Metal Companions Holdings (NYSE:SPLP) is a holding firm or conglomerate. Based on their annual report, they’ve 7 companies within the industrial sector, 2 in vitality and so they additionally personal 100% of Net Financial institution.

The commercial corporations that they personal manufacture area of interest engineered industrial merchandise which might be leaders of their niches. These merchandise embrace becoming a member of supplies, tubing, constructing supplies, efficiency supplies, electrical merchandise, metalized movies and a blade enterprise for meat packing. Their industrial merchandise are bought worldwide.

Their vitality companies present companies to the oil and gasoline exploration and manufacturing corporations.

In SPLP’s most up-to-date quarterly report, they reported robust income of $1.45 per share with revenues up 8.6% from the identical quarter of 2021 regardless of having bought certainly one of their companies. Adjusted free money circulation got here in at $48 million or $2.22 per share. Over the past years, SPLP has purchased again round 40% of their widespread shares.

SPLP is an L.P., so buyers who keep away from Ok-1s will doubtless need to keep away from this firm, though I discover Ok-1’s on most popular shares to be very simple.

Metal Companions Holdings Time period Most popular “A” Shares

Metal Companions Holdings Most popular “A” (NYSE:SPLP.PA) is a time period most popular inventory. It matures on February seventh, 2026 and presents an 8.9% YTM.

For individuals who aren’t aware of time period most popular shares, the overwhelming majority of most popular shares are “perpetual most popular shares”. In different phrases, they haven’t any maturity date and may stay available on the market without end, theoretically. Time period most popular shares, however, have a maturity date like a bond and thus they supply nice security in opposition to greater rates of interest. If you purchase a “time period most popular” inventory, you understand precisely what your complete return can be in the event you maintain it to maturity.

I actually like time period most popular shares. They’re nice in a market the place charges are rising. Whereas many perpetual most popular shares have nosedived from $25 into the kids, and should by no means recuperate, time period most popular shares present the reassurance that you’re going to get $25 par at maturity date. So outdoors of a chapter sort occasion between now and February 2026, SPLP.PA can pay out $25 plus accrued dividends on its maturity date.

Listed here are the main points on SPLP.PA:

Present Value: $22.97

Yield To Maturity 8.9%

Cumulative Sure

Annual dividend $1.50

Maturity Date 2/7/2026

Once I write an article on a bond or time period most popular inventory, I don’t present the present yield as a result of it has no actual that means and solely misleads buyers. I’ve seen many mispricings the place buyers apparently do not perceive this. They overprice a bond with a excessive present yield even supposing its complete return till maturity is poor relative to different bonds or time period most popular shares whose YTM.

One factor to say about SPLP.PA is that within the prospectus it states that SPLP pays dividends on SPLP.PA with inventory in the event that they select and may redeem the shares with $25 value of widespread inventory. This doesn’t concern me. They solely paid 1 dividend with inventory and that was through the COVID market meltdown the place each firm was panicked and hording money. And anybody who held onto this widespread inventory dividend made some huge cash on it. Since this firm is continually attempting to shrink their variety of shares and is continually shopping for again their widespread inventory, it’s fairly uncertain that they’ll redeem SPLP.PA with widespread inventory. And naturally, you possibly can all the time flip round and simply promote your widespread shares within the unlikely occasion SPLP.PA is redeemed with widespread shares.

Security

SPLP.PA doesn’t have a credit standing, however from my evaluation I contemplate it very protected. First, the widespread inventory has been rock stable. Wanting on the chart beneath, you would not know that we’re in a bear market. SPLP is up greater than Four fold over the past 2 years.

2-12 months Value Chart

Yahoo Finance

By way of protection of debt and most popular inventory, adjusted EBITDA was $60 million in the latest quarter which annualizes to $240 million. Their most popular dividends quantity to solely $10 million per yr. The proper means to have a look at protection is to mix curiosity expense plus most popular inventory dividends. Annual curiosity expense is round $40 million whereas most popular inventory dividends come to $10 million. Combining these 2 numbers will get us to $50 million yearly which is lined 4.Eight instances by EBITDA. That is very robust protection for curiosity and most popular dividends.

However it’s actually higher than this as a result of SPLP is a large free money generator. If we annualize the latest quarter’s free money circulation of $48 million, that’s $192 million. So even free money circulation covers the mixed curiosity expense and most popular expense by nearly Four instances.

The corporate additionally continues to imagine in itself and continued to purchase again extra widespread inventory through the third quarter.

And lastly, the truth that they function in 10 completely different companies supplies nice diversification. If instances are robust in a sector the place certainly one of their companies operates, that isn’t a giant deal to SPLP, whereas many corporations merely function in 1 sector and have far more sector danger than SPLP.

Abstract

Metal Companions Holdings is an organization that owns a number of different corporations in varied sectors offering nice diversification.

Time period most popular inventory SPLP.PA presently presents an 8.9% YTM and matures on February 7, 2026.

SPLP widespread inventory has been an excellent performer over the past 2 years, rising greater than Four fold and never pulling again in any respect throughout this bear market.

EBITDA protection of mixed curiosity plus most popular dividends is a really robust 4.Eight instances and SPLP generates huge quantities of free money circulation.

SPLP continues to purchase again its personal widespread inventory, so the administration clearly sees SPLP as having a vibrant future.

I imagine that SPLP.PA is kind of undervalued given the energy of the corporate and the truth that you’ve gotten the security of a maturity date which insulates SPLP.PA from rate of interest danger.

We need to hear from readers who’ve tales to share concerning the results of accelerating prices and a altering economic system. If you happen to’d wish to share your expertise, write to readerstories@marketwatch.com. Please embody your title and the easiest way to achieve you. A reporter could also be in contact.

For many individuals residing within the U.S., these are robust — and complicated — instances.

On Friday, the Labor Division reported 263,000 new jobs in November, whereas the unemployment fee held regular at 3.7%. Layoffs stay low, regardless of mass job cuts within the tech sector. Common hourly wages have additionally risen 5.1% up to now 12 months, however nonetheless lag behind inflation for a lot of staff. And there have been 10.Three million job openings in October — barely down from the earlier month’s 10.7 million.

Some individuals would possibly see the most recent financial knowledge as each difficult and complicated.

In spite of everything, the price of residing rose 7.7% on the 12 months in October. The as soon as red-hot housing market is lastly cooling, because of mortgage charges which have greater than doubled during the last 12 months amid the Federal Reserve’s makes an attempt to rein in inflation, and rents, whereas moderating, have surged from pre-pandemic ranges. Borrowing cash to cowl elevated precarity is turning into costlier too, with the typical credit-card APR at 19.2% as of Nov. 30, in accordance with Bankrate.

“‘It’s simply mind-boggling, the disconnect that we’ve seen.’”

Given all of the conflicting alerts, economists say it may be tough for customers to know precisely really feel concerning the economic system proper now. “It’s not new, this disparity between the precise information on the bottom about what’s occurring within the economic system and the sentiment,” stated Heidi Shierholz, president of the Financial Coverage Institute, a left-leaning suppose tank.

“I bear in mind this summer time it was simply unambiguously the strongest jobs restoration we’ve had in many years,” she added. “There’s simply completely zero probability that we have been in a recession — not solely have been we not in a recession, we have been in simply an awfully quick restoration — and the polling, an enormous share of individuals really thought we have been in a recession. It’s simply mind-boggling, the disconnect that we’ve seen.”

Nonetheless, the truth that inflation is consuming into individuals’s financial savings — and that important items like meals, vitality and housing have spiked in value — is certain to make many individuals sad.

Struggling to pay for lease and meals

“Going into the pandemic, greater than seven out of each 10 extraordinarily low-income renters have been already spending greater than half of their earnings on lease. After which the pandemic hits; we noticed plenty of low-wage staff lose their jobs and see an earnings decline,” stated Andrew Aurand, vice chairman for analysis on the Nationwide Low Earnings Housing Coalition. “Then in 2021, we see this large spike in costs. For a wide range of causes, they’ve struggled for a very long time, and for the reason that pandemic, it’s gotten even worse.”

Reasonable-income Individuals are struggling too. Perhaps you possibly can’t afford your favourite household meals, as the worth of grocery retailer and grocery store purchases has jumped by 12.4% from final 12 months. Or perhaps you’re laying aside a visit to see household this vacation season because of the upper value of airfare, otherwise you’re nervous about shedding your job as some enterprise leaders warn of a recession. Maybe you’re pressured to depend on bank cards and private loans, as credit-card debt is up 15% from a 12 months in the past.

MarketWatch has chronicled many of those adjustments, detailing renters’ frustrations, households’ robust selections on the grocery retailer, and the truth confronted by would-be house consumers sidelined by greater charges and dwindling affordability.

However we want your assist telling an ongoing story concerning the American economic system, centering the experiences of on a regular basis individuals. Our readers know higher than anybody about how at present’s financial circumstances have impacted their every day lives.

It was January 24, 1848, when James Wilson Marshall found a lode of gold whereas engaged on the development of a brand new sawmill. From that second on, hundreds of miners scoured each nook of California, giving rise to a frenzied hunt for gold. Opposite to in style perception, ultimately it was not the various gold prospectors who bought wealthy however these few who bought the instruments to prospect for it, resembling shovels and picks.

As previous as this story is, greater than 150 years, I believe it’s a good analogy to explain my funding thesis. The curiosity of many is directed towards 21st century gold, thus Taiwan Semiconductor Manufacturing Firm Restricted’s (NYSE:TSM) (“TSMC”) chips, however I believe it’s extra affordable to give attention to who permits the chips to be constructed, particularly ASML Holding N.V. (NASDAQ:ASML). On this article I’ll clarify this idea intimately by clarifying the explanations behind my bullish thesis on ASML and bearish thesis on TSMC.

The significance of semiconductors on this planet

Earlier than making a comparability between ASML and TSMC, I believe it’s value stating the primary points of the market during which they function.

Semiconductors make up a market that was value $600 billion in 2021 and can probably be value not less than a trillion {dollars} by the top of the last decade. Their significance is essential, since they’re current in any digital machine, from the smartphone you’re studying this text from, to the washer the place you wash your garments. With out them, it might be nearly inconceivable to have the ability to maintain the identical life-style, however there may be extra. At this time’s society is more and more geared towards technological options involving new digital gear; due to this fact, the extra time passes, the extra dependent we’re on semiconductors.

The present dependence that every one nations on this planet have on semiconductors is one thing extraordinarily harmful in my view, as a result of historical past has taught us that when everybody relies on one thing, new conflicts are prone to be created. Oil a number of instances has been the reason for wars due to its essential significance in right this moment’s industrialized financial system, and gasoline is not any totally different. In any case, we don’t want a conflict to understand how dependent we already are on semiconductors; in truth, the pandemic was sufficient to place us on alert. Steady lockdowns utterly disrupted the semiconductor provide chain, an issue we’re nonetheless paying for right this moment. On the peak of the pandemic, it had turn into advanced to even purchase a automotive and obtain it earlier than a yr had handed.

Lastly, there may be yet another side of semiconductors that needs to be emphasised, most likely a very powerful of all: semiconductors are additionally the primary element for constructing weapons and protection mechanisms. Which means that the nations which have entry to one of the best semiconductors are essentially the most militarily superior ones. So, this market, after all, is more and more the article of curiosity by governments all over the world. To be technologically backward would indicate an incapability to defend in opposition to army assault.

TSMC vs. ASML

TSMC and ASML are two pivotal firms within the semiconductor market, and on this part we are going to see what their biggest strengths and dangers are. As soon as I’ve analyzed the businesses individually, I’ll make a comparability that can help my funding thesis.

TSMC: everyone needs its chips

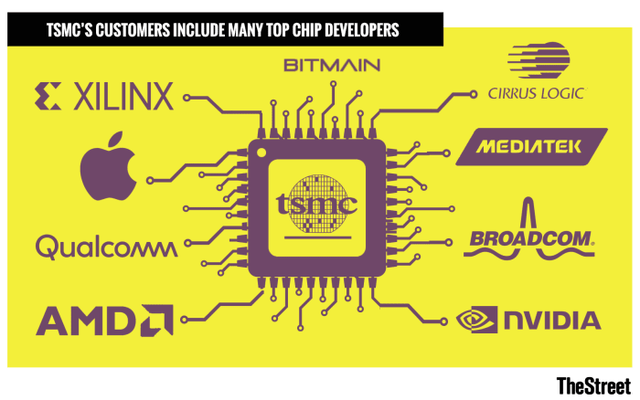

In the beginning of the article, I in contrast TSMC’s chips to gold, however this comparability most likely doesn’t do justice since they’re value way more than gold. The aggressive benefit this firm has gained over the previous decade is one thing spectacular, and its numbers nearly sign a monopoly place.

The Avenue

90% of the world’s tremendous superior pc chips are manufactured by TSMC. Main clients embrace Apple (AAPL), Qualcomm (QCOM), and Nvidia (NVDA).

TSMC has a 53.40% share of the worldwide pure-play foundry market.

Furthermore, its essential opponents, Intel (INTC) and Samsung (OTCPK:SSNLF), don’t come near TSMC’s present dominance. Intel is investing closely in new crops in each america and Europe, however it’s nonetheless lagging far behind in 5nm chip manufacturing. Suffice it to say that TSMC will ship 3nm chips in 2023 and is already well-positioned on manufacturing 2nm ones. Samsung has a 16.50% share within the world foundry market and is barely forward within the manufacturing of 3nm chips; nonetheless, it nonetheless stays one step behind TSMC, because the latter has a greater buyer base. Even when Samsung produces 3nm chips a number of months upfront, it doesn’t have the identical demand as TSMC. As we now have seen earlier than, Apple is a significant buyer, and there should not that many firms that want such highly effective chips.

However why does TSMC have a greater buyer base? The reply lies within the totally different enterprise mannequin in comparison with Intel and Samsung. TSMC operates as a contract producer that produces chips designed by different firms, whereas Samsung and Intel are IDMs, so they’re concerned in each chip design and manufacturing. So, for a possible buyer, it seems each cheaper and extra environment friendly to design their very own chips and outsource manufacturing to TSMC. That is precisely the method adopted by “fabless” firms resembling Nvidia and Superior Micro Gadgets (AMD).

As well as, there may be additionally motive to incorporate the side associated to attainable conflicts of curiosity within the circumstances of Samsung and Intel. Assuming Intel was within the present place of TSMC, it’s unlikely that it might produce AMD-designed chips, since this could favor the sale of AMD processors. The identical is true for Samsung with its opponents. For TSMC, being engaged solely in manufacturing, this drawback doesn’t exist because it doesn’t compete in opposition to firms that design chips.

TIKR Terminal

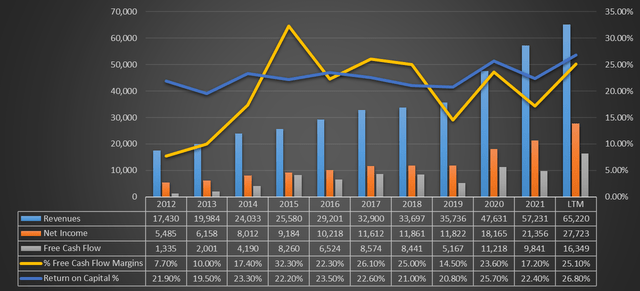

Contextualizing what has been mentioned in financial/monetary information, TSMC is principally a cash machine. Revenues and earnings rising nearly yearly, return on capital firmly above 20%, and a excessive free money circulation margin contemplating the business during which it operates. Objectively, TSMC is presently top-of-the-line firms on this planet when it comes to aggressive benefit and profitability.

The benefit Taiwan Semiconductor has gained over its opponents is so nice that it might not take simply years to shut it. In Intel’s case most likely not even a decade. As well as, it’s to be dominated out that new opponents may take over in these years because it operates in an business during which giant sums of capital are wanted to start out a enterprise. An organization ranging from scratch and wanting to check itself with TSMC would face an nearly insurmountable barrier to entry. TSMC’s aggressive benefit is prone to endure; in truth, analysts predict that revenues can proceed to develop quickly pushed by rising demand for essentially the most refined chips.

TIKR Terminal

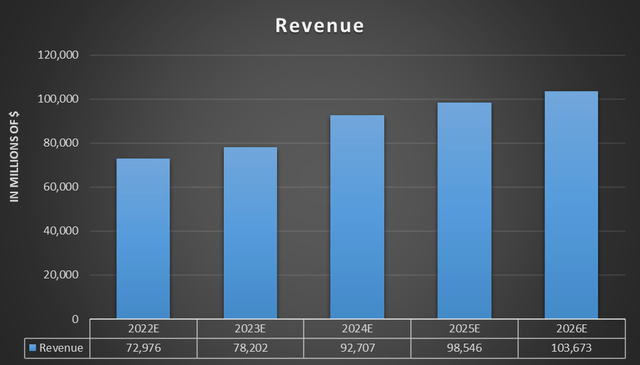

In accordance with TIKR Terminal analysts, TSMC may cross the $100 billion income threshold in 2026, nearly double the quantity produced within the full yr 2021. In mild of those concerns, one would possibly assume that TSMC is the proper firm, however that’s not fairly the case. In contrast to most firms, its essential weak spot will not be financial, however geopolitical. In reality, the following part will cope with this.

Taiwan Semiconductor: The geopolitical danger

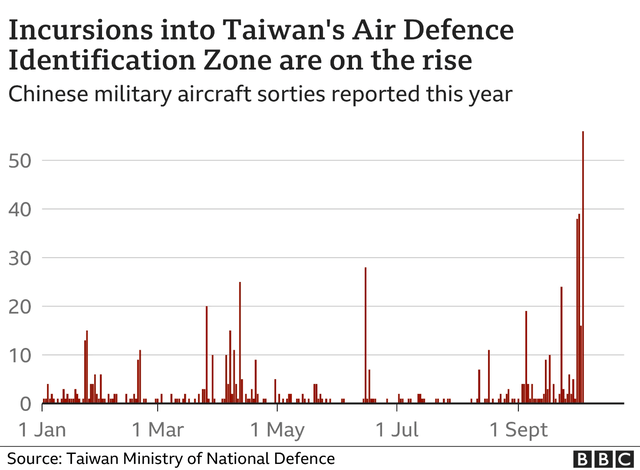

As defined earlier, the semiconductor market is more and more turning into a political problem, which is why the world’s main nations are doing every little thing they’ll to seize one of the best chips. Since TSMC is the corporate on which just about your entire world relies upon for the manufacturing of essentially the most superior chips, it’s apparent that it has attracted the curiosity of the key financial powers, particularly China and america.

The issue is that TSMC is a Taiwanese firm, and China has made it very clear a number of instances that it doesn’t settle for Taiwan’s independence. Alternatively, america clearly doesn’t need China to have management over TSMC, as it might have too nice a bonus within the semiconductor market. President Biden has already acknowledged that the U.S. will defend Taiwan militarily within the occasion of an assault, however Xi Jinping has additionally declared in flip that he’ll take all mandatory measures to reunify Taiwan. In the meantime, Chinese language incursions have gotten increasingly more frequent.

BBC, Taiwan Ministry of Nationwide Defence

At the moment, TSMC is within the eye of the storm, and I personally can’t see how this case could be resolved. My hope is that it will not come to a army battle, however I’ve my doubts about that, since neither China nor america is stepping again. Having dominance over one of the best semiconductors is just too essential as a result of it might imply being the primary energy on this planet. However in all this, how is TSMC doing?

Taiwan’s largest firm is attempting to diversify its enterprise away from its headquarters in order to untie itself from Beijing’s grip. In Arizona, TSMC is giving delivery to its most technologically superior manufacturing unit, whereas different investments are being made in Japan. This diversification course of, nonetheless, is under no circumstances simple, as there are three issues:

The primary is that extreme funding overseas, and particularly “in enemy territory” may set off an assault from China. Definitely, the investments in Arizona didn’t please Xi Jinping.

The second is that the manufacturing capability of factories in Taiwan is large, and years of abroad funding won’t be sufficient to diversify the enterprise. For instance, the manufacturing unit in Arizona, as technologically superior as it’s, will likely be nowhere close to comparable when it comes to manufacturing capability to these in Taiwan. Definitely, a $12 billion funding will not be sufficient to diversify the enterprise of an organization as giant as TSMC. Big quantities of capital will likely be wanted to take a position, however with out upsetting China an excessive amount of.

The third drawback is that sustaining crops overseas tends to be costlier, which would scale back revenue margins. Paying labor prices in america will not be the identical as paying them in Taiwan, in addition to many different bills.

Total, the scenario is just too advanced from a geopolitical perspective, and nobody now can know exactly what this may result in. As a lot as I recognize TSMC’s numbers, I’m compelled to not put money into it as a result of I consider that the dangers associated to an funding could outweigh the advantages. Everybody needs its chips, however the issue is that an assault on Taiwan is turning into extra of a actuality than a black swan. From the phrases of Protection Minister Chiu Kuo, Taiwan is already making ready:

We’re build up our arsenal and making ready for conflict in keeping with our personal plan. We wish to guarantee we now have a sure interval of stockpiles in Taiwan, together with meals, together with crucial provides, minerals, chemical substances and power after all.

Lastly, if you’re questioning what would occur to TSMC within the occasion of a army assault, right here is the reply from its president Mark Liu:

No person can management TSMC by drive. When you take a army drive or invasion, you’ll render TSMC manufacturing unit not operable. As a result of that is such a complicated manufacturing facility, it is determined by real-time reference to the skin world, with Europe, with Japan, with U.S., from supplies to chemical substances to spare elements to engineering software program and prognosis.

Beforehand we now have seen how TSMC, Intel, and Samsung are preventing for an ever-larger share within the semiconductor market. Everybody needs to supply one of the best chips and everybody needs to purchase one of the best chips. However have you ever ever questioned how TSMC, Samsung and Intel produce such cutting-edge chips? How have they got such highly effective machines to generate 3nm chips? The reply is that every one the key semiconductor firms are depending on equipment from the identical provider, ASML.

All the semiconductor provide chain depends on ASML, as a result of its EUV lithography machines are presently the one ones on this planet that allow the creation of essentially the most superior chips. If for TSMC there may be Samsung that comes near its know-how, for ASML there isn’t a competitor that may maintain a candle to it, since nobody has been capable of develop such superior know-how. Furthermore, what makes the hole with opponents develop even wider is that ASML continues to innovate. By subsequent yr, the primary Excessive-NA EUV lithography machine could possibly be delivered, and early hypotheses are already being made concerning the Hyper-NA EUV. For ASML, competitors exists solely within the sale of DUV lithography machines, that are these designed to create lower-performance chips. Nonetheless, the technological improvement of right this moment’s society requires more and more high-performance chips, so the expansion of ASML appears nearly inevitable.

TIKR Terminal

As could be seen from this graph, ASML skilled some difficulties rising earlier than 2017, however from that yr on, development has not stopped as EUV lithography started to be broadly used. What’s extra, the demand for superior chips is favoring the sale of EUV machines, and the outcomes achieved prior to now three years are proof of that. In accordance with TIKR Terminal analysts, this firm may practically double its revenues by 2026.

TIKR Terminal

Ascertaining how essential and strong ASML is, I want to elaborate additional concerning its aggressive benefit as I believe it’s fascinating. As you’ll have guessed, ASML is a very powerful know-how firm on this planet as a result of it manufactures one of the best lithography machines, that are crucial within the preliminary stage of producing one of the best chips round. With out ASML, TSMC wouldn’t have the ability to manufacture Apple’s designated chips, and the identical goes for Samsung and Intel. So, it’s clear that if ASML have been to cease promoting its machines, the entire world couldn’t proceed to develop technologically. However how is it attainable that one firm has a lot energy? How is it attainable that nobody else may create an EUV lithography machine? Extra importantly, couldn’t the machines already bought by ASML be “copied” by a technique of reverse engineering? A complete article would most likely not be sufficient to reply these reliable questions, however I’ll attempt to be as clear and concise as attainable.

ASML

To begin with, the EUV machines bought by ASML are tough to breed due to an financial problem. They’re presently bought for $200 million every, whereas the brand new Excessive-NA EUV ones will likely be bought for not less than $300 million every. This side already places off potential opponents who don’t current sufficient funds to breed them.

Those that do have the cash, nonetheless, could have appreciable problem sourcing main and minor elements in addition to assembling them. An EUV system weighs practically 200 tons and consists of 100,000 elements, 3,000 cables, 40,000 bolts and a pair of kilometers of hoses. All bought from 5,000 totally different suppliers.

Even assuming {that a} hypothetical firm managed to have every little thing readily available, it nonetheless wouldn’t have the ability to correctly assemble the 100,000 elements. Reproducing the mechanism of an EUV system is one thing extraordinarily advanced even when in possession of all the required elements and hundreds of engineers readily available. To present you an thought, the corporate acknowledged that an EUV system controls mild beams so exactly that it’s equal to shining a flashlight from earth and hitting a 50-cent coin positioned on the moon. Lastly, as if that weren’t sufficient, it takes 40 cargo containers, unfold over 20 vans and three cargo planes, to ship an EUV system.

China has been attempting for years to breed what’s presently essentially the most highly effective machine on this planet, however it’s nonetheless too removed from discovering an answer. What’s extra, the Dutch authorities, below stress from america, has banned the export of the most recent EUV techniques to China. The goal is clearly to go away China as far behind as attainable from a technological perspective. At the moment, ASML can proceed to promote solely the much less refined techniques resembling DUV to China. This final side will likely be mentioned in additional element within the subsequent part on ASML’s dangers

ASML: U.S. stress and technical limitations

ASML is the one firm on this planet able to creating EUV lithography machines, so it goes with out saying that there’s a geopolitical element to investigate right here as properly. As anticipated earlier, america pressed the Dutch authorities to ban ASML from exporting EUV lithography machines to China. This selection, though affordable from a sure perspective, hurts its profitability because it can’t broaden its enterprise in China. Furthermore, it have to be mentioned that earlier than the blockade China had already bought some EUV lithography machines; due to this fact, this determination doesn’t profit ASML in any manner. Sooner or later, it can’t be dominated out that DUV lithography machines will even be subjected to the identical therapy, and this could make the scenario even worse. Ought to this second ban turn into a actuality, a discount in revenues of about 10% is anticipated. Past this attainable quick loss, I consider the long-term financial injury is bigger, since China is prone to be the most important semiconductor market on this planet.

The second danger is solely technical in nature. How lengthy can ASML innovate? Present lithographic know-how borders on perfection, and it is going to be tough to enhance on the brand new high-NA EUV machines. Past the bodily limitations that stop chips from being miniaturized past a sure degree, there may be additionally an financial side to think about. ASML CTO Van den Brink doesn’t presently consider that hyper-NA EUV is possible, and high-NA EUV could be the final NA.

We’re researching it, however that does not imply it’ll make it into manufacturing. For years, I have been suspecting that high-NA would be the final NA, and this perception hasn’t modified. Theoretically, it may be finished. Technologically, it may be finished. However how a lot room is left out there for even bigger lenses? May we even promote these techniques? I used to be paranoid about high-NA and I am much more paranoid about hyper-NA. If the price of hyper-NA grows as quick as we have seen with high-NA, it’ll just about be economically unfeasible. Though, in itself, that is additionally a technological problem. And that is what we’re wanting into.

Ultimate Ideas

Earlier than I summarize my the reason why I consider ASML is a greater funding total, I want to say my two cents about an occasion involving TSMC lately that could be mentioned within the feedback.

In current weeks, I’ve observed that there was a variety of positivity about TSMC after it was found that Warren Buffett invested $4.1 billion in it. Definitely this can be a constructive sign, however I don’t assume it may be decisive in an funding thesis. Because the day this information got here out, I’ve seen a variety of evaluation based mostly on bullish theses, as if “the Warren Buffett impact” has utterly erased geopolitical danger. For my part, having crucial and private pondering is the idea of any profitable funding, as a result of copying the operations made by another person (even when it’s the greatest investor in historical past) will not be essentially an excellent technique. Berkshire Hathaway’s (BRK.B) causes for investing in TSMC could also be totally different from these of the common investor, who maybe expects a revenue as early as the following few months.

As well as, one should additionally take into account that for Berkshire to take a position $4.1 billion in an organization represents just one.40% of the entire portfolio. There are numerous points to think about so as to not copy an investor managing a whole bunch of billions of {dollars}, and if you’re you will discover extra info on this article. To put money into TSMC, it isn’t sufficient to know that Warren Buffett did it, however we have to perceive whether or not this firm matches our area of data and whether or not, by our personal quantitative valuation, it’s undervalued.

That mentioned, the conclusion of the article displays my private comparability of ASML and TSMC.

ASML and TSMC from a quantitative perspective current an unusual power, furthermore they’re completely positioned inside a market that’s destined to develop in the long term. If we seemed solely on the numbers, these firms are extraordinarily fascinating, Nonetheless, this isn’t sufficient, as we should additionally take into account the context during which they function. The latter side, in truth, is what leads me to doubt investing in Taiwan Semiconductor in the long run.

China won’t cease urgent TSMC, america won’t again down, and Taiwan is already ready to defend itself in opposition to an assault. Nobody can know precisely what this geopolitical pressure will evolve into, however actually the premises should not rosy. Primarily based on my diploma of danger aversion, with remorse, I favor to keep away from investing in Taiwan Semiconductor since I already know that I might not expertise properly any value fluctuations because of the upcoming information between China and Taiwan. I wished to level out that it’s a remorse for me, for the reason that firm is undoubtedly a cash machine. If it weren’t for this side, I might put money into it at an acceptable value.

The entire world relies upon primarily on TSMC, Samsung and Intel in chip manufacturing, and these firms are warring with one another to supply one of the best chips. Nonetheless, though geographically totally different from one another, they’ve one factor in frequent: all of them rely on ASML’s EUV lithography machines. It’s true that ASML additionally has a geopolitical danger, however it’s restricted to the lack to promote its EUV/DUV machines in China; the remainder of the world in truth should buy them. Personally, I even take into account it extra affordable to put money into Intel quite than TSMC. Along with not having geopolitical danger, current investments in high-NA EUV may skinny the hole with each TSMC and Samsung. I lately wrote an article about this.

To conclude, linking again to the preliminary thesis, whether or not it’s Taiwan Semiconductor, Samsung, or Intel that dominates the semiconductor market sooner or later issues little to ASML, since they are going to all have to purchase its machines anyway. Nobody can know who would be the winner and who would be the loser within the race to supply essentially the most superior chips, however we do know that whoever produces the machines to construct them will profit from the competitors. As within the mid-nineteenth-century gold rush, one of the best technique could change into to not search what everybody needs, however to promote the means to hunt what everybody needs.

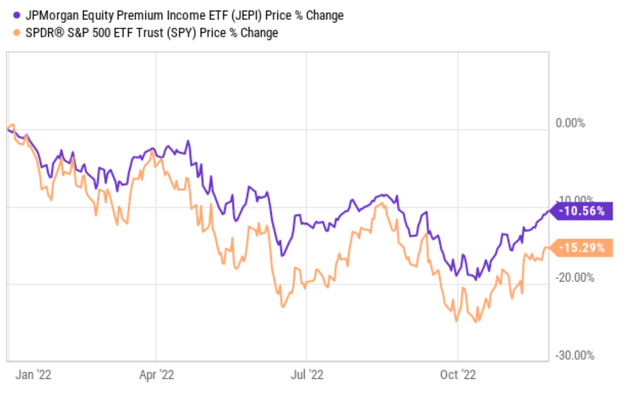

Over the previous 12 months or two, I wrote a number of articles to alert readers about dangers related to the JPMorgan Fairness Premium Revenue ETF (NYSEARCA:JEPI). Once I printed my first article on it again in June 2021, the fund was buying and selling at $61. The fund suffered a couple of 10% worth correction since then however pays a mouthwatering dividend yield of 10%+ as of this writing. Moreover, on a relative foundation, as proven within the following chart, JEPI outperformed the general fairness market by a superb margin. The SPDR S&P 500 Belief ETF (NYSEARCA:SPY) suffered a complete lack of greater than 15% YTD. In consequence, JEPI led the general market approximated by SPY by about 10%.

The above mixture of 10%+ yield and outperformance (even solely in relative phrases) could draw the curiosity of many potential traders. Thus, the logical query is whether or not its outperformance (both relative or absolute) can proceed.

Within the the rest of this text, I’ll argue that the reply is not possible for a number of causes. JEPI’s lead within the brief historical past since its inception was primarily because of the rotation to worth shares and in addition using choices throughout massive market corrections. And if we broaden the historic context a bit, we are going to see such a mix is in direction of its finish. And furthermore, underneath “regular” circumstances (i.e., different market situations), its equal mutual fund the JPMorgan Fairness Premium Revenue Fund Class AA (JEPAX) fund, offers extra historic knowledge and exhibits a special image.

Supply: Searching for Alpha.

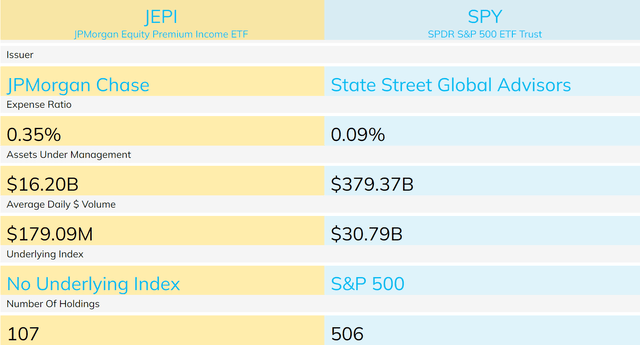

JEPI and SPY: Fundamental data

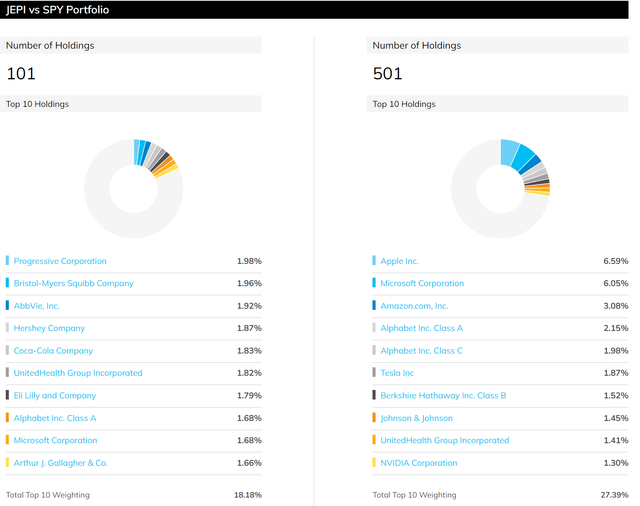

Each JEPI and SPY are listed with the S&P 500 index because the benchmark. Each maintain large-cap shares. SPY’s median market cap is $170.9 billion and JEPI’s is $103.5 billion. As a result of indexing technique and deal with massive caps, lots of their holdings additionally overlap (and we are going to element this later).

Now, the variations. JEPI is actively managed, and SPY is passively listed. In consequence, JPEI’s expense ratio of 0.35% is about 4x increased than the 0.09% charged by SPY.

JEPI makes use of a proprietary technique to hunt a mix of capital appreciation potential, excessive earnings, and low volatility. The technique to realize such a lofty mixture lies in A) the choice of each overvalued and undervalued shares, and B) using choice overlays on these shares. As detailed within the fund description (barely edited with the emphases added by me), the JPEI fund:

Seeks to generate excessive earnings by means of a mix of promoting choices and investing in U.S. massive cap shares.

Constructs a diversified, low volatility fairness portfolio by means of proprietary analysis designed to establish overvalued and undervalued shares with enticing danger/return traits.

Seeks to ship a major portion of the returns related to the S&P 500 Index with much less volatility, along with month-to-month earnings.

Supply: ETF.com

JEPI vs. SPY: Nearer examination of holdings

As simply talked about, each JEPI and SPY are centered on the large-cap house. Since they draw from the identical pool of shares, they overlap fairly a bit even amongst their high 10 holdings as seen from the chart beneath. You see UnitedHealth Group Inc (UNH), Microsoft Corp (MSFT), and Alphabet Inc (GOOGL) (GOOG) in each funds.

Though there are massive variations of their holdings too. First, SPY holds your complete large-cap house (with ~500 shares), however JEPI holds a subset of the large-cap house (with ~100 shares chosen by its proprietary analysis aforementioned). Therefore, JEPI contains a extra concentrated portfolio. Second, JPEI’s choice technique is extra geared towards worth, whereas SPY is listed by market cap. As detailed in JEPI’s fund description (barely edited with emphases added by me),

The fund advisers make use of a 3-step course of that mixes analysis, valuation and inventory choice. The analysis permits the adviser to rank corporations in line with what it believes to be their relative worth… The Fund buys and sells … utilizing the analysis and valuation rankings as a foundation. On the whole, the adviser selects securities which can be recognized as enticing and considers promoting them once they seem much less enticing.

Therefore, in a nutshell, JEPI is extra value-oriented whereas SPY is listed by market cap. And the basic variations of their indexing methods will be simply seen from their high 10 holdings beneath. As seen, JEPI holds extra shares within the conventional worth sectors resembling well being care (e.g., UNH, BMY, and ABBV) and shopper staples (resembling Hershey (HSY) and KO). Furthermore, JEPI holds these shares at a better focus than SPY. Within the meantime, it holds extra growth- and tech-oriented shares resembling MSFT and GOOGL at a decrease focus than SPY. For terribly costly shares like Tesla (TSLA) and Nvidia (NVDA), JEPI avoids them fully.

Supply: ETF.com

Therefore, as talked about above, the lead of JEPI over SPY within the 1 or 2 years was largely because of the substantial correction of the tech and progress sector, which harm SPY greater than JEPI. And if the lead is to proceed sooner or later, then we might want to assume that the worth sectors will hold outperforming progress and know-how shares. Nevertheless, this assumption doesn’t appear to be a sound one at the moment given the present situations.

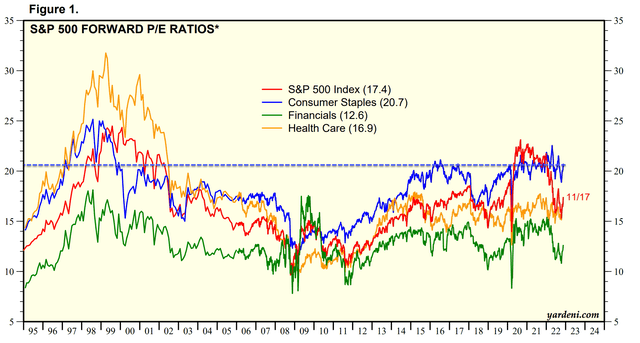

As you may see from the next chart, the S&P 500 index was priced at a big valuation premium in comparison with different sectors throughout 2021 and 2022 with a PE near 24x. Such a PE is sort of 1.6x increased than healthcare (about 15x PE at the moment) and about 10% above shopper staples (about 22x at the moment). Then the correction got here and harm the S&P 500 greater than these worth sectors. To wit, SPY’s present PE is just 17.4x, primarily on par with healthcare’s 16.9x. And it’s considerably beneath shopper staples, which stands at 20.7x PE, a file degree since ~2000.

Supply: Yardeni.com

JEPI vs. SPY: How about using choices?

The usage of choices (within the type of ELNs, Fairness Linked Notes) will help generate excessive earnings, and the earnings will increase as market panic heightens – like what we simply skilled. In JEPI’s case, it employs as much as 20% of its complete belongings on choices. Nevertheless, the choice overlay will restrict the fund’s upside potential as detailed in its fund description (once more, edited with emphases added by me),

So as to generate earnings, the Fund could make investments as much as 20% of its internet belongings in ELNs… ELNs by which the Fund invests are by-product devices which can be specifically designed to mix the financial traits of the S&P 500 Index and written name choices in a single be aware type. The ELNs present recurring money stream to the Fund primarily based on the premiums from the decision… Investing in ELNs could scale back the Fund’s volatility as a result of the earnings from the ELNs would scale back potential losses incurred by the Fund’s fairness portfolio. Nevertheless, the ELN would additionally scale back the Fund’s capability to totally revenue from potential will increase within the worth of its fairness portfolio.

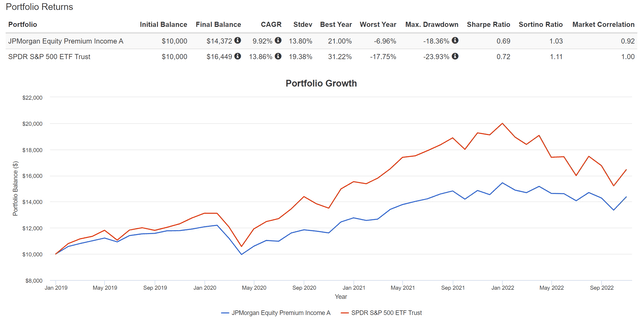

Attributable to JEPI’s brief historical past (it was launched solely in 2021), I’ll use the subsequent chart beneath to point out the roles of the choice overlay. The chart beneath makes use of JEPAX as a proxy to approximate JEPI. The JEPAX is a mutual fund that was launched in Sep 2018 with a method much like JEPI. Therefore, JEPAX offers ~Three years of information to see the function of the choice underneath a broader vary of market situations.

Now you may see that over an extended timeframe, JEPAX lagged SPY by a big margin. Over this time period, SPY supplied a good-looking return of 13.8% every year and a complete return of 64%. In distinction, JEPAX solely returned 9.9% per 12 months and 43% in complete. It lagged SPY by ~5% on a CAGR foundation and 21% on a cumulative complete foundation. And a key basic trigger is using choices that put a ceiling on the upside potential of a superb a part of its belongings.

Supply: PortfolioVisulizer.com

Dangers and closing ideas

To recap, in its brief historical past, JEPI offered traders with a sexy mixture of excessive dividend yield and relative outperformance. To wit, it led SPY by about 5% in complete return YTD and it at the moment offers a 10%+ yield. For potential traders drawn to the fund, the logical query is whether or not its outperformance (both relative or absolute) can proceed.

Sadly, my reply to the query is very seemingly. JEPI’s lead to this point was primarily because of the rotation from progress and tech shares to worth shares. The rotation is at an finish as a result of SPY’s present PE of 17.4x is on par with value-sector resembling well being care and much beneath shopper staples (20.7x). Moreover, JEPI’s choice overlay limits the upside potential in the long term as demonstrated within the case of JEPAX.

To shut, I’d counsel JEPI solely to traders who want present earnings in a easy fund. For many who don’t thoughts some DIY (not that a lot as detailed in my weblog article ), I see a extra dynamic method combining a core fund (resembling SPY) and some tactical holdings as a extra promising technique going ahead. Plus, you get to avoid wasting the 0.35% price charged by JEPI.

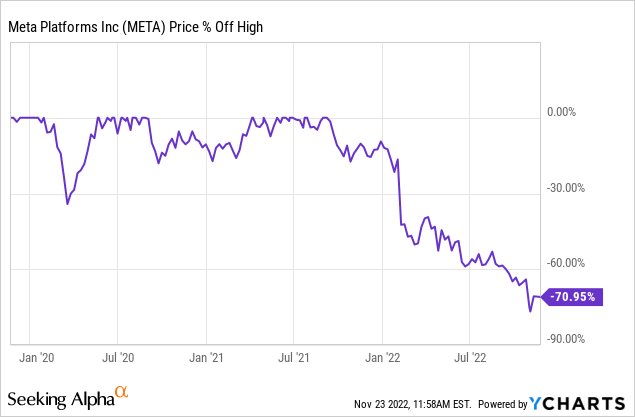

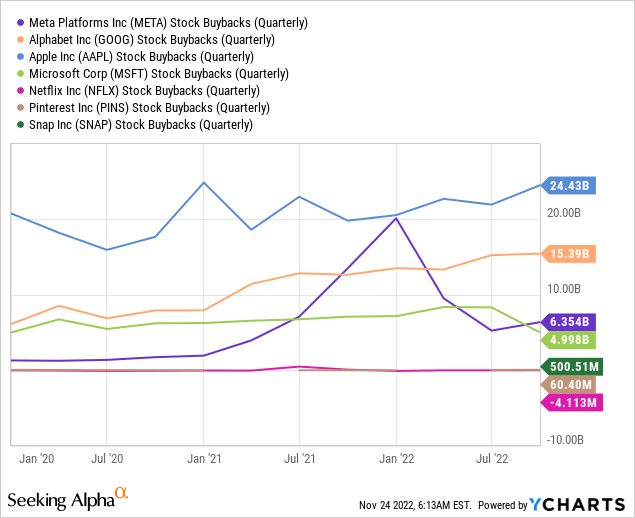

Generations have been evolving all through the years, which has solely been doable by improvements. Modifications made our lives extra environment friendly, safer and created higher dwelling situations. Meta (NASDAQ:META) realigned their embodiment of innovation to fulfill the wants of the next technology. Nevertheless, traders are punishing Meta’s actions. Consequently, the inventory is now down 70% from all-time highs, which makes it a superb time to take a deeper dive.

Information by YCharts

The Core Enterprise

Let’s begin off with saying that Meta’s core enterprise is way from lifeless. Though the promoting market is weaker in the mean time, specifically Europe, it’s nonetheless producing a ton of cash. Yr-over-year promoting income stayed secure in all areas however Europe. Europe’s shopper market is presently extraordinarily weak, that is additionally clearly seen in different companies. So it’s no shock that promoting income is down by 16.3% in Europe, as firms attempt to reduce on advertising efforts within the area.

Meta-Investor Relations Q3 22

Nonetheless, this doesn’t imply individuals are utilizing much less social media. Meta has been in a position to enhance day by day lively folks and month-to-month lively folks on their platforms. Final weekend, I’ve visited Barcelona (Spain), the place I might witness the social media exercise within the metro, prepare and busses. Barcelona, generally known as one of many busiest cities in Europe, is utilizing Instagram, Reels and WhatsApp very incessantly. Abruptly, I’ve not seen a single individual use TikTok. AI developments within the scaling of advice fashions have led to observe time will increase of 15% for Reels. Therefore, I think that individuals are utilizing Reels increasingly more, as a substitute for the competitor TikTok.

Meta-Investor Relations Q3 22

So, Meta’s platforms are fully tremendous and Europe is the one actual laggard for now. Europe just isn’t lagging by way of lively customers, however in income earned per consumer. In Asia-Pacific and the remainder of the world, ARPUs have elevated year-over-year.

Meta-Investor Relations Q3 22

Personally, I nonetheless see alternatives of development within the core enterprise. Reels has a superb likelihood to take again market share from TikTok. Reels are included in Instagram and Fb, which makes it a greater all-in-one expertise. Additional, the monetization of Messenger and WhatsApp is one other big alternative. Mark Zuckerberg, CEO of Meta, mentioned within the Q3 2022 earnings name:

We began with Click on-to-Messaging advertisements, which let companies run advertisements on Fb and Instagram that begin a thread on Messenger, WhatsApp or Instagram Direct to allow them to talk with prospects immediately. That is one in every of our quickest rising advertisements merchandise, with a $9 billion annual run fee. This income is totally on Click on-to-Messenger as we speak since we began there first, however Click on-to-WhatsApp simply handed a $1.5 billion run fee, rising greater than 80% year-over-year.

Paid messaging is one other alternative that we’re beginning to faucet into, and it continues to develop rapidly however from a smaller base. We’re placing the muse in place now to scale this with key partnerships like Salesforce, which lets all companies on their platform use WhatsApp as the principle messaging service to reply buyer questions, ship updates, and promote immediately in chat. We additionally launched JioMart on WhatsApp in India and it is our first end-to-end procuring expertise that reveals the potential for chatbased commerce by means of messaging.

Between Click on-to-Messaging and paid messaging, I’m assured that that is going to be a giant alternative.

Click on-to-Messenger/WhatsApp is rising extraordinarily quick and will take an even bigger share of complete income within the following years.

Total, promoting is experiencing a brief downturn, however this shouldn’t be troublesome for traders in the long run, because the underlying enterprise remains to be sturdy.

The Valuation

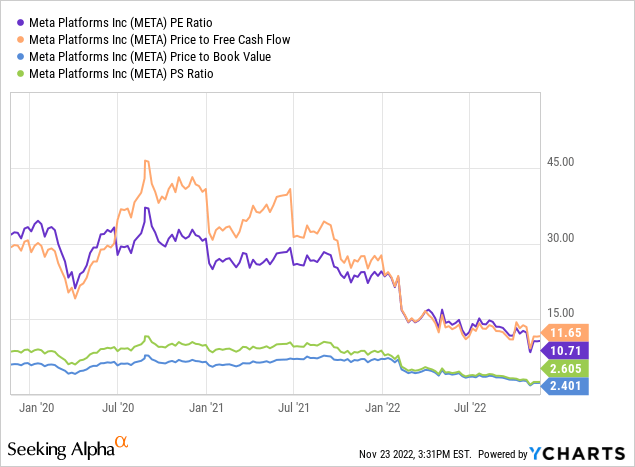

Up to now, I’ve not talked concerning the metaverse enterprise, given that it doesn’t matter. Meta is buying and selling at 11.65x earnings and 10.71x free money move, even within the COVID-19 crash the corporate was not this low-cost. The metaverse has a unfavourable affect on PE and PFCF ratios, because it generates unfavourable earnings and desires a whole lot of free money move, but these metrics are going decrease.

So, if Meta’s journey within the metaverse involves an finish, no extra unfavourable impacts on earnings and free money move, then the inventory would look much more discounted. Equally, if the metaverse begins producing optimistic earnings and free money move, then the inventory would additionally look extra discounted. Additional, the present valuation might be the underside, as Meta is slicing prices and the core enterprise and the greenback energy is stabilizing.

Information by YCharts

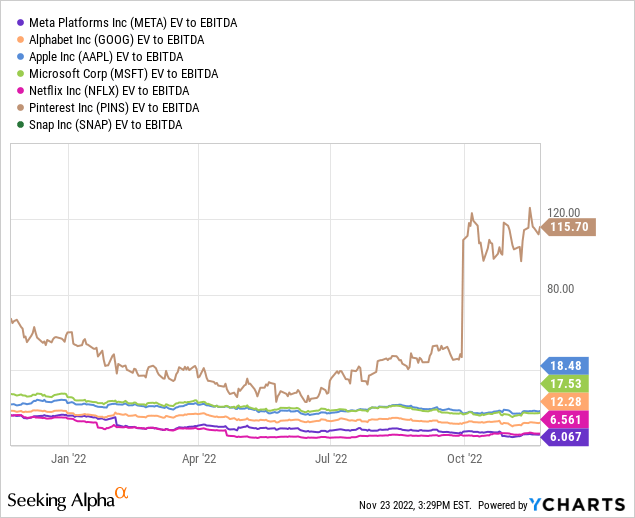

By way of EV-to-EBITDA, solely Netflix (NFLX) is near the valuation of Meta. Different friends and advertising-based firms commerce at a big increased a number of.

Information by YCharts

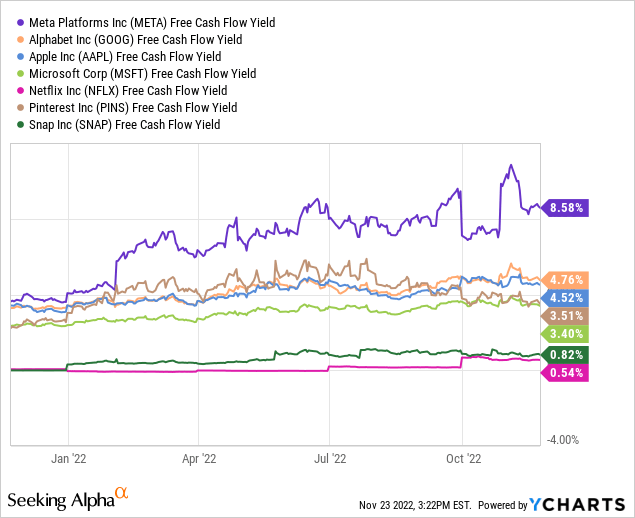

As well as, Meta’s free-cash-flow yield is manner superior than firms like Alphabet (GOOG) and Apple (AAPL). Subsequently, Meta seems to be discounted based mostly on fundamentals. One may argue that Apple, Microsoft (MSFT) and Alphabet are increased high quality companies and deserve a extra premium valuation. Nevertheless, the discrepancy between them is simply too giant for me to contemplate that argument.

Information by YCharts

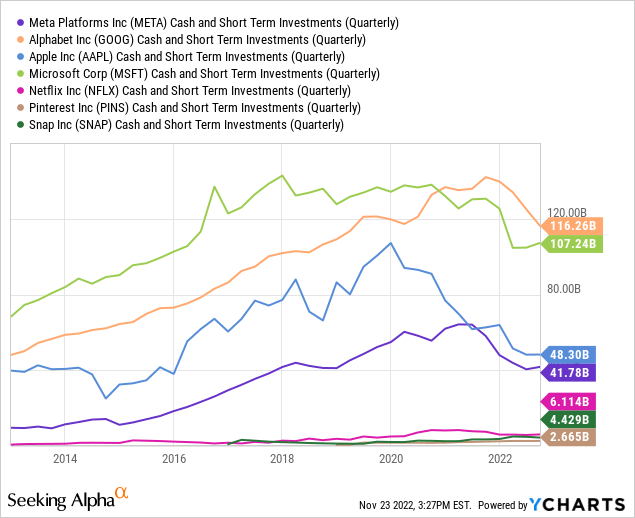

Lastly, Meta’s liquidity is matching that of Apple’s. The stability sheet makes it doable to do investments or give again to shareholders by means of buybacks. Meta has been actively shopping for again shares, but the corporate nonetheless has 14% of the present market cap in liquidity. Snap (SNAP)’s and Pinterest (PINS)’s money and short-term investments are exhausting to match with that of the bigger firms.

Information by YChartsInformation by YCharts

The Metaverse

I’ve all the time had this thought; that no matter is unknown, is strenuous to grasp, till it turns into actuality. Attempting to think about what lies past the identified boundaries of the universe is a reasonably troublesome train. What creatures might be on the market? Your thoughts will flood you with photographs that you’ve seen prior to now; however cannot there be one thing new that has by no means been seen earlier than? One thing even your thoughts struggles to examine…

There’s… and it’s known as innovation. Innovation is a broad time period and stands for implementing a brand new product, service or course of. As traders, we’re cautious about this time period:

Because the earnings that firms can earn are finite, the value that traders needs to be prepared to pay for shares should even be finite – Benjamin Graham.

The metaverse is nearly totally calculated into the inventory worth. To not the upside, however to the draw back. Traders assume nothing will come out of the Metaverse, for that motive, the inventory is likely to be an important alternative. As we all know, a decreased inventory worth lowers the chance and creates the next doable return. The inventory is now down 70%, which implies the inventory is much less dangerous than it was at increased costs. Subsequently, I might say that the margin of security on Meta is sizeable at as we speak’s worth.

Nevertheless, if the metaverse would in some way handle to make some optimistic free money move, the inventory worth might see some promising returns. And as a matter of reality, the metaverse does look fairly reasonable. Studying by means of imaginative and prescient and bodily training are the perfect methods to enhance your abilities. Globalization might be much more environment friendly than the present web of issues that we’ve now. Moreover, productiveness has nonetheless room to develop. Individuals need progress, one thing higher, extra environment friendly, compact and so forth… If these issues can be found, it is going to be purchased very quickly.

Nevertheless, I do agree that Meta’s storytelling has not been the perfect. It is vitally necessary to grasp that the metaverse doesn’t solely resemble digital actuality, but additionally augmented actuality. Not like digital actuality, which creates a very synthetic atmosphere, augmented actuality customers expertise a real-world atmosphere with generated perceptual data overlaid on high of it.

Personally, I see extra real-life use in augmented actuality. In the intervening time, deaf folks lastly have an opportunity to create significant conversations by means of augmented actuality glasses. The glasses can transcript spoken language to subtitles that seem within the glasses.

Proper now, I’m writing this text on my laptop with a second display screen. However with the Meta headset, you’ll be able to have as many screens as you need and even select the place to position them with augmented actuality. Moreover, the screens can have touchscreen functionalities to extend productiveness. House and cable administration received’t be an issue any longer.

Meta – Web site

This innovation just isn’t all glamour, the corporate is spending billions of {dollars} within the mission, which is absorbing a whole lot of the free money move. But, you will need to know that Meta just isn’t solely spending on the metaverse. Meta is in a brand new funding cycle to enhance infrastructure, increase AI capability and produce extra information heart capability on-line. In Q3, Meta spent $4billion on Actuality Labs, the remaining went into different components of the enterprise. For instance, AI developments have led to observe time will increase for Reels.

Meta-Investor Relations Q3 22

Meta is partnering up with firms like Microsoft, Adobe (ADBE), Autodesk (ADSK), Zoom (ZM), Accenture (ACN) and plenty of extra to create new options and functions on the metaverse units.

Investing in a start-up is kind of dangerous as the corporate just isn’t making any cash, burns money and dilutes shareholders. In an growing rate of interest atmosphere, it’s not as straightforward as earlier than to get maintain on capital. Consequently, it needs to be averted by clever traders. Nonetheless, Meta has the capital, the infrastructure and a powerful underlying enterprise to make this metaverse start-up work.

Takeaway

The downturn within the promoting cycle mixed with towering investments make Meta a scary place for traders. The corporate is now more durable to mannequin with numbers and enterprise analysts are blacked out.

Even so, Meta’s enterprise has been round for nearly 2 a long time, has a powerful core enterprise with 2.93 billion day by day customers and doesn’t dilute shareholders (the truth is in lowering excellent share rely). Would you actually thoughts them innovating to fulfill the wants of the subsequent technology?

Absolutely, free money move will probably be struggling for some years by the excessive investments. However higher returns might come ahead shortly within the Reels, Messenger and WhatsApp segments, because the core enterprise just isn’t out of focus. The weak promoting market and the sturdy greenback headwinds briefly overshadow the standard of the enterprise.

For my part, traders are manner too bearish; due to this fact I see worth in Meta. The danger-reward stability is beneficial on the present costs. I’ll say that Alphabet gives a safer deal for me with much less threat and the same reward. At all times keep in mind that it’s a must to search for an funding that matches you.

I fee Meta a Purchase. Should the inventory worth go down beneath $100 a share, I would re-rate it to a Robust Purchase.

Let’s finish with a considerate quote of Carl Jung:

The creation of one thing new just isn’t completed by the mind however by the play intuition appearing from inside necessity. The inventive thoughts performs with the objects it loves.

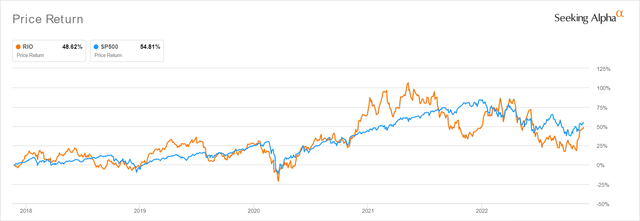

Contemplating China’s progressive stimulus price $146B and potential reopening post-Zero Covid Coverage, it’s no marvel that the Rio Tinto Group (NYSE:RIO) inventory has rallied by 24.74% over the previous few weeks, considerably aided by the upbeat October CPI studies. Due to this fact, we might even see greater iron ore imports by H2’22, because the nation consumed 1.12B tons of the fabric in 2021, accounting for 43.07% of the worldwide manufacturing then. Moreover, 75.8% of analysts at the moment are projecting that the Feds will pivot early with a 50 foundation factors hike, as seen by the Financial institution of Canada’s latest moderation. Assuming so, we might even see this tsunami of confidence lifting all boats reasonably from 14 December onwards.

However, relying on how the scenario develops, we doubt that this optimism is sustainable over the subsequent few weeks (or months). Most notably, Apple (AAPL) is reportedly having bother securing staff for the Zhengzhou manufacturing unit in China, because of the overly strict quarantine protocols and, consequently, triggering violent riots delaying manufacturing. That is regardless of the supposed ‘focused and exact’ strategy from Beijing and native authorities alike, in an try to reduce the affect on financial development. The ensuing employee unrest has contributed to world delays within the iPhone 14 deliveries, since 4 in 5 iPhones are assembled there. Thereby, triggering extra suspicions amongst the watching worldwide viewers.

There isn’t any telling when President Xi Jin Ping will lastly relent on its hardline strategy, because the latter continues to hinder the restoration of home property and labor sectors. The Chinese language chief has beforehand clamped down on speculative frenzies and induced an ongoing property disaster, as costs proceed to fall drastically since June 2021. It nonetheless stays to be seen, if the latest $30B stimulus is ready to revive the extremely indebted builders. With the housing market in a deep disaster and restricted catalysts for restoration, China’s reopening progress and iron ore urge for food stay dangerously unsure.

RIO Faces Margin Headwinds With Unsure Prospects Forward

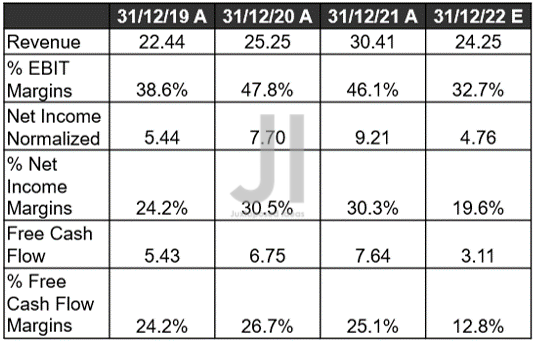

RIO Income, Web Earnings ( in billion $ ) %, EBIT %, andFCF %

S&P Capital IQ

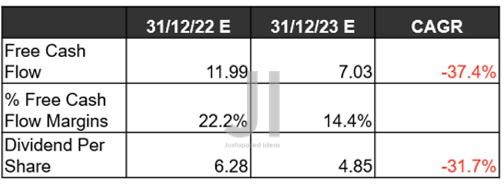

For its upcoming earnings name in February 2023, RIO is predicted to report revenues of $24.25B with EBIT margins of 32.7%, indicating a drastic decline of -20.25% and -13.Four share factors YoY, respectively. With its profitability additionally probably affected by -48.31% and -10.7 share factors YoY, the corporate’s Free Money Stream technology could also be tragically halved to $3.11B then. Due to this fact, it’s no marvel that the inventory has additionally beforehand hit all-time low with a -36.88% plunge from earlier peak optimism ranges of $84 in March 2022.

RIO Projected Income, Web Earnings ( in billion $ ) %

S&P Capital IQ

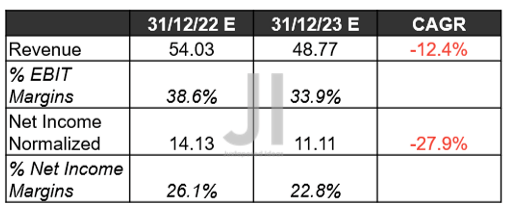

As a result of normalization of iron ore costs, RIO is predicted to report a notable -9.73% drop in top-line development for FY2023, considerably worsened by peak recessionary fears. Its projected EBIT margins of 33.9% additionally symbolize one other underperformance in opposition to pre-pandemic ranges of 39%. Thereby, additionally impacting its profitability by -21.37% YoY, with naturally declining margins to 22.8%, in opposition to FY2019 ranges of 24%.

It’s obvious that Mr. Market is extra bearish than we thought, since RIO’s operations could additional undergo from cyclical price inflation and elevated vitality prices within the brief time period.

RIO ProjectedFCF ( in billion $ ) % and Dividends

S&P Capital IQ

It’s no marvel then, that RIO selected to chop dividends to $2.67 for H1’22, comprising 50% of earnings in opposition to H1’21 ranges of 75%. The administration’s prudent name has allowed for a more healthy stability sheet, with money and equivalents of $11.4B by the top of final quarter. Nevertheless, market analysts are additionally comparatively optimistic that the corporate will revert to its earlier stance by H2’22. That is because of the projected $3.61 payout then, indicating a wonderful annual yield of 11.41% for individuals who had entered on the mid $50s. We’re extra real looking with in-line payouts $2.67, sadly.

Moreover, we anticipate to see extra headwinds to RIO’s inventory efficiency, since its FCF margins are anticipated to additional deteriorate to 14.4% by FY2023, in opposition to FY2019 ranges of 21.8% and FY2021 of 28.3%. Thereby, additionally impacting its projected dividends payout subsequent yr, with a possible YoY reduce of -22.77% then.

However, market analysts additionally anticipate RIO to proceed paying down debt, because it did up to now few quarters. By the newest quarter, the corporate has efficiently paid off -$2.13B of its long-term money owed since H2’20, whereas anticipated to additional deleverage by -$1.5B via FY2023. Moreover, buyers needn’t fear, because the weighted common maturity is estimated at ten years, with the closest one due by 2024 at $1.5B. Thereby, securing the corporate’s rapid liquidity via the unsure financial situations forward.

So, Is RIO Inventory A Purchase, Promote, or Maintain?

RIO YTD EV/Income and P/E Valuations

S&P Capital IQ

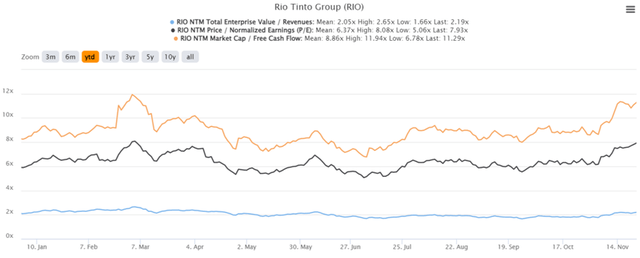

RIO is presently buying and selling at an EV/NTM Income of two.19x, NTM P/E of seven.93x, and NTM Market Cap/ FCF of 11.29x, comparatively inflated close to its YTD highs of two.65x, 8.08x, and 11.94x, respectively. Nonetheless, we’ve got to confess these ranges are nonetheless considerably affordable in comparison with its 5Y means of two.44x, 8.57x, and 10.86x, respectively. In that case, buyers who don’t thoughts the smaller margin of security should still nibble at a value goal of roughly mid $50s to $60s. Portfolios ought to naturally be sized appropriately, within the occasion of volatility as properly.

Iron Ore Costs

Buying and selling Economics

For now, iron ore spot costs have additionally briefly lifted from $73.62 to $98 per tonne on the time of writing, nearer to pre-pandemic highs in 2019. Nevertheless, bulls would probably nonetheless be discouraged by the huge distinction of -18.30% from latest highs in August 2022 or a catastrophic -56% plunge because the peak in Might 2021. Within the brief time period, we anticipate demand and costs to stay stunted till property markets increase once more globally. Issues are unlikely to enhance, because of the cooling property markets within the US & unsure Zero Covid Coverage in China. Ouch, since each nations comprise 73.61% of RIO’s revenues in FY2021.

One other phrase of warning, because the Feds could not pivot this early, because of the raised terminal charges of over 6%. Assuming so, we might even see one other backside re-test, as seen in July and September 2022. Consequently, conservative buyers could need to anticipate extra readability earlier than including RIO to their portfolio. There isn’t any level chasing this rally.

A necessity to repair or save others is an indication that we have to repair ourselves.

Saviors typically have hero complexes; they imagine their love may help somebody or change them for the higher.

MONTREAL (PRWEB)October 11, 2022

Most individuals would give a large berth to potential companions who’re addicts, behave unpredictably, or carry quite a lot of emotional baggage. Why tackle the burden of another person’s issues? Why attempt to assist an individual who could not even need to change? Compassion definitely performs a job, as does the love of a problem, a hero advanced, and admittedly, the thrill of courting somebody “unhealthy” or rebellious, however a current examine by PsychTests.com factors to deeper points.

Analyzing information collected from 3,279 individuals who took the Relationship Attachment Type Take a look at, PsychTests’ researchers in contrast the persona profile of two distinct teams: people who find themselves drawn to companions who’ve issues, comparable to addictions or private points (henceforth labeled as “Saviors”), and those that favor to not date problematic companions (labeled as “Averters”) .

Right here’s what their examine revealed:

INDIVIDUALS WHO DATE PROBLEMATIC ROMANTIC PARTNERS ARE MORE LIKELY TO BE UNCOMFORTABLE WITH INTIMACY/CLOSENESS

> 56% of Saviors stated they’ve bother creating an emotional reference to somebody (in comparison with 30% of Averters).

> 69% are uncomfortable relying on different individuals (vs. 57% of Averters).

> 34% are commitment-phobic (vs. 19% of Averters).

> 63% stated that they discover it exhausting to “let their partitions down” (vs. 47% of Averters).

> 29% really feel an urge to depart when a relationship begins to turn out to be shut (vs. 13% of Averters).

> 72% have belief points (vs. 36% of Averters).

INDIVIDUALS WHO DATE PROBLEMATIC ROMANTIC PARTNERS MAY OFTEN RELY ON OTHERS TO MAKE THEM FEEL GOOD ABOUT THEMSELVES

> 22% of Saviors stated that they really feel like a “no person” except they’re in a relationship (vs. 6% of Averters).

> 35% admitted that their sense of self-worth relies upon totally on their associate’s opinion of them (vs. 15% of Averters).

INDIVIDUALS WHO DATE PROBLEMATIC ROMANTIC PARTNERS NEED TO BE NEEDED

> 42% of Saviors really feel resentful when their associate refuses their assist (vs. 18% of Averters).

> 30% are happier when their associate is totally depending on them (vs. 14% of Averters).

> 35% favor to be in complete management of the connection (vs. 19% of Averters).

INDIVIDUALS WHO DATE PROBLEMATIC ROMANTIC PARTNERS ARE MORE LIKELY TO BE PEOPLE-PLEASERS

> 53% of Saviors disregard their private preferences with the intention to make others glad (vs. 25% of Averters).

> 48% neglect their very own wants and focus totally on the wants of their associate (vs. 20% of Averters).

> 20% would cease seeing their buddies if their associate demanded it (vs. 7% of Averters).

> 25% assume complete accountability for his or her associate’s happiness (vs. 10% of Averters).

INDIVIDUALS WHO DATE PROBLEMATIC ROMANTIC PARTNERS ARE OFTEN TERRIFIED OF BEING ALONE

> 52% of Saviors fear incessantly about being dumped (vs. 25% of Averters).

> 51% cling to their relationships as if their life trusted it (vs. 18% of Averters).

> 27% would do something to maintain their associate as a result of they do not assume they’re going to have the ability to discover anybody else (vs. 12% of Averters).

> 19% grew to become so clingy that they scared off earlier companions (vs. 5% of Averters).

> 24% stated that they would not depart a relationship even when they had been being mistreated or abused by their associate (vs. 9% of Averters).

“Relationship somebody who has points serves two functions: First, it makes you are feeling wanted, which might increase your sense of self-worth,” explains Dr. Ilona Jerabek, president of PsychTests. “‘Saviors’ typically have hero complexes; they imagine their love may help somebody or change them for the higher. Second, courting an individual who has issues is, oddly, a safer selection, within the sense that if this individual leaves you, it’s going to nonetheless damage however it can save you face by blaming it on their habit, unhealthy relationship historical past, or no matter their difficulty is. In case you had been to be dumped by somebody who’s emotionally wholesome, you’ll be pressured to look deeper at your self and the way your actions contributed to the demise of the connection, and that form of interior reflection isn’t one thing Saviors are comfy doing.”

“We’re drawn to companions we really feel we deserve,” continues Dr. Jerabek. “In case your shallowness is wobbly then it’s possible you’ll pursue individuals who really feel equally insufficient or who deal with you poorly. Saviors typically have their very own demons to take care of, whether or not it’s a historical past of abuse, of coping with a mother or father who was an addict, emotional neglect, or a determined want for approval. When you’ve got gone unloved and unappreciated your complete life and you discover somebody who wants you, it’s exhausting to stroll away. the individual isn’t good for you, however you need to be needed. That is the kind of dynamic that usually kinds the premise of codependent relationships, the place one individual is the dependent and the opposite is the hero, savior, giver and, primarily, the enabler. The fact is that each companions are simply utilizing one another, albeit subconsciously.”

What’s your attachment type? Discover out by visiting the Relationship Attachment Type Take a look at right here: //testyourself.psychtests.com/testid/2859

Skilled customers, comparable to HR managers, coaches, and therapists, can request a free demo for this or different assessments from ARCH Profile’s intensive battery: //hrtests.archprofile.com/testdrive_gen_1

To study extra about psychological testing, obtain this free eBook: //hrtests.archprofile.com/personality-tests-in-hr

About PsychTests AIM Inc.

PsychTests AIM Inc. initially appeared on the web scene in 1996. Since its inception, it has turn out to be a pre-eminent supplier of psychological evaluation services and products to human useful resource personnel, therapists and coaches, lecturers, researchers and a bunch of different professionals all over the world. PsychTests AIM Inc. employees is comprised of a devoted staff of psychologists, take a look at builders, researchers, statisticians, writers, and synthetic intelligence specialists (see ARCHProfile.com).

Dr. Bawa says that ladies who “faux” satisfaction within the bed room are dishonest themselves and their associate out of true achievement by pretending that every thing is OK. The reality will assist fulfill one another’s wishes.

LONDON (PRWEB)June 30, 2022

Dr. Kanwal Bawa is visiting the UK July four although 7 to debate the “Orgasm Hole” with Londoners and to coach the general public about sexual and intimate wellness remedies to rework their lives.

Dr. Bawa’s Dr. Intercourse Fairy podcast is within the prime 10% globally. Her TikTok account skyrocketed to over 28 million views and 334,000 followers simply two months after launch, that includes informative and entertaining movies on sexual and intimate wellness.

Dr. Bawa says that ladies who “faux” satisfaction within the bed room are dishonest themselves and their associate out of true achievement by pretending that every thing is OK. The reality will assist fulfill one another’s wishes and orgasmic potential.

The Orgasm Hole is a time period used to explain the disparity in orgasms between sexes. Research have used it to measure sexual satisfaction amongst totally different teams and have discovered that there’s a appreciable distinction between the variety of orgasms women and men are having in heterosexual relationships.

“The Orgasm Hole doesn’t simply exist between heterosexual women and men. It’s fascinating to notice that that lesbian and bisexual ladies report considerably extra orgasms than their heterosexual feminine counterparts,” says Dr. Bawa.

“Well-liked tradition contributes to the difficulty,” says Dr. Bawa. “Actors in love scenes are likely to observe a predictable formulation: sizzling, passionate and euphoric. In Emma Thompson’s new movie, ‘Good Luck to You, Leo Grande,’ she performs a widowed instructor who hires a male escort within the hope of getting her first orgasm late in life, a theme seen as pushing the boundaries.”

Dr. Kanwal Bawa is a Cleveland Clinic skilled doctor in Boca Raton, Florida, coming quickly to Miami and different cities. She focuses on sexual and intimate wellness, beauty and laser surgical procedure, hair restoration and anti-aging remedies. She can be lively in caring for the LGBTQ+ neighborhood, particularly for transitioning transgender people.

Love Tales TV, the worldwide content material chief in inspirational, actual love tales as leisure, right this moment introduced its large library of professionally produced wedding ceremony movies is accessible as a 24/7 FAST channel on Video On Demand platform Rakuten TV throughout Europe.

The 2022-2023 wedding ceremony season is the busiest in 40+ years and demand from shoppers and advertisers for wedding ceremony content material is at an all time excessive. Love Tales TV, the primary and solely linked TV channel within the $300 billion world wedding ceremony trade, is bringing its content material to Europe through a partnership with Rakuten TV. “We’re thrilled to be teaming up with Rakuten TV, one in all main Video on Demand platforms in Europe, to succeed in new audiences and make it simpler than ever for viewers to observe unbelievable actual weddings, by probably the most proficient filmmakers on the planet,” says Love Tales TV CEO Rachel Jo Silver.

Viewers of the Love Tales TV channel shall be impressed by actual weddings like: this folksy, boho elopement within the Transylvanian Alps, a magical engagement movie from The Czech Republic, a sublime vacation spot wedding ceremony in Aix, this gorgeous elopement atop the hills in Greece, and a glamorous, French wedding ceremony in Provence.

As the one wedding ceremony media model with a streaming tv channel, Love Tales TV is creating distinctive and unique alternatives for manufacturers and advertisers searching for entry to the explosive linked TV market. Love Tales TV has partnered with Wurl to energy the expertise and promoting options behind its new FAST channel which is able to launch within the US on Sling, Native Now, TCL, and Vidaa Hisense within the coming weeks.

The corporate has seen sustained year-over-year development, producing 800M month-to-month video views throughout Snapchat, YouTube, TikTok, and its different channels.

About Love Tales TV

Love Tales TV is a world media model which supplies leisure and wedding ceremony inspiration by uplifting, top quality, and emotional video content material. As the one video platform in a $300 billion trade, Love Tales TV reaches 40M+ month-to-month viewers by their web site, social, and streaming TV channel. Love Tales TV has the trade’s solely streaming TV and Snap Uncover channels, largest YouTube and TikTok channels, in addition to deeply engaged audiences on Instagram, Fb, Pinterest, and extra. On lovestoriestv.com the corporate has a library of 25,000+ professionally produced actual wedding ceremony movies contributed by videographers from all around the world. Every video is tagged with the marriage information and particulars which populates right into a market of 50,000+ wedding ceremony professionals that {couples} use to browse, uncover, and call professionals for his or her wedding ceremony. //www.lovestoriestv.com

About Rakuten TV

Rakuten TV is among the main Video On-Demand platforms in Europe that mixes TVOD (Transactional video-on-demand), AVOD (Promoting video-on-demand), FAST (Free Advert-Supported Streaming TV) and SVOD (Subscription video-on-demand).

The TVOD service gives an genuine cinematic expertise with the most recent releases to purchase or lease in excessive audio and video high quality. The SVOD service permits subscription to the premium service Starzplay. The advertising-supported providing includes AVOD and FAST providers. The AVOD service options greater than 10,000 titles obtainable on-demand, together with movies, documentaries and collection from Hollywood and native studios, in addition to the Rakuten Tales catalogue with Unique and Unique content material. The FAST service consists of an intensive line-up of over 250 free linear channels from world networks, high European broadcasters and media teams, and the platform’s personal thematic channels with curated content material. Rakuten TV is accessible in 43 European territories and presently reaches greater than 110 million households through its branded remote-control button and pre-installed app in Sensible TV units.

Rakuten TV is a part of Rakuten Group, Inc., one of many world’s main web providers firms, specializing in e-commerce, fintech, digital content material, and communications. Rakuten is the official associate for the NBA, the Golden State Warriors, Davis Cup and Spartan Race.

//www.rakuten.television

About Wurl

Wurl, the world chief in powering streaming TV, interconnects over 1200 streaming channels from the world’s high content material firms with the main streaming distribution providers in over 50 nations. The Wurl Community platform helps main studios corresponding to A+E Networks, AMC Networks, Bloomberg, BBC Studios, CNNi, Reuters, and Sony Studios, ship programming to the most important streaming platforms, together with Amazon IMDb TV, Roku, Samsung TV Plus, LG Channels, Rakuten, Twitch, and VIZIO, whereas maximizing monetization. Reaching over 300 million linked TVs across the globe, Wurl makes it easy for content material firms to construct and monitor world distribution for branded linear channels, reside occasions, and on-demand programming to handle and monetize their advert stock. The corporate additionally just lately introduced its new efficiency advertising and marketing service, Wurl Carry out, designed to cut back churn, purchase new viewers and enhance return on advert spend. Wurl is headquartered in Palo Alto, California.

Condoms alone is not going to forestall STIs, those self same STIs might be unfold by different sexual contact i.e., cunnilingus, anilingus, which is why the corporate additionally contains “Intimate Oral Dams”, often known as dental dams, in each considered one of their Intimacy Kits.

TORONTO (PRWEB)April 12, 2022

When used appropriately the male “Intimate Condoms™” are 98% efficient in stopping STIs & undesirable pregnancies. Nevertheless, those self same STIs might be unfold by different sexual contact i.e., cunnilingus, anilingus, which is why the corporate additionally contains “Intimate Oral Dams”, often known as dental dams, in each considered one of their Intimacy Kits.