“I completely suppose it’s the suitable transfer to make use of a W-2 worker workforce whenever you care about delivering a greater product to your prospects.”

— Mike Evans, co-founder of Grubhub and Fixer

Mike Evans co-founded Grubhub Inc., one of many high food-delivery platforms within the nation after DoorDash Inc. DASH, -1.53% and Uber Applied sciences Inc.’s UBER, -0.72% Uber Eats.

In his new ebook, “Hangry: A Startup Journey,” he recounts how conflicted he ultimately grew to become about Grubhub and the course it took on its path to an preliminary public providing, together with the corporate’s shift to utilizing drivers it considers unbiased contractors. Earlier than that, Grubhub merely allowed on-line ordering from eating places that already provided supply. For that and different causes, Evans walked away from the corporate shortly after it went public in 2014, based on his ebook.

So it’s no shock that in an interview with Yahoo Finance printed Friday, Evans reiterates that he thinks the gig-economy mannequin of solely utilizing contractors as an alternative of staff is flawed.

“One of many issues I might argue very strongly for is that your greatest drivers ought to really be your staff… so you’ll be able to ship a differentiated product to the shopper,” Evans mentioned in that interview. “That the meals will get there sizzling, will get there fast and will get there safely — these items matter to the shopper.”

He contended that there’s barely any differentiation between DoorDash, Uber Eats and Grubhub, and that the businesses should compete in opposition to each other on advertising and marketing as an alternative.

In 2017, Evans based Fixer, an on-demand platform for locating helpful individuals for when prospects want issues fastened round the home. These individuals are educated staff of the corporate, not contractors, as a result of he mentioned “the standard of the work is a very essential issue. And also you simply can’t management that throughout the contractor market.”

Requested about whether or not he feels that means about ride-hailing drivers being thought-about unbiased contractors by Uber and Lyft Inc. LYFT, +1.57% — an enormous authorized and regulatory difficulty within the nation and around the globe — he mentioned sure.

See: ‘Gig work’ rule is in Biden administration’s crosshairs

“A hybrid mannequin is the way in which to go,” Evans mentioned within the interview, then went on to precise his concern about gig employees. He acknowledged the employees can profit from the pliability being an unbiased contractor brings, however much less so if they’re doing gig work full-time.

He added: “The gig economic system is nice if it’s your aspect hustle. But when it’s a profession selection… I’m unsure that when you work 40 hours per week for 5 years at Uber, when you’re in a greater place than the day you began from a marketable-skills perspective.”

In his ebook, Evans additionally recounts getting disillusioned with the corporate’s enterprise capital traders pushing for Grubhub to take as large a minimize from eating places because it presumably might. He even thought-about leaving the corporate earlier than the IPO, telling one VC that “the corporate is headed down a path I don’t agree with.”

European firm Simply Eat Takeaway.com JET, -2.28% purchased Grubhub in 2020; the acquisition closed final 12 months.

Additionally: Unions should reckon with racial inequality and converse to ‘a extra marginalized workforce,’ former U.S. labor board chair says

This text was printed on Dividend Kings on Tuesday, December 27th.

—————————————————————————————

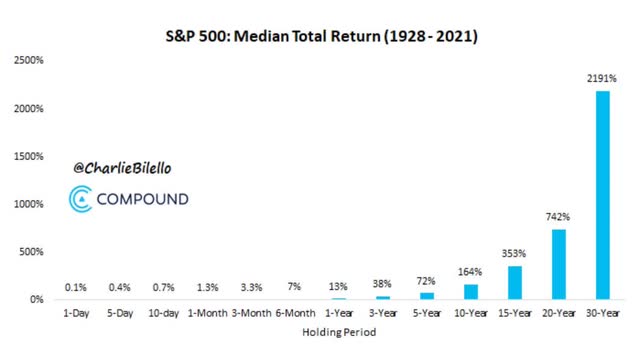

$366,000, an sum of money that most individuals would envy. That is how a lot I’ve personally misplaced in a lifetime on account of hypothesis and day buying and selling.

That was earlier than I discovered the straightforward fact about easy methods to really retire wealthy and keep wealthy in retirement.

Many individuals consider Wall Avenue as a on line casino, and they’re proper. Within the brief time period, something can occur. However in the long run, it is all about stacking the chances in your favor.

Billion-dollar casinos aren’t constructed on the backs of winners, however from long-term chances, particularly that the home at all times wins.

Charlie Bilello

Within the short-term, shares can do something, particularly in a bear market. Within the long-term, barring an apocalypse, they solely go up.

And have you learnt the one factor higher than shares for the long-term if you wish to retire in security and splendor?

Legacy Analysis

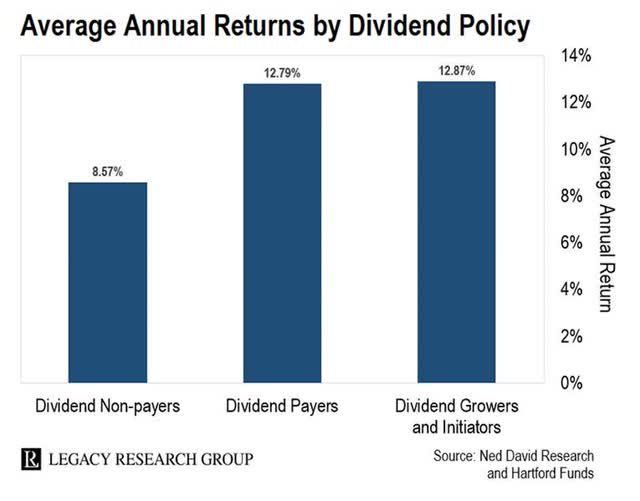

Dividend development blue-chips. Why? As a result of a diversified dividend development portfolio harnesses the facility of everybody on earth to fund your monetary desires.

How’s that? Take into account the Dividend Kings ZEUS Revenue Development portfolio, which owns stakes starting from 0.01% to six% within the 578 biggest firms on earth.

There is not an individual on earth that is not a buyer of this portfolio. Each one of many Eight billion individuals on the earth is sending dividends to this portfolio each quarter.

All through historical past, each emperor and dictator has dreamed of conquering the world and bending all of humanity to their will. Guess what? When you personal a blue-chip revenue portfolio you could have completed simply that.

Each individual on earth is voluntarily sending you cash, from each nook of the globe, so that you could grow to be financially impartial.

You do not have to kill or conquer anybody as a result of, by means of the magic of blue-chip dividends, all of humanity is united behind one easy aim. Letting you retire in consolation or splendor and develop steadily richer over time.

Right now I need to spotlight two tremendous star high-yield dividend blue-chips which are firing on all cylinders proper now, Amgen Inc. (AMGN) and Broadcom Inc. (AVGO). These aren’t essentially the most undervalued high-yield blue-chips you should purchase, however they’re two of the best high quality and most secure.

Not only for 2023, a recession yr, however for doubtlessly many years of superior revenue, revenue development, and life-changing returns.

So let me present you why Amgen and Broadcom are two of the very best high-yield dividend blue-chips you should purchase right this moment to assist construct your revenue development empire and obtain your monetary desires.

Amgen: A World-Beater Biotech Blue-Chip

Amgen is not a dividend aristocrat…but. It started paying a dividend 11 years in the past. But when this world-beater, high-yield blue-chip would not grow to be an aristocrat in 2037, I will eat my hat.

Why is Amgen such an exquisite dividend development blue-chip?

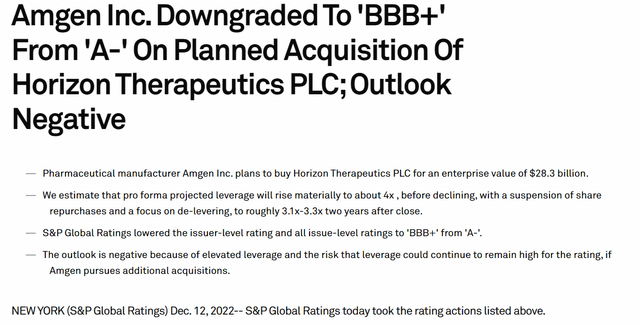

Let’s begin with the Horizon Therapeutics (HZPN) mega-deal for $28 billion, its largest acquisition ever.

S&P

Amgen will tackle a variety of debt to fund this deal, which is able to imply elevated leverage for the subsequent few years.

We anticipate the corporate to droop share repurchases and deal with debt reimbursement over the subsequent a number of years. We undertaking that leverage will decline to three.1x-3.3x two years publish the shut of the acquisition, nonetheless barely excessive for the ‘BBB+’; ranking. We’d contemplate reducing the ranking additional if leverage stays over 3.3x past the 2 years.” – S&P

Nonetheless, this deal makes a variety of sense from the attitude of future development.

The acquisition improves Amgen’s portfolio, including a number of fast-growing commercialized medicine. Horizon’s key belongings overlap with Amgen’s energy in auto-immune illnesses and leverage its presence in nephrology. We anticipate Tepezza and Krystexxa to develop at a double-digit fee over the subsequent few years. This may probably increase Amgen’s development fee, which we anticipate to speed up in 2023 with the expansion of Lumakras and Tezspire and the launch of Amjevita within the U.S.” – S&P

What concerning the unfavorable outlook?

The outlook is unfavorable due to elevated leverage and the chance that if Amgen continues to pursue extra acquisitions, leverage will stay excessive.

We might decrease the ranking if the corporate makes different acquisitions or makes a large tax settlement that may maintain leverage elevated and above 3.3x for greater than two years.

We might revise the outlook to steady if we grow to be extra sure that leverage will stay under 3.3x. This might happen if the corporate steadily reduces leverage and builds capability for future acquisitions.” – S&P

Horizon has a number of medicine already available on the market which are a great match for Amgen’s medicine available on the market. Combining medicine right into a single remedy for a affected person is turning into extra frequent, and for this reason analysts are so enthusiastic about what this mega-deal means for Amgen’s development potential.

FactSet Analysis Terminal

For context, Moody’s estimates that the pharma trade’s long-term earnings development fee is 4%. Amgen is rising virtually 4X as quick due to its Horizon acquisition.

Nonetheless, the largest potential development driver for the Horizon portfolio could possibly be improved uptake amongst sufferers with persistent thyroid eye illness; key knowledge must be accessible within the second quarter of 2023 that would broaden the penetration of this market. We additionally see important potential from Horizon’s latest key drug, Uplizna, for neuromyelitis optica. Extra potential indications in testing (like myasthenia gravis) would match nicely with Amgen’s upcoming launch of a biosimilar model of Soliris.” – Morningstar

In different phrases, Horizon is doubtlessly turbocharging AMGN’s robust pipeline of present and future medicine and can assist it keep really distinctive profitability.

FactSet Analysis Terminal

Inside just a few years, Amgen’s free money move (“FCF”) is anticipated to develop about 30% to round $13 billion. How spectacular is that?

2022 FCF margin consensus: 39%

2023 FCF margin consensus: 49%

2027 FCF margin consensus: 44%.

For context, Amgen’s present free money move margin is within the high 5% of all firms on earth. And it is anticipated to get even stronger with Horizon’s excessive margin medicine added to its arsenal.

Amgen is at the moment spending $4.5 billion on its dividend, or roughly 33% of what analysts anticipate it to be producing inside just a few years.

That leaves round $Eight to $8.5 billion per yr it could spend on de-leveraging or much less aggressive buybacks.

Or, to place it one other manner, if AMGN had been to spend 100% of its post-dividend retained free money move on paying down debt, it might pay for this complete deal in about 3.5 years.

However here is even higher information. Not solely does Amgen has a plan to soundly deleverage and obtain among the finest development charges in its trade, but it surely’s more likely to stay a double-dividend development super-star.

5-year dividend development consensus 10.2% yearly.

Amgen simply raised its dividend by 12% for 2023, and analysts anticipate it to develop one other 47% by 2027.

Meaning the at the moment beneficiant and really secure 3.2% yield might attain 4.7% on right this moment’s value by 2027.

Gurufocus Premium

That is a may enticing very secure yield for a future dividend aristocrat whose moat is as huge as they arrive.

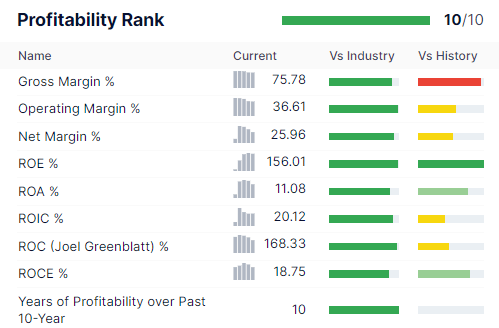

That features gross margins of 76% and returns on capital of 170%, 12X that of the S&P 500 and 65% higher than the dividend aristocrats.

Lengthy-Time period Consensus Return Potential

Funding Technique

Yield

LT Consensus Development

LT Consensus Complete Return Potential

Lengthy-Time period Threat-Adjusted Anticipated Return

Do I consider that AMGN can actually ship 17% to 18% long-term returns? It is really not as loopy because it sounds.

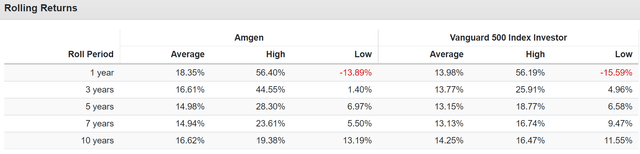

Amgen Rolling Return Since 2011 (The Dividend Period)

Portfolio Visualizer Premium

Since Amgen began paying a really secure and double-digit development dividend 11 years in the past, it is constantly delivered 15% to 18% annual returns, operating circles across the S&P.

31% Annual Revenue Development Over The Final 11 Years

Portfolio Visualizer Premium

Amgen’s dividend development over the past 11 years has been about 4X quicker than the S&P’s, an distinctive 31% per yr. That is clearly going to sluggish over time, particularly because it focuses on deleveraging.

However the level is that Amgen is actually a high-yield dividend development tremendous star, with many different admirable qualities.

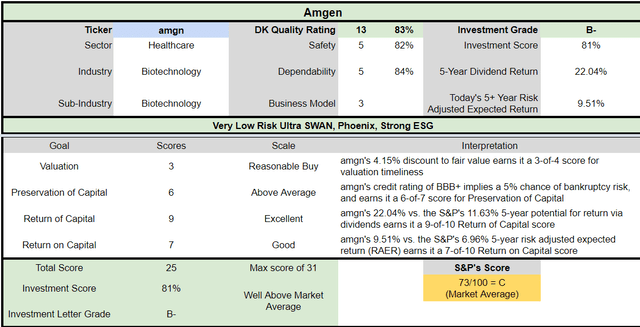

Causes To Doubtlessly Purchase Amgen Right now

Metric

Amgen

High quality

83% 13/13 Extremely SWAN (Sleep-Nicely-At Evening) High quality Drug Maker

Threat Score

Very Low Threat

DK Grasp Record High quality Rating (Out Of 500 Firms)

264

DK Grasp Record High quality Percentile

48%

Dividend Development Streak (Years)

11

Dividend Yield

3.2%

Dividend Security Rating

82%

Common Recession Dividend Minimize Threat

0.5%

Extreme Recession Dividend Minimize Threat

1.95%

S&P Credit score Score

BBB+ Adverse Outlook

30-Yr Chapter Threat

5.00%

LT S&P Threat-Administration World Percentile

97% Distinctive, Very Low Threat

Truthful Worth

$273.53

Present Value

$263.92

Low cost To Truthful Worth

4%

DK Score

Potential Cheap Purchase

P/E

14.9

Money-Adjusted P/E

10.5

Development Priced In

4.0%

Historic PE

13.5 to 15

LT Development Consensus/Administration Steering

14.3%

PEG Ratio

0.73

5-year consensus whole return potential

8% to 10% CAGR

Base Case 5-year consensus return potential

9% CAGR (About Equal to The S&P 500)

Consensus 12-month whole return forecast

4%

Basically Justified 12-Month Return Potential

7%

LT Consensus Complete Return Potential

17.5%

Inflation-Adjusted Consensus LT Return Potential

15.2%

(Supply: Dividend Kings Zen Analysis Terminal)

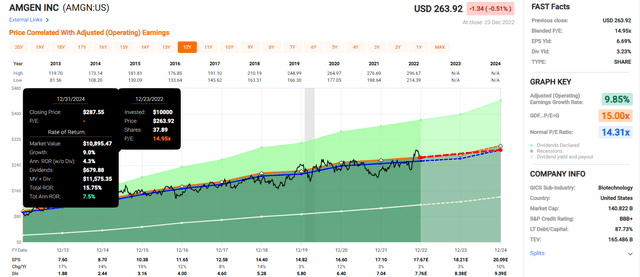

Amgen is not a discount, but it surely does symbolize a traditional Buffett-style “fantastic firm at an affordable worth.” Its cash-adjusted P/E of 10.5X is decrease than the typical personal fairness deal in 2022 of 11.3X.

For one of many widest moat pharma giants on earth, and one of many most secure double-digit rising 3.2% yields on the planet.

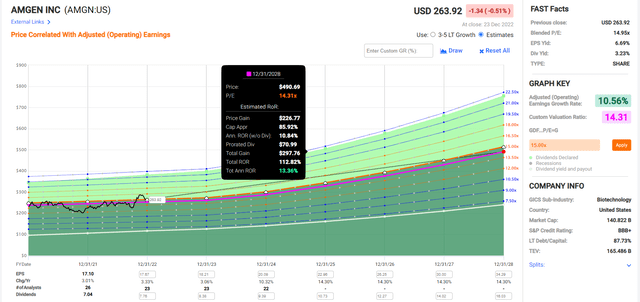

Amgen 2024 Consensus Complete Return Potential

FAST Graphs, FactSet Analysis

AMGN’s sluggish development in 2023 signifies that its short-term return potential is modest.

Amgen 2028 Consensus Complete Return Potential

FAST Graphs, FactSet Analysis

However over the subsequent 5 years, AMGN provides the potential to greater than double the market’s returns, a really enticing 13% yearly.

Amgen Funding Choice Rating

Dividend Kings Automated Funding Choice Rating

AMGN is an above-average high-yield alternative for anybody snug with its danger profile. Take a look at the way it compares to the S&P 500.

4% low cost to honest worth vs. 1% low cost S&P = 3% higher valuation

3.2% secure yield vs. 1.8% (2X greater and far safer)

roughly 17.5% long-term annual return potential vs. 10.2% CAGR S&P

about 50% greater risk-adjusted anticipated returns

2X greater revenue potential over 5 years.

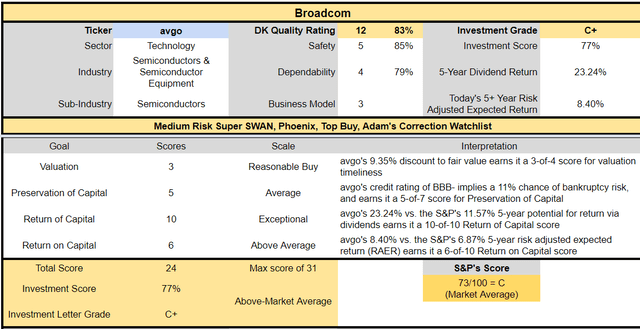

Broadcom: A Free Money Stream Minting World-Beater Tremendous Star Dividend Grower

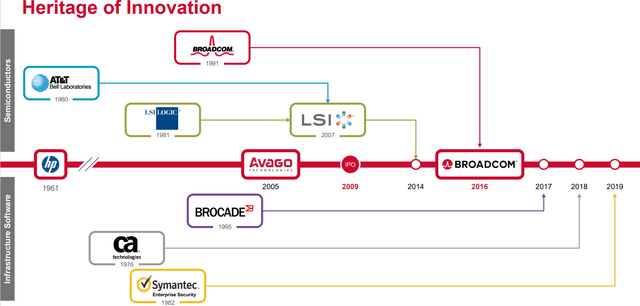

Broadcom is one among my favourite chip shares for a number of causes.

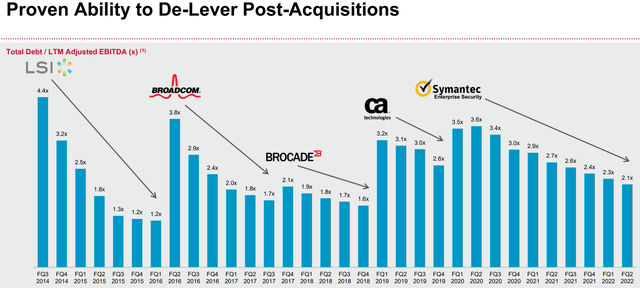

First, nobody does M&A on this trade higher than CEO Hock Tan.

Investor Presentation

Broadcom is just like the Berkshire of chip makers, making quite a few good offers which have helped to enhance the corporate’s profitability and turbocharge development.

Broadcom makes use of the money move generated from its current companies to take care of its aggressive edge in core finish markets by bolstering analysis and growth in addition to future acquisitions. As a serial acquirer, Broadcom has seemingly perfected the method of buying expertise firms with best-of-breed merchandise at enticing valuations, trimming noncore product strains to streamline the enterprise, and in the end driving value synergies.” – Morningstar

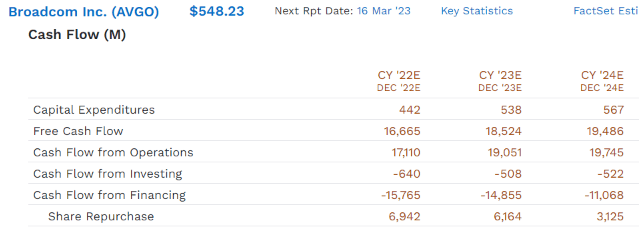

What’s extra essential for revenue buyers is that it is centered on shopping for software program firms with recurring contracted money flows. AVGO spends $5 billion yearly on R&D, rising its portfolio of 19,00Zero patents that assist it ship among the most spectacular profitability within the trade.

The $61 billion acquisition of VMWare (VMW) will imply that 50% of all gross sales are from software program, creating essentially the most steady money move within the trade.

Meaning its PE ought to proceed to rise steadily over time because it turns into extra of a tech utility.

Is Broadcom with out danger? After all not, and one of many greatest proper now could be regulatory approval for the VMWare deal.

Broadcom, VMware sink as EU opens up ‘in-depth’ investigation into $61B merger.

Each the U.S. and EU are carefully scrutinizing this deal, fearful that it’d lead to a tech conglomerate with an excessive amount of market energy.

Gurufocus Premium

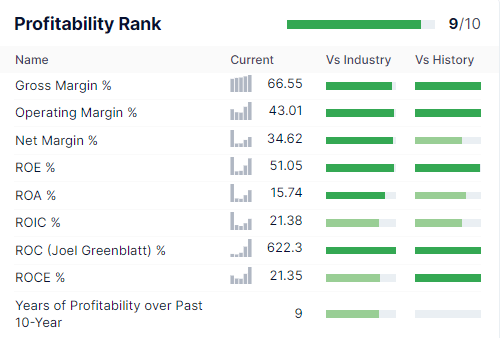

AVGO’s masterful use of M&A has helped it grow to be one of the crucial worthwhile firms on earth, in any trade. That features insane returns on capital of 622%, 43X higher than the S&P 500 and 6X greater than the dividend aristocrats.

4X greater than Amgen

FactSet Analysis Terminal

Broadcom’s free money move margins are distinctive due to its low capital-intensive enterprise mannequin.

Broadcom’s dividend is operating $7.9 billion per yr, that means that it is anticipated to retain $10 billion subsequent yr after dividends. Administration’s coverage is to pay a secure 50% FCF payout ratio and use the remainder for buybacks and de-leveraging.

49% free money move margins in 2022

high 1% of all firms on earth

2024 consensus FCF margin 52%.

Usually you anticipate 50% free money move margins from firms like Visa (V) and Mastercard (MA), not a chip maker. Not even biotechs like Amgen and AbbVie (ABBV) are capable of maintain such margins over time, a lot much less maintain enhancing upon them.

Investor presentation

There’s naturally danger concerned with debt-funded M&A, and within the arms of a lesser firm, this technique might spell catastrophe.

44% Annual Revenue Development For 11 Years

Portfolio Visualizer Premium

Within the arms of Hock Tan, Broadcom’s M&A-focused development technique has resulted in spectacular revenue development. Traders who purchased Broadcom in 2011 when it grew to become a dividend inventory now get pleasure from a 75% yield on value.

OK, however clearly, development goes to sluggish sooner or later. And that is very true if regulators block the VMware deal or ones just like it. We have already seen an tried $117 billion acquisition of Qualcomm (QCOM) nixed by the Trump administration, and the VMW deal has a possible $2.25 billion in termination charges related to it.

What does Broadcom’s development outlook seem like on a risk-adjusted foundation if it isn’t allowed to purchase VMW?

FactSet Analysis Terminal

Broadcom’s development outlook was 15.5% earlier than the EU and FTC elevated the chance of one other failed mega-deal. However 12.5% development remains to be 50% greater than the S&P 500 and about 25% higher than dividend development shares, as represented by VIG.

Lengthy-Time period Consensus Complete Return Potential

Funding Technique

Yield

LT Consensus Development

LT Consensus Complete Return Potential

Lengthy-Time period Threat-Adjusted Anticipated Return

Broadcom nonetheless provides a sexy yield rising at double-digit and the potential for 16% long-term returns. When you’re trying to turbocharge a core ETF place to spice up yield, development, and return potential, it is the most effective long-term selections you may make.

Causes To Doubtlessly Purchase Broadcom Right now

Metric

Broadcom

High quality

83% 12/13 Tremendous SWAN (Sleep-Nicely-At Evening) High quality Chip Maker

Threat Score

Medium Threat

DK Grasp Record High quality Rating (Out Of 500 Firms)

259

DK Grasp Record High quality Percentile

49%

Dividend Development Streak (Years)

12

Dividend Yield

3.4%

Dividend Security Rating

85%

Common Recession Dividend Minimize Threat

0.5%

Extreme Recession Dividend Minimize Threat

1.80%

S&P Credit score Score

BBB- Optimistic Outlook

30-Yr Chapter Threat

11.00%

LT S&P Threat-Administration World Percentile

41% Common, Medium Threat

Truthful Worth

$609.20

Present Value

$551.91

Low cost To Truthful Worth

9%

DK Score

Potential Cheap Purchase

P/E

14.5

Money-Adjusted P/E

11.4

Development Priced In

5.8%

Historic P/E

14.5 to 15.5

LT Development Consensus/Administration Steering

12.5%

PEG Ratio

0.91

5-year consensus whole return potential

14% to 25% CAGR

Base Case 5-year consensus return potential

17% CAGR (About 2.5X The S&P 500)

Consensus 12-month whole return forecast

23%

Basically Justified 12-Month Return Potential

14%

LT Consensus Complete Return Potential

15.9%

Inflation-Adjusted Consensus LT Return Potential

13.5%

(Supply: Dividend Kings Zen Analysis Terminal)

Broadcom is not an important discount proper now, simply one other Buffett-style “fantastic firm at an affordable worth.” Its 11.4X cash-adjusted P/E is what personal fairness is paying for firms now.

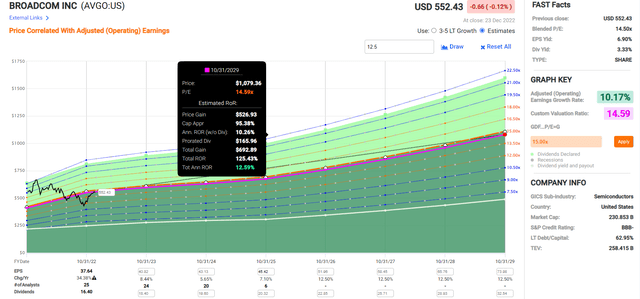

Broadcom 2025 Consensus Return Potential

(Supply: FAST Graphs, FactSet)

As a result of slower development within the subsequent few years, partially as a result of smartphone improve cycle, AVGO’s return potential by means of 2025 is roughly equal to the market’s.

Broadcom 2029 Consensus Return Potential

(Supply: FAST Graphs, FactSet)

Even at a modest low cost to honest worth, AVGO’s robust yield and regular development are anticipated to ship about 2.5X the returns of the S&P over the approaching 5 years.

Broadcom Funding Choice Rating

Dividend Kings Automated Funding Choice Rating

AMGN is an above-average high-yield alternative for anybody snug with its danger profile. Take a look at the way it compares to the S&P 500.

9% low cost to honest worth vs. 1% low cost S&P = 8% higher valuation

3.4% secure yield vs. 1.8% (2X greater and safer)

roughly 15.9% long-term annual return potential vs. 10.2% CAGR S&P

about 33% greater risk-adjusted anticipated returns

2.5X greater revenue potential over 5 years.

Backside Line: Amgen And Broadcom Are Two Of The Greatest Excessive-Yield Blue-Chips You Can Purchase For 2023 And Past

Let me be clear: I am NOT calling the underside in AMGN or AVGO (I am not a market-timer).

Not even Extremely SWAN high quality does NOT imply “cannot fall onerous and quick in a bear market.”

Fundamentals are all that decide security and high quality, and my suggestions.

over 30+ years, 97% of inventory returns are a perform of pure fundamentals, not luck

within the brief time period; luck is 25X as highly effective as fundamentals

in the long run, fundamentals are 33X as highly effective as luck.

Whereas I am unable to predict the market within the brief time period, here is what I can let you know about AMGN and AVGO.

Each are high-yield dividend superstars which are more likely to grow to be dividend aristocrats.

Each provide far superior development prospects than virtually any standard ETF or funding technique.

Each are Buffett-style “fantastic firms at affordable costs.”

Each have delivered robust double-digit dividend development for 11 to 12 years and are anticipated to proceed to take action sooner or later.

And each are fantastic examples of why world-beater dividend development blue-chips are the best-performing asset class in historical past.

When you’re bored with shedding cash in bear markets, then perhaps it is time to cease speculating and begin investing in your long-term future.

As 2022 winds down and traders replicate on a horrendous yr, they will take some consolation in the truth that the large guys had their share of misses.

Amongst them is Harris Kupperman, the president of hedge fund Praetorian Capital, who lately blogged about his 2022 calls he nailed — a selloff of huge tech names— and those who missed the mark — a sustained surge in oil costs.

Kupperman is doubling down on the latter in our name of the day, as he predicts 2023 will likely be “the yr of oil crushing all different” investments, with a barrel of crude probably hitting $200, laying that out in his AdventuresInCapitalism weblog (h/t Quoth the Raven)

Oil CL00 CL is about to complete with a acquire of round 6% in a yr that noticed U.S. benchmark futures surge to over $130 a barrel after Russia’s invasion in Europe, earlier than a gradual ratcheting decrease on recession worries as central banks fought to include inflation. West Texas Intermediate crude was buying and selling slightly below $80 a barrel on Wednesday morning.

From early 2022, he defined, “there was minimal spending development on exploration, whereas world demand has continued to rebound and develop. The postponement of my theme was primarily brought on by the surprising purge of SPR stock, together with China going offline resulting from germs. These two developments appeared destined to reverse in 2023,” he stated, including that Russian oil manufacturing is “completely impaired and certain in free fall.”

Notice, China’s quickly fading zero-COVID coverage took one other daring step on Tuesday as the federal government introduced it would begin issuing passports. Nevertheless that has additionally triggered issues about COVID unfold and inflation fallout (extra beneath).

Paying off for Kupperman had been power investments — Valaris VAL and Tidewater TDW — which he stated would prone to proceed main power markets greater in 2023 resulting from their valuations. And whereas his oil futures and futures choices positions didn’t work out as nicely, he’s affected person.

“As soon as once more, I believe it’s essential to repeat that if you happen to haven’t stress-tested your portfolio for oil costs north of $200, you’re going to endure dearly when that ought to come to go,” stated the supervisor.

Kupperman additionally foresaw continued housing market energy in 2022, however is now tossing the names he was holding within the sector that’s rolling over resulting from rising rates of interest. “Whereas I stay bullish, I’m going to attend for building exercise to backside and start its restoration,” he stated.

The supervisor additionally defined the tech rout name that he obtained proper. Since 2019, he’s been pounding the desk over what he known as “Ponzi Sector” firms — Lyft LYFT, Uber UBER and Peloton PTON that had “no capacity or need to ever develop into worthwhile.”

Learn: Lyft inventory closes decrease than $10 for the primary time; three-quarters of its valuation has been wiped away this yr

He predicted these firms would falter in 2022 and drag down the so-called “Tiger-40″ — top quality however overowned large-cap tech shares reminiscent of Microsoft MSFT, Amazon.com AMZN, Meta Platforms META, Roblox RBLX and DoorDash DASH, primarily based on high 40 holdings of hedge fund Tiger World Administration. He notes that “over-owned” fund was aped by most huge portfolio managers.

“That is seemingly brought on by an anticipated financial slowdown, resulting from quickly rising rates of interest. One might say that the market is wanting by way of a interval of over-earning and penalizing their share costs — regardless of many of those firms buying and selling at low single-digit earnings multiples on full-cycle earnings,” stated Kupperman.

Not fairly correct was his name for a “mom of all sector rotations” for 2022, as traders swap out of these high names. Worth names haven’t carried out nearly as good as he’d hoped.

“Whereas my publicity stays subdued, I’ve an incredible buying listing of near-monopoly worth names to buy when The Pause comes, if it turns into apparent that the lengthy finish doesn’t utterly panic. I’ve spent a lot of the yr constructing on this listing, however have executed little in addition to proceed to be taught the names higher,” he stated.

Total, 2022 was a yr to keep away from land mines and “battle one other day,” stated Kupperman. “For now, I need to keep conservative, follow low-risk setups and keep extremely liquid. I believe that 2023 will likely be tough for longs, particularly as oil crushes every part else,” he stated.

Learn the remainder of his weblog for extra positions that did and didn’t work out.

Learn: Listed below are 5 stock-market ‘early indicators’ that would resolve the destiny of your portfolio in 2023

The markets

MarketWatch

Inventory futures ES00 YM00 NQ00 are modestly greater, as bond yields BX:TMUBMUSD10Y pull again. The greenback DXY is flat, however surging in opposition to the ruble USDRUB as western sanctions are apparently beginning to chew, and oil CL is decrease.

For extra market updates plus actionable commerce concepts for shares, choices and crypto, subscribe to MarketDiem by Investor’s Enterprise Day by day.

The thrill

Probably the most oversold it’s ever been, and hit by one other worth goal minimize — Baird to $252 from $316 per share — Tesla shares TSLA are pointing to the primary acquire in seven classes.

And shares of AMC Leisure AMC, whose CEO Adam Aron desires to forgo his 2023 pay and get different executives to do that similar, is greater in premarket after a three-session loss. However AMC’s most well-liked fairness inventory is down about 10% .

U.S.-listed shares of Hong Kong journey group Journey.com TCOM are up after China dropped journey restrictions, although fears of a brand new wave of infections have led nations reminiscent of Japan and Italy to tighten guidelines on inbound Chinese language vacationers. The U.S. is also reportedly contemplating comparable strikes.

Learn: Chinese language are snapping up flights overseas as Beijing drops extra journey restrictions

U.S. Transportation Secretary Pete Buttigieg has vowed to carry Southwest Airways’ LUV accountable over the vacation flight “meltdown” that noticed 1000’s of flights canceled.

FTX founder Sam Bankman-Fried borrowed $546 million from Alameda to purchase an almost 8% stake in commission-free buying and selling app Robinhood HOOD, based on a information report citing court docket papers.

Pending dwelling gross sales are due at 10 a.m. Japanese.

Better of the net

Citing ‘woke tradition,’ Chemours director resigns over abortion advantages for workers

Hybrid working? How the Metropolis of London is getting it executed (subscription required)

A celeb cemetery in Paris has develop into a haven for wildlife

The chart

Twitter

The tickers

These had been the top-searched tickers on MarketWatch as of 6 a.m. Japanese:

Ticker

Safety title

TSLA

Tesla

APE

AMC Leisure most well-liked shares

GME

GameStop

AMC

AMC Leisure

AAPL

Apple

NIO

NIO

NVDA

Nvidia

AMZN

Amazon.com

MULN

Mullen Automotive

BBBY

Mattress Bathtub & Past

Random reads

When Niagara Falls freezes over.

How a calendar of nude residents saved this dying Spanish city.

Mugger tries to take blind BBC reporters iPhone, fails spectacularly.

Have to Know begins early and is up to date till the opening bell, however join right here to get it delivered as soon as to your e-mail field. The emailed model will likely be despatched out at about 7:30 a.m. Japanese.

Hearken to the Greatest New Concepts in Cash podcast with MarketWatch reporter Charles Passy and economist Stephanie Kelton.

In February of this 12 months, I concluded that shares of Churchill Downs (NASDAQ:CHDN) have been racing greater because it continued to construct out its empire with its announcement of an enormous acquisition. I’ve grown way more appreciative of the enterprise over time, as its observe report is difficult to argue with, but concern that now shouldn’t be the time to become involved.

A Fast Recap

Churchill Downs is finest recognized from the Kentucky Derby, however exterior its horse racing actions, the corporate has substantial property associated to casinos and on-line video games as effectively. Forward of my take earlier this 12 months, I went again all the way in which to 2017 when the corporate divested its Large Fish operations with proceeds successfully used to purchase again low-cost inventory and reinforce the enterprise in different methods.

Shares really traded round $220 in 2017, the identical degree as they did earlier this 12 months, however that’s misrepresenting the efficiency as shares have been break up on a three-for-one-basis within the meantime. A $882 million enterprise which generated $286 million in EBITDA in 2017 had grown to $1.Three billion in 2019 on which EBITDA got here in at $451 million. Earnings per share energy had almost doubled over the identical time interval, adjusted for the stock-split in fact.

Revenues fell to $1.05 billion in 2020, no shock given the character of the actions and the affect of the pandemic and associated lockdowns, however shares had rallied to $260 early in 2021 already in anticipation of an awesome 12 months. That has turned out to be actuality as revenues have been up 58% to $1.23 billion within the first 9 months of the 12 months, with earnings coming in at $5.23 per share already, on observe to come back in round $7 per share.

Internet debt stood at $1.65 billion, and with EBITDA trending at $670 million, that labored all the way down to a 2.5 instances leverage ratio. The 39 million shares traded at $220 early this 12 months, for an $8.6 billion fairness valuation, or $10.2 billion enterprise valuation. This was equal to 6-7 instances gross sales, 15 instances EBITDA and 30 instances earnings, steep multiples by all means

Simply forward of the discharge of the fourth quarter outcomes for 2021, Churchill introduced a $2.48 billion deal to accumulate the Peninsula Pacific Leisure Firm, a deal valued at roughly 1 / 4 of its personal valuation on the time. With the deal the corporate would purchase the Colonial Downs Racetrack, extra services equivalent to casinos and the Arduous Rock Lodge & On line casino in Sioux Metropolis. The 9 time EBITDA a number of was a bit cheaper, because the affect on the underside line was onerous to gauge. Professional forma web debt was seen round $3.Eight billion as the corporate introduced a big deal to promote land to Blackstone as effectively.

I believed that earnings may rise to $9 per share, for a 25 instances earnings a number of, but together with almost Four instances leverage, the valuations have been actually not low-cost. Given this excessive valuation, though accompanied by a robust observe report, I concluded to develop into a purchaser within the excessive a whole bunch, because the market at giant was nonetheless a lot stronger in fact, not impacted by rising rates of interest but.

Stagnation

Since my upbeat but cautious tone in February, shares of Churchill have been buying and selling vary certain between $180 and $240 per share, at present exchanging arms proper in the midst of this vary at $210 per share.

In February, the corporate posted its full 12 months outcomes with revenues as much as $1.60 billion on which $627 million in EBITDA was reported, in addition to web earnings of $249 million, equal to $6.35 per share. The corporate has seen strong progress within the first two quarters of the 12 months, closing on the sale of land to Blackstone and retained earnings forward of the Peninsula deal, for which the corporate already secured borrowing effectively upfront of the deal closing, nice timing with the advantage of hindsight.

In October, the corporate posted third quarter outcomes which revealed a modest year-over-year decline in gross sales, with earnings per share down eight cents to $1.49 per share, albeit that the EBITDA efficiency elevated a bit. Internet debt got here in at $1.49 billion forward of the Peninsula deal, nonetheless large quantities as professional forma web debt would soar to $4.zero billion, albeit that professional forma EBITDA will probably exceed the billion mark following some operational beneficial properties seen this 12 months. The cope with Peninsula closed on November 1, so within the fourth quarter, as the true affect of the deal is simply seen within the new 12 months in fact.

Regardless of a nonetheless elevated leverage state of affairs, the corporate really introduced one other bolt-on, but substantial deal. The week forward of Christmas, the corporate introduced 1 / 4 of a billion deal to accumulate Exacta Programs, a know-how supplier of historic horse racing operations, with few particulars introduced on the deal.

Therefore, we stay considerably in the identical state of affairs. Earnings are nonetheless trending at $7-Eight per share in regular situations (forward of the Peninsula deal) and leverage is excessive, partly the results of the continued operational capital expenditures made by the enterprise.

Given the large enhance in rates of interest, the debt is extra critical than was the case at the beginning of the 12 months, as total valuation multiples have come down, which makes that the relative outperformance of Churchill appears to be pushed by the long run observe report, however it doesn’t essentially create a pleasant set-up for potential and perspective traders right here. That stated, it’s too early to write down off the shares right here because the Peninsula deal may create a roadmap for earnings to pattern round $10 per share, however for that loads of issues nonetheless must work out.

There are a lot of dynamics within the present financial and inventory market surroundings. Inflation, rate of interest will increase, company gross sales/earnings, and geopolitical occasions are all elements shaping the outlook for 2023. The Federal Reserve has been targeted on driving down inflation with a sequence of curiosity charge will increase. The most up-to-date improve of 0.50 proportion factors introduced the first credit score charge to 4.5%.

It’s my opinion that these rate of interest will increase have not been totally mirrored within the financial system but. Certain, we now have seen mortgage charges improve from document low ranges of two.65% for a 30-year mortgage in January 2021 to the present degree of about 6.5%. There have additionally been mass layoff bulletins from Amazon (AMZN), Meta Platforms (META), Twitter (TWTR), Netflix (NFLX), Carvana (CVNA), Peloton (PTON), Goldman Sacs (GS), Micron (MU), and others. It’s seemingly that larger charges and layoffs may have a snowball impact within the broader financial system as demand for items/providers declines as customers and firms reduce on spending on account of larger borrowing prices and with extra folks out of labor.

Curiosity Price Outlook for 2023

The Federal Reserve usually has a aim of two% for the inflation charge over the long-term. The most recent inflation charge was 7.1% for November 2022. Whereas this was decrease than the 7.7% charge from October, the extent nonetheless stays stubbornly excessive. So, there may be nonetheless work for the Fed to do to drive down inflation.

The Fed hinted that it’s going to improve its goal rate of interest to five.1% in 2023. This means extra will increase that quantity to 0.75 proportion factors. So, the borrowing prices for properties, automobiles, and companies to broaden are prone to develop into costlier in 2023. That is prone to scale back demand for large-ticket gadgets and for enterprise enlargement. Subsequently, company gross sales/earnings are prone to decline and extra layoffs are prone to happen in 2023 because of this.

As borrowing turns into costlier, potential house consumers usually tend to postpone buying properties, customers could maintain off on buying new automobiles and different big-ticket gadgets, present house homeowners most likely will not refinance and should postpone massive house enchancment initiatives, companies could halt investments for enlargement, and many others.

Greater rates of interest usually result in recessions as part of the traditional enterprise cycles. We witnessed that within the monetary disaster of 2008, the dot com bubble burst in 2000, and in different recessions. Earlier recessions occurred after a sequence of rate of interest will increase. It’s prone to occur once more as financial exercise slows down.

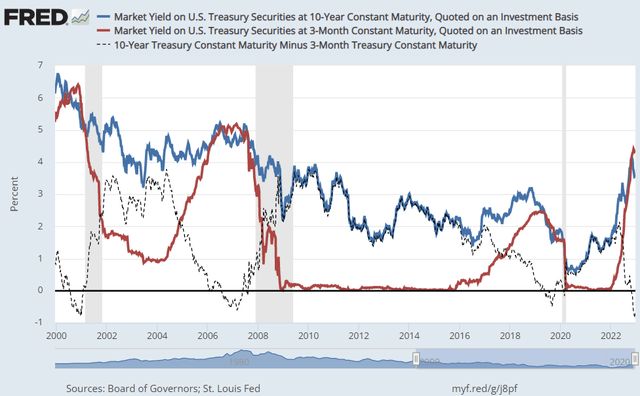

Yield Curve Inversion

One dependable recession indicator is the connection between the three month and 10-month treasury yields. When the 3-month treasury yield turns into larger than the 10-year treasury yield, the yield curve is alleged to be inverted. This prevalence predicted the final 10 recessions. The three-month treasury is presently yielding 4.28% whereas the 10-year treasury yields 3.75%. Usually, the longer-term treasuries may have larger yields. So, when the alternative happens, it signifies that financial circumstances are altering on account of short-term rate of interest will increase.

jobs.utah.gov

We are able to see within the chart above that the 3-month treasury yield (purple line) rose larger than the 10-year yield (blue line) previous to the final three recessions. It occurred earlier than the COVID-related recession in 2020, previous to the 2008 monetary disaster, and throughout the dot com bubble burst and recession that adopted. Whereas there isn’t any assure that the present inversion will end in a recession, this indicator has been dependable for the reason that 1980s. So, I do suppose it does improve the possibility of a recession occurring in 2023 considerably.

Company Earnings Declines

Analysts have been reducing EPS estimates for the S&P 500 (SP500) (SPY) firms for This autumn 2022 by a bigger margin than common. The EPS estimates had been lowered by 5.6% for This autumn. The typical decline for estimates over the previous 5 years has been 2.1%.

These bigger estimate declines are prone to proceed in 2023 for my part. The rationale for that’s inflation remains to be excessive and rates of interest are nonetheless rising. The price of most gadgets together with meals and vitality are nonetheless excessive which might scale back demand for different discretionary items/providers within the financial system. Many customers could need to put most of their cash into meals, shelter, and commuting prices and restrict spending on journey, leisure, eating out, and different discretionary items/providers.

Greater borrowing prices are prone to scale back demand for mortgages and residential purchases. This will result in much less demand for different large-ticket gadgets akin to home equipment, furnishings, and huge house enchancment initiatives. Greater borrowing prices may scale back demand for brand spanking new automobiles.

With all of this in thoughts, many firms are prone to see lowered demand resulting in decrease income and earnings as in comparison with when the financial system was more healthy. When demand decreases, then firms start shedding staff. That’s prone to result in an uptick in unemployment as many firms and companies are shedding staff.

Declining Financial Indicators

One financial indicator meaning so much for the well being of the financial system is the housing market. The rationale why housing is so vital is as a result of it includes about 15% to 18% of GDP. We’re experiencing important declines in actual property gross sales on account of larger mortgage charges.

Housing begins declined 16.4% in November 2022 over November 2021. Constructing permits declined 22.4% year-over-year with an 11.2% decline from October to November. Whereas new house gross sales elevated 5.3% from October 2022 to November 2022, they dropped 15.3% year-over-year in November 2022. Current house gross sales fell for 10 consecutive months. November present house gross sales declined 7.7% from October with a big 35.4% decline year-over-year.

Greater mortgage charges are having a detrimental impact on house gross sales. That is solely prone to worsen because the Fed continues to extend charges in 2023. Many potential consumers are prone to look ahead to decrease charges and/or decrease costs as they is likely to be priced out of the marketplace for the kind of home that they need to buy.

One other indicator that appears troublesome is the ISM Manufacturing report. Financial exercise within the manufacturing sector declined in November which marked the primary decline since Might 2020. The November Manufacturing PMI got here in at 49%. Percentages under 50% present contraction in manufacturing exercise. The Backlog of Orders Index got here in at 40% and was 5.3% decrease than the October studying. This could possibly be the beginning of a brand new downward pattern in manufacturing particularly with the backlog of orders declining.

One brilliant spot within the financial system has been the providers sector. The ISM Companies PMI got here in at 56.5% in November. This marked the 30th consecutive month of development for providers. Nevertheless, I believe it’s seemingly that some components of the providers sector are prone to decline in 2023. That features actual property which is prone to decline as larger mortgage charges scale back demand. Declines in 2023 might additionally happen in development, retail, wholesaling, transportation, and warehousing if slower financial exercise spreads on account of much less client and enterprise funding demand. Companies which are prone to maintain up properly embrace Agriculture, Healthcare, Utilities, and Meals Companies which will be thought-about non-discretionary spending.

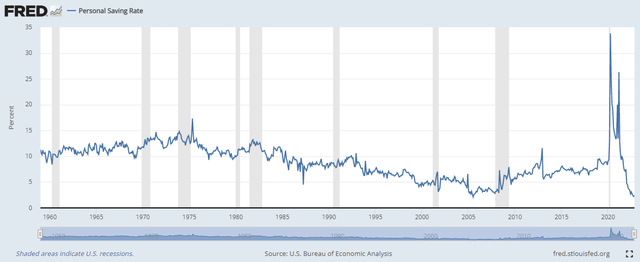

One other vital level for the 2023 outlook is that the private financial savings charge declined to a low degree.

fred.stlouisfed.org

The chart above exhibits that the private financial savings charge dropped under the place it was originally of 2008. The excessive financial savings charge in 2020 led to sturdy development because the financial system opened again up from the COVID lockdowns. Nevertheless, customers are actually starting 2023 with a lot much less saved up. That is prone to suppress demand as cash is extra prone to be spent on requirements akin to meals and vitality and fewer on main discretionary purchases akin to new properties, automobiles, journey, and leisure.

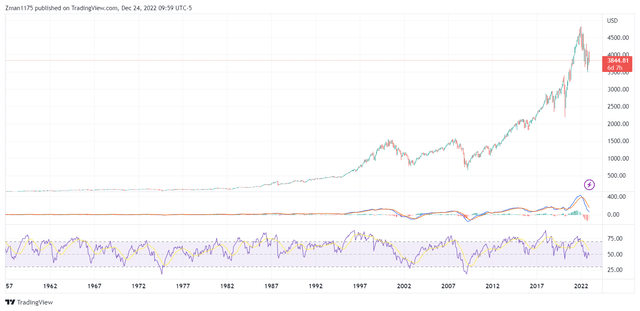

Technical Perspective

S&P 500 (tradingview.com)

The month-to-month chart above supplies a long-term perspective on how the S&P 500 traded by way of overbought and oversold circumstances. The RSI (purple line on the backside of the chart) has been declining and is displaying weak point under 50, and could possibly be headed for an oversold situation under 30. Be aware that the final two main bear markets in 2008 and 2002 drove the RSI under 30. I did not rely the COVID recession as a result of that was an anomaly and never part of the longer-term pure enterprise cycle. If this bear market behaves equally to the 2002 and 2008 markets, then there may be far more draw back to go.

The MACD indicator above the RSI has been in decline and appears bearish because it has been dropping in the direction of the zero line. Be aware that the MACD did drop under the zero line in 2002 and 2008. So, this might additionally point out that we might see a lot decrease costs in 2023 for the S&P 500.

Value-wise, the S&P 500 misplaced about 50% within the dot com bubble bear market and about 58% within the 2008 monetary disaster bear market. We might see losses much like the 2000-2002 bear market as valuations might have to return down additional earlier than the underside is in. If we get a 50% drop on this bear market from the market highs, we might see the S&P 500 drop to $2400. Nevertheless, the market could not fall that a lot on this bear market.

2023 Forecast for S&P 500

It may be troublesome to forecast precisely the place the S&P 500 shall be on the finish of 2023, however I’ll make an informed calculation for leisure functions. I’ll do that based mostly on anticipated earnings and the valuation for the S&P 500.

I believe the rate of interest will increase will take slightly longer to have a big detrimental impression on the financial system to the purpose of two consecutive quarters of detrimental development. So, I’m projecting that we see a recession in Q3 & This autumn of 2023.

I believe that analysts are overestimating the S&P 500 earnings for 2023. Goldman Sachs Group is projecting S&P 500 EPS of $224, whereas JPMorgan Chase & Co (JPM) initiatives $205. The consensus estimate is $231. I’m projecting a decrease EPS of $180. The rationale why I’m going decrease is as a result of I believe the vitality sector will take a success within the 2nd half of 2023. Power will most likely stay sturdy within the 1st half of 2023 because the financial system stays weak however not in deep recession territory. The vitality sector (oil costs particularly) tends to drop considerably throughout full-blown recessions. I imagine that can occur within the 2nd half of 2023. Subsequently, earnings for oil and energy-related firms are prone to decline considerably in Q3 and This autumn 2023 for my part.

The S&P 500’s valuation by way of trailing P/E ratio is presently about 19. I’m projecting that the S&P 500’s PE ratio drops to 16 by the tip of the 12 months because the market continues to sell-off throughout an finish of 12 months recession. Subsequently, my projection for the S&P 500 value on the finish of 2023 is $2880 (PE of 16 x EPS of $180). This may be a few 40% drop from the all-time excessive of $4818 and 25% decrease than the present value.

There are a lot of elements/dangers to think about that might make my projections incorrect. An precise finish of the Russian-Ukraine conflict can be constructive for the market and would seemingly result in a rally. The actions of China opening up its financial system could possibly be extra constructive for the worldwide financial system than anticipated and assist us to keep away from a recession.

Alternatively, if China backtracks and implements full blown lockdowns someday throughout the 12 months, it might result in financial circumstances to be worse than anticipated. If the Ukraine conflict escalates and different international locations develop into extra concerned, it might result in a way more bearish market and decrease than what I’m projecting.

I’m usually constructive and optimistic concerning the inventory market and the financial system. Nevertheless, the present developments have me realistically bearish when 2023.

Editor’s Be aware: This text was submitted as a part of Searching for Alpha’s 2023 Market Prediction contest. Do you’ve a conviction view for the S&P 500 subsequent 12 months? If that’s the case, click on right here to search out out extra and submit your article right now!

Have you ever ever been to a candle-lit service at a church for Christmas? Maybe a candle-lit vigil? Have you ever maybe lit a candle for a liked one whereas they’re away and even left a proverbial “candle within the window” for somebody?

Lighting a candle is a largely common expression. Folks all world wide and from numerous walks of life have interacted with the idea of lighting a candle. We gentle them for birthdays, weddings, funerals, anniversaries, vigils, and extra. A lit candle invokes sturdy emotions, from joyful frivolity to the non secular to the poignant.

We gentle them to shine a lightweight on our recollections, to light up our hopes and goals for the long run, and to provide course and hope to these we need to see once more. A lit candle displays our wishes and losses, our hopes and struggles. This Christmas, many will gentle a candle to recollect those that handed this yr and couldn’t take part on their household’s traditions. Some will gentle a candle on the closing of the yr to light up their hopes for the following.

Immediately the market is closed, and we’ve got time to get pleasure from ourselves with our household and mates. I need to gentle some digital candles right here with you.

Remembering This Previous 12 months – The first Candle Lit

2022 has been a loopy yr. The markets have been down closely, with Progress taking a a lot tougher hit than Worth has all year long:

Knowledge by YCharts

Whereas the market has been crushed down, there was a lot of wonderful alternatives to lock in earnings for many years to come back. The Federal Reserve has typically made strikes that negatively impacted the market, particularly mounted earnings.

We now have been laser-focused on discovering wonderful earnings investments all through 2022, and a few of our favorites this yr, you may see we’re fortunately amassing dividends with some nice capital good points on prime:

Knowledge by YCharts

Robust dividend payers like Enterprise Merchandise Companions (EPD), Antero Midstream (AM), and Greystone Housing Affect Buyers, LP (GHI) (fka ATAX) have allowed Excessive Dividend Alternatives members to remain forward of the market and outearn it. Posting optimistic returns in an in any other case sea of unfavourable returns available in the market.

That is the advantage of having a diversified portfolio. Whereas our portfolio had its share of holdings that had been down and some that had been down quite a bit, we additionally had some holdings that had been up quite a bit. 2022 was an ideal yr for power, it was a really troublesome yr for nearly the whole lot else.

The yr did have some optimistic swings, together with its sturdy drops. The market is way from a peaceful flat lake however is a consistently shifting and wavy ocean. It can be crucial, in my view, to look again over the previous yr and consider how you will have finished. You could have winners and losers in your portfolio – all of us do.

How have you ever finished at progressing towards reaching your retirement targets? For earnings traders, this implies contemplating your year-over-year earnings modifications. Are you nearer to your earnings objective, or are you falling behind your deliberate tempo?

Many Excessive Dividend Alternatives members have been sharing how their annual earnings is considerably up resulting from further excessive yields provided by the market. Whereas EPD and AM are examples of enormous capital good points in our portfolio this yr, neither had been our largest dividend raisers. Along with the 14 particular/supplemental dividends we noticed this yr, the HDO Mannequin Portfolio had 44 dividend hikes! Lots of our holdings skilled greater earnings, even whereas share costs declined.

Did you get caught up within the noise and distractions of life or investing? Or possibly made decisions that do not align along with your targets? Let this time of reminiscing be while you refocus your efforts as we glance towards a brand new yr. When you achieved your targets, take a second to provide your self reward and be completely satisfied along with your exhausting work. Success financially is one thing one hardly ever stumbles into however is one thing that requires exhausting and diligent work.

Be happy with your successes and study out of your shortcomings.

Take a Second to Dream and Hope – The 2nd Candle Lit

We lit a candle in remark of the previous. Now, it is time to gentle a second candle. This one is to shine gentle upon and illuminate our hopes and goals.

What’s it in 2023 that you simply need to obtain? Take a second to consider it. Set some targets to your subsequent yr of life. These could be much less sensible targets and extra hopeful ones. Dream huge!

2022 was nearly nothing like we might’ve anticipated it to be, however those that dreamed huge had been nonetheless capable of finding methods to work in direction of their end-game targets.

I wish to take this time to assist paint an image of what I hope to do in my retirement. What’s it that you simply hope to do? Spend extra time with family members? Study a brand new interest? Journey? Meet new individuals to befriend?

Do you ever see individuals taking a second to snap a photograph of their meals? Social media consideration seekers? Not so quick, a examine within the Journal of Character and Social Psychology confirmed those that take an image of their meals usually tend to get pleasure from it – loopy, proper? It builds hope and anticipation for the approaching meal, noting the optimistic facets of it earlier than consuming it.

Taking time to dream and picture with the one you love or partner, if in case you have a life companion, and even by your self, may also help you construct the need and motivation to place the work in to realize it. Consider this because the birthday to your portfolio and retirement goals. We’re lighting a candle to light up your hopes.

Make a plan for what you need your future to seem like, evaluate it to prior years, and see the way it’s adjusted and altered. All of us develop and alter because the years go by, and so can your wishes for the long run. Change your targets accordingly!

A Gentle For the Misplaced and Sorrowful – The third Candle Lit

Our final candle in the present day shall be one for the misplaced. If you inform somebody, “I will go away the sunshine on for you”, you are telling them you’ll maintain shining a beacon to seek out their manner dwelling. In case they get misplaced, sidetracked, or misled, they’ll nonetheless discover their option to the protection of dwelling. The candle serves as a beacon to the misplaced to seek out their manner again dwelling. Shining out towards the darkish, chilly world and offering a ray of hope.

A few of you’re actually discouraged. The market has been a bully to many this yr! Add to that indisputable fact that retirement planning and saving are robust! I get that. A few of you’re discouraged since you’ve misplaced your manner a bit of bit. Life’s storms have kicked up, and the outcomes are leaving you circled and misplaced. It may well occur to the perfect of us.

Present me somebody who has “by no means failed”, and I will present you somebody who has by no means dreamed large enough.

I need to shine a beacon to convey you in direction of and illuminate what has led me to success for thus a few years – earnings investing. You do not want 1,000,000 or multi-million-dollar steadiness retirement account. You do not have to make $100ok a yr to see success.

We will all obtain it – one dividend at a time.

I’ve the enjoyment of seeing many begin down the highway of dividend investing and having it revolutionize their retirement outlook. They forgo playing in hopes of discovering the following Amazon or Netflix. They purchase dependable earnings turbines and reinvest the dividends diligently. This offers you a easy means to find out how a lot earnings your portfolio will produce in your retirement. Want extra? Add as a lot spare change as attainable and maintain reinvesting these dividends. We suggest even retirees reinvest 25% of their dividend earnings at a minimal to maintain their earnings stream rising yr over yr. Einstein is famously quoted as saying that compounding is the eighth surprise of the world. I must agree. It is likely one of the strongest instruments in existence, and it might assist take a small assortment of shares and switch your portfolio into one thing magnificent.

If you focus much less on the swings in market costs and extra on the dividend-earning energy of your portfolio, it modifications the way you see your portfolio every day. As a substitute of fearing the crimson days, you begin trying ahead to them as alternatives.

So maybe you are exiting 2022 discouraged and disheartened. Perhaps some surprising money want, job loss, or different life occasion prevented you from assembly your retirement targets this yr. This candle is for you. My want is that it brings you hope as you employ it to information you towards a brand new outlook on investing.

The sunshine is on for you, my pal.

Dreamstime

Conclusion

Investing is likely one of the most original journeys many people soak up our lives. The market stays some of the efficient wealth turbines in existence, bar none. This implies we’re typically compelled to work together with it if we need to see monetary success, but we are able to have very totally different approaches and experiences.

Lighting a candle is a common expertise, however its which means could be diverse and deeply private. So too, will our outlooks on learn how to make investments finest and the way we extract wealth from the market.

I’m and at all times shall be an earnings investor. This Christmas, I’m lighting three candles for every of you. One to encourage you to reminisce on 2022 and its successes and shortcomings. One to encourage you to dream of the long run and make clear your hopes for 2023 and past. Lastly, another as a beacon to the misplaced and discouraged – there may be hope and a manner ahead if solely you comply with the sunshine to expertise it!

Retirement ought to be one thing we sit up for, get pleasure from throughout it, and go away pleasure behind for others trying ahead to their very own retirement. Collectively we are able to make this attainable, and the market pays for it! Feels like an ideal plan, in my humble opinion.

Have an exquisite Christmas if you happen to have a good time it. I sit up for our new experiences collectively in 2023.

“Expensive Santa, please deliver equities for subsequent yr” is the easy message from the most recent In search of Alpha ballot. Greater than 2,300 readers responded to this week’s Wall Road Breakfast ballot. Requested the place they might deploy most of their investing capital in 2023, a overwhelming majority of readers mentioned “shares.”

Greater than 62% of respondents will tilt most of their investments to equities (SPY) (QQQ) (IWM) (URTH), in keeping with the outcomes. For the extra risk-averse, money (SPRXX) at 17.5% was a favourite over bonds (TBT) (TLT) (SHY) (JNK) (LQD) (BNDW) at 12.2%, indicating that these traders are skeptical of Fed charge cuts coming subsequent yr.

The most recent Abstract of Financial Projections “exhibits the ‘median’ FOMCer expects brief charges to rise to five.1%, and stay there for the whole thing of 2023, inflation to stay tons of of foundation factors above goal via the top of subsequent yr, the yield curve to stay in inversion for 2 extra years (given the present stage of lengthy charges) and the unemployment charge to ‘solely’ rise 110 bps from latest trough to potential peak,” MKM strategist and economist Michael Darda wrote in a be aware (emphasis his).

Rounding out the outcomes, 5.4% mentioned they are going to put most of their capital to work in commodities (USO) (GLD) (DBC), nudging out crypto (BTC-USD) (ETH-USD) (<a href="//seekingalpha.com/image/GBTC" title="Grayscale Bitcoin Belief (BTC)”>OTC:GBTC) at 2.7%.

Wall Road skeptical: The arrogance in shares from these surveyed is in sharp distinction to the expectations from Wall Road strategists.

Strategists count on below-average returns for the S&P 500 (SP500) (SPY) in 2023, with lots of their colleagues on the economics aspect predicting a worldwide recession. On common, the 2023 finish value goal for main Wall Road outlets is 4,080, rather less than a 7% rise from present ranges.

On the highest finish, Fundstrat’s Tom Lee is probably the most bullish with a goal of 4,750. BNP Paribas’ Greg Boutle is probably the most bearish, predicting a drop to three,400. Amongst different notable calls, J.P. Morgan’s Dubravko Lakos-Bujas is anticipating the S&P to shut out subsequent yr at 4,200, a view additionally shared by Wells Fargo’s Chris Harvey. Goldman Sachs’ David Kostin, Citi’s Scott Chronert and BofA’s Savita Subramanian all predict a principally sideways yr with a goal of 4,000.

No Santa but: The inventory market would wish a significant rally on this Friday for a Santa Claus rally to seem. The S&P is at present down 1.45% for the week main into Dec. 25 and the three-day Christmas weekend. However opinion is split on when precisely a Santa Rally seems.

For these within the camp that it’s the week main as much as Jan. 2, there’s a probability bulls might immediate some outsize good points in subsequent week’s holiday-shortened, low-volume buying and selling. (three feedback)

Musk says no gross sales

Tesla (TSLA) CEO Elon Musk mentioned he won’t promote any extra Tesla inventory for about two years. Whereas talking in a Twitter Areas audio chat, Musk additionally mentioned he expects the financial system to be in “severe recession” in 2023, decreasing demand.

His feedback got here after a Tesla inventory selloff deepened on Thursday over worries about softening demand for electrical vehicles and Musk’s distraction with Twitter and his inventory gross sales. Shares have been down for 5 periods in a row.

“I will not promote inventory till I do not know most likely two years from now. Positively not subsequent yr beneath any circumstances and possibly not the yr thereafter,” Musk mentioned, responding to a query from TSLA investor Ross Gerber, who clashed in tweets with Musk earlier this week. (25 feedback)

$250M bail

FTX co-founder and former CEO, Sam Bankman-Fried posted a bond of $250M and will likely be allowed to reside in his mum or dad’s home in California whereas ready for his trial on expenses of fraud. Assistant U.S. Lawyer Nicolas Roos had proposed the bail phrases and alleged that Bankman-Fried “perpetrated a fraud of epic proportions.”

Justice of the Peace Decide Gabriel W. Gorenstein, who agreed to the bond and the home arrest proposal, mentioned Bankman-Fried will likely be required to get an digital monitoring bracelet. Bankman-Fried was arrested within the Bahamas 10 days in the past, after the U.S. filed prison expenses towards him. On Wednesday, he waived his proper to struggle extradition to the U.S. and flew again to the U.S. accompanied by FBI brokers and the U.S. Marshals Service. (49 feedback)

APEs going away?

Shares of AMC (AMC) slumped, however got here properly off session lows, whereas most popular models (APE) surged after the proposal from the cinema chain to swap all most popular inventory for widespread shares, which might then bear a reverse cut up.

The corporate additionally mentioned it meant to have a particular shareholder assembly to vote on proposals from its board of administrators to transform APE models into widespread inventory and reverse cut up its inventory at a 1-10 ratio.

AMC additionally mentioned it was elevating $110M in fairness, promoting APE shares to Antara Capital at a weighted common value of $0.66 per share. As well as, AMC mentioned it lower its debt load by $100M, decreasing its 2nd lien notes due in 2026 that had been held by Antara in trade for the 91M APE models. (101 feedback)

Earnings of Impartial Financial institution Corp. (NASDAQ:INDB) will likely proceed to surge via the top of 2023. The rate of interest hikes of 2022 will increase the web curiosity margin for subsequent yr. Additional, subdued mortgage progress will supply some assist for the backside line. General, I am anticipating Impartial Financial institution to report earnings of $5.63 per share for 2022, up 62%, and $6.44 per share for 2023, up 15% year-over-year. In comparison with my final report on the corporate, I’ve elevated my earnings estimates for each years principally as a result of I’ve raised the margin estimates following the third quarter’s surprisingly good efficiency. Subsequent yr’s goal worth suggests a reasonable upside from the present market worth. Due to this fact, I am sustaining a maintain ranking on Impartial Financial institution Corp.

This Yr’s Charge Hike to Increase Earnings Subsequent Yr

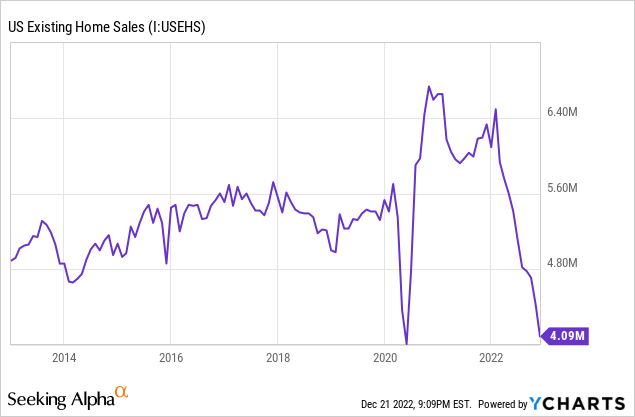

Impartial Financial institution’s internet curiosity margin surged by 37 foundation factors within the third quarter following the 18-basis factors progress within the second quarter of this yr. The third quarter’s efficiency beat my estimates given in my final report on the corporate. A part of the margin growth was attributed to the deployment of extra money into higher-yielding belongings. The money place is now nearly again to regular; due to this fact, this issue will not contribute towards margin growth in upcoming quarters.

SEC Filings, Creator’s Calculations

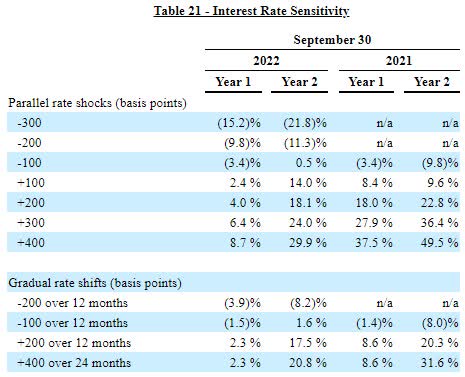

Nonetheless, the margin outlook stays vibrant due to the 425 foundation factors fed funds fee hike this yr and its lagged affect on the margin. Impartial Financial institution’s loans are slower to reprice than the deposits; due to this fact, the margin stands to profit extra within the second yr of a fee hike than the primary yr. The administration’s rate of interest simulation mannequin reveals {that a} 200-basis factors hike in rates of interest might increase the web curiosity revenue by 4.0% within the first yr and 18.1% within the second yr of the speed hike, as talked about within the 10-Q submitting.

3Q 2022 10-Q Submitting

Contemplating these elements, I am anticipating the margin to develop by 5 foundation factors within the final quarter of 2022 and 30 foundation factors in 2023. In comparison with my final report on Impartial Financial institution, I’ve raised my margin estimates for each years due to the third quarter’s efficiency which exceeded my earlier expectations.

Revising Downwards the Mortgage Progress Estimate Following the Third Quarter’s Disappointing Efficiency

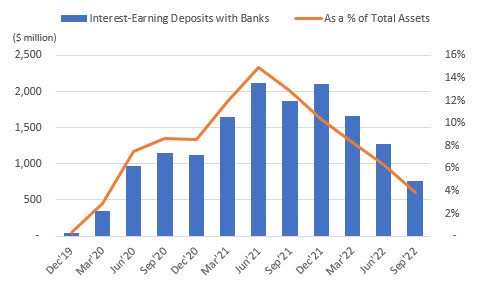

Impartial Financial institution’s mortgage portfolio grew by solely 0.2% within the third quarter, which missed my expectations. The outlook for residential mortgages and residential fairness loans is bleak because of the excessive interest-rate setting. Residential loans are an essential focus space for Impartial Financial institution as they made up 22% of whole loans on the finish of September 2022. Because of high-interest charges, U.S. house gross sales have plunged this yr, as proven beneath.

Information by YCharts

Nonetheless, the outlook for business loans stays optimistic. Impartial Financial institution principally operates in Massachusetts, whose present financial exercise is in a greater situation than the nationwide common.

The Federal Reserve Financial institution of Philadelphia

Contemplating these elements, I am anticipating the mortgage guide to develop by 0.75% within the final quarter of 2022, taking full-year progress to 1.6%. For 2023, I am anticipating the portfolio to develop by 3.0%. In comparison with my final report on the corporate, I’ve lowered my mortgage progress estimates following the third quarter’s below-expected efficiency.

In the meantime, I am anticipating deposits to develop considerably in keeping with loans. The next desk reveals my stability sheet estimates.

Monetary Place

FY18

FY19

FY20

FY21

FY22E

FY23E

Internet Loans

6,842

8,806

9,279

13,440

13,655

14,069

Progress of Internet Loans

8.7%

28.7%

5.4%

44.8%

1.6%

3.0%

Securities

1,075

1,275

2,348

4,789

3,935

4,015

Deposits

7,427

9,147

10,993

16,917

16,462

16,961

Borrowings and Sub-Debt

259

303

181

152

114

115

Frequent fairness

1,073

1,708

1,703

3,018

2,563

2,558

E book Worth Per Share ($)

38.8

49.7

51.5

74.8

55.9

55.8

Tangible BVPS ($)

29.0

34.1

35.5

49.6

33.8

33.7

Supply: SEC Filings, Creator’s Estimates(In USD million until in any other case specified)

Anticipating Earnings to Surge by 15%

The anticipated margin growth and subdued mortgage progress will drive earnings via the top of 2023. Alternatively, heightened inflation will push up working bills, which can prohibit earnings progress. Additional, the tight labor market will increase wage bills, which may also damage the underside line.

In the meantime, I am anticipating the provisioning for anticipated mortgage losses to stay close to a traditional stage. Non-performing loans have been 0.41% of whole loans, whereas allowances have been 1.08% of whole loans on the finish of September 2022. Though this protection isn’t excessive, it appears enough for a doable financial recession. General, I am anticipating the web provision expense to make up 0.06% of whole loans in 2023, which is similar as the common for 2017 to 2019.

Contemplating these elements, I am anticipating Impartial Financial institution to report earnings of $5.63 per share for 2022, up 62% year-over-year. For 2023, I am anticipating earnings to develop by 15% to $6.44 per share. The next desk reveals my revenue assertion estimates.

Earnings Assertion

FY18

FY19

FY20

FY21

FY22E

FY23E

Internet curiosity revenue

298

393

368

402

607

686

Provision for mortgage losses

5

6

53

18

3

8

Non-interest revenue

89

115

111

106

111

108

Non-interest expense

226

284

274

333

373

398

Internet revenue – Frequent Sh.

122

165

121

121

258

295

EPS – Diluted ($)

4.40

5.03

3.64

3.47

5.63

6.44

Supply: SEC Filings, Creator’s Estimates(In USD million until in any other case specified)

In my final report on Impartial Financial institution, I estimated earnings of $5.29 per share for 2022 and $5.81 per share for 2023. I’ve raised my earnings estimates principally as a result of I’ve elevated my margin estimates.

My estimates are primarily based on sure macroeconomic assumptions that won’t come to fruition. Due to this fact, precise earnings can differ materially from my estimates.

Sustaining a Maintain Ranking

Impartial Financial institution is providing a dividend yield of two.6% on the present quarterly dividend fee of $0.55 per share. The earnings and dividend estimates counsel a payout ratio of 34% for 2023, which is beneath the five-year common of 43%. As Impartial Financial institution has solely not too long ago elevated its quarterly dividend, I’m not anticipating one other dividend hike in 2023.

I’m utilizing the historic price-to-tangible guide (“P/TB”) and price-to-earnings (“P/E”) multiples to worth Impartial Financial institution. The inventory has traded at a median P/TB ratio of 1.92 previously, as proven beneath.

Multiplying the common P/TB a number of with the forecast tangible guide worth per share of $33.7 provides a goal worth of $64.Eight for the top of 2023. This worth goal implies a 23.5% draw back from the December 21 closing worth. The next desk reveals the sensitivity of the goal worth to the P/TB ratio.

P/TB A number of

1.72x

1.82x

1.92x

2.02x

2.12x

TBVPS – Dec 2023 ($)

33.7

33.7

33.7

33.7

33.7

Goal Worth ($)

58.1

61.4

64.8

68.2

71.5

Market Worth ($)

84.7

84.7

84.7

84.7

84.7

Upside/(Draw back)

(31.5)%

(27.5)%

(23.5)%

(19.5)%

(15.5)%

Supply: Creator’s Estimates

The inventory has traded at a median P/E ratio of round 18.9x previously, as proven beneath.

Multiplying the common P/E a number of with the forecast earnings per share of $6.44 provides a goal worth of $121.9 for the top of 2023. This worth goal implies a 44.0% upside from the December 21 closing worth. The next desk reveals the sensitivity of the goal worth to the P/E ratio.

P/E A number of

16.9x

17.9x

18.9x

19.9x

20.9x

EPS 2023 ($)

6.44

6.44

6.44

6.44

6.44

Goal Worth ($)

109.0

115.5

121.9

128.4

134.8

Market Worth ($)

84.7

84.7

84.7

84.7

84.7

Upside/(Draw back)

28.7%

36.4%

44.0%

51.6%

59.2%

Supply: Creator’s Estimates

Equally weighting the goal costs from the 2 valuation strategies provides a mixed goal worth of $93.4, which means a 10.2% upside from the present market worth. Including the ahead dividend yield provides a complete anticipated return of 12.8%. For my part, this return isn’t excessive sufficient; due to this fact, I’m sustaining a maintain ranking on Impartial Financial institution.

It was solely final week that Morgan Stanley opined that one of many macroeconomic surprises for 2023 may very well be that the Financial institution of Japan decides to not make any modifications to its ultra-loose coverage.

That simply goes to point out the perils of forecasting surprises after Japan’s central financial institution on Tuesday widened the band that it could tolerate bond yields by 1 / 4 level, a transfer that despatched the yen surging and rattled markets.

Extra on the BOJ to come back.

Analysts at wealth supervisor Glenmede Funding Administration level on the market’s been an enormous disparity between the efficiency of actual property funding trusts listed publicly, and people which can be personal.