an fascinating enterprise thought. It is the one public floor lease firm obtainable presently, and it focuses strictly on investment-grade floor lease firms, so as to improve its security and handle solely an institutional quality-level portfolio.

So what precisely is a Land-lease REIT?

The corporate acquires, manages, and capitalizes on floor leases. On this enterprise thought, the tenants personal their buildings, however not the land that the constructing is constructed upon. The lease entails undeveloped business land that in flip is leased to tenants, given the precise to develop the property during the lease.

A superb instance of an organization that makes use of floor leases is Macy’s (M). The corporate’s buildings are owned by Macy’s, together with issues like parking, however the tenant nonetheless pays lease on the land.

Structurally and organizationally, a floor lease is similar to every other type of lease. The tenant makes month-to-month lease funds. With a floor lease REIT like Safehold, the leases are internet leases, which signifies that tenants assume duty for taxes, insurance coverage, and CapEx/OpEx during the lease.

It would not take a lot explaining past this as to why that is a pretty enterprise mannequin. The corporate, in contrast to many different REITs in places of work, residences, or different segments, additionally would not maintain any huge overexposure to anyone space.

SAFE IR (SAFE IR)

The enhancements that could possibly be made contain extra publicity to sunbelt and central – however apart from that, that is a pretty mannequin.

The enchantment of the mannequin for the tenant is that it would not require the corporate leasing the land to place up huge quantities of capital for the land itself. As a result of these leases include very lengthy leasing phrases – not unusual to see over 50 years right here – it allows firms to primarily optimize their capital combine by not having to make use of vital quantities of its personal capital or debt to develop – whereas the homeowners of the lands, the REIT, get vital and long-term security from recurring lease checks. They get a long time’ value of earnings safety and may ultimately, often means off sooner or later, gather a lump sum fee for the property.

The tenant may also get entry to land that they in any other case would don’t have any entry to. That is why the mannequin is utilized by retail tenants comparable to Macy’s, but in addition McDonald’s (MCD) and Starbucks (SBUX).

I am going extra into the varied lease sorts and why landlords need unsubordinated versus subordinated leases from their tenants. However that’s how floor leases work, and why they’re engaging. And Safehold has been rising massively.

Over the previous few quarters, Safehold has been managing fairly properly. The quarterly outcomes ought to be taken with a justifiable share of salt, as a result of present prices of the incoming merger with iStar, inc.

There appear to be two methods to view this play. One facet, the extra bearish facet, views SAFE as uncovered to what are primarily Workplace-type properties in an actual property bubble/atmosphere that’s not conducive to places of work, as we have seen from the valuations for Workplace REITs. They are saying regardless of the corporate declining considerably in value, this firm shouldn’t be going wherever close to an upside, and the corporate’s elevated publicity to floating-rate debt together with its merger makes the whole play an unappetizing potential.

On the opposite facet, extra a constructive notice, say (and level out) that SAFE lacks the fairness threat of managing actual property – it is a capital supplier with none precise property obligations, making the comparability to an Workplace-type firm or REIT fully moot. Whereas the leases it holds could possibly be stated to be beforehand particular to places of work, it would not dictate that places of work must be constructed there.

Moreover, any debt threat must be put within the context of its maturities – and these are among the longest within the business, at a debt-to-book fairness of beneath 2x and a complete debt to Fairness market cap of beneath 2.5x. The common maturities listed here are over 22 years, and no maturities coming due till 2026.

So, as is considerably typical with me, I say that the pessimist is simply too pessimistic, and the unbridled optimism is simply too optimistic. The reality is, as I see it, someplace in between.

Over the previous couple of quarters, SAFE earnings have been beneath the forecasted price. 1Q got here in at ~80% decrease YoY, however after all, this was largely because of merger prices, which we will internet out. Apart from these, the earnings decline was largely a product of accelerating publicity to floating charges and debt load.

Anybody investing in SAFE wants to concentrate on what occurs when financing prices change because of rate of interest adjustments, no matter lengthy maturities, both because of float publicity or because of refis. That is sure to supply some downward stress in earnings, each GAAP and FFO, that might see the corporate go even decrease right here.

Whereas I will not declare that I foresaw the precise nature of this again 1-2 years in the past once I acquired my eyes opened to SAFE, I did see the danger in rates of interest, and this triggered me to remain out of the inventory till it fell beneath $26/share. The bubble we noticed in 2020-2022, which ended when SAFE fell from grace and from a share value of over $60/share was by no means one thing I noticed as sustainable.

Nonetheless, claiming in the identical vein that the corporate’s present debt combine/composition is untenable and can trigger a downfall goes too far. The argument is being made as a result of near-billion in debt that SAFE has placed on an unsecured revolver – not sometimes the ability you’d need to use for that quantity as a result of rate of interest value of such an answer. These current strikes have left the corporate a bit cash-strapped and with rates of interest going up. We’re seeing notes at over 5%, and yet one more $100M revolver at LIBOR + 1.5%, which is important on this atmosphere. LIBOR was properly beneath 3% a yr in the past, and the corporate’s curiosity funds are actually over 6% on common for that barely north of $1B.

If a criticism could be levied on the analysts following SAFE and their forecasts from march-April 2022, is that they anticipated rates of interest to remain the identical, and fully didn’t forecast this huge delta in debt-related funds.

The present rate of interest atmosphere additionally signifies that something the corporate tries to do on the debt combine/finance facet goes to be influenced by present market circumstances. There aren’t any “good” or “straightforward” hedges to get out of this case, comparable to floating to fastened swaps or some refinancings. The dangers financiers take will come at a price, and that leaves me with the next expectation for earnings for the subsequent few years – that they will not be massively rising.

On the identical time, the bearish facet takes far too destructive a view and infrequently forgets what the corporate has truly achieved – and the way it operates – such because the essential variations in its principal security.

Safehold IR (Safehold IR)

The corporate’s working mannequin entails an AAA-like place within the capital construction, nearly immune from the forms of dangers you see in single-asset CMBS. Even with contractual inflation captures, the corporate’s inflation-adjusted yield is over 6% at 3% long-term inflation.

Bears additionally neglect, or underestimate (in our opinion) the worth of the CARET construction and the worth it provides – each when it comes to monetization and different considerations. For these unfamiliar with it, the CARET program is an innovation when it comes to making an attempt to worth future cap appreciation, with CARET unit reflecting unrealized capital appreciation the corporate expects to obtain as soon as leases terminate or expire.

Who would need to purchase these, it’s possible you’ll ask?

Clearly, loads of educated traders, on condition that 3% have been bought to institutional traders, comparable to sovereign wealth funds and household places of work that are identified to spend money on long-term stable progress and security potential. These holders are entitled to take part in any proceeds above the fee foundation as soon as property are bought.

The maybe largest “drawback” I see when it comes to threat is the focus of its land portfolio to Manhattan, which nonetheless makes up round 24% of the corporate’s gross guide worth or GBV. SAFE has been diversifying right here, however it nonetheless has lots of work to do so as to discover worth in areas that I’d contemplate to be “engaging” relative to considerably riskier west and east-coast areas.

Bears additionally characterize the corporate as an workplace landholder – that is false. 44% is Workplace, however multifamily is over 35%. This makes the corporate a diversified holder with a tilt towards Workplace.

The corporate’s sturdy fundamentals, together with its BBB+, give a very totally different image than among the bears telling us to not spend money on the corporate wish to convey. They’re additionally rated in a different way than a REIT, which can be not coated in among the bearish stories.

Let’s take a look at valuation.

Safehold – The valuation could be very tough

Every time somebody says “Properly, this firm cannot be measured historically“, I are likely to take about nineteen steps again.

Usually, I actually do not belief any enterprise that claims that so as to worth it “correctly”, you need to do X and Y.

Why? As a result of there are 100 engaging funding alternatives that don’t require us to take distinctive approaches to one thing so simple as a valuation for a enterprise.

So, perceive that once I say this firm is engaging and could be purchased, it comes with a sure threat profile that can be thought-about in a different way than your conventional firms – and by totally different, I imply increased in some methods.

With regards to SAFE, there’s some sound reasoning behind why it would want some variations when it comes to its metrics – and among the ones are talked about above. The corporate’s debt is sky-high – over 12.5x internet debt/EBITDA. However on the identical time, SAFE has no obligations to its properties within the type of CapEx. The idea is that when that extraordinarily long-maturity debt comes due in over 25-30 years, the compounding nature of its money flows could have finished wonders. It is not a improper assumption to have both.

In an effort to see the protection, you want solely take a look at what the corporate has finished already to enhance its metric. Again 5 years in the past, the payout was 90%+ of internet. That’s now lower than 35% of internet at a yield of virtually 5%.

Publish the merger, and given its difficult peer state of affairs (no different direct friends exist), evaluating this firm is maybe the toughest a part of this text and of wanting on the firm.

We are able to take a look at some analyst estimates. With regards to S&P World, estimates right here put the corporate at round $24-$25/share on common, however given the low protection, I are likely to ascribe this to a lack of knowledge of the corporate’s earnings potential and upside.

That’s not to say that I anticipate SAFE to return to $60/share or wherever near it, at the very least not within the close to time period. With the current internalization of its administration and the method is at present in, coupled with the near-zero years of precise publicly-traded historical past, I are likely to say that SAFE is tough to conservatively forecast expectations from – however a 13-16x P/FFO price, coming to a 2025E of round $29-$33/share appears the baseline minimal of what I’d anticipate from the corporate right here.

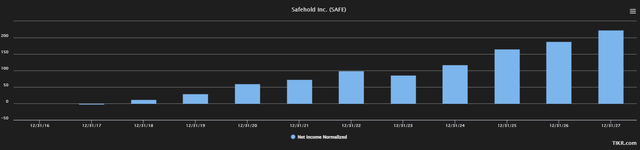

After I final wrote concerning the firm, we had been at lower than $26/share, which I considered as fairly engaging with a possible long-term upside within the triple digits. I nonetheless view this as being totally attainable. And I’m removed from alone on this. Right here is the anticipated internet earnings progress past the 2023E dip.

TIKR.com SAFE forecast (TIKR.com)

And you may see the identical developments in different measures – be it income, EBITDA, EBIT, EBT – supplier’s alternative, it is forecasted to rise. The curiosity expense I discussed, that is anticipated to remain at or concerning the degree it at present is, anticipating administration to type it out at or barely above the degrees we’re at present at, with rising bills as the corporate grows. (Supply: S&P World)

If this seems to be the case, then I consider this to be a catalyst for additional upside. Many analysts have very constructive targets for the enterprise – upwards of $50/share. If sure optimistic views materialize, that is totally attainable. However I are likely to view this with a wholesome dose of skepticism and would common it out to a PT of round $32/share, which might nonetheless be a double-digit upside from present ranges.

One other argument, and one well-covered in Brad’s current article, is insider data and CEO information.

Coupling all of this, I see a little bit of threat and maybe not as unerringly a powerful purchase as for another qualitative REITs on the market – however I undoubtedly see an upside to the corporate.

My place in SAFE is not huge – however it’s within the inexperienced, and I am open to increasing it right here.

I am at a “BUY”, and I give it a present PT of $32/share.

Recent off the presses, 3M Firm (NYSE:MMM), simply bought some constructive information concerning their PFAS case:

3M’s inventory jumped greater than 10% on Friday morning after Bloomberg Information reported the corporate agreed to a tentative settlement of at the least $10 billion with a wide range of U.S. cities and cities to resolve water air pollution claims tied to “perpetually chemical compounds.”

To be truthful, the replace from the courtroom pundits additionally goes on to level out that extra prices needs to be within the pipeline concerning this case. Additionally it is not inclusive of the earplug case, which is ongoing. 3M Firm is a dividend king and one of the vital steady cash-flowing corporations within the DJIA exterior of their unknown litigation prices. Let’s check out how low cost MMM inventory is perhaps after deducting some litigation value assumptions mixed with the exit of 3M’s PFAS enterprise come 2025.

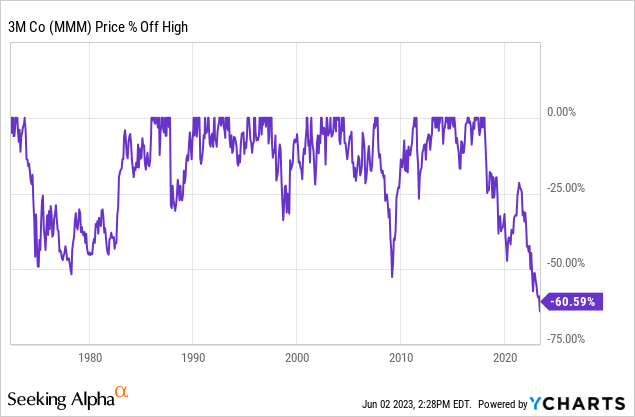

The chart

Knowledge by YCharts

60% down might imply plenty of positive aspects forward ought to 3M resolve its litigation points. This Dow blue chip is at the moment buying and selling at a market cap of solely $52 Billion.

What they do

From the 10-Ok:

3M is a diversified expertise firm with a world presence within the following companies: Security and Industrial; Transportation and Electronics; Well being Care; and Client. 3M is among the many main producers of merchandise for lots of the markets it serves. Most 3M merchandise contain experience in product growth, manufacturing and advertising, and are topic to competitors from merchandise manufactured and offered by different technologically oriented corporations.

Valuation mannequin

I will be looking at 3M at the moment utilizing a Buffett proprietor earnings discounting mannequin. This mannequin is a novel discounting methodology that hunts for high quality shares which have an equilibrium between Depreciation and Amortization versus their CAPEX. When administration is operating effectively, the big capital outlays come to start with and it should not take tons of additional capital to take a position and maintain worthwhile thereafter.

You would be stunned what number of corporations have capital expenditures far in extra of depreciation and amortization. That is the other of a well-run enterprise. We should always say such a enterprise is extremely aggressive and has a low to no moat nature. Dividend aristocrats and kings are likely to exhibit a really shut equilibrium between the 2 aforementioned gadgets and a moat due to this.

Litigation prices

Firstly, this evaluation cannot be as easy as punching within the numbers on the guidelines. I will make a possibly not-so-conservative assumption right here and assume that there are $30 Billion in litigation prices to hold ahead. Let’s view what occurred with the latest Johnson & Johnson (JNJ) case to see how the construction of the funds is laid out:

Johnson & Johnson mentioned on Tuesday that it had agreed to pay $8.9 billion to tens of 1000’s of people that claimed the corporate’s talcum powder merchandise triggered most cancers, a proposal that attorneys for the plaintiffs referred to as a “important victory” in a authorized struggle that has lasted greater than a decade.

The proposed settlement could be paid out over 25 years by means of a subsidiary, which filed for chapter to allow the $8.9 billion belief, Johnson & Johnson mentioned in a courtroom submitting. If a chapter courtroom approves it, the settlement will resolve all present and future claims involving Johnson & Johnson merchandise that comprise talc, akin to child powder, the corporate mentioned.

Principally, a belief is about up for the payout to happen over 25 years. I’d assume one thing related right here. With that in thoughts, $30 Billion over 25 years could be a litigation value of $1.2 Billion a yr.

PFAS 2025 Exit

One other deduction we have now to place into our mannequin is the PFAS exit. The corporate plans to exit the enterprise utterly by 2025, here’s what the enterprise was bringing in in accordance with 3M Firm:

Web gross sales of $1.three Billion

EBITDA margin of 16%

Equal to $208 million in EBITDA

A $163.32 Million a yr loss in web earnings assuming an EBITDA to Web Revenue conversion of 79.7%. 79.7% is the newest EBITDA to Web Revenue conversion fee for 3M Firm.

Modified proprietor earnings

Now that we have now our deductions to penalize 3M firm for, let’s run the mannequin:

Knowledge courtesy of In search of Alpha

TTM web earnings is $5.45 Billion

Plus TTM depreciation and amortization of $1.838 Billion

Minus $1.Eight Billion TTM CAPEX

Minus $1.2 Billion litigation value/yr

Minus $163.32 million in PFAS enterprise earnings

Equals proprietor earnings of $4.127 Billion

Discounted by risk-free fee of the 10-year treasury, March 2nd, 2023, of three.6% = $114.657 Billion truthful market cap

Discounted at a brief risk-free fee of 5%, $82.55 Billion.

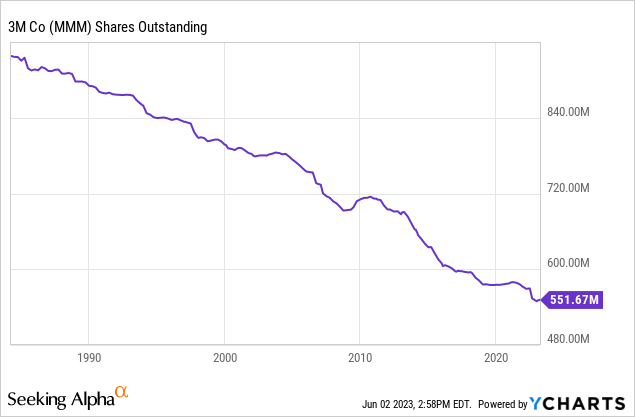

Buffett discounted stabilized companies akin to these on the 10-year treasury fee. I baked in a excessive and a low-end market cap based mostly on the lengthy and brief ends of the risk-free yield curves. Mixing the 2 will get a good market cap of $98 Billion. There are 551.672 million shares excellent as of June, 2nd 2023. This will get us to a good worth of $177.64 a share based mostly on these assumptions.

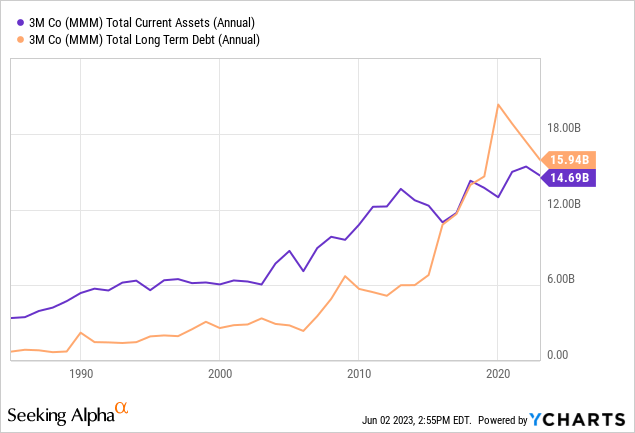

The stability sheet

Knowledge by YCharts

Long run debt and present belongings are about in equilibrium right here. Not the very best stability sheet however not a poor one both.

Knowledge by YCharts

The development in shares excellent is excellent. This firm is aware of give again to its shareholders and continues to take action. That is how you purchase again beneath intrinsic worth.

Knowledge by YCharts

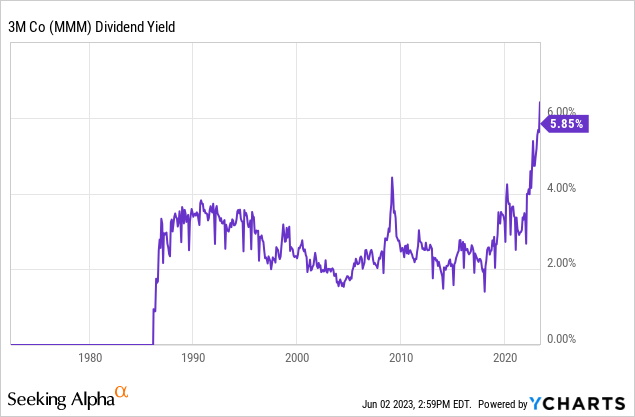

Lastly, the yield. Buyers proper now in 2023 have by no means seen a greater dividend yield on 3M Firm. The market is risk-off on them proper now, however that is historical past within the making. Is Mr. Market proper or fallacious? Even a 33% dividend minimize would go away us close to traditionally excessive ranges.

The dividend and free money stream

To be truthful, the dividend is roofed by earnings however marginally lined by free money stream.

looking for alpha

With a $6 per share dividend and a TTM free money stream of $7.23, that is a payout ratio of 82%. I am assuming buybacks should be curbed sooner or later to take care of the dividend king standing and protect capital. The dividends are extra necessary than the buybacks to protect the share worth and the moniker.

Catalysts

Extra revelations across the precise prices of litigation. Plain and easy, we’re up almost 10% after discovering out that a part of the litigation could possibly be capped at $10 Billion. I am baking in $30 Billion to my equation, some have been floating numbers above $100 Billion only for the PFAS portion alone. You by no means know the place this may wind up. Not less than the market has been ready for the worst for fairly a while.

Conclusion

I’ve began shopping for once more. I used to be merely holding my shares on DRIP for the higher a part of a yr. I, like most, have been ready to listen to any revelations within the 3M courtroom case. $10 Billion feels like lots, with extra to return, however at the least we’re getting some rational judgments. That is mixed with the truth that any payout is possible to be paid over a few years fairly than a lump sum. I am shopping for cautiously right here and my large dividend on DRIP is doing the remainder of my DCA.

WeWork Inc. bonds have been sinking deeper into distressed territory after two high executives left the corporate on the heels of a posh debt restructuring.

WeWork’s roughly $163 million of seven.875% bonds due Might 2025 had been buying and selling arms at about 45 cents on the greenback on Thursday, down from about 55 cents in mid-Might, in response to BondCliQ knowledge.

That’s Nvidia Chief Government Jensen Huang, who stated he sees the potential for “monumental injury” to U.S. corporations if the chip conflict with China escalates.

He made the feedback in a latest interview with the Monetary Occasions, cautioning lawmakers to consider the implications of additional Chinese language commerce restrictions.

Cloudflare’s (NYSE:NET) inventory reacted negatively to first quarter earnings, which have been pretty disappointing. The inventory has since largely recovered, which may point out religion within the long-term potential of the enterprise or over enthusiasm for tech shares usually on the again of AI hype. Cloudflare has a singular enterprise that has the potential to do nicely over a multi-decade interval, however there are additionally near-term headwinds which may worsen.

Market

Cloudflare noticed a cloth lengthening of gross sales cycles in the course of the first quarter, and a big decline in shut charges, regardless of win charges remaining sturdy. What is just not actually clear, at this stage, is how a lot of Cloudflare’s development deceleration is because of firm particular go-to-market points and the way a lot is said to broader market points.

Trying on the outcomes of Test Level (CHKP), CDW (CDW) and AWS (AMZN); a broad market slowdown seems seemingly. This might not likely be stunning given the turmoil attributable to SVB’s chapter. Any evaluation is at present sophisticated by restricted information and differing product and buyer exposures between firms.

The enterprise atmosphere reportedly deteriorated considerably in March, because the macro outlook grew to become extra unsure and banking points got here to gentle. Cloudflare’s administration acknowledged that this brought about a lengthening of gross sales cycles, delays in collections and a closely back-end weighted quarter. Nearly half of Cloudflare’s new enterprise closed within the final two weeks of the quarter, which is uncommon for Cloudflare. This implies the primary quarter may probably have been a lot worse, and likewise raises the specter of discounting getting used to incentivize deal closures.

Cloudflare

From a product perspective, there appears to be little doubt about Cloudflare. The corporate continues to innovate quickly and introduce merchandise which have the potential to be best-in-class.

There are actually 4.92 million Staff functions operating on Cloudflare’s platform, up 146% during the last six months. Roughly 30,000 paying prospects are using R2, storing over seven petabytes of knowledge, up 25% QoQ. These figures point out rising adoption of Cloudflare’s edge compute platform, albeit off a small base. Whereas Cloudflare’s SASE product is but to essentially acquire traction in business analyst assessments, the consensus appears to be that from a technical perspective, it is going to seemingly find yourself being among the best merchandise in the marketplace.

Doubts round Cloudflare at present middle on the corporate’s gross sales perform, and the success of Cloudflare’s shift up market. Cloudflare has traditionally been a product led firm with a predominantly self-serve buyer base. Lengthy-term success is now depending on top-down enterprise gross sales, as the corporate’s product portfolio is changing into extra strategic for patrons.

Cloudflare has already gained roughly a 3rd of the Fortune 500, indicating some success amongst bigger organizations, however the significance of this actually is determined by the providers that these prospects have adopted. Cloudflare must show that giant organizations are keen to belief the corporate as a strategic accomplice and standardize their infrastructure (safety, supply and compute) on Cloudflare’s platform.

Cloudflare’s present struggles additionally have to be seen in gentle of the conduct of opponents. Zscaler (ZS) and Palo Alto (PANW) are each well-resourced and extra mature organizations which might be defending their core markets aggressively. Palo Alto has been utilizing the massive amount of money on its steadiness sheet to finance prospects. This is a bonus that Palo Alto has as a bigger and extra mature safety vendor, however it additionally raises questions in regards to the extent to which it is ready to win offers based mostly solely on the deserves of its merchandise. Zscaler’s CEO has famous that there’s pricing stress available in the market on account of macroeconomic situations, and there have been recommendations that Zscaler is being extra aggressive with free trials to win prospects. The significance of this isn’t actually clear, although, as community safety is just not one thing the place the worth is the first deciding issue.

Cloudflare’s administration has acknowledged that prime gross sales folks have solely seen round a 1% lower in productiveness, probably indicating that present issues are associated to personnel/processes, fairly than product. There has additionally been a suggestion that previous product adoption has been pushed by the efficacy of Cloudflare’s merchandise fairly than the competence of the gross sales group. Now that Cloudflare is promoting merchandise in additional aggressive markets and that demand is mushy, among the salesforce is underperforming.

Monetary Evaluation

Whereas Cloudflare is going through robust macro situations and income development has decelerated meaningfully previously few quarters, the corporate’s pipeline stays sturdy, exceeding the plan for the second quarter in a row. Whereas Cloudflare’s incapacity to transform pipeline into income is considerably regarding, there do not at present look like any main firm particular points. Win charges towards competitors reportedly stay at document excessive ranges, and renewal charges have been regular.

Cloudflare’s common gross sales cycle in the course of the first quarter was 27% longer than the common of the earlier 4 quarters. Gross sales cycles elevated most importantly in growth offers, which have been 49% longer than the common of the earlier 4 quarters. Know-how, e-commerce and monetary providers are Cloudflare’s largest finish buyer verticals by income, and weak point inside these industries is probably going no less than partly liable for Cloudflare’s efficiency.

Cloudflare is now solely guiding for 30% income development within the second quarter, which is probably going largely why the market reacted so negatively to earnings. Whether or not this represents the trough stays unclear, however buyers ought to most likely brace themselves for additional points, notably if the macro atmosphere continues to deteriorate.

Determine 1: Cloudflare Income Development (Supply: Created by creator utilizing information from Cloudflare)

Buyer additions remained moderately sturdy within the first quarter, though giant buyer development has fallen off considerably over the previous 12 months. Massive buyer development is a vital metric given Cloudflare’s tried shift up market. Cloudflare’s dollar-based internet retention additionally fell to 117% within the first quarter, highlighting the slowdown in growth from current prospects.

Determine 2: Cloudflare Prospects (Supply: Created by creator utilizing information from Cloudflare)

The variety of job openings mentioning Cloudflare within the job necessities rebounded within the early a part of 2023 and has stabilized in latest weeks. This would seem to help Cloudflare’s sturdy pipeline and continued buyer development.

Determine 3: Job Openings Mentioning Cloudflare within the Job Necessities (Supply: Revealera.com)

Search curiosity for “Cloudflare Pricing” continues to show power. The significance of this isn’t clear, however it seems to align with hiring information.

Determine 4: “Cloudflare Pricing” Search Curiosity (Supply: Created by creator utilizing information from Google Developments)

Whereas development has disenchanted to the draw back in latest quarters, Cloudflare continues to enhance its margins. The burden of working bills is declining, despite the fact that Cloudflare continues to put money into product improvement and buyer acquisition. The corporate continues to be effectively managed and needs to be extremely worthwhile at scale, though investor consideration is more likely to be on development within the brief run.

Determine 5: Cloudflare Working Bills (Supply: Created by creator utilizing information from Cloudflare)

Cloudflare had roughly 3,390 staff on the finish of the primary quarter, a 23% enhance YoY. Job openings at Cloudflare have fallen sharply in latest weeks, which is a damaging indicator on condition that administration has acknowledged that it could rent based mostly on market situations in 2023.

The Cloudflare story is at present considerably complicated. The corporate has a gorgeous product portfolio that continues to broaden, however it isn’t clear that buyer adoption is the place it needs to be. Numerous metrics counsel an ongoing slowdown in development going ahead, however the demand image does not seem as weak as what administration has guided to.

The reason of the corporate’s present points can be questionable. Attributing issues to SVB does not actually make sense, on condition that this occurred in direction of the top of the quarter. Teething points with Cloudflare’s shift up market mustn’t have been sudden. The significance of it will rely on if and when Cloudflare can tackle the issues with its go-to-market movement.

Given these uncertainties, the latest enhance in Cloudflare’s share value seems unwarranted. The corporate has monumental long-term potential, however it might be in for a few tough years. Paying excessive multiples for a inventory is a dangerous proposition at the perfect of instances, not to mention when fundamentals are deteriorating and macro uncertainty is excessive.

Determine 7: Cloudflare Relative Valuation (Supply: Created by creator utilizing information from Searching for Alpha)

Pay attention on the go! Subscribe to The Hashish Investing Podcast onApple PodcastsorSpotify.

2:50 – 420 Investor’s origin story

8:30 – Hashish investing timeline – now is just not essentially the time for everyone to purchase hashish shares

17:50 – Ayr’s (OTCQX:AYRWF) debt and government adjustments

24:00 – Tangible guide worth and the way to gauge hashish shares

29:00 – Planet 13 (OTCQX:PLNHF) a enterprise that is managed properly

34:40 – Nonetheless bullish on WM Expertise (NASDAQ:MAPS)

Subscribe to 420 Investor

Transcript

Rena Sherbill: Alan, welcome again to The Hashish Investing Podcast. Thanks for taking the time on a protracted vacation weekend. Admire your time.

Alan Brochstein: I am blissful to be right here and really grateful to you for internet hosting me once more.

RS: Joyful as at all times to have you ever. It is thrilling instances for us at Looking for Alpha. You formally joined our — I may say rejoined, however joined in a brand new approach to one among our Investing Teams, 420 Investor formally launched at Looking for Alpha.

I might love to start out there, sort of share what is going on on? How does it really feel to be again locally in that means, via 420 Investor, not simply writing some articles? After which additionally perhaps share what you’ve got sort of occurring over there what you are sharing with subscribers, or what the dialogue is revolving round just a little bit.

AB: Certain. And for people who do not know me, 420 Investor goes to be 10 years previous very quickly.

RS: What?

AB: I do know. Wow, am I glad to be at Looking for Alpha. So let me inform the entire story. February of 2013, I learn at my favourite monetary portal Looking for Alpha, the place I used to be a giant contributor, a few hashish inventory. I used to be like, wow. I mentioned, wow, for 2 causes. Primary, is way as I used to be pro-cannabis, I hadn’t actually paid consideration. I did not notice that two states, Colorado and Washington had legalized.

However quantity two, holy crap, these firms are horrible. And so, I began writing on Looking for Alpha about how dangerous the publicly traded hashish shares have been. The truth is, they weren’t actually hashish shares for probably the most half. And most of these firms are gone now, and so they have been nearly all scams. I appreciated GW Pharma, however the remainder of them no.

And a number of the readers accused me of being paid off by massive alcohol or massive pharma or massive tobacco for bashing on the hashish sector. They did not actually perceive. No, I’m very professional hashish. And actually, I did not discuss it. However I had been a hashish client in faculty and after I moved to New York Metropolis. And after I acquired married in 1990, I had not used hashish in any respect. So it had been fairly a while, greater than 20 years of no hashish.

And worse than the no hashish was I did not find out about hashish, all of the medical advantages, the authorized complexity, all that. So I turned to Benzinga and I requested them, would you have an interest or would you permit me to run a cannabis-focused service? They usually mentioned, allow us to name you again. Two minutes later, they referred to as me again and mentioned, sure. And the remainder is all historical past.

So to reply your query, I’m so blissful to be at Looking for Alpha. I am not blissful, and we talked about this in February. The instances are very powerful proper now for hashish buyers and hashish firms. And no, I am not blissful about that. However I am additionally not the sort of person who’s going to inform everyone, you are going to purchase hashish shares proper now? No.

And so what am I doing at 420 Investor, lots. I am maintaining my subscribers knowledgeable. I am studying all of the filings, sharing all of the press releases on now 28 names that I carry on my focus record. And I am giving previews of their earnings experiences with one – year-end value targets, which I will change to 1 yr at mid-year. However proper now, I am specializing in year-end 2023.

I am operating two mannequin portfolios. One’s referred to as — these are straightforward to determine, one’s referred to as Beat The International Hashish Inventory Index, the place I am attempting to Beat the International Hashish Inventory Index, which is maintained by New Hashish Ventures. And that is previous. I had it underneath a unique identify at Benzinga. And I really had two mannequin portfolios, 420 Alternative and 420 High quality that have been just about the identical factor. They usually have been the very same factor, in the end, with completely different guidelines.

However – after which the brand new mannequin portfolio is known as Beat the American Hashish Operator Index Mannequin Portfolio, the place I am mainly attempting to beat that index. However I am attempting to beat (MSOS). And that is been a troublesome mannequin portfolio this yr. And the opposite one on my head of the – you already know, I am doing my job. However I inform all my subscribers, I am attempting to go down lower than different hashish shares or go up greater than them after they’re rallying. And I can not assure that you will make any cash, as a result of if hashish shares go down, it is arduous to earn money in hashish shares.

And so that is what I am doing proper now, and attempting to suppose what else. I do 10 movies every week. I am sharing 4 of them are on a weekday afternoons for the following day. After which each morning, an hour after the open, I give what’s referred to as My AM video. So 10 movies every week. And for the 9 that are not on the weekend. They’re 5 to 15 minutes, and so they’re primarily technical, however one on the weekend, I do know that a whole lot of subscribers are busy dwelling their lives, and so they do not have time to learn every part and I attempt to take that into consideration. And I attempt to be sure that not solely am I protecting the charts, which I feel are crucial, however I am additionally attempting to share valuation and information updates as properly. I feel that is all.

RS: I feel that is all. Yeah, not too many issues. Only a couple.

AB: It is a full-time job.

RS: I wager it’s. I do know that it’s. I do know that it might be 4 full-time jobs. There’s a lot to absorb. So I need to sort of decide aside just a little bit by way of the timeline of investing or whether or not or not buyers ought to get in. And that is one thing that is bandied about quite a bit in numerous circles and at numerous instances.

And lots of people that now we have on the podcast at all times sort of spotlight the truth that the timeline for hashish investing needs to be lengthy. It needs to be one thing that you are looking out on the horizon by way of when it will — the basics are going to match, sort of what it appears to be like like within the market and the costs which can be mirrored.

So how are you — I do know you mentioned that you simply’re not going to say what time it’s it, whether or not or not it is time to get into the market. However what would you say to buyers is the time? Is it — I do know you’ve got spoken a bit on this podcast and in addition not too long ago about 280E coming down and uplisting that the timing of that’s unknown. However would you level to these issues as catalysts that buyers can sort of look out for?

AB: Sure. So let me simply state clearly for our listeners. Now for my part is just not essentially the time for everyone to purchase hashish shares. I would not brief them. I do not commerce hashish shares, as I’ve defined to you up to now why. But when I have been a long-term investor, I’d acknowledge A, the hashish shares are actually low cost. B, the 2 good issues that I shared with you final time that you simply simply repeated, are the one two good issues that I can provide you with nonetheless, that are the elimination of 280E, which we will discuss extra, or the flexibility to commerce on the NASDAQ for American hashish firms, which we will discuss extra.

These are actually the 2 solely issues that proper now that I am actually centered on. And on the similar time, I used to not be so involved in regards to the debt ranges for American hashish firms, however I’m now. The market is down lots. And I am certain your listeners know this. However we’re down 21.4% year-to-date. And it is dangerous. It is not ending. It is a bear market that began in February of 2021, and right here we’re 27 months later. And it is nonetheless — we made a brand new all-time low Friday, it’s nonetheless a bear market.

And so I feel if you are going to purchase the dip, you must get the timing proper. I used to be mistaken. After my tragedy, I noticed the costs have fallen. I am like, whoa, what an excellent deal. It is a larger deal now. And so, I feel it is actually difficult for folks to see an excellent deal and to attempt to get the timing proper, when is an effective deal not going to be such an excellent deal anymore. And so, I am not seeing something proper now. And we talked final time about a number of the issues out there are technical. And the volumes stay very low, buying and selling volumes, unbelievably low.

And even when it rallies, it’s very low. And to me, proper now, it appears to be like like just about a completely retail investor base, as a result of the establishments aren’t concerned proper now, for probably the most half, is sort of out of time and out of cash. They usually’re not seeking to purchase something. And after I write an article on Looking for Alpha, I do an excellent job, for my part, and within the view of some others, of sharing each optimistic and adverse concepts. And no, if I write one thing optimistic, the inventory does not essentially go up. And if I write one thing adverse, like I did final week on Tilray (TLRY), you already know what occurs? I get whacked by the readers.

They do not accuse me of being paid off by massive alcohol, massive tobacco or massive pharma, they simply accused me of being — you possibly can learn the feedback. They make some fairly nasty… a whole lot of them get deleted, however a number of the ones that keep up are fairly nasty. And the way in which I have a look at it’s this, that the retail buyers don’t need you to say something dangerous in regards to the shares that they are means, means down on. And I do not care. I imply, I really feel dangerous for them. However I need to share an excellent long-term perspective.

And so I have been very essential of two shares particularly. We talked about them final time. And I mentioned, I do not like both of those shares. They’re down a lot since then, Cover Development (CGC) and Tilray. And if I criticize them of their article, wow, do folks get bent out of practice?

RS: Yeah. I need to get into the debt dialog. I – first, I feel we should always preserve it broad as we’re moving into it. I am to listen to your perspective on the way you suppose 280E will get taken out of the system? And what, if something, replaces it and what that appears like?

AB: Yeah. And so sadly, there isn’t any laws being launched to take 280E out. Ought to we be shocked? No. For the federal authorities, that is free cash. And there are folks on the market that suppose it is mistaken. There are politicians, however they haven’t any energy. And it will be arduous for Congress to simply make issues proper for the hashish business.

So the truth stays. Proper now the way in which the regulation is, if hashish is moved from Schedule 1, which is sort of foolish by the DEA, I imply actually foolish, we will all agree on that even, when individuals are speaking about medical hashish, they’re like 90% of the individuals are in favor of it. So it shouldn’t be Schedule 1. But when they have been to maneuver it to Schedule 2, it would not matter. The best way the regulation is written now, written then I ought to say, presently after which, if it is scheduled three or larger, then 280E goes away.

Now, as I mentioned final time, Biden has by no means confirmed himself to be a pal of the hashish business. And I feel I perceive why. I feel it has to do together with his son’s habit issues. And I do not suppose they have been associated to hashish. However he isn’t professional hashish. He did come out in December and say some issues that have been sort of professional hashish, however that authorities, underneath his management, hasn’t actually finished something. However he did recommend that the DEA ought to overview the scheduling. And so there’s a likelihood that they hear and that issues change. However I do not suppose the federal government goes to alter 280E in any other case.

The best way I function, Rena is, I am conscious of what is necessary and I look out for it. So if I see one thing that will level to 280E going away, A, I do know that how massive that’s; and B, I can very neatly talk that with my subscribers or with my readers on the proper time. However I would not be betting on that. No. However is it going to occur? I can not rule it out.

RS: Proper. I feel we have seen if we attempt to wager on any political maneuver vis-à-vis the hashish business, it is a idiot’s sort of sport.

AB: I used to be towards folks getting enthusiastic about SAFE Banking. And this has been a whole lot of instances that Congress simply handed it and the Senate hasn’t voted on it. And most not too long ago, the Senate did have a dialogue, and folks acquired all excited prematurely of that. After which they hearken to it, I suppose, and nope, they are not excited.

And I feel should you actually have a look at SAFE Banking, I feel, there are a whole lot of determined folks which can be both buyers or folks which can be paid by buyers or firms that anytime they see one thing that would perhaps probably make a distinction, they get all excited, and I simply do not perceive it.

From my view, SAFE Banking may be very truthful and will cross. Will it cross? I do not know. Will it assist Curaleaf (OTCPK:CURLF), GTI (OTCQX:GTBIF), Cresco (OTCQX:CRLBF)? No. All of them have financial institution accounts already. And I do know some folks will — they’re going to say another issues like, properly, perhaps custody will happen. Effectively, perhaps. However A, it is – it might not even cross; and B, I feel now we have time to react if it does.