A thoughts all logic is sort of a knife all blade. It makes the hand bleed that makes use of it.”― Rabindranath Tagore.

It has been practically a 12 months since we final took a look at AbCellera Biologics Inc. (NASDAQ:ABCL). The corporate’s income stream fell over a cliff because of the ebbing of the Covid pandemic. Nevertheless, these gross sales helped the corporate construct up an enormous money hoard. AbCellera continues to develop its wide selection of partnerships throughout the drug developmental house. An replace on this pretty distinctive concern follows under.

Searching for Alpha

Firm Overview:

AbCellera Biologics has constructed a platform for antibody drug discovery and growth and is headquartered in Vancouver, BC. The corporate is targeted on discovering antibodies from pure immune responses, that are pre-enriched for antibodies. The inventory trades round $5.50 a share and sports activities an approximate market capitalization of $1.5 billion.

November Firm Presentation

Now that its Covid-related income has dried up, AbCellera is solely targeted on using its AI-driven expertise platform to find antibodies that may be developed by its extensive assortment of companions all through the healthcare house.

November Firm Presentation

As you may see above, it’s fairly the intensive record. AbCellera can earn varied milestones (developmental, regulatory, gross sales) round these candidates in addition to royalties on any eventual commercialized gross sales. As well as, the corporate has garnered funding from authorities entities as nicely.

November Firm Presentation

Third Quarter Outcomes:

AbCellera Biologics posted its Q3 numbers on November 2nd. The corporate delivered a GAAP lack of 10 cents a share, three pennies a share above expectations. Revenues fell over 93% to $6.6 million, lacking the consensus by some $5 million. $6.four million of income got here from partnership analysis charges and the remainder from licensing charges.

Many of the over $380 million in revenues AbCellera racked up in 2022 was on account of a COVID-19 remedy known as bamlanivimab, which AbCellera collaborated on with drug big Eli Lilly (LLY) on. These revenues are within the firm’s rearview mirror now.

Current Developments:

On November 29th, the corporate introduced an approximate 10% discount in its workforce to chop prices. In September, AbCellera prolonged its partnerships. First, by asserting a brand new strategic developmental settlement with Incyte (INCY). Simply over every week later, the corporate disclosed it had expanded an present partnership with Regeneron (REGN).

Analyst Commentary & Stability Sheet:

Since third quarter outcomes posted, six analyst companies together with Piper Sandler and Truist Monetary have reiterated Purchase/Outperform scores on the inventory. Value targets proffered vary for $6 to $28 a share. Benchmark Co. downgraded the shares to a Maintain shortly after Q3 outcomes hit the wires.

Slightly below 13% of the excellent float of the shares is at present held brief. A number of insiders bought roughly $1.6 million in inventory collectively in 2023. There have been no insider gross sales of fairness final 12 months. There was insider exercise within the shares thus far in 2024. AbCellera Biologics exited the third quarter with some $813 million in money and marketable securities on its stability sheet after posting a web lack of $28.2 million for the quarter. The corporate carries no long-term debt.

Verdict:

The corporate made 50 cents a share in FY2022 because of revenues of simply over $385 million. In FY2023, the corporate is on observe to lose 47 cents a share as revenues drop all the way in which all the way down to $38 million. Fourth quarter outcomes are scheduled to submit on February 20th. The present analyst agency consensus is that AbCellera Biologics will lose 61 cents a share in FY2024 as revenues rise to $60 million in the course of the 12 months.

I proceed to take care of a small “watch merchandise” place in ABCL by way of lined name holdings. AbCellera has constructed up an enormous money hoard because of its Covid-related income stream and has a formidable record of partnerships throughout the drug trade.

Searching for Alpha

As of the tip of the third quarter, AbCellera had 182 applications underneath contract with 42 completely different companions.

November Firm Presentation

In principle, AbCellera’s developmental strategy ought to ends in decrease developmental prices and quicker time to marketplace for its companions. As well as, AI pushed efforts throughout the drug trade are getting extra discover and growing their share of the developmental greenback. The problem is the corporate’s accomplice pipeline is sort of solely early-stage candidates at this level.

November Firm Presentation

AbCellera did record two of its personal led excessive potential IND enabling research on its final company replace in November. The problem for AbCellera Biologics Inc. is revenues and earnings (really losses) are going to be lumpy for years as a result of timing of charges and milestone payouts. The corporate is well-funded, however it is going to be years earlier than any extra potential partnered merchandise are accepted and hit the market. As such, the inventory solely deserves a small place in a affected person, long-term investor’s nicely diversified portfolio whereas awaiting additional developments.

There are crimes of ardour and crimes of logic. The boundary between them just isn’t clearly outlined.”― Albert Camus.

Altria (NYSE:MO) is a “Dividend King” and there are solely about 55 corporations that at present qualify for this title. To make this checklist, an organization must have at the very least 50 years of consecutive dividend will increase. Altria has a 54-year historical past of consecutive dividend will increase. The corporate has been ready to do that despite main laws and despite declines in tobacco utilization, which is spectacular. The tobacco trade has persistently been in a position to make up for lowered volumes by growing costs, and this development seems poised to proceed. Whereas it’s regarding to see an organization that expects lowered volumes sooner or later, it might proceed to boost costs, and I believe there’s a robust probability that smokeless merchandise and hashish (when it’s doubtlessly legalized in all 50 states) will provide Altria new alternatives for progress.

This autumn Outcomes Have been Good Sufficient

The decline in gross sales has been regarding for traders, and as a current Looking for Alpha article factors out, Altria has been lacking income estimates for a lot of quarters now. Due to this, expectations for This autumn weren’t excessive. Luckily, Altria delivered in-line outcomes with non-GAAP earnings per share of $1.18, though revenues got here in at $5.02 billion, which was a miss by $60 million. The corporate additionally stated it anticipated 2024 earnings to return in at $5 to $5.15 per share. The Board of Administrators (having not too long ago accomplished a $1 billion share buyback), additionally introduced a brand new $1 billion share buyback, which is anticipated to be accomplished by the top of 2024. Since Altria was in a position to match analyst estimates for This autumn, and because it earned $1.18 per share, that is adequate, and it permits Altria to comfortably pay a $0.98 quarterly dividend. The steering of $5+ per share in earnings in 2024 can be sufficient to comfortably pay the beneficiant dividend it presents.

Earnings Estimates And The Dividend

With administration anticipating Altria to earn $5 to $5.15 per share for 2024, the dividend is totally lined after which some. With the dividend totaling $3.84 per share for the 12 months, this inventory is now yielding about 9.8%. Moreover, the dividend seems protected, for the reason that payout ratio is round 75%. Continued share buybacks also can assist enhance earnings per share, and subsequently hold the payout ratio at an inexpensive degree and in addition permit the corporate to extend the dividend, simply because it has been doing for therefore a few years.

For example, in 2013, the quarterly dividend was 44 cents per share. Nevertheless, due to annual dividend will increase, the quarterly dividend is now 98 cents per share. Meaning the dividend has greater than doubled in simply round 10 years. If Altria continues to purchase again shares, and if it develops progress potential in associated industries sooner or later, this might permit it to considerably enhance the dividend over the subsequent 10 years, simply because it has for the previous 10 years.

Right here Is How Altria’s Dividend Might Double Your Cash In About 7 Years

Not way back, money balances had been incomes nearly nothing. However today, I like incomes round 5% on my money that is parked in cash market funds. I do not count on a return to a Zero Curiosity Charge Coverage or “ZIRP”; nevertheless, it appears seemingly that rates of interest will hand over at the very least a few of the good points we have now seen, particularly if and when an financial slowdown or recession happens. This implies it is a perfect time to lock the upper yields we’re having fun with now by shopping for choose shares that provide a beneficiant and sustainable dividend. By doing this, traders may very well be poised to lock in excessive yields and in addition place themselves for capital good points that might happen when rates of interest decline.

With this in thoughts, Altria’s beneficiant payout, which is excessive sufficient to roughly double your cash in nearly seven years or so. That is based mostly on the rule of 72, whereby you divide 72 by the yield. For instance, 72 divided by 10 (from a virtually 10% yield), means it should take about 7.2 years to double your cash.

Altria Has A Main Asset It Might Monetize For Extra Dividends In The Future

Altria owns a significant stake in Anheuser-Busch InBev (BUD). In accordance with a Barron’s article the stake is value about $11 billion and it would monetize this asset sometime. If this asset is offered, the money it raises could be used to pay a particular dividend or it may very well be used to purchase again shares. Altria at present has a market capitalization of about $71 billion, so an asset sale of $11 billion may very well be sufficient to purchase again about 15% of the shares excellent, which might enhance earnings per share for the remaining shareholders. Altria has roughly 1.Eight billion shares excellent, so in the event that they offered the stake in Anheuser-Busch InBev for $11 billion, this works out to simply over $6 per share in proceeds that may very well be paid out as a particular dividend. Anheuser-Busch InBev shares at present commerce for about $60 per share, however traded for over $120 per share in 2016 and 2017. Maybe Altria administration is ready and hoping for the inventory to return to those ranges, wherein case the worth of this stake can be about double the present worth and subsequently be doubtlessly value round $22 billion, which might symbolize a really main achieve from present ranges.

The Chart

Because the chart beneath exhibits, Altria shares dropped from across the $41 degree to simply about $38, after the corporate reported weaker than anticipated Q3 outcomes on October 26, 2023. The inventory has recovered a bit and has since been in a buying and selling vary, roughly between $40 to $42 per share. The 50-day shifting common is $40.79 and the 200-day shifting common is $41.62. Altria continues to be on this buying and selling vary, even after This autumn earnings, and that may be a constructive.

stockcharts.com

Hashish Might Be Altria’s Future Development Driver

It appears clear that the main tobacco corporations within the U.S. have been treading very fastidiously and prevented making the potential misstep of getting straight concerned within the hashish trade. U.S. Federal regulation nonetheless makes marijuana unlawful (together with associated merchandise) and that makes moving into this enterprise straight manner too dangerous for a corporation like Altria proper now. Nevertheless, there are a selection of payments earlier than Congress that might legalize marijuana on a Federal degree. This is able to be a gamechanger and that is once I count on corporations like Altria to behave aggressively to straight enter this trade. Altria has already proven some severe curiosity in hashish by investing within the trade in addition to supporting it. In 2019, Altria acquired a 45% stake in Cronos Group, Inc., which is a Hashish firm situated in Canada. Concerning this funding, Altria states:

“This funding positions Altria to take part within the rising world hashish sector, which we imagine is poised for speedy progress over the subsequent decade. It additionally creates a brand new progress alternative in a class that’s adjoining and complementary to our core tobacco companies.”

I imagine Altria might simply be ready for hashish to be legalized on the Federal degree, and maybe that would be the second that they resolve to promote the Anheuser-Busch InBev stake. This can be a large asset, and the proceeds, or at the very least a few of them, may very well be used to amass a number one hashish firm. This may very well be the expansion driver that Altria must alleviate investor considerations, and broaden the value to earnings a number of. As well as, Altria seems to publicly help the legalization of hashish on a Federal degree, by stating:

“We help a complete federal framework for all hashish merchandise that’s based mostly on science and proof, and we imagine it’s time for a nationwide dialogue about that regulatory framework.”

The Potential Draw back Dangers

The primary potential danger appears to clearly be that fewer persons are smoking today, and laws and bans appear to be growing. If Altria would not remodel itself by shifting into high-growth classes like maybe hashish, the shares might commerce at an excellent lower cost to earnings ratio sooner or later. If administration makes investments or acquisitions which can be ill-conceived, that’s one other potential danger issue.

In Abstract

There are positively some potential draw back dangers when investing in tobacco shares, so I might not take a giant stake by way of positioning in my portfolio. However the dividend yield is so compelling that, in my view, it is smart to personal some shares. I might scale right into a place and see how the inventory does over the subsequent couple of quarters. The dividend may be very beneficiant and will proceed to see small annual will increase due to Altria’s capability to boost costs and since it might monetize the stake it has in Anheuser-Busch InBev. Even when this inventory goes nowhere over the subsequent seven years or so, the dividend alone is sufficient to double your cash in that timeframe.

If rates of interest decline within the subsequent couple of years, traders may very well be prepared to pay extra for this inventory, and that might give traders who purchase now some potential capital good points. I believe the priority over declines in tobacco volumes are greater than offset by the potential positives which embody a decline in rates of interest, continued share buybacks, the potential for Altria to monetize a significant asset, and the potential for the corporate to boost costs and maybe get into greater progress industries comparable to hashish. If declining rates of interest in some unspecified time in the future converge with a brand new progress driver comparable to hashish for Altria, this inventory may very well be re-rated a lot greater. It isn’t simply This autumn outcomes that present Altria can carry on paying the beneficiant dividend, additionally it is the steering it offered for 2024, and naturally the multi-decade historical past it has of paying dividends.

No ensures or representations are made. Hawkinvest is just not a registered funding advisor and doesn’t present particular funding recommendation. The knowledge is for informational functions solely. It is best to all the time seek the advice of a monetary advisor.

The Federal Reserve’s pushback on expectations for interest-rate cuts over the previous two weeks has traders closing watching inflation information and piling more money into money-market funds.

Buyers stashed a report $6.48 trillion away in U.S. money-market funds via the top of January, with the stability rising as euphoria in December over a Fed coverage pivot fizzled, based on Crane Information.

Fed Chairman Jerome Powell first poured chilly water on aggressive expectations for charge cuts at a late January coverage assembly by indicating a March charge minimize wasn’t probably. He adopted up days later with a CBS Information “60 Minutes” interview, telling 6.6 million viewers that the central financial institution would tread rigorously on charge cuts as a result of inflation isn’t but convincingly tamed.

“He actually put an enormous damper on it,” stated Deborah Cunningham, chief funding officer, world liquidity markets at Federated Hermes, a gaggle that had $560 billion in money-market property as of Dec. 31. “The market bought forward of itself in November and December.”

Cautious bonds

Earlier optimism about decrease rates of interest, probably as quickly as March, helped U.S. bond funds swing to optimistic returns in 2023.

But, many benchmark bond indexes have been again within the crimson in February, with the 10-year Treasury yield BX:TMUBMUSD10Y climbing to 4.186% on Friday, the very best since mid-December.

“The fairness market wouldn’t discover, however the bond market is actually listening to Powell,” stated George Catrambone, head of mounted revenue at DWS Group, in a telephone interview.

“Powell took away the punch bowl in January, however that was wanted,” he stated. “They do want to protect towards a reacceleration of inflation.”

With that backdrop, Catrambone referred to as subsequent Tuesday’s scheduled launch of the consumer-price index for January the week’s “principal occasion,” significantly after a robust January jobs report and information displaying a the U.S. financial system grew 3.3% within the fourth quarter.

See: The primary huge inflation report of 2024 is popping out. Right here’s what the CPI is prone to present.

A seasonally-adjusted CPI for the fourth quarter got here in Friday at a 3.3% annual charge, underscoring the progress the Fed has made in bringing worth pressures down from a greater than 9% peak on this cycle. Nonetheless, the price of residing stays above the central financial institution’s 2% goal.

“I do suppose the Fed is happy with the inflation progress to date, however we have to see extra,” Catrambone stated. With that backdrop, he stays an advocate of investing within the front-end of the Treasury yield curve, significantly with charges on 6-month Treasury payments BX:TMUBMUSD06M above 5% for practically a yr.

“Whereas the bar to chop is excessive, the bar to boost is even increased,” Catrambone stated.

Learn: Recession fears evaporate in new forecast of high economists

S&P 500’s milestone

Cautious tones within the bond market in current weeks have been largely lacking from U.S. shares, with the Dow Jones Industrial Common DJIA and S&P 500 index each embarking on a record-setting spree to start out 2024, and the Nasdaq Composite Index not far behind.

See additionally: U.S. shares have simply completed one thing that hasn’t occurred since 1972

Adam Hetts, world head of multiasset at Janus Henderson Buyers, stated that staying in money will be tempting, particularly final yr when recession issues had been on the forefront for thus lengthy.

“Buyers are actually anticipating a Goldilocks situation,” Hetts stated, a scenario the place the financial system retains rising however inflation continues to fall. Alongside the best way, they probably have to abdomen “cold and warm financial information.”

“Buyers too targeted on the recession crystal ball went into money, enticed by excessive charges,” Hetts stated. However by avoiding shares, traders would have missed out on the S&P 500’s roughly 23% advance up to now 12 months, based on FactSet information.

“Money is king for short-term liquidity wants, however being obese money will be poisonous for long-term monetary planning,” Hetts stated.

To that finish, he favors a extra conventional 60:40 allocation to shares and bonds, particularly given the upper yields out there in intermediate-duration mounted revenue to offset any turmoil that might erupt in equities that look “priced to perfection.”

The S&P 500 SPX on Friday closed above the 5,000 mark for the primary time ever, whereas gaining 1.4% for the week to shut at a report 5,0526.61, based on Dow Jones Market Information.

See: S&P 500 reaches 5,000 for first time. Right here’s what it means for the market.

The Dow superior lower than 0.1% for the week, ending at 38,671.69, whereas the Nasdaq rose 2.3% for the week, ending at 15,990.66, solely 0.4% off its earlier report from November 2021, based on Dow Jones Market Information.

In the meantime, money parked in money-market funds has been incomes about 5% for a lot of months, helped alongside by the yield on the 1-month Treasury invoice BX:TMUBMUSD01M and 3-month BX:TMUBMUSD03M round 5.38% as of Friday, based on FactSet.

With the brand new “realty test” in markets round rate-cut expectations this yr, Cunningham at Federated Hermes stated attending to a $7 trillion stability for money-market funds isn’t exhausting to think about.

Learn: Magnificent Seven shares have soared, however traditionally it’s been ‘profitable’ to guess towards the largest shares

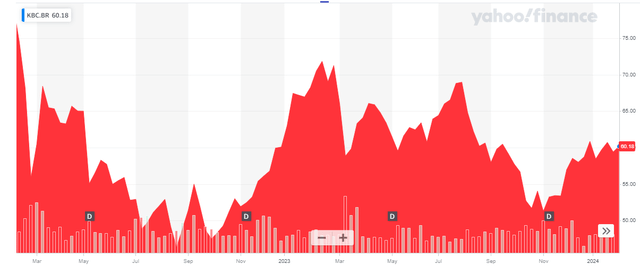

Because it has been some time since I mentioned KBC Group (OTCPK:KBCSF) (OTCPK:KBCSY), the current publication of the full-year outcomes for 2023 is an efficient second to inspect the efficiency of the Belgian financial institution/insurance coverage firm.

Yahoo Finance

KBC Group has its major itemizing in Belgium the place the corporate is buying and selling with KBC as its ticker image. The Brussels itemizing has a median quantity of 625,000 shares per day (for a financial worth of roughly 36M EUR), making it essentially the most liquid itemizing and I might strongly advocate to make use of the Euronext Brussels itemizing to commerce within the firm’s inventory. As KBC Group studies its monetary ends in Euro and has its major itemizing in the identical foreign money, I’ll use the EUR as base foreign money all through this text.

The financial institution’s web site accommodates a ‘obtain solely’ hyperlinks, however you could find all of the related info I’ll be referring to right here.

Regardless of the turmoil, KBC posted a good set of ends in This autumn

The monetary sector hasn’t had a simple 2023 however luckily most European banks weren’t hit by the fallout attributable to the problems within the US banking sector. I additionally just like the mannequin of providing banking providers and insurance coverage providers beneath one roof as cross-selling of merchandise could be fairly worthwhile.

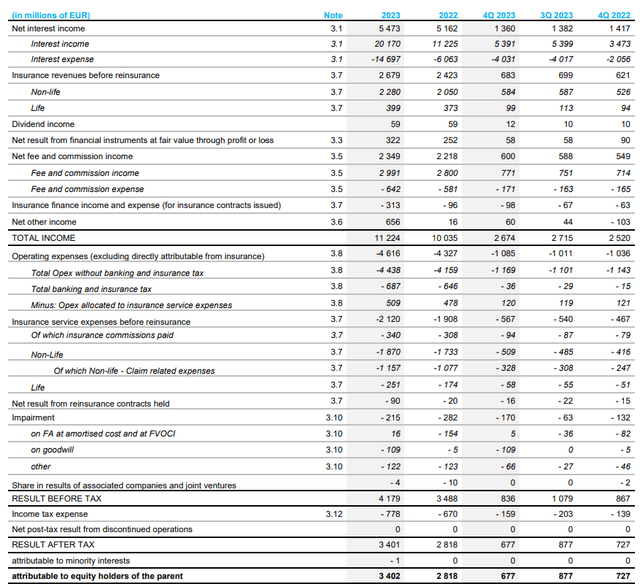

However after all, the principle focus has been on the evolution of the online curiosity revenue. And KBC Group has really executed a fairly good job in defending its internet curiosity margin. Whereas the stress elevated in the direction of the top of the yr, the FY 2023 outcomes point out a pleasant 6% enhance within the internet curiosity revenue, which jumped to five.47B EUR.

KBC Investor Relations

Wanting on the different parts that make up the 2023 outcomes, we see the full insurance coverage income elevated to 2.68B EUR whereas the bills associated to the insurance coverage actions have been simply 2.12B EUR leading to a constructive contribution of roughly 560M EUR. The revenue assertion above additionally clearly reveals the financial institution has its mortgage loss provisions beneath management. Whereas it recorded a 215M EUR impairment cost, in extra of half that cost was associated to the impairment of goodwill on the steadiness sheet. The ‘different impairment’ costs have been primarily associated to intangible mounted belongings.

The sturdy credit score threat atmosphere was boosted by a 155M EUR launch of beforehand recorded provisions for geopolitical and rising dangers and that launch absolutely compensated for the 139M EUR recorded mortgage loss provisions throughout FY 2023 and that is why the revenue assertion above reveals a provision launch of 16M EUR on monetary belongings. Whereas we should not financial institution on this taking place once more sooner or later (the mortgage loss provisions will normalize), it didn’t have a serious impression on the financial institution’s reported internet revenue as the opposite impairment costs have been increased than typical which implies the full impairment cost was simply 67M EUR decrease than within the earlier yr.

The web revenue generated throughout 2023 was 3.4B EUR which works out to an EPS of 8.04 EUR per share. KBC Group is proposing to pay a dividend of 4.15 EUR per share (topic to the usual dividend tax in Belgium of 30%).

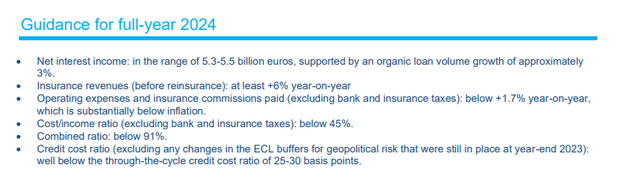

Wanting ahead to the 2024 efficiency

The financial institution has additionally supplied an preliminary steering for 2024. It expects a internet curiosity revenue of 5.3-5.5B EUR and the midpoint of this steering represents a small 1.5% lower in comparison with the FY 2023 internet curiosity revenue. Nonetheless, the anticipated insurance coverage income will probably offset the impression of the decrease internet curiosity revenue.

KBC Investor Relations

The mortgage loss provisions ought to stay very low: as you’ll be able to see above, KBC Group is guiding for a credit score price ratio ‘effectively beneath’ the through-the-cycle price ratio of 25-30 bp. With a complete quantity of 306B EUR in monetary belongings on the steadiness sheet, assuming a 15 bp credit score price ratio would lead to complete impairment costs of 450M EUR. I believe 15 bp is fairly conservative contemplating the financial institution’s current credit score price ratios for the interval 2020-2023 have been respectively 0.60%, -0.18% (a internet launch), 0.08% and 0.00% in 2023. Odds are KBC can preserve the credit score price ratio beneath 10 bp through which case there ought to be no noticeable impression on the financial institution’s earnings assuming no different goodwill or intangible asset impairments are essential.

This means we will count on the financial institution’s earnings to stay comparatively steady in 2024. Nonetheless, if I am making use of the upper credit score price ratio, I anticipate a small earnings lower in the direction of 7.75-7.85 EUR per share. A decrease credit score price ratio would clearly increase the earnings outcome.

Funding thesis

I at present don’t have any direct place in KBC Group however I’ve a fairly substantial lengthy place in a mono-holding whose solely asset is a stake in KBC Group, so I not directly have publicity. Buying and selling at simply over 60 EUR per share, KBC Group just isn’t costly in any respect because the inventory is buying and selling at roughly 7.5 instances the 2023 earnings and at lower than Eight instances my anticipated 2024 internet revenue. The dividend yield of just about 7% is interesting as effectively and given the low payout ratio of round 50%, that dividend is sustainable, even when the EPS would present a slight lower in 2024.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.

Larson: Hiya and welcome to our newest MoneyShow MoneyMasters Podcast. I am Mike Larson, editor in chief at MoneyShow. And at the moment I am talking with Mike Inexperienced, portfolio supervisor and chief strategist at Simplify Asset Administration. Welcome to the podcast, Mike.

Inexperienced: It is a pleasure to be right here. Thanks for having me.

Larson: I do recognize you taking the day out to speak right here. You speak slightly bit about virtually each market on the market. I additionally know you are a macro man who’s concerned in a number of completely different markets. However I wish to begin by taking a minute out to offer a bit about your background – and Simplify’s – in addition to speak slightly bit about your agency’s ETF lineup.

Inexperienced: Positive. So, I have been doing this for in all probability longer than I ought to have. I obtained began in 1992, and have managed all the things from mutual funds to separate accounts to hedge funds, and have achieved all the things from small-cap worth to macro. And it is a perform of only a profession that my trajectory moved from valuation skilled initially, really specializing in M&A, after which transitioning to being targeted on issues like derivatives, and so forth., which traces up very properly with my historic profession.

In 2020, the principles modified round ETFs. The SEC launched what’s known as the spinoff rule, which adopted sizzling on the heels of one other change in 2019 known as, excitingly, the ETF Rule. The ETF rule made it simpler for brand spanking new ETFs to be launched. The spinoff rule created the principles round which we might embrace hedge fund-type methods in ETFs.

And so we acknowledged that the tax benefits of the ETF framework, in addition to issues like not having the Okay-1s that you’d have with conventional partnerships, makes the ETF really a greater residence for a lot of hedge fund methods for high-net value people or people who wish to acquire entry to these diversified methods.

We had been very lucky. We launched in September 2020, we had been principally pandemic infants. We’re a really digital firm, with our staff unfold all throughout america. A pair really had been worldwide till very lately. And we have grown as much as nearly three and a half billion {dollars} in belongings beneath administration now, which is good from a standing begin. However as I prefer to remind folks, that is nothing in an trade during which belongings are often measured within the trillions.

And our lineup contains all the things starting from fixed-income merchandise like our credit score high-yield product, the place we provide a credit score hedge overlay on prime of the excessive yield. That is really carried out fairly properly, outperforming benchmarks even though we’ve not seen a lot credit score unfold widening, and most of that outperformance has really come through the transient intervals of credit score unfold widening. So the technique thus far has labored actually, very well.

We additionally provide options merchandise, issues like quantitative investments methods that you might have heard known as transportable alpha. We’re the primary ETF agency to supply these in a fund, and we additionally provide issues like managed futures or trend-following methods that historically haven’t been accessible in ETF kind, or if they’ve been accessible in ETF kind, they have been what’s known as a Replicator. They successfully have tried to fast-follow the habits of others within the trade. We had been the primary to truly design a product that could possibly be traded in a liquid surroundings the place we had been capable of execute trades on a each day rebalancing foundation. That product has been doing fantastically properly, and so we’re actually happy with the event of Simplify.

Larson: Now, your fundamental product, I assume, is the Simplify Macro Technique ETF, or “FIG”, if I am not mistaken.

Inexperienced: Properly, it is my asset allocation product. The product that I really am instantly managing when it comes to the underlying parts as in comparison with asset allocating is the credit score high-yield product that I recognized. However general, sure, I focus my efforts on this concept of asset allocation.

Larson: Properly, let’s speak macro technique. Let’s speak about a number of the big-picture issues which can be occurring on the market and type of what you discover fascinating. I imply, the Fed is absorbing a number of consideration on Wall Road, and heck on 60 Minutes for that matter.

What are your ideas on Powell and the outlook for rates of interest right here? I do know you speak slightly bit about what the Truflation – real-time inflation gauges – are exhibiting, so I’m inquisitive about your take there.

Inexperienced: Yeah. So, I believe it is a actually fascinating interval. We have now the US CPI or PCE knowledge, which, by building, is designed to clean out inflationary metrics. So, most individuals usually are not conscious of this. But when you concentrate on issues like about 40% of the CPI is definitely composed of a shifting common of housing bills, together with issues like rents, and so forth., or the rents that you simply consider or that will be recognized related to a property much like yours – it is not a survey, I simply wish to be very clear on that – these are likely to create clean photos, and because of this they underreported inflation in 2021 they usually overreported inflation at the moment.

I notice that that makes folks annoyed as a result of they take a look at their grocery invoice they usually’re like, it is not coming down. Keep in mind that inflation is the change within the value degree, not absolutely the degree of the value degree. And so, your milk is dearer, your cereal is dearer.

The query is, is it changing into dearer at a extra fast fee, or has it retreated to the kind of low inflation that we skilled previous to the occasions of the worldwide pandemic? And the reply seems to be that we have largely retreated again. Actual-time metrics – issues that aren’t making an attempt to interact in that smoothing habits, merchandise like Truflation, which may be discovered at Truflation.com – provides you with a sign of what real-time inflation seems like. That is suggesting we’re again down under 2%, someplace within the 1.4% vary is what that seems to be. That meshes fairly properly with the information that I am seeing when it comes to a direct part.

The issue, after all, is that in case you have 5.5% or 5.25% rates of interest and 1.4% inflation, you are really operating a extremely constructive, actually robust actual fee. That, sadly, simply would not actually match up with the potential progress for the U.S. financial system. Keep in mind that the expansion of an financial system is a mix of the variety of employees, the variety of hours they every work, and the way productive they every are in these hours. The information that we’re seeing means that the expansion of employees is now fantastically low, someplace within the neighborhood of 20-30 foundation factors, or 0.2-0.3%. If we take a look at the hours that individuals work, these are literally falling. And if we take a look at the productiveness, or the quantity that they are placing out per employee, we’re not seeing that change in any marked approach.

We have seen some catch-up previously couple of quarters. However general that implies that now we have comparatively low progress potential for the U.S. financial system, and that is largely matched by the information we’re seeing, the place it is requiring explosive progress in authorities debt as a way to push the financial system to the degrees of progress that we’re at the moment seeing, about 3% year-over-year GDP ranges.

You realize, that simply that traditionally would counsel that you simply require a lot decrease ranges of rates of interest, and we’ll see if that finally ends up being the case. The problem proper now could be that after a number of years – like, so, actually a decade of very low rates of interest – many entities within the markets had termed out their debt publicity. So, in different phrases, they are not topic to the short-term forces of the Fed mountaineering rates of interest.

And so, perversely, what we’re seeing is a really sluggish burn, the place the U.S. authorities’s rate of interest expense rose pretty quickly as we noticed new borrowing within the type of T-bills, and so forth. come by way of. Curiously sufficient, many households are experiencing a lot greater rates of interest on issues like cash market funds. That is benefiting those that at the moment have capital.

However what we have additionally seen is companies and households that theoretically must be refinancing their debt, whether or not that is as a result of they’re shifting into a bigger residence or shifting to a brand new location to pursue employment. That might be a sort of refinancing related to the mortgage area. Or companies within the excessive yield or investment-grade area which can be confronting the truth of a lot greater rates of interest, they’ve delayed that refinancing. And so now we’re really a “maturity wall,” proper. The refinancing wants related to excessive yields, they’re among the many highest we have ever seen in historical past. And other people overlook that about 30% of the employment in america is tied to corporations which can be levered in a technique or one other.

And so now we really get to search out out in the middle of 2024 what occurs when these corporations attempt to refinance. And I obtained to let you know, sadly, we’re seeing a number of knowledge that implies it is not significantly constructive. We’re seeing the extra distressed corporations wrestle to acquire refinancing. We’re seeing an increase in bankruptcies. We’re seeing an increase in company stress ranges that, you understand, sadly, that’s not being matched by what we’re seeing when it comes to market pricing. However we’re really empirically observing this within the underlying knowledge.

And so it is an fascinating crossroads that we’re at. Do the markets start to reprice to what we’re seeing within the empirical expertise? Or does the empirical expertise counsel that the knowledge of the crowds and market is the extra doubtless consequence? I personally suppose that we’re extra more likely to see a market disconnected from fundamentals at this cut-off date.

Larson: I’m glad you introduced that up as a result of the commonly accepted narrative appears to be okay, we skirted recession. It seems like we have the Fed really by some means managing a gentle touchdown for the primary time in eternally. Would it not be truthful to say that you simply take the opposite facet of that? Or how do you see issues evolving over the course of this yr?

Inexperienced: So, I believe that there are parts of that. I imply, any time that you’ll be able to forestall a recession for an prolonged time frame, you see issues like we simply noticed, which is buying orders or, you understand, sentiment amongst companies which have allowed their inventories to be drawn down as a result of they’re involved about issues. You see that finally they’re pressured to return into the market and purchase stuff, proper? And that is contributed to a number of the rebound within the financial knowledge that we have seen.

In different areas – and I might deal with some that Jerome Powell very explicitly talked about this weekend on 60 Minutes, as you highlighted – within the labor market we’re really getting actually disjointed knowledge. I believe that is vital on a few fronts. One, due to the inflation and wage will increase that we have seen, we’ve not really achieved issues like alter unemployment advantages to inflation ranges.

And because of this, the unemployment advantages have fallen in actual worth dramatically. The state of California, the place I owned a house most lately and really bought it and I am at the moment wandering the earth, is form of the simplest technique to describe my trajectory. Within the state of California, the utmost unemployment advantages over the course of any 12-month interval is about $11,000. That is 25% of the poverty degree for a single particular person within the state of California. Because of this, the speed of submitting for issues like unemployment claims is actually low. It is about 25% of people who find themselves at the moment unemployed in California are submitting for unemployment claims. That is creating complicated knowledge.

The latest robust jobs report that we noticed was largely resulting from seasonal adjustment components being reintroduced to replicate the truth that the pandemic principally screwed with the entire seasonal adjustment components that we have traditionally had. And apparently sufficient, if we take a look at that very robust employment report and we evaluate that with the family survey, which is completed by asking people as in comparison with companies, they really are indicating that full-time employment fell in that. So we’re now really seeing this unbelievable dichotomy between falling full-time employment versus the BLS telling us that payrolls are increasing at a comparatively fast fee previously couple of months.

Once more, all of the proof means that the payroll knowledge really has some basic flaws in the way it’s constructed and the way it behaves at these turning factors. And the place now we have seen the precise changes, not the seasonal estimation-type adjustment – even on this final report, we noticed that ballot decrease. The primary quarter of 2023, we noticed 350,000 jobs taken out even after all of the downward revisions that we noticed over the course of 2023.

So, we’re simply coping with some actually unsure info. And I might warning those that, like, my largest concern is that the Fed has principally hiked super-aggressively after having not hiked in any respect or modified financial coverage in response to the preliminary waves of inflation. And now we’re simply presuming it has no impression by any means, which might be a really unusual consequence in historical past, to say the least.

Larson: Received it. Let’s shift gears slightly bit to a number of the different matters you’ve got weighed in on lately. Geopolitics, for instance. The US-China relationship, how issues going there, what would you provide on that entrance? Do you suppose that that is going to be an enormous concern for international buyers shifting ahead because the yr goes on?

Inexperienced: Properly, I believe it has been notable that there hasn’t been contagion, successfully, proper? That now we have seen the Chinese language inventory market and the Chinese language financial system, whereas ostensibly on headline numbers remaining very robust, we have really seen actually disappointing ends in the information that we will really observe for China, issues like commodity consumption, and so forth.

I might simply warning China that, you understand, all of us stroll into varied service institutions and see the signal that claims the client’s all the time proper. Proper? And we’re the client because it pertains to China. And changing China within the provide chain is definitely proving to be comparatively easy and comparatively straightforward. We have outsourced or reshored into locations like Mexico and Canada. We have moved manufacturing away from China into areas like India and Vietnam. And we appear to be doing that with comparatively few disruptions.

That is creating situations for China that, I believe, are fairly difficult. It is forcing them to hunt out partnerships with issues just like the BRICS, which is principally a bunch of autocratic regimes that do not wish to really comply with, you understand, conventional requirements or what we might consider as Western requirements. These entities are more and more getting remoted. They’re more and more experiencing adversarial occasions, and america is slowly pulling away, simply because it did in opposition to the Soviet Union, proper.

Central planning would not work. It would not work after we do it domestically. It would not work after we do it internationally or in international nations. It might briefly really feel such as you’re getting one thing actually improbable completed. However you are failing to consider all the data that is contained in costs or particular person habits. And because of this, we simply proceed to separate when it comes to financial efficiency.

Larson: Now, once more, I wish to shift gears to a different matter that was lately in your Substack. Nice work there, I do prefer to comply with that. Bitcoin and what’s been occurring within the crypto area, I imply, buyers are paying consideration once more after an extended interval the place all these scandals and stuff was occurring. What are you considering there? It looks as if you’ve got typically had a skeptical tone about Bitcoin and the longer term for crypto, even with all of the ETF cash that is form of flowing into that area.

Inexperienced: Sure. So look, the issue with Bitcoin is that there is really, sadly, a really basic flaw within the underlying rationale behind Bitcoin’s creation, which is a peer-to-peer cost system. The adoption of a tough restrict when it comes to the variety of Bitcoin that may ever be created really, sadly, makes it actually unsuitable for peer-to-peer cost.

We have really seen someplace round 15% of all Bitcoin that theoretically is finally going to grow to be accessible has already been misplaced. And we will simply mechanically suppose by way of these underlying dynamics of what occurs if there’s just a few frictional loss or the equal of gold cash falling into the ocean and by no means being recovered, proper? We have seen that traditionally in many fiscal techniques.

So, there’s nothing stunning that is occurring there. However that tough cap, the entire inflexibility of the financial provide, really has a basic flaw in it. It successfully would not permit any reward for human ingenuity, proper? The gold commonplace would reply to alerts, it says the gold value is rising. In different phrases, the coin worth is falling or the greenback worth is falling. That encourages folks to go discover extra gold. You do not have the equal in Bitcoin, proper? There isn’t a reward for human ingenuity. And what you really get a reward for is strictly what they let you know to do. To “HODL” – Maintain on for Pricey Life.

Holding cash beneath your mattress might theoretically permit you to keep away from shedding it in different investments, nevertheless it’s horrible for society. And so Bitcoin really at its core is an anti-investment surroundings. I believe that is a foul concept, and I believe the information will finally present that, you understand, this has been a speculative bubble like many who got here earlier than it. It simply, sadly, it may result in much more social outrage as a result of the narrative that is been constructed round is the one approach this fails is that if governments assault it. I believe that is a really caustic message to truly ship out to the general public.

Larson: I do wish to contact briefly in your take, and the commentary and analysis you’ve got achieved, on passive versus energetic investing. Earlier than I do shift to that, although, if you take a look at the macro panorama for the remainder of 2024, is there something that stands out to you as possibly an enormous alternative? And on the flip facet, an enormous danger, one thing that you simply’re primarily fearful about at this level?

Inexperienced: Properly, I imply, look, I believe the largest dangers that I stay involved about are in that geopolitical framework, or let me rephrase it. One of many largest dangers I am fearful about is within the geopolitical framework because it turns into more and more obvious that China is being remoted, that China is being pushed away from its provide relationships. And finally, do not forget that China, with a falling inhabitants, wants to determine learn how to supply demand from abroad as a way to continue to grow and gaining.

Properly, their, candidly, unhealthy habits on the political stage has created situations beneath which fewer and fewer markets can be found to them. And because of this, they may search insurance policies designed to open up these markets that embrace issues like capturing bullets. Sadly, I believe that is one of many largest dangers that we see. We noticed that with Russia. We have seen that with outbreak of violence within the Center East. These kind of behaviors are comprehensible and considerably predictable in these kinds of situations, however they’re finally, you understand, not good for anybody within the recreation.

The second danger is definitely tied to my work round passive investing. The thought of what are the implications of the expansion of successfully senseless methods that function off of the world’s easiest algorithms. Did you give me money? In that case, then purchase. Did you ask for money? In that case, then promote. That is all passive “investing” is. And it is actually vital for buyers and people to know that the idea behind passive investing really depends on passive buyers by no means transacting. That is actually the definition within the literature, is any person who by no means transacts.

Properly, each time you ship your paycheck to Vanguard, they’re transacting. So, they are not passive buyers in any respect. They’re really energetic buyers that function off of guidelines that change behaviors in markets. And sadly, they’ve grown to the size that we’re now really beginning to actually see that represented in market habits.

Larson: Properly, yeah. And, you understand, I am glad you alluded to that. I believe that that concern once more, that is form of how I first stumbled throughout your work, is a number of the commentary you had there. And I believe it is crucial for buyers. So, the implications? What is the nugget of knowledge that you simply’d cross on to folks which can be making an attempt to navigate a market dominated by passive?

Inexperienced: Yeah. So I believe that there is a few parts, proper? Keep in mind, once more, like the principles of passive are: Did you give me money? In that case, then purchase. Did you ask for money? In that case, then promote. The giving of money is a perform of incomes. The asking of money tends to be a perform of asset degree. So, when asset ranges rise much more quickly than incomes do, as we have seen inside the U.S. inventory markets, that raises the danger that withdrawals exceed contributions. And the one response to that’s falling costs.

We have seen a couple of examples of that traditionally. Now we’re really confronting the realities of a passive share that has grown massive sufficient that the pressures of the retirement of the Child Boomers are literally beginning to present indications that it might result in these flows changing into destructive.

And if that occurs, the implications for markets are, you understand, one, unsure as a result of we’ve not seen that kind of structural occasion occur earlier than. However no less than my fashions round the way it behaves result in vital stress that makes U.S. markets look rather more like the cash exiting the Chinese language inventory market has skilled, which is a horrific bear marketplace for years and years and years that fails to answer virtually any measure that is put ahead, proper.

We have now to acknowledge that transactions usually are not passive investing. And so, if you take that cash out, it’s a must to be ready for the truth that you your self are going to impression that market. And I believe that is one thing that most individuals usually are not conscious of.

One other approach to consider it, and we used this lately is, keep in mind the statements that now we have from Internet 2.0 – for those who’re not placing within the work, for those who’re not making the cost, for those who’re not paying for the service, you are the product. And that is actually true in passive investing. Vanguard and BlackRock don’t make cash on three foundation level administration charges. What they’re really earning profits on is the securities lending operations related to the possession of these belongings.

In different phrases, lending it out to hedge funds or others, they’re preserving a few of these proceeds for their very own earnings. You are getting a fraction of it returned within the case of one thing like Vanguard that contributes to the very low price and outperformance. However on the similar time, you might be destroying the energetic supervisor neighborhood that it depends on, proper?

So, that is an unsustainable course of. Individuals want to concentrate on that and they should begin eager about how do I shield myself in opposition to the generational options that we’re about to see?

Larson: Properly, I believe that is an amazing place to wrap up. Some nice recommendation there.

So, Mike, thanks a lot in your time once more. Thanks all for watching.

An enormous power shock following Russia’s invasion of Ukraine in 2022 added to inflation pressures that ravaged eurozone economies following the onset of the COVID pandemic. Switzerland, in the meantime, stood aside.

Eurozone inflation peaked at 10.6% in October 2022. Swiss inflation by no means exceeded 3.3%, topping out in July-August 2022. (The U.S. shopper value index peaked at 9.1% 12 months over 12 months in June 2022.)

See: International inhabitants decline will drive up inflation long-term, ECB’s Isabel Schnabel says

Two components labored in Switzerland’s favor, mentioned Lucie Barette, economist at BNP Paribas, in a Wednesday notice.

First, fossil fuels make up solely 2% of Switzerland’s power combine versus 38% for the eurozone. Second, standing outdoors the euro, a robust Swiss franc additionally stored costs in test (see charts under).

BNP Paribas

Barette broke down how Switzerland’s power combine helped insulate the financial system from surging oil and gasoline costs.

“The burden from hydropower power (68%), nuclear power (19%) and photovoltaic and wind power (11%) has enabled the Swiss financial system to be reasonably impacted by the rise in gasoline costs from Russia and the surge in oil costs,” Barette mentioned.

Power value inflation in Switzerland hit 29% year-over-year at its highest between 2021 and 2022 versus 44% within the euro space over the identical interval. Russia accounted for simply 41% of Swiss gasoline imports, or simply 4% of the nation’s complete power combine.

The economist famous that power additionally accounts for a decrease share of Swiss family shopper spending. Which means the burden assigned to its contribution when calculating inflation is robotically decrease than within the eurozone (5.5% in comparison with 10.2%, respectively).

In consequence, the power element solely contributed 38% to Switzerland’s headline inflation on common, in contrast with 54% within the euro space.

The primary-round results of this shock have then unfold to the opposite elements of the eurozone’s value index. Nevertheless, because the rise in power costs has typically been contained in Switzerland, no important will increase have been seen within the meals and core elements both, Barette wrote.

After which there’s the Swiss franc USDCHF, +0.18% EURCHF, +0.32%.

It’s appreciation additionally helped to include inflation by decreasing the price of imported items and providers and helped the nation get a good firmer grip on costs of imported oil and gasoline, that are largely traded within the euro and greenback, she mentioned.

The restricted rise in costs, in the meantime, allowed the Swiss Nationwide Financial institution to turn out to be of of the final central banks to emerge from interval of damaging rates of interest, Barette mentioned, noting the SNB has hiked charges simply 5 instances, or 250 foundation factors in complete, since mid-2022. It’s nominal rate of interest stands at 1.75%, leaving its actual, or inflation-adjusted, price in damaging territory with inflation standing at round 2% year-over-year on the finish of 2023.

I’ve a banking query for which I want to get additional clarification. I obtained an insurance-claim examine for $22,000, written in opposition to a Financial institution of America account.

On Tuesday morning, I deposited the examine into my checking account. However not one of the funds will probably be out there till basically 5 enterprise days later.

Why does it take that many days for an inside “your department to my account” switch of funds? Aside from verifying the provision of the funds, what’s taking place that requires 5 days?

Curious Buyer

“Checks are an old style cost methodology, and depend on extra archaic processes to clear.”

MarketWatch illustration

Newest Moneyist: ‘I wish to shield my household’: My rich father, 49, is marrying his third spouse. How do I broach the topic of my inheritance?

Expensive Curious,

Provided that settling the common insurance coverage declare can take wherever from 30 days or extra for car insurance coverage to just about 5 months for householders insurance coverage, I’m assuming your query about your examine taking 5 days to clear is as a result of a) you’re merely curious as to the mechanics of paying by examine or b) you’ve waited so lengthy by this level that the ultimate days seem extra torturous than the previous months.

When a financial institution takes time to course of a examine, it’s doing so to make sure the examine’s validity. Checks are ripe for fraud. In truth, the Higher Enterprise Bureau recommends signing checks in black gel ink, which it says is tougher to tamper with than common blue or black pens. “The Crown” actress Claire Foy lately refused to signal an autograph in blue ink; some specialists say blue biro is less complicated to scan for nefarious functions, whereas others say such considerations are overblown.

Checks are an old style cost methodology, and depend on extra archaic processes to clear. “We might assume a maintain has been positioned on the examine referenced,” a Financial institution of America spokesperson instructed MarketWatch. “A maintain could be positioned on a examine for quite a lot of causes — the quantity of the examine, considerations in regards to the validity of the examine, and many others. The maintain permits us time to analysis and confirm the examine, together with contacting the maker of the examine if wanted.” Learn extra right here.

Paper checks depend on a legacy community

Paper-based funds depend on a legacy community to course of and return checks. As an illustration, an income-tax refund can take wherever from three to eight weeks to reach. The paying financial institution has a sure period of time to confirm that the examine is legitimate and approved. If the examine will not be payable, it’s returned and the financial institution will not be notified till the examine is returned. It could be unwise for the financial institution of deposit to withdraw cash primarily based on the examine’s quantity earlier than its validity is established.

Federal legislation additionally permits the financial institution to carry among the cash for a time frame, relying on the kind of examine and the quantity. For a examine just like the one you obtained from the insurance coverage firm, banks should typically make the primary $5,525 out there by the second enterprise day after the “banking day” of deposit, though there are exceptions that permit the primary $5,525 to be held longer. An quantity over $5,525 could also be held even longer than that.

A standard rip-off: Shoppers are fooled into cashing a examine for a 3rd social gathering. The scammer tells an individual with a U.S.-based checking account that they inherited a big sum of cash, however should deposit the quantity and wire the scammer a portion of the funds to be able to obtain a beneficiant fee. Nonetheless, the examine is returned and the client is on the hook for the withdrawn funds. (This New Yorker story on the topic will provide you with goosebumps.)

And in case you are a sufferer of a rip-off? Contact your financial institution, file a police report, and put a fraud alert in your credit score stories to stop any additional injury by a foul actor who could have entry to your private particulars. Even in case you are lucky sufficient to have the cash returned, it might take months. That, I hope, places your five-day wait into perspective. Congratulations on receiving your $22,000 insurance coverage payout. No matter it’s for, I hope you take pleasure in placing it to good use.

You may e-mail The Moneyist with any monetary and moral questions at qfottrell@marketwatch.com, and comply with Quentin Fottrell on X, the platform previously often known as Twitter.

Take a look at the Moneyist non-public Fbgroup, the place we search for solutions to life’s thorniest cash points. Submit your questions, inform me what you wish to know extra about, or weigh in on the newest Moneyist columns.

The Moneyist regrets he can not reply to questions individually.

Earlier columns by Quentin Fottrell:

My spouse and I bought our house to her son at a $100,000 low cost. He’s now promoting at a $250,000 revenue. Do I ask for a lower?

‘If I say the sky is blue, she’ll inform me it’s inexperienced’: My daughter, 19, will inherit $800,000. How can she put money into her future?

My employer hires solely white managers and promotes folks of ‘questionable experience.’ Is that this a very good or dangerous time to leap ship?

U.S. inventory futures slipped Monday, edging backwards after megacap company earnings led to a recent file excessive.

What’s taking place

Dow Jones Industrial Common futures YM00, -0.19% fell 124 factors, or 0.3%, to 38641.

S&P 500 futures ES00, -0.16% dropped 13 factors, or 0.3%, to 4968.

Nasdaq-100 futures NQ00, -0.12% decreased 38 factors, or 0.2%, to 17695.

On Friday, the Dow Jones Industrial Common DJIA rose 135 factors, or 0.35%, to 38654, the S&P 500 SPX elevated 52 factors, or 1.07%, to 4959, and the Nasdaq Composite COMP gained 267 factors, or 1.74%, to 15629. Outcomes from Meta Platforms META, +20.32% and Amazon.com AMZN, +7.87% helped elevate the S&P 500 to its seventh file shut of the yr.

What’s driving markets

Friday additionally noticed the discharge of payrolls information, which noticed a surprisingly sturdy 353,00Zero jobs created in January. That U.S. shares completed larger anyway, regardless of the bond-market weak point the roles report triggered, exhibits the emphasis that the market has been placing on earnings, in line with Mike Wilson, Morgan Stanley’s chief U.S. fairness strategist.

“We see high quality progress persevering with to outperform amid sturdy earnings revisions, notably relative to decrease high quality cyclicals and small caps. For now, the internals of the inventory market are suggestive of the concept a stickier fee backdrop is a disproportionate headwind for shares with poor steadiness sheets and an absence of pricing energy—i.e., decrease high quality cyclicals and lots of areas of small caps,” he mentioned.

Federal Reserve Chair Jerome Powell used an look on the 60 Minutes program to once more push again on the thought the central financial institution would minimize charges in March.

There’s extra financial information in retailer, coming from the ISM companies report. That report final month triggered worries concerning the financial system after an unusually low studying for the employment part.

Within the ever-evolving panorama of geopolitics, the world finds itself at a pivotal juncture marked by structural shifts that redefine world dynamics. The emergence of competing financial and geopolitical blocs stands out as a distinguished characteristic reshaping alliances and influencing worldwide relations. Catherine Kress, head of Geopolitical Analysis and Technique at BlackRock, joins Oscar to discover the macro and funding dimensions of this megaforce, the complicated interaction of geopolitics and world markets and supply insights for traders navigating this new period.

Transcript

Oscar Pulido: Welcome to The Bid, the place we break down what’s occurring within the markets and discover the forces altering the economic system and finance. I am your host, Oscar Pulido.

Within the ever-evolving panorama of geopolitics, the world finds itself at a pivotal juncture marked by structural shifts that redefine world dynamics. The emergence of competing financial and geopolitical blocs stands out as a distinguished characteristic reshaping alliances and influencing worldwide relations.

As we have discovered on earlier episodes, the BlackRock Funding Institute has outlined 5 mega forces which can be shaping the macroeconomic panorama. And geopolitical fragmentation is certainly one of them.

To assist me discover this matter, I am happy to welcome Catherine Kress, head of Geopolitical Analysis and Technique at BlackRock. Collectively we’ll discover the macro and funding dimensions of this megaforce, the complicated interaction of geopolitics and world markets and supply insights for traders navigating this new period.

Catherine, thanks a lot for becoming a member of us on The Bid.

Catherine Kress: Thanks for having me.

Oscar Pulido: So Catherine, we have been speaking to Alex Brazier from the BlackRock Funding Institute, and one of many issues that he is been mentioning, and that truly has been a standard theme all through numerous our episodes, have been the mega forces of which there are 5, synthetic intelligence, getting old demographics, the transition to a low carbon economic system, the way forward for finance, and final however not least, geopolitical fragmentation. Discuss to us a bit of bit concerning the geopolitical panorama and what’s altering.

Catherine Kress: So, I feel it is vital to take a step again and for those who suppose actually to the final half decade or so, it is clear that we have had these cascading occasions which can be actually constructing on one another and now dangle over the worldwide economic system.

We had the US commerce wars again in 2018, 2019, which prolonged into the Covid pandemic, Russia’s invasion of Ukraine, and now the outbreak of struggle within the Center East. These occasions are actually beginning to construct on one another and drive structural change within the world economic system. Our BlackRock view is that geopolitics from an funding perspective has develop into a persistent and structural market danger.

We noticed final 12 months S&P 500 executives use the phrase geopolitics 12,000 instances, which was up 3 times relative to 2 years in the past. In case you take a look at our proprietary BlackRock geopolitical danger indicators, we see them hit their highest degree within the final 12 months. All through historical past, the affect of geopolitics on markets, economies has been pretty short-lived. It has been modest, markets have tended to fade geopolitical shocks once they occur. We really did a examine a number of years in the past throughout the funding institute of historic danger occasions, and that is what we discovered that these occasions had a reasonably short-lived, oblique market affect.

We see at the moment’s occasions as completely different. We consider that they are driving structural long-term change, and the world order that is rising actually stands in sharp distinction to this post-Chilly Struggle interval, which was characterised by US hegemony, constructive and productive relations between main nations, decrease commerce boundaries, ever growing globalization. We see at the moment’s atmosphere as completely different, it is pushed by the emergence of competing financial and geopolitical blocs, competitors between these blocs and more and more much less worldwide cooperation.

Oscar Pulido: You talked about the occasions that you simply look again on over, I think about, many many years. And the truth that the affect on markets was modest and short-lived, however you have additionally stated we’re in a structurally completely different world with respect to geopolitics. So is it truthful to say that going ahead market affect might be much less short-lived and extra impactful?

Catherine Kress: Positive, I imply this can be a dialogue that we’re having proper now: has the atmosphere modified that a lot that markets needs to be treating geopolitical occasions otherwise? Our view is, sure. The world at the moment is much more linked than it was once 4 or 5 many years in the past. So, a danger or a disaster in a single a part of the world can actually emanate and have ripple results to different areas and different points.

Oscar Pulido: You talked about the Russia, Ukraine struggle, folks noticed their meals costs going up and a few of that’s due to the manufacturing of grains in that a part of the world that was impacted. You additionally talked about competing financial blocs, competing geopolitical blocs which can be being shaped. So, discuss a bit of bit extra about that evolution.

Catherine Kress: So actually, during the last a number of years, we have seen the rise and emergence of those competing financial geopolitical blocs. This is likely one of the key fixtures of this fragmented panorama. On the one hand, you will have the US which is as unified because it’s ever been with its allies in Europe and Asia.

You see that with the growth and solidification of NATO in response to Russia’s invasion of Ukraine. We have seen the rise of multilateral fora like AUKUS and the Quad, however in the meantime now we have China and Russia who’re cooperating extra intently than they’ve, and so they’re partnering with nations like Iran and in some circumstances North Korea. These powers are working collectively extra intently than they’ve in many years, and that is one thing that we have actually seen evolve and deepen during the last a number of years.

I discussed Russia and China rising significantly shut. There’s been some fascinating knowledge factors not too long ago that present that. So, for instance, China Russia greenback denominated commerce final 12 months hit $240 billion, which was 26% enhance from a 12 months earlier. At this time, China trades extra with Russia than it does with Germany. In case you take a look at China’s exports of transportation gear particularly to Russia, that is up 800% since Russia’s invasion of Ukraine. And we now see that Chinese language vehicles make up 55% of the Russian market.

However I discussed this casual alignment, deepening as nicely between Russia, China and North Korea and Iran, and there is some fascinating knowledge factors right here as nicely. For instance, Iran has develop into a principal provider of drone expertise to Russia. We have seen North Korea present extra munitions to Russia in its invasion of Ukraine than Europe has offered to Ukraine. And Russia’s offering its companions with provides too, for instance, low-cost power, pure gasoline. More and more, there’s considerations about Russia exporting navy expertise and gear to Iran and North Korea. So we’re seeing these blocs harden and so they’re more and more aggressive with one another.

Oscar Pulido: And on the similar time that these blocs are forming, I feel there’s one other time period that you have used, that are these multi-aligned nations, which can be additionally creating. I am considering of those nations as I feel they’re pals with everyone, or not less than possibly they are not taking a specific facet in relation to a few of these financial blocs. However possibly assist make clear, once we say a multi aligned nation, what does that imply and what are some examples of a few of these nations?

Catherine Kress: So, these are the nations that have not taken sides within the contest between the US and China, or essentially adopted the western place on Russia. They’re very completely different from the non-aligned motion of the Chilly Struggle. So, we have chosen the phrase multi-aligned as a result of we see these nations as essentially completely different.

The non-aligned motion of the Chilly Struggle was way more about statements and posturing and protests. At this time, the multi-aligned nations are main economies on the earth which have a whole lot of energy and affect.

The Economist calls them the “Transactional 25” or the T25. Collectively, the T25 make up greater than half the world inhabitants and a couple of fifth of world GDP, which is greater than the EU. The multi-aligned nations are pragmatic. They’ve a fluid transactional strategy to the world. In a manner, they’re unsure concerning the future distribution of energy, and they also’re hedging their bets and aligning with each blocs in keeping with their nationwide pursuits.

An particularly vital grouping of multi-aligned nations are the nations within the Center East. So, years of excessive oil costs have made the nations, the Gulf Oil producers particularly, actually main sources of liquidity within the markets. we expect that they are at an inflection level. They’re going to be the final one standing in fossil fuels. They’ve huge alternative if they will proceed to take care of fiscal self-discipline, if they will handle regional tensions.

However one other multi-aligned participant to look at is India. India’s already the world’s most populous nation, its working inhabitants is anticipated to hit a billion inside a decade. It is projected itself as a pacesetter of the worldwide south.

So, now we have demographics alongside macroeconomic stability, in addition to a deal with bodily and digital infrastructure that I feel make India rather well poised, to compel world progress going ahead.

Oscar Pulido: One of many issues that emerged post-Covid was this recognition on the a part of corporations to convey manufacturing nearer to dwelling. Prioritizing resiliency greater than price, I feel is a whole lot of what we have talked about with a few of our visitors on the podcast. And a few folks discuss this as de-globalization that after many many years of globalization, now we’re stepping into reverse. Possibly Alex Brazier has talked about it because the rewiring of globalization. So, what’s the proper time period and do you agree with this and what are the form of the impacts if this development in truth is going on?

Catherine Kress: I very a lot agree with the framing because the rewiring of globalization. I do not suppose it is right to say that the world is deglobalizing, that we have hit the top of globalization. There are measures of globalization which have receded. For instance, commerce as a share of GDP for the reason that monetary disaster. However there are different areas the place we’re seeing fast globalization like digital commerce and companies.

However I do suppose it is truthful to say that the system of globalization has been politicized and that we’re seeing points, as you stated, like nationwide safety resilience, more and more making their manner into financial coverage, enterprise resolution making, and we’re seeing nations and corporations leverage focused insurance policies like export controls, tariffs, funding restrictions, commerce agreements with like-minded nations to realize financial and coverage goals.

So, our view is that globalization is rewiring, and this can be a dynamic that we had been hypothesizing for a while that nationwide safety and resilience would drive this rewiring and more and more play virtually a much bigger function than conventional financial and market elements like pure price effectivity, comparative benefit, in provide chain choices.

And more and more, there is a important mass of research popping out that helps that speculation. That coverage and geopolitics are driving this rewiring of globalization, and at a excessive degree, it reveals that commerce is not essentially declining, however it’s shifting, and we’re seeing this in a few particular areas.

First, we’re seeing that commerce between geopolitical blocs is slowing. So, since Russia’s invasion of Ukraine, the World Commerce Group has reported that commerce between geopolitical blocs has grown 4-6% slower than commerce throughout the geopolitical blocs. And at the moment, China’s buying and selling extra with creating nations than it’s with the US, Europe, and Japan mixed. So, we’re seeing that type of shift among the many blocs.

Second, we’re seeing some diminished dependence on cross border suppliers. So, there is a component of that reshoring that is going down. Third, and that is what I feel is essentially the most fascinating and presents an funding alternative, which is that as we see commerce between the blocs decline, we’re seeing the rising up of nations, which Bloomberg has known as the connector nations.

These are the nations which can be injecting themselves into world provide chains and turning into intermediaries. So, as US direct sourcing from China declines for instance, nations like Vietnam, Mexico, Indonesia, Morocco, Poland are inserting themselves into world provide chains, and China’s buying and selling extra with them and so they’re buying and selling extra with the US.

So, the US is not essentially decreasing commerce publicity to China solely, but it surely’s being extra intermediated. These nations, in accordance with one Bloomberg evaluation, reported $Four trillion in financial output in 2022. They’ve all seen commerce develop above development for the final 5 years. So, they mirror a very fascinating and vital alternative going ahead.

Oscar Pulido: So, let’s return to the truth that you stated a few of these geopolitical adjustments, or all of the geopolitical adjustments you are mentioning are extra structural in nature. That this is not only a one- or two-year sort of development, however that, the world is essentially shifting. So, what does that imply for future geopolitical shocks, like how ought to an investor or simply people be enthusiastic about them versus what they’ve seen previously?