shaunl/E+ through Getty Photographs

ZIM: Unimaginable Restoration As Tensions Persist

ZIM Built-in Transport Companies Ltd. (NYSE:ZIM) buyers have loved a spectacular run as persistent geopolitical headwinds and resilient client spending underpinned improved investor sentiments. My cautious ZIM article in early February 2024 is assessed to be well timed earlier than ZIM fell towards its March 2024 lows. It additionally coincided with the pullback in international freight charges earlier than ZIM staged a big rebound in April and Might 2024. In consequence, ZIM has outperformed the S&P 500 (SPX) (SPY) considerably since bottoming out in November 2023.

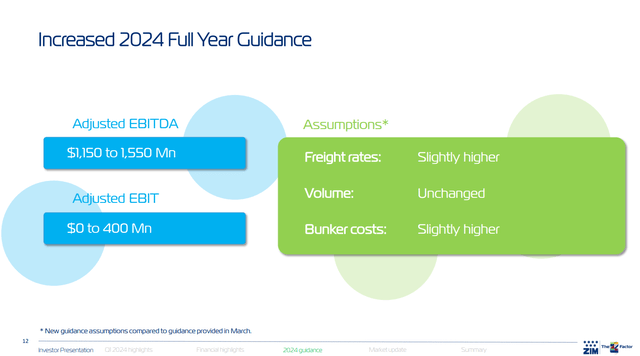

ZIM Built-in Transport’s Q1 earnings launch was well-received by the market. ZIM’s administration choice to revive ZIM’s quarterly dividend possible helped to bolster shopping for confidence. ZIM’s capacity to boost its full-year 2024 steerage additionally suggests a assured outlook via the second half of 2024.

I assess that ZIM has been consolidating near the $21 stage since late Might 2024. That stage was additionally examined in April 2023, earlier than ZIM fell considerably towards its November 2023 lows ($6.four stage). Due to this fact, I consider it is well timed for me to assist buyers reassess whether or not there’s nonetheless a chance to affix ZIM’s restoration.

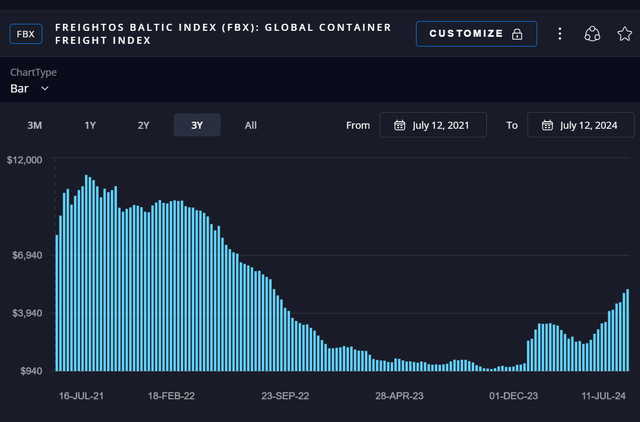

ZIM: Freight Charges Surged. However For How Lengthy?

Freightos International Container Freight Index (Freightos)

As seen above, whereas the latest restoration in international freight charges has been important, we’re nowhere near the pandemic highs in 2021. Analysts are blended on whether or not the freight price restoration can rally additional or whether or not the surge in freight charges is merely transitory. Geopolitical headwinds within the Center East are anticipated to persist at the same time as a possible ceasefire settlement between Israel and Hamas is being labored out. Due to this fact, market volatility attributed to the progress of the ceasefire talks ought to be anticipated. A constructive decision of the Israel-Hamas battle may affect the continued bullishness in international freight charges.

ZIM FY2024 Steering replace (ZIM filings)

As a reminder, the Purple Sea assaults have prompted a rerouting of container transport routes. It has additionally benefited ZIM, serving to to “soak up important transport capability.” It has created a “pseudo-supply constraint that has contributed to larger freight charges throughout completely different international commerce lanes.”

Consequently, ZIM has develop into extra assured that it’ll profit from the rise in spot charges. Accordingly, ZIM Built-in has recalibrated its spot market publicity to capitalize available on the market restoration. In consequence, ZIM anticipates about “65% of its Transpacific quantity to be spot-related,” with the remaining 35% based mostly on contract.

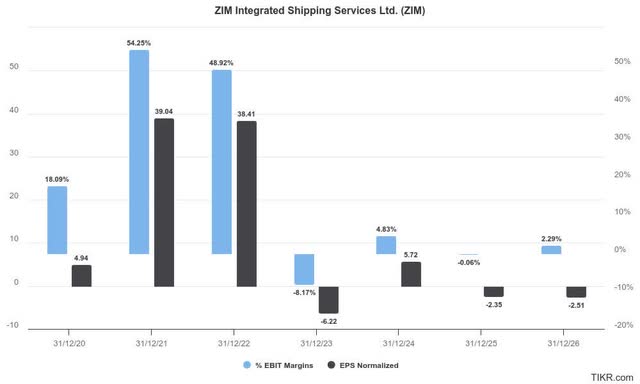

ZIM: Earnings Might Be In The Purple In 2025

ZIM estimates (TIKR)

Wall Avenue stays skeptical concerning the sustainability of the restoration in freight charges. As seen above, the earnings accretion is anticipated to stage off in 2024 earlier than falling via FY2026.

I assess that pessimism in ZIM’s restoration thesis is justified. There are considerations about whether or not the latest surge was attributed to pull-forward demand as US importers look to avoid probably larger tariffs. As well as, US manufacturing capability stays nicely beneath the height noticed within the post-pandemic surge. Therefore, the provision chain constraints aren’t assessed to be structural. Even when they persist via the top of 2024, important uncertainties on an additional restoration in 2025 may hamper shopping for sentiments on ZIM.

Whereas client spending is assessed to stay resilient, it has already normalized from the pandemic patterns. In consequence, it appears unreasonable to anticipate one other provide chain snafu just like the one we noticed in the course of the pandemic chaos.

Furthermore, ZIM’s elevated publicity to identify charges has additionally left the corporate extra weak to a probably sharper downturn in freight charges, hurting its ahead steerage. Earnings buyers should not take ZIM’s restoration of its dividend without any consideration, because it’s predicated on its earnings profile.

Given ZIM’s estimated dividend yield of simply 5.2%, it may not be adequate for earnings buyers to think about returning aggressively. Whereas the Fed is anticipated to chop rates of interest from the September 2024 FOMC assembly, the cadence stays unsure.

Is ZIM Inventory A Purchase, Promote, Or Maintain?

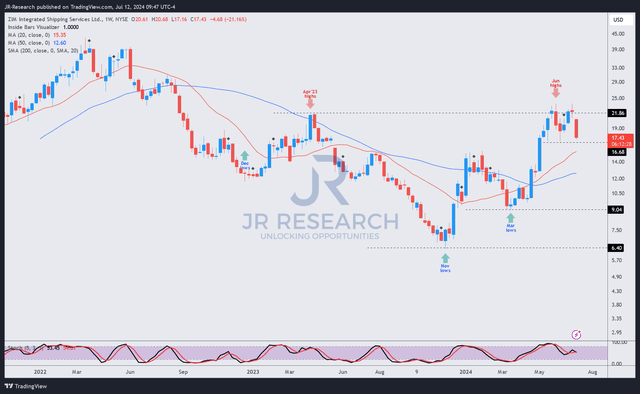

ZIM worth chart (weekly, medium-term) (TradingView)

ZIM’s worth motion signifies that the inventory has been consolidating below the $21 stage since late Might 2024. Makes an attempt to interrupt out of that resistance zone since then have been futile.

Promoting depth additionally rose this week, suggesting a re-test of the $17 stage seems more and more possible. However my warning, I’ve additionally assessed that ZIM has decisively shaken off its downtrend bias. In consequence, patrons would possibly return to help the inventory as it is not costly.

In search of Alpha Quant charges ZIM with a “B” valuation grade. Upgraded Wall Avenue estimates on ZIM recommend that ZIM’s dip-buyers may bolster steep pullbacks if heightened freight charges persist.

Regardless of that, I view the chance/reward as comparatively well-balanced, given the stiff resistance zone below the $21 stage.

Score: Keep Maintain.

Essential observe: Buyers are reminded to do their due diligence and never depend on the knowledge offered as monetary recommendation. Think about this text as supplementing your required analysis. Please all the time apply impartial considering. Word that the score isn’t meant to time a particular entry/exit on the level of writing except in any other case specified.

I Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a essential hole in our view? Noticed one thing vital that we didn’t? Agree or disagree? Remark beneath with the intention of serving to everybody locally to study higher!