Api Group Company (NYSE: APG) is predicted to drive natural income development in FY2023 because of its enterprise technique which focuses on market share features and cross-selling alternatives. Moreover, the corporate intends to reinforce its adjusted EBITDA margin by shifting its enterprise combine in direction of higher-margin providers. When contemplating the beneficial development prospects and a P/E ratio that’s decrease than historic ranges, I’m inclined to assign a “purchase” ranking to this inventory.

Elevated Regulation

The life security business operates below a framework of rules imposed by federal, state, and native authorities. Throughout the framework, the regulation adjustments together with mandated constructing codes and inspection and upkeep necessities act as a development tailwind for APG. Particularly, the Uniform Constructing Codes written by the Nationwide Hearth Safety Affiliation and the Worldwide Code Council regulate fireplace suppression and sprinkler programs.

These codes require testing, inspections, restore, and upkeep of fireside suppression and sprinkler programs which generate recurring income. With new and stringent rules imposed by the authorities, the demand for APG’s providers ought to proceed to stay wholesome within the coming years as properly.

Deferred Infrastructure Funding

A number of years of deferred investments within the infrastructure of the U.S. has created a state of affairs of ageing infrastructure programs requiring vital restore, upkeep, and retrofit providers. State and native municipalities have postponed their infrastructure spending for a few years which has resulted in the necessity to rebuild or retrofit a big portion of the U.S. infrastructure. In keeping with the essential want, the U.S. authorities has additionally handed the Infrastructure Funding and Jobs Act into legislation which incorporates $550 billion in new federal funding for America’s infrastructure. Therefore, I imagine the state of affairs of ageing U.S. infrastructure ought to end in a powerful demand setting for APG’s providers sooner or later.

Harnessing Market Share Progress and Cross-Promoting Synergies

APi Group has been centered on attaining 60% of its income from inspection, upkeep, and restore companies. To perform this, APG has carried out a go-to-market technique that prioritises the sale of inspection providers. During the last couple of years, the proficient administration of APG has efficiently expanded its inspection providers by means of market share features.

The first goal behind selling inspection providers as a precedence is to capitalize on cross-selling alternatives. It’s price noting that every greenback of inspection income sometimes interprets to roughly $3-$four of upkeep income. Contemplating the strong demand out there, I’m assured that the corporate is well-positioned to attain natural income development in FY2023 pushed by market share features and cross-selling alternatives.

Bolt-on Acquisition

Along with natural development prospects, the corporate anticipates pursuing further bolt-on acquisitions within the coming years. As of the primary quarter of FY2023, APG’s internet debt to adjusted EBITDA ratio was reported at 3.1x. Nonetheless, the corporate maintains a powerful deal with producing money and goals to achieve a focused internet leverage ratio of two.0x-2.5x by the top of FY2023. This strategic endeavour ought to improve APG’s monetary place and strengthen its steadiness sheet, offering a stable basis for pursuing additional inorganic development within the foreseeable future.

Margin Growth

Based mostly on APG’s technique, it seems fairly possible to me that the corporate ought to obtain a 13% adjusted EBITDA margin by 2025. As mentioned earlier, the corporate is actively transitioning its enterprise portfolio in direction of inspection, restore, and upkeep providers. This strategic shift is predicted to contribute to margin growth because of the increased gross margins related to inspection and repair income (10% plus increased) in comparison with different contract income.

Moreover, monitoring income affords a gross margin of 20% plus in comparison with different contract income. Contemplating APG’s constant execution of its technique, I anticipate that the corporate’s margins ought to enhance within the coming quarters as properly.

APG’s historic adjusted EBITDA margin (Firm information, BI insights)

Danger

APi Group operates in a extremely fragmented market the place it competes with different corporations starting from small unbiased corporations servicing native markets to bigger corporations servicing regional and nationwide markets. Sure of its prospects’ work is awarded by means of proposal processes on a project-by-project foundation the place the worth is commonly a big issue to win the mission. Smaller opponents could have a bonus towards the corporate over value because of their decrease prices and monetary return necessities. This dynamic has the potential to adversely have an effect on its inventory value.

Valuation and Conclusion

APi Group is presently buying and selling at 15.05x FY2023 consensus EPS estimates of $1.50 and 12.63x FY2024 consensus EPS estimates of $1.79 which is a reduction to its 5-year common P/E ratio of 16.27. Furthermore, upon comparability with the sector median of 16.0x, the corporate appears to be undervalued. Based mostly on my evaluation, I’ve recognized compelling alternatives for the corporate to attain natural development and broaden its margins within the coming future. Taking into consideration the beneficial development prospects and a P/E ratio that’s decrease than historic ranges, I like to recommend a “purchase” ranking for APG inventory.

Stormy occasions forward, or only a passing drizzle?

That is the massive query on the horizon for Kingsoft Cloud Holdings Ltd. (NASDAQ:KC, 3888.HK), which has simply reported a blended bag of quarterly outcomes that will or could not replicate a broadly reported rising worth battle in China’s cloud companies sector. The corporate’s newest earnings report exhibits its income fell 14.2% year-on-year within the first quarter, which is rarely signal for an organization in this type of high-growth sector.

However Kingsoft Cloud executives have been fast to downplay stories of a constructing worth battle in China’s extremely aggressive cloud companies sector, with CEO Zou Tao saying the stories have been “extra geared in direction of PR functions.”

“The tier gamers catalog worth reduce is definitely restricted if we simply take a detailed take a look at the particular merchandise which are included on this motion,” he stated on the corporate’s earnings name this week. “And we additionally don’t assume that it has any materials influence to the trade as of now.”

Buyers did not appear too reassured by Zou’s evaluation. Kingsoft Cloud’s New York-listed shares tumbled 15.7% within the two buying and selling days after the discharge of its newest outcomes, and have now misplaced greater than half their worth from a peak in early April. However we must also level out that the April run-up appears like an anomaly primarily based on speculative shopping for, and even after the newest sell-off the inventory remains to be up barely year-to-date.

China’s cloud companies trade may be very a lot a poster baby for the sorts of freakish issues that occur in sectors that Beijing has chosen for robust promotion, and on the similar time closes off to overseas participation. Each of these components apply on this case.

Large international names like Amazon (AMZN) and Microsoft (MSFT) are solely allowed to enter China’s profitable cloud companies enterprise by working with native companions because of the ban on overseas possession of such delicate telecoms infrastructure. In consequence, these international corporations are largely marginal gamers in China, leaving the sphere open for domination by native corporations which are typically lured by robust authorities incentives.

On this case, almost all of China’s main tech corporations have jumped on the cloud bandwagon, with numerous names from web giants Alibaba (BABA, 9988.HK), JD.com (JD, 9618.HK), Tencent (OTCPK:TCEHY, 0700.HK), and Baidu (BIDU, 9888.HK), to telecoms titans like Huawei and China Cell (CHL, 0941.HK) all providing each public and enterprise cloud companies. Alibaba, particularly, could also be attempting to spice up its market share proper now because it prepares to spin off and finally individually checklist its cloud companies unit, which is considered one of its few worthwhile divisions outdoors its core e-commerce enterprise.

Alibaba was one of many first to slash its costs, saying worth cuts of as much as 50% for a few of its companies final month. Tencent and China Cell joined the fray final week by saying their very own cuts of as much as 40% for the previous and 60% for the latter. JD.com joined in this week by saying its personal cuts to some companies.

Market share seize

Maybe it is all a PR train, as Zou indicated since many of the stories point out the cuts are just for choose packages and will solely be supplied for restricted occasions. However this type of worth battle is kind of frequent in China, particularly throughout economically sluggish occasions like we’re seeing now.

Right here, we must also level out that this worth battle actually solely dates again to April, that means any influence for Kingsoft Cloud would not present up till its second-quarter outcomes.

In that regard, the corporate appeared to point it wasn’t anticipating any huge influence simply but, forecasting its second-quarter income could be roughly flat year-on-year. Particularly, it forecast its second-quarter income would land between 1.85 billion yuan and a couple of billion yuan, which might symbolize wherever from a 3% decline on the low finish to a 5% achieve from final yr’s 1.91 billion yuan, and could be roughly flat on the midpoint of that vary.

That will be a giant enchancment from the 14.2% first-quarter decline, which noticed the corporate’s income fall to 1.86 billion yuan within the first three months of this yr from 2.17 billion yuan a yr earlier. Kingsoft Cloud attributed the decline to changing into extra selective in selecting prospects for each its public cloud companies which account for about two-thirds of its income and its enterprise companies which make up the rest.

Some cynics may say the corporate’s rising “selectiveness” could merely check with the lack of prospects who jumped ship for higher offers from its rivals. However a take a look at Kingsoft Cloud’s enhancing margins seems to indicate it’s critical about jettisoning lower-paying, much less worthwhile prospects in a bid to finally earn a revenue.

The corporate’s value of income fell by 20% through the quarter, outpacing its income decline, although its working bills really rose 30% through the interval. Nonetheless, the previous prices are a a lot bigger proportion of the corporate’s complete, and the massive decline in that space helped the corporate considerably increase its gross margin to 10.4% from 3.7% a yr earlier.

The underside line for Kingsoft Cloud is that the corporate seems to be centered on high quality over amount, particularly aiming for higher-paying prospects that may assist it to function profitably, and letting go of lower-paying ones which are merely good for market share. The issue, after all, is that even the higher-paying prospects may resolve to leap ship if they will get higher offers from huge names like Alibaba and Tencent.

Considerations that such an exodus may occur, which could pressure Kingsoft Cloud to decrease its personal costs, have been most likely an element behind the selloff within the firm’s shares following the newest outcomes announcement.

Following that selloff, Kingsoft Cloud’s inventory trades at a price-to-sales (P/S) ratio of 1.17, which is hardly what you’d count on for an organization in such a high-growth sector. Even Ming Yuan Cloud (0909.HK), which gives cloud companies to the embattled property sector, trades at the next P/S of three.24. Then once more, Kingsoft Cloud is not precisely rising today, and its income contraction might proceed for at the very least the subsequent few quarters if the current worth battle would not ease quickly.

Disclosure: None

Authentic Submit

Editor’s Be aware: The abstract bullets for this text have been chosen by In search of Alpha editors.

U.S. inventory futures have been combined after the highest Triple-A credit score scores of the U.S. have been positioned on “ranking watch detrimental” by credit score agency Fitch Scores Wednesday night, as a result of “brinkmanship” in Washington, over elevating the federal government’s borrowing restrict and the nation’s rising debt burden.

Dow futures YM00, -0.24% have been off about 66 factors, or 0.2%, close to 32,800 on Wednesday night, in line with FactSet, signaling the potential for continued stress on the blue-chip index after it closed Wednesday down for a fourth day in a row.

S&P 500 futures ES00, +0.38% have been up 0.4%, whereas these of the Nasdaq Composite NQ00, +1.38% have been up 1.4%, eventually examine.

After the U.S. reached its $31.Four trillion debt restrict in January, the Treasury has been taking “extraordinary measures” to keep away from breaching the debt ceiling, however is predicted to exhaust its choices as quickly as June 1, 2023, or the “X-date,” with money balances on the Treasury falling to $76.5 billion as of Could 23, Fitch mentioned.

“The failure to achieve a deal to lift or droop the debt restrict by the x-date can be a detrimental sign of the broader governance and willingness of the U.S. to honor its obligations in a well timed trend, which might be unlikely to be in step with a ‘AAA’ ranking,” Fitch mentioned.

Additionally, avoiding a default by minting “a trillion-dollar coin or invoking the 14th modification is unlikely to be in step with a ‘AAA’ ranking and is also topic to authorized challenges,” the ranking agency mentioned.

Associated: McCarthy addresses debt-ceiling angst: ‘I’d not, if I used to be within the markets, be afraid of something’

“As Secretary Yellen has warned for months, brinkmanship over the debt restrict does critical hurt to companies and American households, raises short-term borrowing prices for taxpayers, and threatens the credit standing of the US,” Treasury spokesperson Lily Adams mentioned Wednesday night time. “Tonight’s warning underscores the necessity for swift bipartisan motion by Congress to lift or droop the debt restrict and keep away from a manufactured disaster for our economic system.”

Whereas Fitch mentioned the probability of the U.S. failing to make full and well timed funds of its debt securities was a “very low likelihood occasion,” it might be thought-about a debt default that may lead to scores on affected securities being slashed to “D,” with different debt securities maturing within the following 30 days downgraded to “CCC.”

S&P International Scores in 2011 minimize its long-term credit score scores for the U.S. to AA+ from Triple A, after a protracted U.S. debt-ceiling struggle.

Serving to enhance Nasdaq futures was Nvidia Corp. NVDA, -0.49%, which has its shares bounce greater than 25% within the prolonged session Wednesday, after executives predicted that income would exceed the corporate’s document by greater than 30% within the present quarter.

See: Nvidia barrels towards uncommon $1 trillion valuation after placing a greenback determine on AI enhance

American Tower (NYSE:AMT) gives a sustainable dividend yield of three.3% and good dividend progress prospects, plus its valuation can be engaging, making it fairly attention-grabbing for long-term traders.

Firm Overview

American Tower is an actual property funding belief [REIT] that owns and operates telecommunications infrastructure, particularly towers associated to wi-fi and broadcast communications. Its primary enterprise is to lease antenna websites on multi-tenant towers, being one of many primary firms on this trade worldwide. Its present market worth is about $90 billion and trades on the New York Inventory Trade.

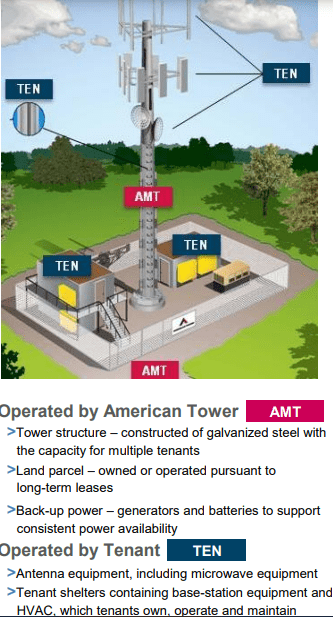

On the finish of final March, it had a portfolio of greater than 226,000 communication websites, together with greater than 43,000 properties within the U.S. and Canada, plus over 182,000 properties in the remainder of the world. Its enterprise mannequin is to personal the actual property and tower construction, whereas its tenants normally personal the remaining tower gear, as illustrated beneath.

Tower (American Tower)

Its enterprise supplies comparatively predictable and rising income, earnings, and money flows over the long run, on account of some particular traits, together with long-term leases with contractual rental escalators, excessive renewal charges, and comparatively low upkeep expenditures.

Certainly, most of its tenant leases with wi-fi carriers have preliminary intervals of 5 to 10 years, with a number of renewal phrases, plus provisions that result in lease will increase on an annual foundation, linked to inflation or fastened escalation. Given the present inflationary surroundings the world over, American Tower’s enterprise is kind of nicely protected on account of a lot of these leases, thus its working efficiency might even enhance on account of inflation, if it will probably keep a superb price management and its working bills improve at a decrease progress charge than rents.

Past having a superb hedge in opposition to inflation, its enterprise additionally enjoys optimistic working leverage, on condition that when the corporate set up a property and a tower, the prices of including further tenants are fairly low and subsequently when it’s in a position so as to add tenants to an current web site, most of incremental income flows on to its working revenue.

Geographically, American Tower has a superb diversification profile on account of its world attain, which additionally offers it good progress prospects over the long run. In the newest quarter, some 55% of its income was generated within the U.S. and Canada, whereas worldwide markets accounted for the remaining. Inside international operations, its most essential area is Latin America (accounting for some 17% of whole income), adopted by Africa (11.7%), Asia-Pacific (9.3%), and Europe (7.1%).

However, from a tenant perspective, it has rather more focus, particularly within the U.S. Certainly, its three largest tenants are T-Cell US (TMUS), AT&T (T), and Verizon (VZ), which collectively account for some 45% of whole income. Different essential tenants are additionally Airtel Africa (OTCPK:AARTY) and Telefonica (TEF), which one accounting for about 10% of whole income, which implies its prime 5 tenants symbolize about 65% of the corporate’s income.

Whereas traditionally tenants have excessive renewal charges and discovering options shouldn’t be straightforward, if a serious tenant decides to maneuver to a different tower supplier, it will probably have a major impression on American Tower’s income, which might not be straightforward to interchange because the variety of giant wi-fi operators is proscribed, particularly within the U.S.

Concerning progress, American Tower has comparatively good progress prospects supported by trade tendencies similar to growing knowledge utilization, which ought to proceed to drive telecom operators’ funding in wi-fi networks and result in extra leasing exercise for tower operators.

Moreover, it additionally has traditionally sought exterior progress via acquisitions, of which crucial previously few years was its $10 billion acquisition of CoreSite Realty, which diversified its enterprise by including knowledge facilities to its enterprise portfolio. Whereas its present technique is to prioritize steadiness sheet deleveraging, American Tower is more likely to pursue acquisitions sooner or later if the chance arises.

Furthermore, its publicity to some creating markets additionally offers it good natural progress prospects within the coming years, as smartphones penetration is decrease than in comparison with its home market and different developed areas, thus it’s anticipated stable wi-fi knowledge demand for years to return.

Monetary Overview

Concerning its monetary efficiency, American Tower has a superb observe file, reporting rising income and powerful enterprise margins over the previous few years. In 2022, because of the acquisition of CoreSite, some 7% of its income was generated by knowledge facilities, whereas the remaining got here nearly all from its tower section.

Its annual revenues within the final 12 months amounted to $10.7 billion, up by 14% YoY, of which 6.9% was associated to tenants billing progress. Its adjusted EBITDA was $6.6 billion, representing an EBITDA margin of 62%. The corporate’s internet revenue was $1.7 billion, and its adjusted funds from operations (AFFO) have been almost $4.7 billion, a rise of seven% YoY.

Throughout the first three months of 2023, American Tower maintained a optimistic working momentum, with whole income growing by 4% YoY to $2.77 billion, boosted by natural tenant billing progress of 6.4%, whereas then again foreign exchange was a headwind. Its knowledge middle section reported income progress of 10%, exhibiting that can be having fun with sturdy momentum.

Income (American Tower)

Concerning its profitability, American Tower reported an adjusted EBITDA of $1.7 billion in Q1 (margin of 63.7%), on account of sturdy price management that’s permitting some margin enlargement. Its AFFO was near $1.2 billion, a small improve in comparison with the earlier 12 months.

For the complete 12 months, American Tower’s steering is to attain property income of about $10.7 billion, up by round 3% YoY, supported by rental progress whereas foreign exchange is predicted to impression negatively income progress. Its EBITDA must be above $6.9 billion, or a 62.9% margin, whereas its AFFO is predicted to be some $4.5 billion.

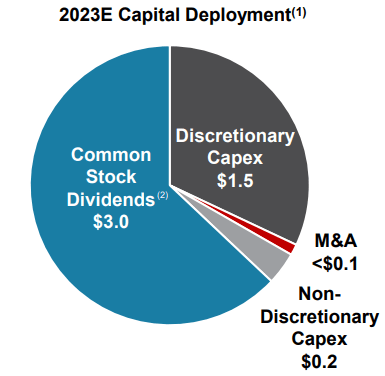

Whereas American Tower has a recurrent and extremely money generative enterprise, its monetary leverage is considerably excessive, as the corporate elevated its debt place following the acquisition of CoreSite. On the finish of final March, its internet debt-to-EBITDA ratio was 5.2x, decrease than 6.1x on the finish of 2021, however nonetheless above its long-term goal of between 3-5x. Subsequently, American Tower’s purpose within the brief time period is to deleveraging its steadiness sheet, which implies most of its natural money movement must be allotted to shareholder remuneration and capex, whereas giant acquisitions aren’t anticipated till it reduces monetary leverage to a suitable stage.

Taking this background into consideration, the corporate’s capital deployment plan for 2023 is to distribute some $Three billion to shareholders via dividends, representing an annual improve of about 10%, allocate some $1.7 billion to capex and a really small quantity to M&A.

Capital plan (American Tower)

Concerning its dividend, American Tower has an excellent historical past, delivering a rising dividend over the previous few years. Its final quarterly dividend was set at $1.56 per share, or $6.24 per share yearly, which at its present share worth results in a dividend yield of about 3.3%.

Provided that its dividend is roofed by AFFO and the corporate’s enterprise mannequin is very recurrent and predictable, plus has a superb money movement era capability, American Tower’s dividend is clearly sustainable and is more likely to keep a rising development within the close to future.

Certainly, in accordance with analysts’ estimates, its dividend is predicted to develop to about $6.45 per share this 12 months, and improve to about $7.82 per share by 2025, exhibiting that American Tower’s dividend progress prospects are fairly good supported by the corporate’s sturdy fundamentals.

Conclusion

American Tower is an organization with a stable profile, on account of its recurring income, earnings and money flows stream, being a powerful help for a sustainable dividend over the long run. Whereas its comparatively excessive monetary leverage is the primary weak issue of its funding case, I don’t see this being a menace to revenue traders as the corporate’s precedence is to cut back steadiness sheet leverage somewhat than looking for additional acquisitions.

Concerning its valuation, it’s at present buying and selling at some 19x FFO, at a reduction to its historic common of about 25x over the previous 5 years. Thus, American Tower has a sustainable dividend and in addition gives a lovely valuation in comparison with its historical past, being subsequently a superb revenue funding proper now.

Olin Company (NYSE:OLN) is a Virginia-based chemical firm with long-standing experience within the chlor-alkali area (130 years of expertise and 54% of group gross sales). A number of the firm’s chief merchandise embody caustic soda, chlorine, hydrogen, bleach merchandise, epoxy supplies, aromatics, industrial cartridges, and ammunition (each sporting and army) OLN’s merchandise are utilized primarily by industrial and business entities throughout the globe (39% of group gross sales come from outdoors the US).

We consider there is a time to pursue shares equivalent to OLN, however that point is not now. Listed below are a couple of explanation why we aren’t prepared to leap on the OLIN bandwagon at this juncture.

Cyclical impression and excessive sensitivity to broader markets

At this stage of the enterprise cycle, it’s unwise to get too cozy with commodity chemical performs, given the inherently pronounced sensitivity to international GDP. The IMF was already beforehand anticipating actual international GDP progress to say no from 3.4% in FY22 to 2.9% this 12 months, however this has been scaled down as soon as once more to 2.8% as per its most current forecast in April.

These underwhelming GDP numbers will little doubt go away a mark on chemical volumes. Statista believes that FY23 chemical volumes in necessary areas equivalent to North America (1.9% vs 2.7% in FY22) and Europe (1.6% vs 1.3% in FY23) will fail to maintain tempo with what was seen in FY22 while no area is predicted to see an enchancment in these progress charges.

Statista

On account of inauspicious industry-related situations count on strain on each the topline and working stage (based on Fitch, income progress shall be subdued at 1.6% whereas margins look poised to contract by 40bps) while monetary leverage pressures will inch up on account of weak working leverage and a decent financial coverage setting. The one factor that will keep resilient is FCF conversion, however as you will see in a while on this piece, Olin is more likely to wrestle right here as nicely.

Fitch

A weakening progress dynamic ought to weigh on the efficiency of broader markets, and it does not assist that Olin’s inventory is hyper-sensitive to the actions of the benchmarks. As you’ll be able to see from the picture under, Olin’s beta has elevated over the previous 12 months, and at present stands at an elevated studying of over 2x!

YCharts

Epoxy division considerations

Olin’s second-largest division – the division which produces epoxy supplies and precursors (~29% of group gross sales) is in a foul manner, and it will be unrealistic to count on a fast turnaround.

Demand within the American and European markets continues to be weak, and administration has additionally acknowledged that they resorted to overpricing in a few of these markets, which impacted their positioning. Notice that Chinese language producers have additionally ramped up the availability place, and since demand within the Asian markets is not resilient sufficient, one is going through an overdose of provide within the export markets.

In the event you’re affected by both of quantity or pricing challenges, Olin might maybe be higher positioned for a speedy bounce again, however once you’re hamstrung by each side of the equation, it turns into even tougher to get well. For context, out of the 54% YoY income decline of this division, 25% was from decrease volumes, and 5% was from weak pricing. FX impacts and the closure of sure models additionally left a mark. Olin is at present within the course of of creating changes to its international epoxy asset footprint and can incur extra restructuring prices linked to the closure of sure models (administration expects one other $30m of contemporary restructuring fees)

Ongoing free money circulate pressures might weigh on buyback momentum

OLN administration takes nice pleasure of their constancy in the direction of shopping for again the inventory, but when current FCF pressures had been to persist, it might put a spanner within the works. Apart from, additionally word that buyback tendencies have already been slowing over time. A 12 months in the past, the corporate was deploying round $400-$450m of money per quarter on shopping for again inventory; as of late it has halved.

YCharts

Coming again to the FCF, we are able to see that the corporate didn’t generate a constructive quantity within the March quarter (-$24m), and while weak profitability performed an element, Olin additionally did not do an important job in managing its working capital nicely sufficient.

YCharts

The money conversion cycle offers you a way of how lengthy money is tied up with working capital, and we are able to see that it just lately hit 5-year highs of 65 days within the March quarter (Olin usually retains it at lower than 50 days).

YCharts

The prime perpetrator right here was the heightened quantity of stock build-up which got here in at 64 days, a 10-year excessive, and ended up sucking out $146m of money!

YCharts

Weak market and demand situations for caustic soda, vinyl intermediates, and epoxy supplies are anticipated to linger for the foreseeable future, so do not count on a speedy decline of these heightened stock ranges. For sure, this could possibly be a drag on money technology. Money gen is also pressurized by upcoming worldwide tax funds of $50m-$100m for the corporate’s energy property within the Gulf Coast.

Underwhelming sell-side estimates for FY23 go away an antagonistic mark on ahead valuations

Olin has been incurring heavy margin strain for over a 12 months now (the picture under highlights how the EBITDA margins have been sliding on a trailing twelve-month foundation), and that’s unlikely to abate as we progress by means of this 12 months.

YCharts

As per YCharts estimates (the typical estimates of 12 sell-side analysts) group income in FY23 will hunch by-17% YoY, however the EBITDA impression shall be much more pronounced at -30% YoY (this might suggest that margins drop to 22%, virtually a 400bps YoY impression)!

Within the Q1 presentation, Olin’s administration recommended that EBITDA in FY23 could possibly be within the ballpark of $1.6-$1.9bn. Consensus at present is a bit of decrease than the mid-point of that vary, at $1.71bn. On that EBITDA quantity, the inventory at present trades at a dear ahead EV/EBITDA of 5.6x, which might represent a 20% premium over the 5-year common a number of of 4.68x. Even when we assume a drastic turnaround in H2 (which seems unlikely) with the corporate hitting the higher finish of the vary, that might nonetheless level to a dear EV/EBITDA of 5.1x, which remains to be above the long-term common.

YCharts

Unappealing technical panorama and restricted assist from establishments

If one considers the weekly value imprints of OLN over the past two years or so, we are able to see that issues have been somewhat uneven, with the inventory making giant swings throughout the $43 to $61 vary. We’re but to see any value vary the place the inventory has managed to stabilize, and thus it turns into much more pertinent to play the 2 boundaries and take positions accordingly. In that regard, if one had been to kick-start a protracted place on the present value level, the risk-reward doesn’t work in your favor. You usually wish to take positions the place the reward-risk equation is over 1x. However on the $54 stage, the equation works out to a sub-par variety of 0.84x

Investing

The opposite factor to notice is that Olin is unlikely to profit from any mean-reversion curiosity for these fishing within the supplies sector, as its relative positioning versus the Vanguard Supplies ETF remains to be fairly elevated (~48% larger than the mid-point of the long-term vary).

StockCharts

Ideally, you additionally wish to see the fellows with deep pockets, to show extra constructive in your inventory, however that theme is but to be mirrored with Olin. Each the whole variety of establishments that pursue Olin and the web shares owned by them have been sliding each single month for the reason that flip of the 12 months. For context, on a YTD foundation, the previous metric is down by 11% and the latter metric is down by 18%.

This text is devoted to our summer time interns at iREIT on Alpha, who’re all school college students and desirous to study dividend investing.

As it’s possible you’ll know, I educate steadily at many faculties and universities, lecturing on the subject of Actual Property Funding Trusts (‘REITs’) as I actually get pleasure from educating college students the advantages of proudly owning actual property in a securities wrapper.

To this point this yr I’ve lectured at Penn State, College of North Carolina, NYU, and Clemson College, and I stay up for launching my very personal REIT Masterclass this summer time when my new REITs For Dummies guide is revealed.

As I’m certain you realize, educating and investing go hand in hand, as I typically remind readers right here on Searching for Alpha, investing boils all the way down to 4 phrases: studying out of your errors.

I’ll be the first to confess, I’ve realized quite a bit over my 30+ yr investing profession, and I can guarantee you that studying curve continues to be rising. That is one such instance of the so-called “studying curve”.

supply: bumpy-learning-curve

I take into consideration my very first job of being a newspaper supply boy (I used to be 15) during which I used to be accountable for dropping off round 50 newspapers every day. As the training curve illustrates (above), it began out simple after which as soon as I obtained a number of complaints from clients (for being late or the paper was moist) it bought tougher.

However I saved pedaling and simply after I thought I had issues underneath management, I discovered “I don’t know s***” (as per the above chart). I needed to discover ways to acquire cash and guarantee that clients have been paying me. I grew to become assured and after a number of months, I used to be on the level the place I had figured all of it out.

It took a number of pace bumps and a breaking level, however I used to be in a position to overcome quite than giving up and retreating to my consolation zone. That in itself, is what investing is all about.

It takes self-discipline, arduous work, and close to failure.

Oftentimes the speed of development is sluggish in the beginning after which rises over time till full proficiency is obtained, however after all in the case of investing, I’m not sure that anybody can declare they know all of it, even Warren Buffett.

“It’s a must to continue to learn if you wish to grow to be an excellent investor. When the world modifications, you could change.”

My Massive Pivot

As I knowledgeable our new interns on their first day, I used to be an actual property developer for over 20 years during which I realized the idea of worth creation actually “from the bottom up”.

My formal introduction to the world of brick-and-mortar was hiring architects, engineers, and contractors to assemble and lease out buildings to nationwide chains corresponding to Walmart, Walgreens, Advance Auto Elements, and numerous others.

I realized the advantages in proudly owning non-public actual property and the wealth that may be created by use of leverage, native market experience, and shrewd negotiations. I constructed a substantial internet value using the identical studying curve displayed above.

Simply in regards to the time I believed I had figured all of it out… and shouted “I did it”…

…one thing depraved appeared that I had by no means seen earlier than…

…and it compelled me again down the training curve during which I mentioned to myself, “I don’t know s***.”

You guessed it…the Nice Recession.

So, I landed on Searching for Alpha (13 years in the past) and through this time I’ve grow to be one of many most-followed writers (I simply handed 110,000 followers) with over 3,600 articles to my credit score.

The educational curve didn’t begin from scratch although, I used to be in a position to make the most of the entire classes realized from a long time of actual property expertise and channel them into the REIT sector… and this contains the teachings realized through the Nice Recession.

So, as I identified, this text is devoted to our interns (that features my son) and all of these of their 20s. Nonetheless, you don’t need to cease studying right here as a result of I feel most anybody can profit from the picks on this article.

Alexandria Actual Property (ARE)

Alexandria is an actual property funding belief (“REIT”) that focuses on life science workplace properties. In contrast to the remainder of the workplace sector, ARE doesn’t face the identical challenges from the do business from home motion since they lease area to pharmaceutical firms, biotechnology firms, educational analysis, medical analysis establishments, and authorities analysis companies.

Their tenants use their amenities to conduct analysis in labs which can’t be executed from dwelling. ARE’s properties are situated in Boston, San Francisco, New York Metropolis, Seattle, San Diego, and Maryland. They’ve round 1,000 tenants and their whole actual property portfolio covers 74.6 million sq. ft.

ARE has a mean AFFO development charge of 5.56% over the previous 10 years. They pay a 4.07% dividend yield that’s effectively coated with an AFFO payout ratio of 72.17% and have elevated the dividend by 8.62% on common since 2013. ARE is at the moment buying and selling at a P/AFFO of 17.69x which is a major low cost to their regular AFFO a number of of 24.21x. At iREIT we charge ARE a STRONG BUY.

FAST Graphs

Mid-America Residence Communities (MAA)

MAA is an internally managed REIT that focuses on multifamily communities. They’ve properties in 16 states and the district of Columbia and have a robust concentrate on the sunbelt area with their prime 5 markets situated in Atlanta, Dallas, Tampa, Orlando, and Austin.

Their multifamily properties include 102,000 residence items which have an occupancy charge of 95.7% as of year-end 2022. MAA has an A- credit standing from S&P International and wonderful debt metrics with a internet debt to adjusted EBITDAre of three.5x and a long-term debt to capital ratio of 38.34%.

Moreover, their debt is 100% mounted charge and has a weighted common rate of interest of three.4%.

Since 2013 MAA has had a mean AFFO development charge of 6.42% and analysts anticipate that to proceed with projected AFFO development estimated to be 8% in 2023. MAA pays a 3.76% dividend yield that could be very safe with an AFFO payout ratio of 60.95%.

Moreover, MAA has a mean dividend development charge of 5.92% during the last 10 years. At present MAA is buying and selling at a P/AFFO of 18.87x which is barely beneath their regular AFFO a number of of 19.18x. At iREIT we charge MAA a BUY.

FAST Graphs

Realty Earnings (O)

Realty Earnings is REIT that focuses on buying retail properties which are primarily single-tenant and leased on a triple-net foundation. Their portfolio contains 12,237 properties which are in all 50 states, Spain, Italy and the UK.

Their properties embody 236.Eight million sq. ft and have an occupancy charge of 99.0% with a weighted common remaining lease time period of 9.5 years. Realty Earnings pays month-to-month dividends and has elevated the dividend for 29 consecutive years making them one of many few REITs which are a Dividend Aristocrat.

They’ve an A- credit standing and robust debt metrics together with a internet debt to professional forma adjusted EBITDAre of 5.4x and a 4.6x mounted cost protection ratio. Their debt is 90% mounted charge and has a weighted common time period to maturity of 5.9 years.

Realty Earnings pays a 5.05% dividend yield and that’s effectively coated with an AFFO payout ratio of 75.69%. Since 2013 Realty Earnings has had a mean AFFO development charge of 6.16% and a mean dividend development charge of 5.76% and are presently buying and selling effectively beneath their regular AFFO a number of.

At present Realty Earnings trades at a P/AFFO of 15.35x which is effectively beneath their regular P/AFFO a number of of 18.86x. At iREIT we charge Realty Earnings a BUY.

FAST Graphs

American Tower (AMT)

AMT is likely one of the bigger REITs with a market capitalization of roughly $89 billion. They concentrate on multitenant cell towers and different wi-fi communication infrastructure. AMT has round 226,000 international websites situated on 6 continents and in 26 nations.

Their portfolio consists of roughly 43,000 cell towers within the U.S. and Canada and greater than 181,000 worldwide towers. Moreover, AMT has 1,700 Distributed Antenna Methods and 28 knowledge facilities. Cell towers are a part of the “e-commerce trifecta” (together with logistic warehouses and knowledge facilities) as they’re a needed element for on-line retail.

AMT has a mean AFFO development charge of 11% and a mean dividend development charge of 20.70% during the last ten years. They pay a 3.09% dividend yield that’s effectively coated with an AFFO payout ratio of simply 60.04%. At present AMT is buying and selling at a P/AFFO of 20.03x which is a reduction to their regular AFFO a number of of 23.19x. At iREIT we charge AMT a BUY.

FAST Graphs

Digital Realty Belief (DLR)

Digital Realty Belief is an information middle REIT that owns or has an possession curiosity in 316 knowledge facilities situated in 28 nations and on 6 continents. DLR has a world footprint with properties within the U.S., Europe, Latin America, Africa, Asia, Australia and Canada.

Knowledge facilities are the place the cloud lives. They retailer servers which are used for digital communication and processing transactions and are one other a part of the “e-commerce trifecta”.

Primarily, as soon as an order is positioned on-line, the sign is distributed to a cell tower which then routes it to a knowledge middle the place the knowledge is gathered and arranged. As of December 31, 2022, DLR’s portfolio of knowledge facilities was roughly 84.7% leased.

Since 2013 DLR has had a mean AFFO development charge of 5.71%. Analysts anticipate AFFO development of three% in 2023 after which 6% and seven% within the years 2024 & 2025 respectively. DLR pays a 5.10% dividend yield that’s effectively coated with an AFFO payout ratio of 81.33%.

Moreover, DLR has a mean dividend development charge of 5.29% during the last 10 years. At present DLR is buying and selling at a P/AFFO of 15.76x which is effectively beneath their regular P/AFFO a number of of 19.15x At iREIT we charge DLR a STRONG BUY.

FAST Graphs

VICI Properties (VICI)

VICI is a REIT within the gaming sector that acquires gaming properties, particularly casinos, and different hospitality and leisure locations by means of sale-leasebacks which are structured on a triple-net lease foundation. Their portfolio contains trophy properties corresponding to Caesars Palace, the Venetia Resort, and MGM Grand in Las Vegas.

In whole VICI has 50 gaming properties unfold throughout 15 states and Canada that covers round 124 million sq. ft and options round 60,100 resort rooms and roughly 450 eating places, nightclubs and bars.

VICI pays a 4.95% dividend yield and that’s effectively coated with an AFFO payout ratio of 77.72%. Since 2019 VICI has had a mean AFFO development charge of 6.92% and a mean dividend development charge of 10.80%. At present VICI trades at a P/AFFO of 15.71x which compares favorably to their regular P/AFFO a number of of 16.29x. At iREIT we charge VICI a BUY.

FAST Graphs

Hannon Armstrong Sustainable (HASI)

Hannon Armstrong is an internally managed Mortgage actual property funding belief (“mREIT”) that invests in local weather options together with renewable power, power effectivity and different environmentally sustainable infrastructure tasks.

They supply capital to firms for inexperienced power tasks corresponding to solar energy technology, solar energy storage, on shore wind, and power effectivity enhancements. They primarily present capital and earn nearly all of their income from curiosity earnings, however additionally they personal properties for which they obtain rental earnings.

HASI’s emphasis on clear power is centric to their funding technique, a lot so {that a} prerequisite for them to offer capital is that the mission has to cut back carbon emissions, or be carbon impartial, or present another environmental profit corresponding to decreasing water consumption.

HASI has a mean adjusted working earnings development charge of 9.72% and a mean dividend development charge of 6.46% during the last eight years. They pay a 6.13% dividend yield that’s effectively coated with a payout ratio of 72.12% when based mostly on adjusted working earnings.

At present HASI is buying and selling at a P/E of 12.03x which is a major low cost to their regular P/E ratio of 19.06x. At iREIT we charge HASI a STRONG BUY.

FAST Graphs

Ladder Capital (LADR)

Ladder Capital is an internally managed mortgage REIT that focuses on business actual property lending. LADR originates senior first mortgage loans and variable charge loans which are collateralized by business actual property in addition to conduit loans on stabilized properties which are securitized and offered as business mortgage-backed securities.

Along with mortgage origination, LADR invests in securities which are secured by business actual property and owns business actual property that they obtain rental earnings from.

LADR has a mean adjusted working earnings development charge of -2.27% since 2016, nevertheless, analysts anticipate earnings to develop by 12% in 2023. They pay a 9.51% dividend yield that’s effectively coated with an adjusted working earnings payout ratio of 75.86%.

Their common dividend development charge is -9.79% since 2016, however they did enhance the dividend by 10% in 2022. LADR is at the moment buying and selling at a P/E of seven.97x which is a effectively beneath their regular P/E a number of of 10.33x. At iREIT we charge LADR a BUY.

FAST Graphs

Solar Communities (SUI)

Solar Communities is a REIT that focuses on manufacturing housing (“MH”), leisure car (“RV”) parks, and marinas. They’ve properties within the U.S., the UK, and Canada and have been buying, growing and working MH and RV parks since 1975, and extra not too long ago marinas in 2020.

Their portfolio consists of 669 properties that embrace 353 MH communities, 134 marinas, and 182 RV parks. Their MH communities include a complete of 118,204 developed websites, Their RV parks include 61,514 developed websites (each annual and transient), and their marinas include 47,823 moist slips and storage areas.

SUI has a mean AFFO development charge of seven.73% and a mean dividend development charge of three.43% during the last ten years. They pay a 2.91% dividend yield that could be very safe with an AFFO payout ratio of simply 55.0%.

At present SUI is buying and selling at a P/AFFO of 19.69x which is a reduction to their regular AFFO a number of of 24.12x. At iREIT we charge SUI a BUY.

FAST Graphs

Additional House Storage (EXR)

Additional House Storage is a REIT that operates and owns self-storage properties. Their portfolio contains wholly owned self-storage properties, storage properties that they’ve an possession curiosity in, and storage properties that they handle.

As of year-end 2022, EXR owned or operated 2,338 self-storage properties that include round 1.6 million items which are situated in 41 states and canopy roughly 176.1 million sq. ft.

Along with their rental earnings, EXR generates revenues by means of administration charges on the amenities they handle for third occasion house owners and revenues from their reinsurance program that insures towards the lack of items of their amenities.

EXR has a mean AFFO development charge of 13.96% and a mean dividend development charge of 22.96% during the last ten years. They pay a 4.34% dividend yield that’s effectively coated with an AFFO payout ratio of 73.98%. At present EXR is buying and selling at a P/AFFO of 18.39x which compares favorably to their regular P/AFFO a number of of 22.46x. At iREIT we charge EXR a BUY.

FAST Graphs

In Closing…

As you realize, it’s virtually not possible to eradicate all funding danger, however you possibly can scale back it by filtering out the disadvantageously positioned shares from the outset.

Through the use of elementary evaluation, our crew has been in a position to generate stable whole returns throughout our numerous portfolios. One of the crucial necessary classes realized for me is to not put all of your eggs in a single basket.

In any case, it takes only some giant losses to decimate total funding efficiency, even when many different investments show profitable.

Keep tuned for extra “classes realized” articles.

Glad SWAN Investing!

Writer’s be aware: Brad Thomas is a Wall Avenue author, which implies he isn’t all the time proper along with his predictions or suggestions. Since that additionally applies to his grammar, please excuse any typos it’s possible you’ll discover. Additionally, this text is free: Written and distributed solely to help in analysis whereas offering a discussion board for second-level pondering.

It’s all change once more within the boardroom at Chinese language e-commerce big JD.com Inc. (NASDAQ:JD; 9618.HK), barely a 12 months after founder Richard Liu stepped down from the highest job.

Liu’s successor, Xu Lei, has resigned as CEO and is transferring to a non-executive place on the advisory board, the web retailer introduced final week, citing what had been described as “private causes” for the choice. The vacated CEO submit is to be crammed by the present CFO, Sandy Xu, who turns into its third occupant in simply over a 12 months.

The manager shake-up, approaching the heels of a retail enterprise overhaul, has sparked hypothesis that Liu could also be planning an official comeback after persevering with to tug strings behind the scenes.

In its surprising announcement, which coincided with quarterly earnings, the corporate quoted the outgoing CEO as desirous to dedicate extra time to his household. The place of CFO on the e-commerce group could be crammed by Ian Shan, presently CFO of JD Logistics, Inc. (OTCPK:JDLGF; 2618.HK).

JD.com has been reorganizing its most important enterprise unit, JD Retail, in what media studies have referred to as the most important transformation in 5 years, with modifications within the enterprise construction and platform. It will seemingly take at the very least six months for the restructuring to mattress in.

Up up to now, Xu Lei had been accountable for the retail enterprise and had beforehand served as CEO of JD Retail. Due to this fact, the timing of his departure from the highest spot is puzzling the market.

Step ahead Richard Liu?

Some observers are questioning whether or not the stage is being set for Liu’s return as government chairman. The corporate founder has been busy within the wings since stepping out of the highlight a 12 months in the past amid China’s crackdown on highly effective tech firms.

He steered a number of waves of the reorganization, recognized a low-price technique as the way in which ahead for JD Retail for the following three years, and accused some colleagues of underperforming.

All this factors to deep and ongoing involvement within the day-to-day operating of the corporate. JD’s share worth jumped 7.3% the day after the administration modifications had been made public, maybe reflecting hopes of an official comeback for the JD.com founder.

A more in-depth have a look at the corporate’s quarterly outcomes, additionally introduced final Thursday, might provide clues to the explanations behind Xu Lei’s departure.

JD’s first quarter income rose simply 1.4% 12 months on 12 months to 243 billion yuan ($35.2 billion), dragged down by a 4.3% drop in product income to 195.6 billion yuan. Income from providers fared higher, leaping 34.5% to 47.Four billion yuan.

Throughout the identical interval, JD’s working revenue greater than doubled to six.Four billion yuan, from 2.Four billion yuan within the first quarter of final 12 months. As for the underside line, the corporate made a web revenue of 6.26 billion yuan, reversing a year-earlier loss. Its non-GAAP adjusted revenue, which displays precise enterprise efficiency, rose round 88% to 7.59 billion yuan.

Trying on the financial context, official figures present Chinese language gross sales of client items rose 10.6% within the first quarter from the year-earlier interval, however some segments bucked the brighter development. Family home equipment sagged 1.7%, whereas audio-visual and communication tools fell 5.1%.

JD has historically been sturdy within the house equipment enterprise. With that in thoughts, Liu might have wished to place the flagging core of the retail enterprise into the fingers of a finance skilled within the hopes of engineering a fast turnaround.

In a convention name after the outcomes, Xu Lei stated that the lifting of Covid controls had helped to revive client demand, however momentum was nonetheless missing, resulting in divergent recoveries throughout retail classes.

He stated JD Retail was flattening its administration construction to enhance agility and effectivity, leaving solely three ranges between the CEO and ground-level workers in procurement and gross sales.

Sandy Xu, who will likely be promoted to CEO subsequent month, additionally outlined deliberate modifications to the enterprise construction of JD Retail, whose procurement and gross sales groups could be divided by product class, delegating extra decision-making and administration energy and linking particular person efficiency assessments inside groups.

JD’s gross merchandise quantity (GMV) and income have each accelerated for the reason that begin of the second quarter, Sandy Xu instructed the assembly. Below its low-price technique, the corporate has invested closely in subsidy applications to help third-party retailers, hoping to shift purchasing habits and increase gross sales. In consequence, the transaction quantity at energetic retailers, consumer site visitors and repurchase charges are all steadily rising.

Whereas the low-price technique is beginning to repay, the e-commerce enterprise remains to be grappling with weak Chinese language consumption and home demand. However providers akin to well being and logistics have been outperforming gross sales of products.

Companies on the rise

Service income grew to 20% of whole gross sales within the first quarter, Sandy Xu stated, contributing to wholesome revenue margins. The promotion efforts additionally attracted a document variety of third-party retailers to the JD platform.

The primary drivers of service income had been JD Well being (6618.HK) and JD Logistics. First quarter income from the well being division rose 54% from a 12 months earlier, whereas adjusted working revenue surged 108%. Over at logistics, income jumped simply over 34% and the unit’s adjusted loss shrank 29% to 710 million yuan.

Regardless of the first rate report card for the primary quarter, JD.com’s retail efficiency was nonetheless weak, which doesn’t bode effectively for the following few quarters. The corporate’s ahead price-to-earnings (P/E) ratio is about 13 occasions, falling between the 9.Three occasions for Alibaba (BABA; 9988.HK) and 16.7 occasions for Pinduoduo (PDD), indicating a impartial stance amongst buyers.

Nonetheless, some analysts are upbeat in regards to the outlook after the most recent JD earnings beat some expectations. A Macquarie report stated the determine for adjusted income had been far stronger than anticipated, lifted by the enterprise overhaul and efforts to streamline operations.

The funding financial institution duly raised its forecast for the agency’s adjusted revenue by 8% for 2023 and 5% for subsequent 12 months. Macquarie additionally raised its goal worth from HK$205 to HK$207, whereas sustaining an “chubby” score.

Disclosure: None

Authentic Submit

Editor’s Word: The abstract bullets for this text had been chosen by Looking for Alpha editors.

The US housing market is in the midst of its sixth main downturn for the reason that late 1960s.

Residence costs are declining in 75% of main cities, with many areas posting declines for six or seven consecutive months.

On this article, we’ll have a look at the distribution of residence value declines and present the place residence costs have fallen probably the most and the place residence costs have held up the very best.

We’ll additionally examine the depth and period of this residence value downturn to declines of the previous to see the way it stacks up.

Are Residence Costs Declining In My Metropolis?

Essentially the most time-tested and dependable measure of residence costs is the Case-Shiller Residence Worth Index. The Case-Shiller Residence Worth Index tells us that residence costs on the nationwide degree have began to say no, with a peak in the summertime of 2022.

Case-Shiller

Residence costs do not usually decline in nominal phrases. Later within the article, we’ll have a look at actual or inflation-adjusted residence costs, which is a a lot better methodology for evaluating residence costs throughout historical past.

This chart exhibits that within the final 30 years, nominal residence costs have solely declined thrice. There was a 2% decline within the 1990 recession and a virtually 30% decline across the 2008 recession. Residence costs did not drop in any respect within the 2001 recession.

Case-Shiller

Residence costs have declined about 3% nationally from the height in the summertime of 2022, however as we all know, actual property is regional. So some areas have declined greater than 3%, and a few areas are nonetheless nearer to their peak ranges.

Along with the magnitude or the depth of the house value decline, one other method to measure the correction relies on time or “how lengthy has the correction lasted?”

After the 1990 recession, despite the fact that residence costs solely fell by about 2%, it took 37 months for residence costs to make a brand new peak.

The 2000 recession did not see any decline in residence costs, however the 2008 recession noticed residence costs crash 30%, and it took 116 months to achieve a brand new peak.

Case-Shiller

At the moment, residence costs peaked about eight months in the past. This knowledge is barely delayed, so this quantity is absolutely nearer to 10 or 11 months, however the declines are nonetheless gentle on a nationwide common by way of magnitude.

The Case-Shiller knowledge publishes residence costs for 20 main cities so we are able to measure what number of cities are exhibiting detrimental residence value progress on a rolling six-month foundation.

Within the 1990 recession, despite the fact that residence costs solely declined about 2% on common, the declines lasted for 37 months and impacted 74% of cities.

The 2008 recession was very massive by way of magnitude, falling 30%, it was very lengthy by way of period, taking 116 months to make a brand new peak, and it impacted 100% of cities.

Case-Shiller

We’re clearly in the midst of one other residence value downturn for the reason that declines have been about 3%, the period has lasted 10 or 11 months, and 75% of cities are exhibiting declining residence value progress.

We will debate the magnitude, and within the subsequent part, we’ll examine this residence value decline throughout a bigger pattern of historical past.

However first, we’ve to take a look at the dispersion of residence value declines and see the place residence costs are falling probably the most and the place residence costs have held up the very best as a result of the dialog about actual property may be very divided.

Some folks suppose residence costs of their metropolis are falling, whereas others have barely seen a correction, and this knowledge exhibits why each are true.

This chart exhibits the depth and period of the house value downturn within the 20 main cities throughout the nation. The left axis measures the % decline from the height, and the underside axis measures the period of residence value declines.

Case-Shiller

The higher left exhibits the areas which have been least affected, and the underside proper exhibits the place the housing downturn is hitting the toughest.

Cleveland, Chicago, Atlanta, Miami, and Charlotte have seen just about no correction in any respect, with residence costs inside 1% or 2% from their peak ranges and no constant declines.

On the opposite excessive, San Francisco, and Seattle have seen costs decline nearly 15% in lower than a yr. That is on par with 2008-type declines.

Within the center, we see cities like Dallas, Denver, Phoenix, Las Vegas, Los Angeles, and Portland the place there was a transparent shift, and residential costs have fallen about 6%-10%.

So there is no such thing as a doubt, primarily based on depth, period, and dispersion, that the US is nationally in a house value downturn. Relying on the placement, the downturn is anyplace from non-existent to extreme, with the nationwide common up to now in a average correction.

How Does This Downturn Examine To A Longer Historical past?

If we need to examine housing cycles throughout an extended time frame, we’ve to take a look at residence costs in actual phrases or adjusted for inflation.

There are a number of the explanation why taking a look at actual or inflation-adjusted residence costs is suitable.

Housing is essential for the wealth impact. When residence costs rise, folks really feel wealthier, and it is rather widespread to refinance and pull fairness out of a property to make use of on consumption or extra actual property belongings.

This solely works if the house value is rising in actual phrases, or else the money you pull out of the house cannot assist the consumption of different items rising even sooner in value.

During times of excessive inflation just like the 1970s, residence costs might rise in nominal phrases however fall sharply in actual phrases.

After we have a look at actual residence costs, we are able to see that costs usually decline round recessions. This is smart. The period of the corrections and the magnitude of the corrections fluctuate, however they’re usually centered round recessionary intervals.

Case-Shiller

Actual residence costs had been extra steady within the 4 a long time from 1960 via 2000 earlier than taking up what can solely be described as boom-bust sort progress, rising 75% from 1997 via 2006 and rising 78% from 2012 via 2022.

Actual residence costs peaked on a nationwide degree in Could 2022. The height was earlier for some cities like San Francisco, and later for locations like Miami, however in actual phrases, residence costs have peaked in every single place.

At this level, we’re solely going to consult with the nationwide common.

The US housing market has had six main downturns for the reason that 1960s. Residence costs declined round all of the recession intervals besides 2001 and the COVID recession.

Case-Shiller

Actual residence costs have declined about 6% since Could 2022.

By way of period, throughout previous housing downturns, actual residence costs declined for 33 to 70 months, apart from 2000, which noticed no declines in any respect, not even in actual phrases.

Case-Shiller

The opposite necessary level is that residence costs are likely to backside on the finish of the recession or after the recession. Residence costs are a slow-moving, lagging indicator with a full housing cycle typically taking 3-5 years.

So within the six main housing downturns, together with the intense 2008 state of affairs and the no-decline 2000 state of affairs, the typical recession brings a real-home value decline of roughly 12%, with declines that final for 37 months.

Case-Shiller

At the moment, residence costs have declined for six consecutive months and are about 6% from the height in actual phrases, however the financial downturn and many of the recession are nonetheless in entrance of us, so declines will doubtless proceed and attain at the very least the historic averages.

Main indicators of actual residence value progress are nonetheless shifting to the draw back, one thing we cowl in our Quarterly Actual Property Deep Dive experiences.

Abstract

In abstract, the US housing market is in the midst of an ongoing downturn, with costs declining in 75% of cities. The declines usually are not evenly distributed. Some cities are exhibiting substantial declines earlier than any important crack within the labor market, which is regarding, however some cities have solely simply seen the momentum slowdown with none sizeable reductions in value.

The place the housing market bottoms in relation to previous financial downturns stays an open query, however there is no such thing as a debate that the market hit a transparent peak in 2022, and the broad momentum stays to the draw back.

Whereas the IRS says most workers can solely contribute $22,500 to tax-deferred earnings to 401(okay) plans in 2023, prime executives at U.S. corporations can defer way more than that in the event that they take part in particular nonqualified deferred compensation packages often called “prime hat” plans.

A number of the particulars of these plans can be found in dense company filings, with specifics on the highest officers within the firm. In 2021, the highest executives at S&P 500 SPX, +1.19% corporations held a mixed $8.9 billion in these nonqualified tax-deferred (NQDC) accounts, in accordance with a brand new research from the Institute for Coverage Research and Jobs for Justice referred to as “A Story of Two Retirements,” that added up the road objects reported.

For example, the newest proxy assertion for Walmart WMT, -0.17% filed with the SEC exhibits the balances of deferred compensation of seven prime executives, together with Chief Govt Doug McMillon, who had an mixture steadiness of $169 million in his deferred compensation account on the finish of 2022. That steadiness presently earns a “mounted charge of curiosity set yearly primarily based on the 10-year Treasury notice TMUBMUSD10Y, 3.567% yield on the primary enterprise day of January plus 2.70%,” in accordance with the submitting, however Walmart is shifting towards a extra open system for contributions made starting in fiscal 12 months 2024 that might be market-based, the assertion notes.

Whereas the SEC filings present simply essentially the most extremely paid executives, greater than 700,000 workers are capable of take part in these sorts of plans at over 11,000 corporations, in accordance with a survey by MBS Monetary Group, an administrator of nonqualified government advantages. The common plan holds $16 million and the common participant steadiness is $265,000.

The “Story of Two Retirements” research appears at main companies and their prime executives, together with corporations like Hyatt Motels H, +0.44%, House Depot HD, +3.56%, Centene CNC, +2.67% and Pfizer PFE, -0.70%. It discovered that 64% of CEOs at a lot of these corporations participated in top-hat plans, and of those who did, the common steadiness was $14.6 million.

Credit score: Institute for Coverage Research and Jobs for Justice report, “A Story of Two Retirements.”

“Executives owe earnings taxes on this compensation after they withdraw the funds, however within the meantime, they profit from the tax-free compounding of funding returns,” says Sarah Anderson, director ofthe World Financial system Undertaking on the Institute for Coverage Research.

Tipping the hat for executives

So-called “prime hat” plans are allowed by the IRS as a type of government compensation. The plans are topic to retirement plan laws (Erisa), however not a part of the annual 401(okay) contribution limits. Executives can truly take part in each, deferring as much as the 401(okay) restrict yearly and contributing to the nonqualified choices. These NQDC plans can take many types. Some solely maintain contributions in firm inventory and a few maintain it in mounted earnings, whereas others permit the workers to decide on their investments. Some corporations put limits on how a lot might be contributed, whereas others permit limitless quantities.

The profit to the worker is tax deferral, whereas the profit to the corporate is retention. The cash put aside grows tax-free till the worker withdraws it, both at retirement or after they depart the corporate. The potential large tax hit may also help persuade some executives to remain put of their jobs.

One main potential detriment is that these holdings should not shielded from collectors, as 401(okay) funds can be. “If the corporate goes bankrupt, you’re out of luck,” says Steven Golden, managing director at CSG Companions, an funding financial institution primarily based in New York. “Most individuals don’t consider the worst-case state of affairs, however actually, it could trigger me anxiousness. In some instances, it’s some huge cash.”

Golden additionally factors out that top-hat plans merely delay taxes, they don’t erase the duty. “You’re higher off getting the cash up entrance and investing it after tax, simply to guard that half,” he says.

Extra from Beth Pinsker

That 401(okay) match isn’t simply free cash, 3% might purchase you two years of retirement

Learn how to get beginning investing with an investing membership

Neglect that $22,500 restrict. Some staff can supersize their tax-deferred retirement financial savings as much as $265,000 in 2023.

US Meals Holding (NYSE:USFD) is a meals service distributor that serves a wide range of industries in the USA. The outcomes for USFD in 1Q23 have been wonderful as soon as once more. The optimistic 1Q23 outcomes may be attributed to numerous components. First, better-than-expected progress greater than offset the results of inflation, and a extra worthwhile buyer combine helped increase income considerably. As issues stand, I do not anticipate any issues with USFD’s skill to achieve its FY23 aim.

Along with these components, I believe that the 1Q23 outcomes present how essential an publicity to healthcare and hospitality prospects is to an organization’s total buyer combine, which has helped the USFD get well demand. That is each good and dangerous, as excessive inflation and doable excessive rates of interest are prone to harm demand, placing a damper on the sustainability of the present restoration. As such, I believe a whole lot of traders out there are holding a “wait and see” method on how nicely USFD can execute on this surroundings. Importantly, if administration can present each progress and enchancment in margins, I consider this may forged a powerful optimistic momentum on the inventory valuation (ahead P/E), pushing it again to the historic common (from 14.4x to 16.7x). My take is it is vitally doable for margin to increase provided that a whole lot of the levers are within the hands-on administration akin to pricing and value management. My advice on USFD inventory now could be to attend for 2Q23 outcomes to see how nicely the corporate is progressing to FY23 revenue targets, and likewise assess administration feedback on the demand outlook for remainder of the 12 months.

1Q23 earnings and near-term outlook

Within the first quarter, USFD delivered sturdy monetary outcomes, surpassing market expectations. EBITDA reached $337 million, beating the consensus estimate of $293 million, whereas EPS stood at $0.50 in comparison with the consensus of $0.40. Income confirmed a modest upside at $8.54 billion versus the anticipated $8.48 billion. Notably, progress in whole case quantity was spectacular, reaching 5.7%, with notable energy in unbiased restaurant case progress at 8.1%, in addition to strong efficiency within the hospitality and healthcare sectors at 18.8% and 5.9% progress, respectively.

Regardless of issues concerning the lower-margin chain enterprise, which skilled a decline of 1.1%, it was not as extreme as anticipated, thanks USFD emphasis on unbiased progress. The gross revenue margin per case of 16.9% contributed considerably to the full gross revenue of $1.45 billion. In comparison with the 5.7% improve in instances, this represents a big 14% improve in gross revenue 12 months over 12 months. This successfully showcased USFD skill to extend common pricing (through numerous means like natural value hike, vendor administration, and so on.) – which is a crucial lever to it attaining FY23 targets, for my part.

Whereas the macroeconomic outlook is cloudy for the subsequent few months, it’s encouraging to see administration be very upbeat about present demand and the near-term outlook. I anticipate additional buyer acquisitions and market share positive factors, particularly amongst USFD goal buyer varieties like unbiased institutions, due to the restoration of the hospitality and healthcare industries. I additionally anticipate that the brand new on-line platform being rolled out as a part of USFD’s omni-channel and digital progress initiatives will contribute considerably to efficiency.

Margin upside

I believe it’s clear that margins have improved considerably and I consider there’s nonetheless room for growth this 12 months. There are two key line merchandise at play right here: gross revenue per case and working bills. As talked about above, I consider USFD can proceed to drive larger costs (pricing optimization, labor productiveness, and so on.) this 12 months beneath the guise of inflation (regardless of it exhibiting indicators of coming down). Enhance in pricing right here has big impression on the underside line given the excessive incremental margins. That mentioned, I acknowledge inflation won’t keep larger endlessly, and disinflation would possibly harm margins.

Nonetheless, what’s noteworthy is that USFD’s remarks drew consideration to deflation in particular protein classes the place a hard and fast greenback markup exists, safeguarding gross revenue per case. In the meantime, quite a few different merchandise are nonetheless experiencing inflationary pressures, and it’s anticipated that total inflation will persist. Even when gross revenue per case erodes, I believe USFD’s success in driving firm particular initiatives will assist to cushion and reduce in gross revenue through decrease working bills (i.e. decrease price construction. Moreover, though the extent of future leverage on the working expense line is unsure, the newly appointed CEO hinted at potential cost-saving measures that would result in further revenue progress within the forthcoming years.

Conclusion

USFD delivered spectacular ends in 1Q23, surpassing market expectations with sturdy EBITDA and EPS figures. The corporate showcased sturdy progress in whole case quantity and gross revenue per case. The near-term outlook stays optimistic, with administration expressing confidence in present demand and future prospects, pushed by the restoration of the hospitality and healthcare industries. Whereas macroeconomic uncertainties persist, I consider USFD has the potential to additional improve margins by pricing optimization and value management measures. The introduction of cost-saving initiatives by the brand new CEO additionally presents further upside potential for profitability within the coming years.