Searching for Alpha’s transcripts crew is accountable for the event of all of our transcript-related initiatives. We at the moment publish 1000’s of quarterly earnings calls per quarter on our website and are persevering with to develop and develop our protection. The aim of this profile is to permit us to share with our readers new transcript-related developments. Thanks, SA Transcripts Crew

There are a number of buzzwords that increase concern and angst amongst traders, and “chapter” is certainly certainly one of them. When traders hear these phrases, they promote. When different traders are promoting, it is time to search for the chance they’re leaving behind. As an earnings investor, I perceive that when the market panics, it is a possibility for me to purchase earnings at a reduced worth.

At present we will speak about an organization that noticed a sell-off because of the phrase “chapter.” No, the corporate did not file for chapter. Removed from it, the corporate has an investment-grade steadiness sheet, over $1 billion in liquidity, and well-laddered debt maturities. It has a defensive steadiness sheet that did not falter within the face of COVID.

EPR Properties (NYSE:EPR) was hit with guilt by affiliation. A high tenant filed for chapter, and its share worth fell. Buyers bought with out asking themselves what it meant for the corporate.

Now, EPR has up to date shareholders as Cineworld exits chapter, and it seems that the world did not finish. EPR remains to be gathering lease, and it negotiated a deal that gives the chance for extra upside sooner or later. Let’s have a look.

EPR Properties Updates On Regal Cinemas

Late final yr, EPR Properties noticed its share worth collapse in response to a big tenant submitting chapter. When this information first broke, we mentioned our outlook and our technique, saying:

“EPR’s administration is top-notch and they’re going to be capable to cope with no matter points Regal presents. The underside line is that the properties are important to the enterprise and are cash-flow constructive on the property stage.

It’s too early to “again up the truck” now. We’re reducing our purchase below on EPR to mirror our expectations of this headwind, nevertheless, we don’t anticipate danger to the dividend, and we anticipate to carry EPR by way of Cineworld’s reorganization.”

A key in actual property is that the owner can’t be pressured to renegotiate a lease. Because of this, the owner has plenty of leverage in any negotiations as a result of, at any time, they will merely demand that the tenant vacate the property. For a theater, that often means leaving a big quantity of private property behind and shedding 100% of the income. What’s a theater firm with no theater?

EPR additional protected itself with a “grasp lease.” A grasp lease is a lease settlement that covers a number of properties. If a tenant defaults on one property, it ends in a default on all properties. This protects the owner by making certain {that a} tenant cannot simply stroll away from a single poor-performing property. In the event that they need to preserve their “good” properties, they should pay lease on all properties.

So, whereas EPR was prepared to renegotiate the lease with Regal – in any case, EPR did not actually need all of Regal’s properties to be vacated – EPR did go to the negotiating desk with important leverage. Essentially the most highly effective lever to have obtainable in any negotiation is the flexibility to stroll away, and the opposite facet to know you’ve gotten the flexibility to stroll away. Regal wanted to lease EPR’s properties greater than EPR wanted Regal’s lease.

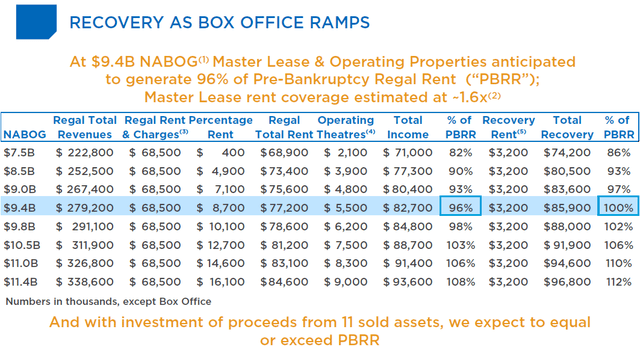

Previous to the chapter, Regal was paying EPR roughly $86.Three million in whole revenues. Beneath the brand new settlement, Regal can pay:

$65 million in base lease, topic to a 10% escalator on annual lease each 5 years.

Reimburse EPR for property-level bills (roughly $3.5 million)

Annual share lease on all revenues exceeding $220 million.

Moreover, EPR will take possession of 16 Regal properties, 5 of which can be leased to different operators and 11 of which EPR intends to promote. So, along with what EPR is gathering from Regal, it would have income from the brand new tenants, plus money that may be reinvested from the bought properties.

Due to the variable part, EPR is taking over some danger, but it surely’s skewed towards the upside. For revenues to be the identical as pre-bankruptcy, EPR wants Regal to have gross revenues of $279.2 million. Here’s what the maths appears like: Supply

EPR June 28th Presentation

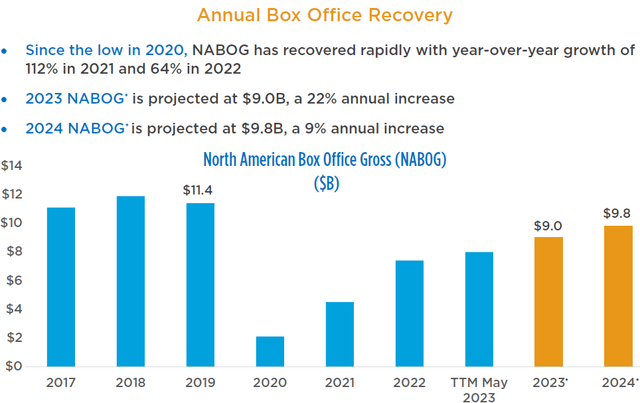

They estimate that might correlate to NABOG (North American Field Workplace Gross) of $9.four billion.

EPR June 28th Presentation

Be aware that at $9.four billion, field workplace receipts would nonetheless be nicely beneath pre-COVID ranges. With a restoration to pre-COVID ranges, EPR may very well be 110%-plus the prior lease settlement. If revenues fail to get well and stay at present ranges, EPR could be a small hit, gathering 93%-97% of pre-bankruptcy lease. One thing that might be recovered with the escalator on base lease.

General, this new lease construction does an important job at offering an affordable base lease for EPR, plus some upside if the field workplace continues to get well to pre-COVID ranges. In fact, all negotiations include some give and take.

The biggest factor that EPR is giving up is that it agreed to cease gathering on the $51.eight million in lease that was deferred throughout COVID. If Regal doesn’t default on the brand new lease for 15 years, that lease can be forgiven.

For shareholders, this deal is a constructive. It gives a transparent outlook for EPR to keep up its present dividend and has ample upside for dividend progress later this yr or early subsequent yr. With this problem behind it, EPR can now look towards the long run.

Conclusion

This can be a pretty widespread incidence available in the market. A tenant information for chapter and the value of the owner falters; a borrower defaults and lenders are punished. On the one hand, we do want to acknowledge that this stuff can have a monetary affect on the owner or lender. Then again, we have to acknowledge that chapter court docket exists for the aim of making certain that the events who’re owed cash get the absolute best restoration.

As a landlord, EPR entered into these negotiations with a positive place. If you wish to use actual property that is not yours, it’s a must to pay lease – it is that easy. At any second, EPR had the ability to stroll away from the negotiations and demand that Regal pay lease as agreed or abandon all the properties.

EPR had an incentive to offer in just a little since backfilling all of the properties would have been an costly and time-consuming process. Understanding a deal that saved Regal in enterprise was positively higher than one that might pressure them out of enterprise.

On the finish of the day, the affect on EPR’s enterprise is really minimal. They anticipate to get well 93%-97% of pre-bankruptcy lease to start out, with the potential for it to develop over 100% of the prior contract if the film business recovers to pre-COVID ranges.

Earlier than the chapter submitting, Regal accounted for 13.5% of EPRs lease. That will be plenty of lease to lose, and the market bought EPR prefer it was going to lose all of it. In actuality, EPR, in a foul state of affairs, would get well 90% of pre-bankruptcy lease, which might be a couple of 1.35% discount in EPR’s whole lease. Even that is not an enormous deal, and with extra aggressive escalators sooner or later, over the entire time period of the lease, EPR will possible accumulate extra lease than it could have if Regal had simply paid as agreed.

For earnings traders like us, this case was not a big risk to our dividend. Now that it’s behind us, we are able to sit up for the subsequent dividend hike from EPR!

As we progress by way of this century, hydrogen adoption will seemingly change into a extra widespread theme, notably given its helpful qualities in serving to decarbonize the globe’s vitality programs. There are fairly a number of industries corresponding to aviation, naval, heavy industries, high-heat manufacturing, fertilizer manufacturing, and so forth. that can seemingly stay stubborn to the waves of electrification, and that is the place hydrogen’s presence can be felt most keenly. All in all, if we’re to hit web zero emissions by 2050, it’s all however sure that we might have an ever-growing hydrogen economic system taking part in an important half in that narrative.

In case you’re intrigued by the rising scope of the broad hydrogen economic system and are in search of appropriate choices, you could contemplate trying on the Direxion Hydrogen ETF (NYSEARCA:HJEN), which is certainly one of two ETFs that traders may probably pursue.

Portfolio Development

As a part of HJEN’s preliminary screening course of, potential shares, together with ADRs (these shares have to have a minimal market cap of $100m and a 6-month common each day turnover of over $ 1 million) should be concerned in a single, or all of a number of the hydrogen-related sub-themes listed under.

Hydrogen Manufacturing & Era Hydrogen Storage & Provide Gas Cell & Battery Hydrogen Techniques & Options Membrane & Catalyst

Do notice that it is not enough to have simply tenuous exposures to those hydrogen sub-themes. Quite, HJEN’s screeners additionally search to determine if these are “pure-play” shares (hydrogen-related income ought to comprise at the least 50% of the group topline), “quasi-play” shares (hydrogen associated income publicity of 20-50%), or “marginal-play” (lower than 20% income publicity to the hydrogen theme).

Ultimately, the highest 30 pure-play shares by market cap make up HJEN’s portfolio, and if they can not discover 30, they may dip into the quasi-play pool, with choice given to bigger shares (by market cap) and people concerned within the first three hydrogen sub-themes.

Although this can be a US-based product (30% of holdings), notice that the majority of the holdings is predicated in Europe (~42% publicity), with some publicity to Asia-Pac shares as properly (24%).

HJEN versus HYDR

As famous earlier within the article, traders even have the choice of pursuing an alternate ETF that seeks to revenue from the rising profile of the worldwide hydrogen industry- The World X Hydrogen ETF (HYDR) which tracks a barely smaller portfolio of solely 26 shares.

Regardless of coming to the bourses three months after HJEN, HYDR seems to be the extra common product on this area, with an AUM of over $47m in comparison with $31m for HYDR. Buyers could have their distinctive causes for gravitating to a sure product, however after we examine the ETFs, we really feel HJEN is a extra well-rounded providing.

Firstly, on the expense profile entrance, HJEN affords an edge with an expense ratio that’s 5bps decrease. One additionally will get the additional benefit of pocketing a helpful dividend yield of 1.16%, one thing which HYDR would not supply in any respect.

Then, as each portfolios observe a comparatively small variety of shares, you are sure to search out some focus results, however but nonetheless, that impact is comparatively decrease within the case of HJEN. The highest-heavy nature is extra apparent with HYDR with the top-10 shares accounting for nearly three-fourths of the overall portfolio; with HJEN, their weight is much less pronounced at 63%.

Additionally notice that HJEN spreads its wings pretty evenly throughout shares concerned in numerous avenues. For example, HJEN isn’t overzealously wedged to producer manufacturing or digital expertise which collectively account for 88% of HYDR’s complete portfolio. Quite, the weights are well-spread out past these two sectors and in addition embrace vitality minerals and course of work.

ETF.com

From a danger angle as properly, HJEN comes throughout as much less risky, providing a month-to-month normal deviation profile that’s round 1500bps decrease than HYDR.

YCharts

We imagine that is dictated by the pockets that these two ETFs dabble with. HYDR, it seems likes to chase extra unproven, early-in-the-lifecycle names, as exemplified by a heightened publicity of 88% to small and micro-cap shares. Nonetheless, HJEN publicity to those pockets is barely round 50%, with the remainder comprising of enormous and mid-cap shares.

ETF.com

Lastly, additionally contemplate that at the moment, HJEN affords a lot superior worth relative to HYDR. The previous’s holdings are at the moment priced at a weighted common P/E of solely 12x, a 52% low cost to the corresponding a number of of HYDR.

Closing Ideas- Technical Commentary

Going purely by the charts, at this juncture, HJEN doesn’t look like probably the most opportune guess. The picture under highlights how HJEN’s relative power over HYDR has been rising over time within the form of an ascending channel. At the moment, that ratio seems to be quite elevated, buying and selling nearer to the higher boundary of the channel, and considerably increased than the mid-point of the vary. We do not essentially suppose the ratio will collapse to the mid-point any time quickly contemplating the long-term pattern, however the prospect of some mean-reversion shouldn’t be dominated out.

Stockcharts

Apart from if we swap our consideration to HJEN’s personal standalone chart, we are able to see that after an honest efficiency this month, the ETF isn’t too distant from hitting the downward-sloping resistance. We cannot rule out a breakout from this resistance however do contemplate that there have been 4 separate situations the place it has didn’t clear it. The preferable terrain to have staged a protracted place was across the $12-$12.5 ranges the place the risk-reward regarded extra enticing.

We have re-examined a few actual property funding trusts, or REITs, we reviewed a yr in the past and extra.

Particularly, we’re speaking about Rexford Industrial Realty, Inc. (NYSE:REXR). I final examined this explicit REIT again in September of 2022, when I discovered the valuation to be considerably prohibitive for the type of wonderful upside that we sometimes search for.

Additionally, the yield is not spectacular.

A 2.75% yield on this surroundings, the place I can get 3.65% from a financial savings account, not even a CD?

You will have to actually persuade me of that one, given the variance in risk-reward.

Nevertheless, REXR has grow to be convincing, which is the rationale I made a decision to improve this one to a Sturdy Purchase (My oh My).

We’re now going to share this with you and make clear why this “sharp shooter” is a STRONG BUY!

Rexford: The Fundamentals

The REIT shouldn’t be healthcare or workplace – it is industrial.

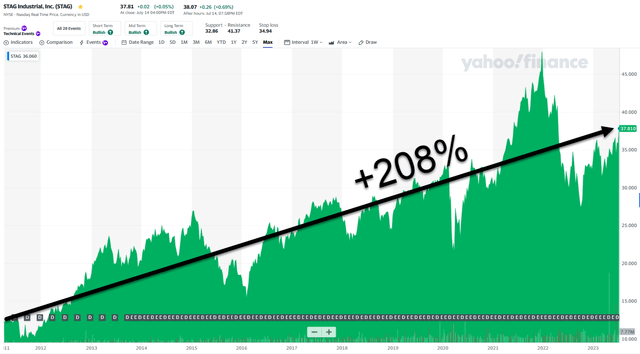

As soon as upon a time, I started investing in STAG Industrial (STAG). Here is my very first article HERE (again in 2011).

Yahoo Finance

Totally different occasions, completely different danger allocations.

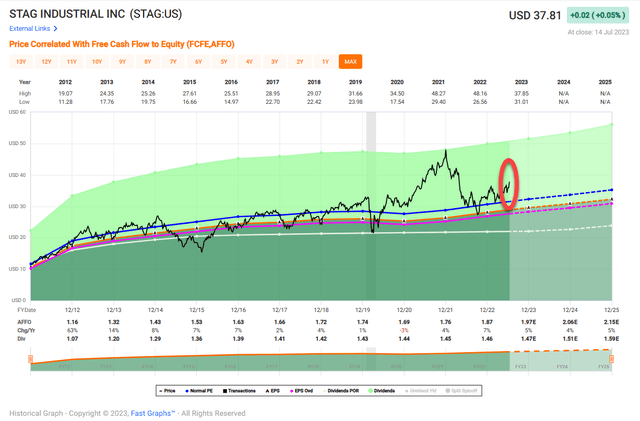

I’ve by no means offered one share of STAG…and I do not plan to, despite the fact that its valuation is not low-cost proper now.

FAST Graphs

My level being, industrial REITs on the proper value are nice investments.

As is REXR.

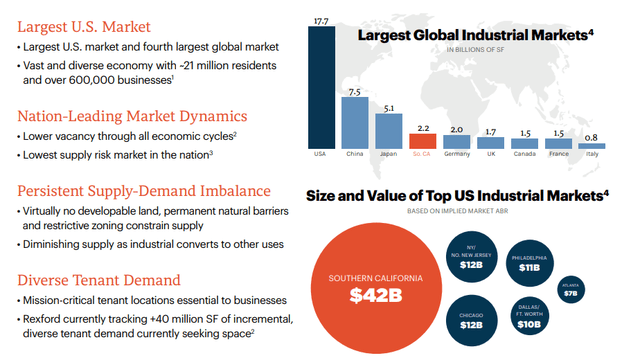

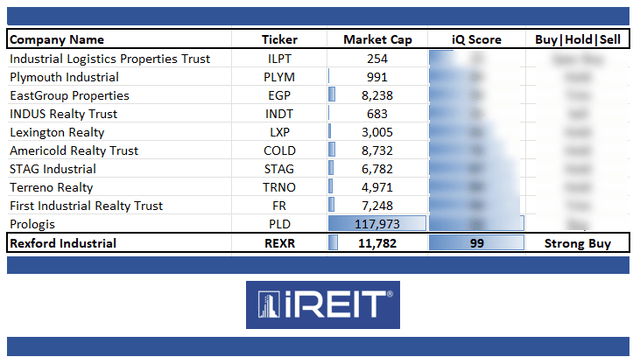

REXR is a BBB+ rated industrial REIT with a market cap of over $11B. It has over 20 years of historical past, it is a member of the S&P500 (SP500) with 44.2 M sq. toes owned.

Return for the previous 5 years is 112%, which suggests outperformance, and the corporate’s annual dividend progress over the previous 5 years is 19% – outperformance right here as effectively.

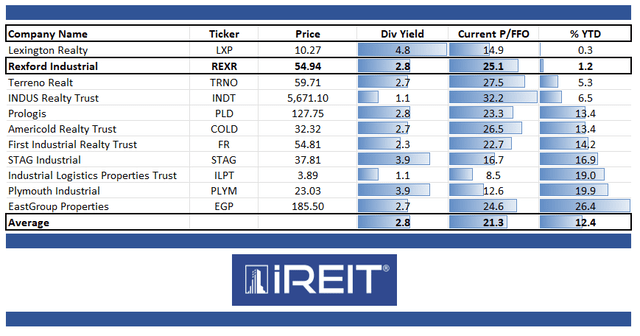

The corporate is the largest pure-play U.S.-focused Industrial REIT on the market. Others are both smaller, not pure-play, or not U.S. Competitors contains companies like STAG, Plymouth Industrial (PLYM) First industrial (FR), and EastGroup Properties (EGP).

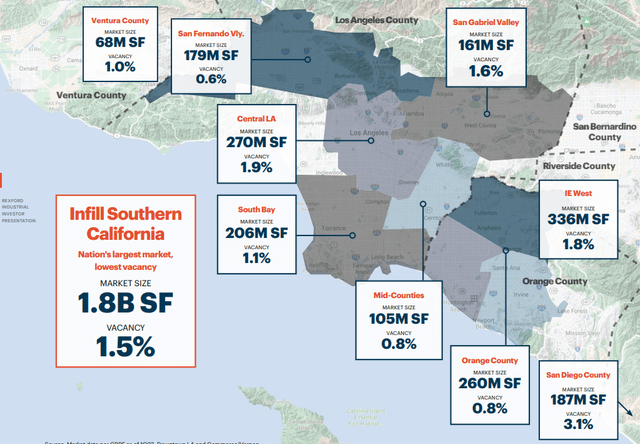

The corporate, nevertheless, is a play on a really particular geography, that may not be your cup of tea – particularly, the corporate has a 100% infill in southern California.

Nevertheless, earlier than you go unfavourable, check out what the corporate really gives when it comes to portfolio and upside – as a result of there’s extra to this story than Southern Cali – although the commercial space of Southern California does deserve highlighting.

REXR IR

We consider such part of the presentation ought to be seen with a modicum of salt, however on the identical, shouldn’t be discounted.

It is unquestionable that the historic enchantment of this space shouldn’t be the identical factor because the ahead enchantment – however as a result of REXR has such mission-critical tenant places, we do not suppose it may be equated with a number of the issues presently current within the state.

The truth that there’s an excessive shortage of land inside the Infill SoCal implies that there actually are only a few options for the companies that function there – they should flip to REXR.

We have additionally been vocal proponents, by investing in residence REITs like AvalonBay (AVB) and Essex (ESS), that issues will not be as dangerous as they appear on the West Coast.

They’re difficult, and might even be characterised as dangerous in sure areas, like San Francisco, however developments will not be as dangerous throughout your complete state, with cities like San Diego being far much less affected by the downturn.

So why REXR?

As a result of the corporate’s portfolio is discovered right here.

REXR IR

Check out a few of these emptiness charges – and the 1.5% infill SoCal emptiness.

As a result of shortage and diminishing provide, this creates a persistent supply-demand imbalance that for me is paying homage to a number of the issues happening in sure areas in Sweden.

As a result of nothing is being constructed, and there’s such a shortage, housing costs can not fall past a sure level, whatever the rate of interest.

Wolf Report noticed the identical within the GFC. Sweden was by no means as affected as a number of the different European nations precisely due to what REXR is describing right here, however for a special sector.

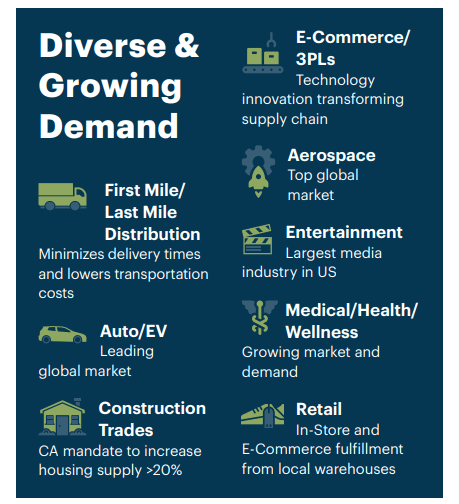

However wait, it will get even worse in SoCal – due to native housing mandates that dictate the conversion of business provide to housing, this additional reduces accessible provide. It will increase demand from development for industrial area and will increase each inhabitants and consumption from the SoCal infill portfolio the corporate has.

The corporate “performs” within the highest-demand industrial market within the nation, and already owns the mission-critical tenant places that, whereas not guaranteeing, do make pretty sure that enchantment goes to be there.

REXR IR

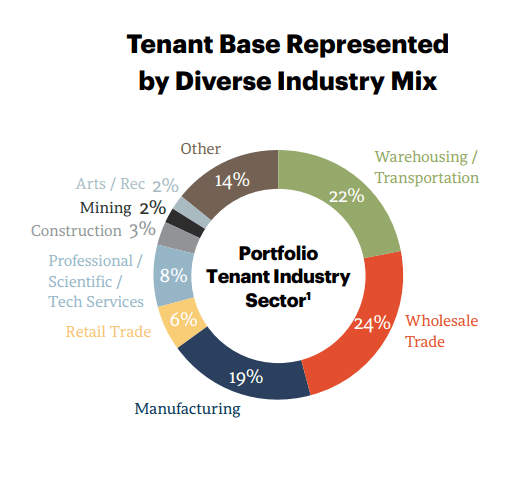

And right here is the tenant-specific diversification of that portfolio, which as you possibly can see is…fairly various. Largely wholesale and warehousing, which is a constructive.

REXR IR

It is unlikely that these are going wherever. Out of 1,600 complete tenants, the dangerous debt as % of income is zero bps. Moreover, REXR’s ABR (annualized base lease) on a per-square foot foundation is nearly twice as excessive as the remainder of the friends, and exceeds them by 75%, reflecting the energy of the precise market.

Spreads are actually wonderful when it comes to renewals, with continued excessive leasing spreads at 80% GAAP and 60% money. The corporate’s leasing expiration schedule is well-filled, although, with about 40% coming due earlier than 2026 – so we’ll wish to keep watch over renewals right here, however at a 13.5% YoY market lease progress with the basics we see, we do not see any challenge or concern right here.

Fundamentals for the corporate are past stable.

$1.85B of liquidity, BBB+, and a 3.6x web debt/Adjusted EBITDA, making it one of many least-leveraged REITs we have checked out – ever.The corporate’s complete debt as a proportion of EVs is lower than 15%.That goes some strategy to lighten the influence of that sub-3% yield.

Expirations are very stable, with a 3.6% weighted common rate of interest, and round 5.Three years common maturity. 100% of the debt is at a hard and fast fee, with no publicity to floating in any respect.

REXR is in some ways the gold commonplace for what an Industrial REIT “ought to” be.

It has a vertically built-in platform with skilled administration – proprietary analysis and origination, M&A’s, good finance/capital market processes, lease and advertising, and development to accounting and finance.

Nobody in administration has lower than 15 years of actual property expertise, and the present chairman has 49 years of RE expertise.

The weaknesses on this explicit thesis or dangers, are easy.

The unfavourable sentiment over California, the place REXR operates – there is no telling how lengthy it’ll final, or how dangerous it’ll get. This uncertainty is basically spilling over not solely to different firms however to REITs and Industrial ones as effectively.

Nevertheless, past its geographical focus, we actually cannot see any danger right here.

The corporate’s leverage is just too low to actually begin speaking about downturns as a result of elevated debt prices. The basics are past stable, and consensus projections are up considerably.

The corporate’s yield shouldn’t be solely conservative, however it’s additionally extraordinarily well-covered.

Leasing spreads are stellar.The general scenario within the firm’s working geography implies that no new vital provide is probably going.

New begins are additionally down, just because the constructing is pricey. The corporate’s dip in occupancy is definitely defined as a result of REXR themselves precipitated it – properties are being put into redevelopment.

In brief, we anticipate the corporate outperformance to proceed, and select to utterly disregard any valuation-related downturn right here, ascribing it to an irrational market.

Now allow us to current the upside for the REIT.

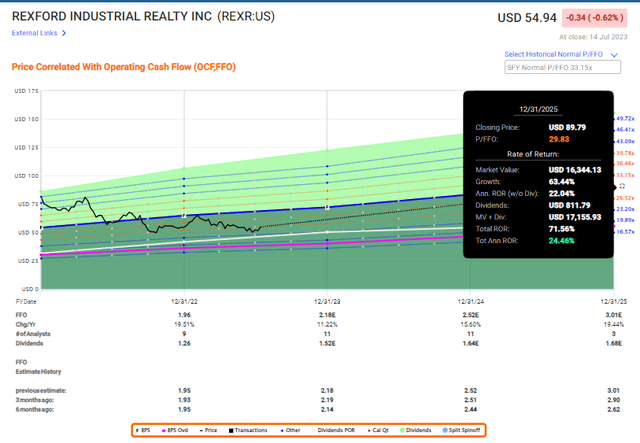

REXR Upside – The valuation

REXR doesn’t “look” low-cost.

It trades at a combined common P/FFO of 26.5x, which is greater than we normally settle for for a REIT. Nevertheless, the mix of very enticing leverage coupled with fundamentals and a really stable upside in the double digits regardless of macro, spells out why we’re constructive on REXR right here.

REXR sometimes trades at a normalized P/FFO of round 33x.

We might normalize that to round 30x on a ahead foundation at most, however even on a 30x P/FFO, the corporate’s upside right here is well-covered, as the corporate is forecasting between 10-20% FFO progress on an annual foundation for the subsequent few years.

How possible is that this?

Nicely, we stated within the earlier part a number of the qualities as to why we consider this to materialize.

However we will additionally take a look at historic developments – now we have 10+ years of them in any case.

FactSet analysts solely miss forecasts right here negatively round ~10% of the time, with the corporate beating consensus round 11% of the time – the remainder of the time, forecasts and steerage are inside the vary at a 10% margin of error.

This interprets into an above-average conviction and steerage/forecast accuracy, and for that purpose, we are saying that the corporate’s estimates may be “trusted” right here.

In spite of everything, we’re seeing all the suitable indicators from the corporate’s earnings reviews.

The upside even on a conservative forecast of beneath 30x P/FFO is important. Based mostly on high-conviction forecasts, that might end in virtually 25% RoR on an annual foundation, or over 70% RoR in a number of years.

REXR Upside (FAST Graphs)

You may even, as a matter of truth, forecast the corporate as little as 17x P/FFO, and also you’d nonetheless not lose cash(inclusive of dividends).

Your draw back on this funding is extraordinarily protected, as we see it, and there’s upside available in spades.

We would not contact the corporate a couple of yr in the past when it traded above 33-34x P/FFO. The upside at that time was so-so, and there have been much better options on the market.

Options nonetheless exist – many good ones, really – however REXR has gone from being on my radar to being on my “STRONG BUY” record right here.

S&P World analysts give the corporate a median vary of $52 to $77 presently, with a median PT of $65/share. That is down from virtually $85/share a yr in the past.

What has modified?

The notion of California, we would argue – as a result of you possibly can’t actually argue something basically having modified to the unfavourable to actually influence it as a lot.

A yr in the past, the high-point value goal (“PT”) for this firm was above $100/share. We see this as a very good instance of the short-term perspective of a few of these analysts. 10 analysts observe the corporate, 7 of that are “BUY” or equal right here.

We add our voices to this refrain, in addition to to our IREIT score, and provides the corporate a “STRONG BUY” score however going as much as $80/share for the long run.

iREIT®

Thesis

REXR is maybe one of many highest-quality industrial REITs on the market. It is fundamentals and total security are exceptional, with one of many lowest leverage out of any REIT we have researched. This goes some strategy to make up for the yield that is presently beneath a financial savings account rate of interest.

The upside right here is coupled reversal, yield, and progress. That upside is very large – and due to this, this funding is much better than any financial savings account. We give the corporate a conservative PT of $80/share, representing a conservatively-adjusted 2025E 29-30x P/FFO degree.

Based mostly on this, we contemplate this firm a formidable “STRONG BUY” right here, and like with residence REITs reminiscent of AVB or ESS, we’re selecting to take the contrarian view of California right here and go “BUY.”

Bear in mind, we’re all about:

1. Shopping for undervalued – even when that undervaluation is slight, and never mind-numbingly large – firms at a reduction, permitting them to normalize over time and harvesting capital positive factors and dividends within the meantime.

2. If the corporate goes effectively past normalization and goes into overvaluation, we harvest positive factors and rotate my place into different undervalued shares, repeating #1.

3. If the corporate would not go into overvaluation, however hovers inside a good worth, or goes again all the way down to undervaluation, we purchase extra as time permits.

4. We reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Here is our standards and the way the corporate fulfills them (italicized).

This firm is total qualitative.

This firm is basically protected/conservative & well-run.

This firm pays a well-covered dividend.

This firm is presently low-cost.

This firm has a sensible upside primarily based on earnings progress or a number of enlargement/reversion.

Based in 1963 as a comfort retailer, CVS Well being Company (NYSE:CVS) has now grow to be a well-diversified well being options firm with the intention of offering complete and inexpensive healthcare companies. It operates in three built-in segments: Well being Care Advantages, Well being Providers, and Pharmacy & Client Wellness:

The Well being Care Advantages phase provides a broad vary of consumer-directed medical health insurance merchandise and associated companies, together with Medicare Benefit and Medigap plans.

The Well being Providers phase supplies a full vary of PBM options (e.g., formulary administration, pharmacy community administration). As well as, it delivers well being care companies in its medical clinics, just about, and within the house, and provides supplier enablement options.

The Pharmacy & Client Wellness phase sells prescribed drugs in its retail pharmacies, supplies ancillary pharmacy companies, and conducts long-term care pharmacy (“LTC”) operations.

Funding Thesis

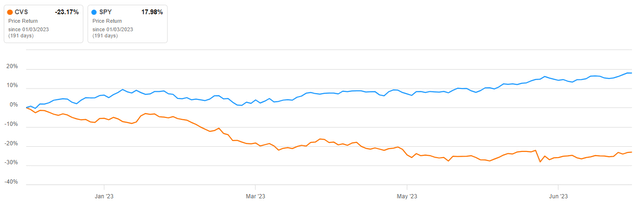

After spending years constructing a complete providing, CVS is now a stable high-quality in addition to defensive enterprise, even when the inventory efficiency appears to ignore it. For my part, there are a number of the explanation why CVS retains underperforming (YTD ~-23%) relative to the broad market.

Seekingalpha.com

First, the entrance retailer is slowly melting beneath stress from e-commerce with quite a lot of wasted area in all of the pharmacies. Nonetheless, this is a matter that CVS is effectively conscious of and it retains efficiently executing by closing “not-necessary” places. 12 months thus far, the corporate closed greater than 100 places and it stays on monitor to shut 300 shops in 2023 and the opposite 600 shops by 2024. For my part, the suitable technique can be to have in place solely the “important shops” and to go away the remainder of the job to its e-commerce arm and its supply program (i.e., CVS Carepass).

Particularly, I need to underline the significance of getting each e-commerce in addition to the “minimal/important” variety of brick-and-mortar shops, which for my part, are important to permit prospects to work together with the product bodily earlier than shopping for a must have for a lot of, to construct and keep model loyalty, and to assist prospects join with firm’s values (one thing that e-commerce can’t supply). The adoption of such a technique would instantly replicate within the firm’s margins (overhead prices down, working margins up).

Second, PBM was top-of-the-line companies on the market (a black field to many), nevertheless, it has been beneath growing stress within the final years not solely because of renewed value competitors but additionally from the legislator itself, which is targeted on including further reporting necessities and ban a number of PBM practices. Furthermore, prospects have gotten rivals, which provides further stress.

Nonetheless, due to its vertical integration with Aetna, CVS is incentivized to leverage its capabilities to cut back drug prices and therefore to vary the narrative round CVS Caremark, from being a foul neighbor to a great neighbor.

Third, the Avenue has a really cautious view on price pattern as the information from Medicare Managed Care suggests a continuation of considerable utilization with the medical profit ratio growing, in 1Q23, by 120bp YoY to 84.6%. Nonetheless, such a ratio displays extra a normalized utilization relatively than a “point-to-panic”.

Fourth, the excessive leverage and threat if downgraded to below-investment grade.

CVS is at 4.9x Web Debt/EBITDA, the optimum can be to revert to three.5x Web Debt/EBITDA

Bonds are at the moment rated Baa2 by Moody’s which is 2 notches above non-investment grade

$1.72B of debt is due in 2023

Enterprise Efficiency

The enterprise retains doing effectively, even when the underside line is beneath continued stress because it retains the downward trajectory, with the latest deterioration pushed by continued pharmacy reimbursement stress, partially offset by means of generic medication. Moreover, the early closure of the acquisitions of Signify Well being and Oak Avenue Well being ought to profit the underside line in the long run as price and income synergies are prone to kick in, however it should signify an extra headwind within the brief time period. In actual fact, as said in the course of the 1Q23 earnings name:

These acquisitions considerably advance our value-based technique by including major care, home-based care, and supplier enablement capabilities to our platform. Additionally they carry cutting-edge know-how and expertise that may speed up innovation in areas corresponding to automation, analytics, and technology-enabled data-driven product improvement. The early shut of the Signify and Oak Avenue transactions enhance our potential to speed up synergy realization.

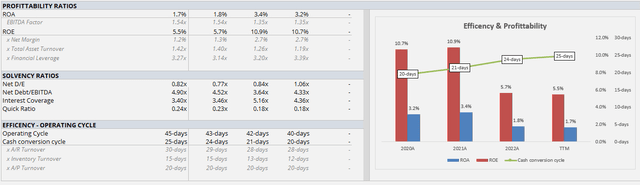

The Stability Sheet stays robust; nevertheless, we will observe a transparent deterioration within the money conversion cycle, which means that enterprise effectivity is melting. At the moment, the money conversion cycle is at 25 days, up from 21 days in 2021. The rise is pushed by decrease A/R turnover, which could point out a downturn within the economic system and a threat for an organization to expertise a rise in unhealthy debt.

Creator’s estimates

Lastly, the enterprise is very money generative, with a stable FCFF Yield of 10.8% (TTM) and a Dividend Yield of three.24% (TTM). This could profit fairness buyers as the corporate pays-down debt (i.e., de-lever)

Valuation

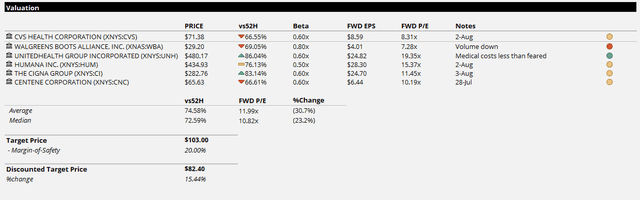

CVS trades at a reduction to its friends, regardless of a seemingly superior strategic place to many. It at the moment trades an FWD P/E of 8.31x vs a median FWD P/E of 11.99x and with the high-end being represented by UnitedHealth (UNH), which in my view deserves a premium vs friends as they’re prone to be the most effective in school because of their vertical integration of medical health insurance, information analytics, companies, PBM, and ASCs.

Creator’s estimates

Whereas the leverage at a traditionally excessive degree coupled with uncertainty across the enterprise uncertainty has put vital stress on the inventory value in latest months, in my view, most of CVS’s dangers are priced into the share value. I do imagine that the 2Q23 earnings report is probably going to supply some extra readability to buyers concerning CVS’s as-is state of affairs, sufficient to drive a multiples enlargement towards the peer common however not sufficient to drive the inventory value by means of 52W highs.

For my part, valuation is prone to stay vary certain as buyers search for additional constructive news-inflow. General, I fee CVS as a stable “Purchase”, with a good worth of $82.40/share (which includes a 20% margin of security).

Dangers

There are a major variety of headwinds with the inventory. Particularly, points by phase are:

Leverage at a traditionally excessive degree

PBM enterprise beneath growing scrutiny and value competitors

Continued stress on front-store from e-commerce

Catalysts

For my part, there aren’t any actual catalysts upcoming, which is probably going one of many primary causes for the continued sell-off. Nonetheless, the next ought to signify a possible tailwind over the subsequent 12 to 18 months:

De-leverage: bringing the Web-Debt/EBITDA under 3.5x is prone to increase the share efficiency as they’re seemingly to make use of vital FCF for repurchases.

De-pricing: CVS’s vertical integration is prone to permit it to supply higher and cheaper care.

Digital–Transformation: closing “pointless” shops and making the purchasers extra depending on its digital retailer is prone to considerably increase its bottom-line

Multiples Enlargement

Ultimate Remarks

For my part, CVS is a stable free-cash-flow generative firm, which provides a superb entry-point from the valuation viewpoint with many of the dangers being priced in.

Within the brief time period, I do not see a robust catalyst which will carry the inventory again to all-time excessive ranges, nonetheless, it is a good firm for these trying to rotate from some overbought sectors (i.e., know-how) into extra defensive ones. In actual fact, I do anticipate within the subsequent 12-18 months the well being sector to be the proper place for these looking for alpha.

Zynex (NASDAQ:ZYXI), a Nevada-based company, is the father or mother firm of varied energetic and inactive subsidiaries. The important thing energetic subsidiaries embody Zynex Medical, Inc. (ZMI) and Zynex Monitoring Options, Inc. (ZMS), each primarily based in Colorado. ZMI designs, manufactures, and markets medical units for continual and acute ache administration, as nicely as muscle rehabilitation utilizing electrical stimulation, with NexWave as their main product. ZMS, alternatively, develops non-invasive affected person monitoring units, notably the CM-1500 monitoring system and the upcoming CM-1600. In 2021, Zynex acquired Kestrel Labs, integrating its noninvasive affected person monitoring know-how into ZMS. ZMI at the moment drives many of the firm’s income.

Latest developments: Zynex has acquired FDA clearance for its non-invasive, wi-fi fluid quantity monitoring gadget, the CM-1600, and plans to hunt FDA approval for a laser-based pulse oximeter within the fourth quarter of the yr. Moreover, Zynex has efficiently priced a non-public providing of $52.5M price of 5% convertible senior notes due 2026. In a transfer that led to an roughly 8% improve in inventory worth, Zynex’s board permitted a $10M widespread inventory buyback program.

Q1 2023 Earnings

Within the first quarter of 2023, Zynex reported a 36% year-over-year improve in income, reaching $42.2 million. The corporate additionally noticed a 14% year-over-year improve in internet revenue, amounting to $1.6 million. The quarter marked the very best variety of orders within the firm’s historical past for the fourth consecutive time, with a 61% year-over-year improve. Zynex’s working capital stood at $44.1 million as of March 31, 2023, and money readily available amounted to $16.Eight million. The corporate generated $1.9 million in money from operations, a 10% improve from the primary quarter of 2022. Zynex additionally repurchased $3.Four million of its widespread inventory in the course of the quarter.

For the total yr 2023, the corporate reiterates its steerage of income between $180 – $200 million and EPS between $0.40 – $0.50. The second quarter orders elevated by 51% from 2022, and the corporate confirms its estimates for Q2 income of $43.5 – $45.5 million.

ZYXI Inventory Evaluation

Per Searching for Alpha knowledge, ZYXI demonstrates sturdy profitability and progress potential. The corporate has a formidable gross revenue margin of almost 80% and a considerable return on fairness of 24.58%. The agency additionally boasts a internet revenue margin of 10.19%, indicating environment friendly value management. Income progress is regular, with YoY progress of 23.31% and a three-year CAGR of 48.67%. This stable progress efficiency is projected to proceed, with anticipated YoY gross sales progress of over 21% till 2025.

Nonetheless, Zynex’s earnings per share [EPS] estimates reveal a possible space of concern. The YoY EPS exhibits a decline of -4.83%, however projections point out a restoration, with a 52.59% improve by 2024 and an extra 31.80% improve by 2025. Nonetheless, the agency’s valuation could also be thought of excessive, with a ahead non-GAAP P/E of 20.69 and an EV/EBITDA of 13.98.

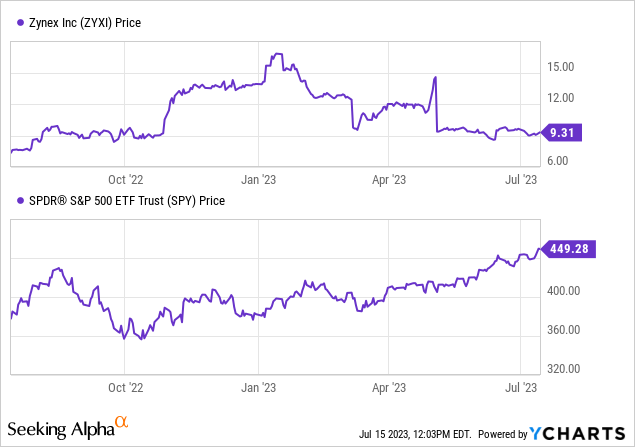

Zynex’s inventory has been underperforming within the quick time period, down 22.03% within the final three months and 44.58% up to now six months. However, it is proven optimistic momentum over the previous yr, up by 26.49%.

Knowledge by YCharts

The corporate’s capital construction is price watching with a complete debt of $24.37M and money readily available of $16.79M (values are previous to convertible notice providing), resulting in an enterprise worth of $343.36M.

Brief curiosity in Zynex is excessive at 27.75%, which might point out a possible threat of a brief squeeze, however it’s considerably offset by an Altman Z Rating of seven.88, suggesting the corporate isn’t at the moment susceptible to chapter.

Zynex Raises ~$50 Million in Convertible Notes Providing for Strategic Development

Zynex lately accomplished a non-public providing of convertible notes, elevating roughly $50.Zero million. If the preliminary purchaser workout routines its possibility to purchase further notes, this quantity might attain $57.2 million. The corporate intends to allocate round $8.5 million from this funding to repay its current time period mortgage of $16.Zero million, which is able to support in decreasing its present debt burden.

The remaining funds shall be utilized for common company functions and to help working capital. This strategic choice is important for Zynex as it should improve its money reserves. We had beforehand recognized the corporate’s modest money readily available as a priority. By repaying a portion of the time period mortgage, Zynex will lower its curiosity bills, thereby positively impacting its total monetary efficiency. Furthermore, using the proceeds for working capital will present the corporate with further assets for its day-to-day operations, an important side of its ongoing progress technique.

However, you will need to contemplate that convertible notes could contribute to potential dilution sooner or later. Upon conversion into fairness, the variety of excellent shares will improve, probably diluting the worth of current shares. Traders ought to stay aware of this chance when evaluating Zynex. General, this motion displays Zynex’s proactive strategy to managing its stability sheet, strengthening its monetary place, and supporting its progress targets.

Zynex’s Technique for Development

Zynex is at the moment pursuing the ache administration market, experiencing a considerable year-over-year income improve of 36% on this division in the course of the latest quarter. The corporate attributes this progress to the constant and worthwhile efficiency of its increasing gross sales crew.

Methods for progress embody enhancing gross sales productiveness, which they’ve already seen a rise of 24% on a per-rep annualized foundation over the primary quarter of 2022. Zynex has centered on integrating new hires extra rapidly into the group and optimizing efficiency via an applied gross sales administration construction. Regardless of going through labor market challenges, the corporate is dedicated to recruiting and retaining a high-quality gross sales and company crew.

Zynex can be increasing into further gross sales territories, aiming to achieve round 525 to 550 gross sales representatives by the tip of the yr to capitalize on the rising orders. Its potential to work with all payer varieties and insurance coverage suppliers, processing all orders it receives and dealing straight with sufferers and their insurers, is seen as a key differentiator from opponents.

Zynex anticipates one other worthwhile yr for the ache administration division and plans to offer updates on its market expansions in future calls.

My Evaluation & Advice

In conclusion, Zynex demonstrates sturdy progress and profitability, significantly in its ache administration division. The corporate’s spectacular gross revenue margin, substantial return on fairness, and constant income progress point out a stable market place and operational effectivity. The agency’s ongoing enlargement of its gross sales crew and deal with bettering gross sales productiveness additional emphasize its strong progress technique.

Nonetheless, there are some issues to contemplate concerning Zynex’s monetary place and inventory efficiency. Whereas the corporate has managed to keep away from speedy dilution, its restricted money reserves and rising debt burden increase potential vulnerability, particularly throughout an financial downturn. From my perspective, Zynex may very well be seen as a “home of playing cards” within the sense that any financial hardship might considerably impression its monetary stability. Moreover, the excessive quick curiosity in Zynex could replicate market skepticism, presumably attributable to its comparatively excessive valuation and up to date underperformance.

Regardless of these issues, Zynex’s sturdy progress technique, dedication to operational effectivity, and increasing market presence point out a promising outlook. Subsequently, as an investor, I’d advocate sustaining a ‘Maintain’ place on Zynex. Whereas legitimate issues exist concerning monetary stability and inventory efficiency, the corporate’s progress trajectory and potential profitability present a counterbalance, making it worthwhile to observe intently within the close to time period. Continuous and cautious monitoring of efficiency shall be essential for adjusting the funding technique accordingly.

The Amplify Lithium & Battery Expertise ETF (NYSEARCA:BATT) (“BATT”) is a broad option to play the lithium-ion battery, electrical automobile (“EV”), and EV metals increase. Present valuation seems to be nice and the expansion outlook is excellent.

The BATT ETF value has moved sideways the previous 5 years regardless of bettering fundamentals

As proven on the chart under the BATT ETF has typically moved sideways or barely down over the previous 5 years, regardless of the EV and battery sector booming. This has largely been attributable to damaging sentiment ensuing within the BATT ETF’s PE ratio falling considerably. We give some extra causes for this within the conclusion.

2018 world plugin electrical automobile gross sales ended at “over 2 million and market share at 2.1%”. 2023 gross sales are forecast by Development Investing to achieve 14.35m and 17.5% market share. That is roughly a 7x improve in 5 years, whereas the BATT ETF has solely moved sideways.

BATT ETF 5 yr value chart (supply) – Worth = USD 13.99

Yahoo Finance

Observe: The chart above excludes the impression of BATT paying distributions annually. You may view BATT’s previous distributions right here.

We did see an identical prevalence with the Tesla (TSLA) inventory value the place it moved sideways for 10 years earlier than surging larger. Typically a inventory or an ETF types a base for a few years, then like a sprung coil it releases larger as sentiment adjustments and the underlying fundamentals turn out to be higher understood and it will get re-rated to the next PE ratio.

Tesla long run inventory value – 10 years of base then surged larger (supply)

Yahoo Finance

A quick abstract of the BATT ETF

BATT is a broad option to play the lithium-ion battery, electrical automobile (“EV”), and EV metals increase which is anticipated this decade and subsequent.

Amplify defines their BATT fund stating:

BATT is a portfolio of firms producing vital income from the event, manufacturing and use of lithium battery know-how, together with: 1) battery storage options, 2) battery metals & supplies, and three) electrical autos. BATT seeks funding outcomes that correspond typically to the EQM Lithium & Battery Expertise Index.

BATT inventory choice methodology (supply)

BATT Truth Sheet

BATT is presently comprised of 103 world firms. The expense ratio is 0.59%pa.

Sector allocation (as of 30 June 2023) is dominated by EVs (24%) and battery know-how (battery producers) (20%). There’s additionally appreciable EV metals publicity to the miners of lithium (15%), nickel (14%), and cobalt (8%); in addition to battery parts firms (10%) and vitality storage firms (4%).

Nation allocation (as of 31 March 2023) of the BATT shares is China (29%), USA (18%), Australia (16%), South Korea (11%), Japan (6%), Switzerland (5%), Canada (4%) and so forth.

Sector and nation allocation as of 30 June, 2023 (supply)

BATT Truth sheet

High ten holdings of the BATT ETF

The highest 10 holdings proven under look to be an excellent high 10 with publicity to the main electrical automobile producers, main battery producers, and among the main EV steel miners.

BATT High ten holdings (supply)

BATT web site

International lithium-ion battery producers by market share in 2022 – CATL leads by far with 37% share (supply)

CNEVPOST

Extra particulars right here on the BATT ETF on the Amplify BATT web site.

Valuation

Valuation seems to be very engaging on a present PE of 14.34 and dividend yield of three.71%.

As of July 13, 2023 the fund is buying and selling on a reduction of 0.63% NTA low cost.

Our view is that the valuation may be very engaging given the expansion outlook for the EV and vitality storage sectors are very robust.

EV and vitality stationary storage gross sales are forecast to surge within the decade or two forward

International electrical automobile gross sales reached 10.522m in 2022 and 13% market share (supply)

EV-Volumes

International plugin electrical automobile gross sales forecast to develop exponentially this decade

Mining.com

Bloomberg forecasts speedy progress in world vitality stationary storage (“ESS”) and a doubling in 2023 (supply) (Jan. 2023)

BloombergNEF

Photo voltaic & wind manufacturing wants to extend by 3x/yr, battery manufacturing by 29x/yr, BEV manufacturing by 11x/yr for a 100% renewable vitality world (supply)

Tesla 2023 shareholder assembly

Tesla Grasp Plan Three estimates that 240 TWh of vitality storage is required to maneuver to a 100% renewable vitality world (supply)

Tesla

Dangers

An EV gross sales slowdown and fewer demand for batteries and EV battery metals.

Battery metals (nickel, lithium, cobalt) costs falling might negatively impression the sector of the fund invested into EV steel mining shares.

Extra competitors, provide chain dangers, know-how change.

ETF dangers – Amplify administration of the fund. The ETF might commerce under its web tangible property (“NTA”) worth.

Sovereign danger – Usually low for the BATT fund. USA, Australia, South Korea, Canada, Japan is low danger. Average danger with China publicity. Additionally among the EV steel miners have ‘mines’ in larger danger nations.

Inventory market dangers – Market sentiment. Liquidity seems to be nice. Foreign money dangers – BATT is priced in USD nonetheless solely 20% of the ETF is in U.S shares. This may imply that non-USA shares can under-perform in USD phrases when the USD is rising and vice versa.

Additional studying

A quote from the BATT ETF commentary 31 March 2023 (supply)

BATT ETF market commentary

Conclusion

The BATT ETF inventory value has performed poorly the previous few years on account of forex impacts because the USD rose (many shares are in non-USD currencies), BATT holding some China shares, the 2022 value falls throughout the sectors (EVs, battery OEMs & EV steel miners), and the powerful fairness market circumstances together with damaging fund flows the previous 1 yr (minus US$12.33m). In consequence the fund’s PE ratio has dropped considerably, particularly prior to now yr (see under).

In the meantime gross sales and the expansion outlook for EVs, lithium-ion batteries, and EV metals continues to be extraordinarily constructive. Tesla 2023 Grasp Plan and 2023 Shareholder Assembly highlighted the huge forecast improve in demand for lithium-ion batteries (240TWh, or a 29x improve in yearly manufacturing wanted) and electrical vehicles (11x improve in yearly manufacturing wanted) to maneuver to a totally sustainable renewable vitality world.

BATT’s high holdings look spot on with the highest two EV producers (Tesla & BYD [HK:1211](OTCPK:BYDDY) (OTCPK:BYDDF)), the highest two battery producers (CATL [SHE:300750] & LG Power Options [KRX:373220] (beforehand LG Chem)), and two high tier EV metals firms (Albemarle (ALB) and Glencore [LON:GLEN](OTCPK:GLNCY) (OTC:GLNCF)).

Valuation seems to be very engaging on a present PE of 14.34 and dividend yield of three.71%, particularly given the large progress outlook for the EV and vitality stationary storage (“ESS”) associated sectors. By comparability in Might 2022 the BATT ETF PE ratio was 19.51 and the yield 3.18%.

Dangers revolve largely across the sector performing poorly on account of poor EV gross sales and therefore much less demand for EVs, batteries and EV metals. Some China firms publicity provides danger. Please learn the dangers part.

We view BATT as a robust purchase, appropriate for a 5 yr plus time-frame, particularly if you’re constructive on the outlook for EV and ESS progress this decade.

As standard all feedback are welcome.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.

Shares of Chinese language cybersecurity corporations had been sharply greater on Friday, boosted by Beijing’s newest artificial-intelligence laws that emphasised cybersecurity and information security.

Information safety options supplier Zhongfu Info Inc. 300659, +19.98% jumped 20%, community safety firm Shenzhen GuoHua Community Safety Tech Co. 000004, +10.02% surged 10% and Beijing Bohui Science & Know-how Co. 688004, +8.12% was up 12%.

The rally got here after China unveiled draft measures on Thursday to manage the rising generative AI trade. The principles, co-published by a number of high authorities businesses together with Beijing’s web regulator and the nation’s high financial planner, pressured the significance of community safety and information regulation because the nascent trade develops and grows.

Analysts at AVIC Securities mentioned that the brand new guidelines may enhance demand for information safety options from AI expertise corporations. “This might result in new progress alternatives for the cybersecurity market normally,” the analysts mentioned.

I’ve a optimistic outlook on ThredUp Inc. (NASDAQ:TDUP) as a result of I consider the corporate has ample alternatives for development and possesses a scalable enterprise mannequin that gives aggressive benefits and the potential for sustained high-profit margins in the long term. The US softlines resale market will proceed to develop at a excessive double-digit tempo, with elements like inflation and a socially aware Gen Z anticipated to drive demand. Furthermore, the acquisition of Remix has expanded TDUP’s complete addressable market (TAM) and the corporate is well-positioned to seize market share because the resale market expands. I view the inventory as a purchase and have an end-of-year value goal of $3.5 on the inventory.

Rising resale market amidst a weaking economic system

TDUP operates in a comparatively small trade, however there’s a lengthy runway for trade development, significantly within the resale sector, which I consider would be the subsequent disruptive power in retail, following e-commerce and off-price retail. This trade aligns with three key macro themes: sustainability, worth, and the shift to e-commerce. TDUP expects the US softlines resale market to develop at a CAGR of roughly 30%, reaching $70 billion by 2027, providing upside potential to the corporate’s development projections. With the acquisition of Remix, the corporate’s TAM has expanded additional.

Furthermore, elevated stress on shoppers on account of inflation and a much less promotional retail atmosphere in 2023 could strengthen ThredUp’s enchantment towards value-oriented shoppers, for my part. In March, shopper sentiment fell for the primary time in 4 months. Although stock ranges stay elevated, as manufacturers work to clear ranges and promotions gradual, ThredUp is properly positioned to seize share from price-sensitive shoppers because the resale market grows. Remix, its European enterprise, could get a lift from the weakening economic system within the area.

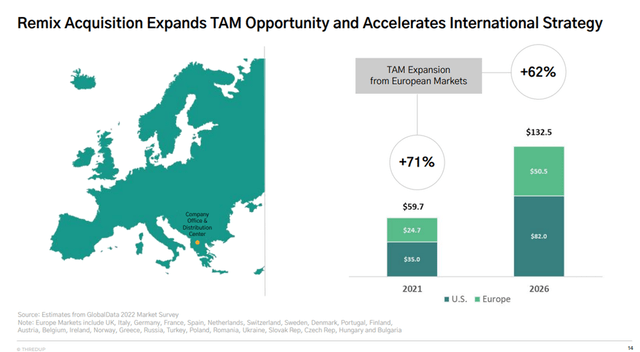

Remix Provides a Gateway to Europe

ThredUp’s enlargement into Europe via the acquisition of Remix in 2021 boosted its complete addressable market, offering entry to the $24.7 billion European secondhand and resale market, which GlobalData suggests might attain $50.5 billion by 2026. Although resale has a higher maintain within the US as we speak, $35 billion vs. Europe’s $24.7 billion, each markets are estimated to greater than double as customers worldwide more and more search reasonably priced and sustainable choices. In 2020, Remix generated $33.9 million in income, and this may occasionally develop as resale beneficial properties recognition in Europe. Leveraging ThredUp’s current advertising and marketing, infrastructure, logistics and knowledge science, coupled with shifting Remix to a consignment mannequin that mirrors the US, could enhance its gross margin, which has been dilutive because the acquisition.

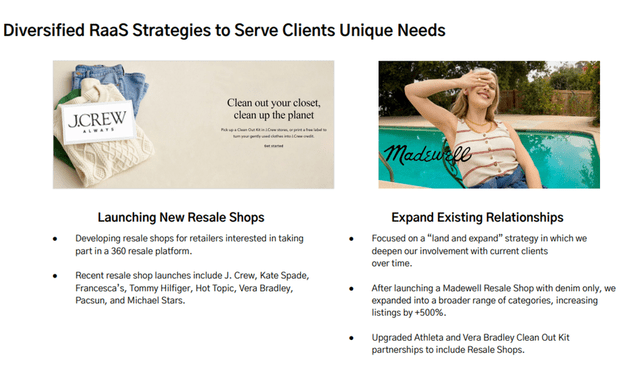

Bringing resale to model names via its Retail-as-a-Service Technique (RaaS) providing offers one other income stream to stretch ThredUp’s attain, improve product availability on its platform and enhance buyer choices. ThredUp had 42 manufacturers on its RaaS platform by the tip of 2022, after reaching 28 in 2021, together with Walmart, Adidas and Reformation. In 1Q, it launched with Kate Spade and H&M and in 2022, it expanded its Madewell resale store into 15 classes outdoors of denim, which noticed listings develop by greater than 500%. Manufacturers can distribute ThredUp’s cleanout kits and permit sellers to earn credit score on the clothes line or use ThredUp’s white-label resale retailers, a extra complete strategy the place the corporate handles clothes consumption, processing and achievement for a model’s personal online-resale platform.

Widening ThredUp’s RaaS consumer base, coupled with remodeling current partnerships from cleanout applications to branded on-line resale retailers, can enhance consignment gross sales in the long run as manufacturers change their RaaS enterprise to a consignment mannequin. ThredUp’s European and RaaS companies at the moment fall beneath product income however will quickly shift towards the consignment mannequin, which can enhance such gross sales development by double digits and support margin. As extra shoppers add resale retailers to their e-commerce websites, ThredUp can even obtain a proportion of these gross sales, vs. simply receiving a one-time integration charge, service expenses and usage-based pricing from manufacturers that solely have cleanout applications.

Firm Presentation

Gen Z to Drive Demand in Resale Market

As youthful generations (Gen Y and Z) change into a bigger proportion of US shoppers, there is a chance for secondhand-apparel retailers to achieve a higher market share. These youthful demographics are likely to prioritize environmental consciousness, resulting in elevated adoption of buying used merchandise. In accordance with a GlobalData survey, 53% of millennials and Gen Z plan to spend extra on secondhand purchases within the subsequent 5 years. Millennials, who surpassed child boomers in 2020 to change into the most important grownup group in America, have substantial spending energy exceeding $600 billion, as reported by Accenture and BLS. Gen Z, comprising 20% of the US inhabitants and influencing $600 billion in household spending, is estimated to have shopping for energy of $143 billion, in accordance with Barkley.

Monetary Outlook

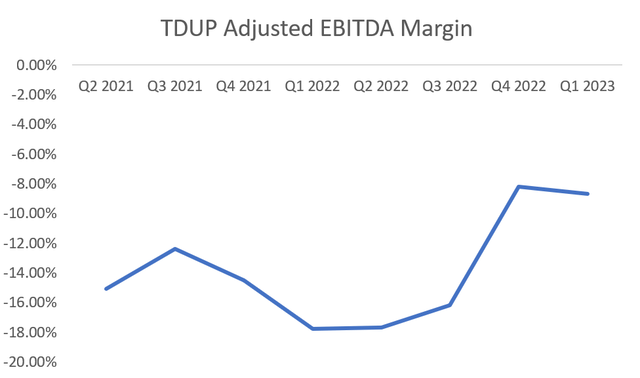

Like different newly public e-commerce firms which might be at the moment not worthwhile, an important query is when TDUP will obtain profitability. The reply to this query primarily depends upon variety of orders, per-order profitability and the mounted prices related to the enterprise. TDUP anticipates important enhancements in per-order profitability, primarily pushed by automation, and expects sturdy order development to proceed. Consequently, the administration sees the potential of attaining adjusted EBITDA profitability by FY24E, with an optimistic situation suggesting breakeven within the second half of 2023. In the long run, the corporate goals for an adjusted EBITDA margin of 20-25%.

I consider ThredUp’s gross sales could speed up in 2Q after lingering 1Q promotional challenges, and there is potential to succeed in breakeven EBITDA in 3Q forward of its 2H objective, given its skill to take share in a resale promote it tasks can develop a lot quicker vs. broader attire. It is clean-out equipment charge, new distribution facilities, development in Resale as a Service, and shopper thrift could spur high-single-digit gross sales development in 2023.

Path to Profitability

Not like many widespread shopper web firms which have skilled a decline in development and shrinking revenue margins on account of rising prices of manufacturing, labor, and different inputs, TDUP has constantly improved its unit economics lately. This has resulted in a record-high gross margin of 74.5% in the newest quarter within the US market. Though the corporate has been shifting its focus in the direction of Europe, which has briefly affected the visibility of its cost-saving efforts, administration is assured that these measures will drive profitability as purchaser and income development recuperate, particularly within the US. Regardless of the progress made thus far in bettering the associated fee construction, I consider there may be nonetheless room for additional gross margin enlargement, significantly as extra of the enterprise transitions to consignment, and the European market expands.

Furthermore, ThredUp has been testing charging a regular $14.99 clean-out charge, which can assist fight rising processing prices for used clothes. Although ThredUp has a historical past of experimenting with these charges, if it sticks with this degree throughout its platform, the corporate might see optimistic EBITDA in 2H or early subsequent 12 months. Long term, the extra charge, which flows straight to the underside line, might make it simpler for ThredUp to succeed in its targets for 75-78% gross margin and 20-25% adjusted EBITDA margin. In 2021, ThredUp processed greater than 2 million Clear Out Kits and facilitated the resale of greater than 1.7 million objects via their resale-as-a-service mannequin thus far. This, together with decrease headcount, R&D bills, and capital spending, is aiding free money stream development.

Firm Filings

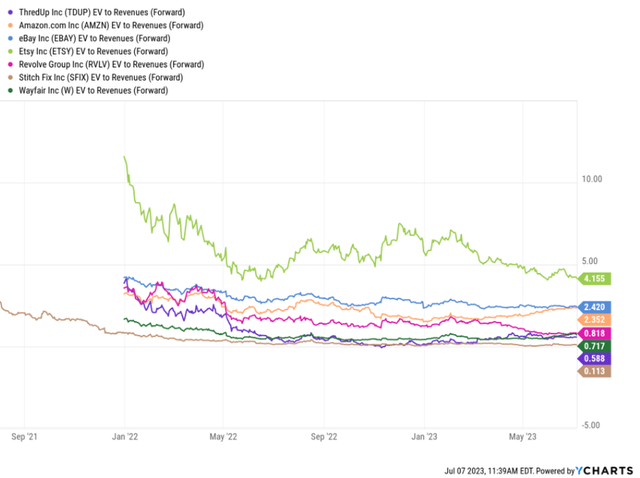

Valuation

For comparable firm relative valuation functions, I separate e-commerce marketplaces and attire & retail e-commerce into two distinct buckets. The marketplaces are usually buying and selling at a big premium to retail e-comm on each ahead income and GP. A few of that is structural, given the asset-light, low/no stock threat, and usually extra engaging margin profiles (as a % of income). There’s additionally a element that displays class publicity – extra discretionary areas corresponding to attire have been significantly laborious hit from a inventory efficiency and a number of perspective, whereas marketplaces which have enough scale and/or serve a wider vary of classes have held up higher. Additionally embedded in these rev/GP multiples is a few consideration for EBITDA/FCF profitability or the dearth thereof, as most traders have been more and more migrating in the direction of extra conventional valuation metrics corresponding to FCF yield or EBITDA multiples. Within the absence of working or money stream profitability, a decrease income/GP a number of might be warranted, for my part.

As a result of TDUP is just not but worthwhile, valuation is much less straight-forward than it’s for a lot of different firms (i.e., conventional P/E and EV/EBITDA metrics aren’t relevant), thus, I believe it’s most acceptable to worth TDUP utilizing an EV/Gross sales a number of. My end-of-year value goal of $3.5 relies on 1x FY24E revenue-roughly in keeping with market friends.

In search of Alpha

Dangers to Score

There are a number of dangers related to investing in TDUP. Firstly, the corporate is at the moment unprofitable and desires to extend its revenue margin with the intention to attain breakeven or change into worthwhile. The administration has laid out a path to profitability in accordance with which the corporate is forecasted to attain EBITDA profitability by FY24. Nevertheless, any delays within the firm’s achievement of profitability would put stress on the inventory to the draw back. Furthermore, the corporate does face competitors from different sellers, which might have an effect on development. Whereas TDUP is at the moment the one managed market for mass attire, there are rivals working a peer-to-peer mannequin that might current aggressive challenges for TDUP. This might negatively affect the corporate’s development if sellers and patrons select these different platforms as an alternative.

Conclusion

I consider TDUP is well-positioned to keep up its management within the on-line resale marketplace for attire on account of its sturdy person base and a user-friendly expertise with minimal obstacles. The acquisition of Remix has expanded TDUP’s TAM, and the corporate is well-positioned to seize market share because the resale market expands. I view the inventory as a purchase and have an end-of-year value goal of $3.5 on the inventory.

SYDNEY–The Reserve Financial institution of New Zealand left rates of interest unchanged at its coverage assembly on Wednesday however warned that coverage settings might want to stay tight for a while but.

The official money charge was left on maintain at 5.5%, its highest stage in 14 years, as extensively anticipated. The RBNZ had hiked at every of the 12 prior coverage conferences since October 2021.

“The committee agreed that rates of interest might want to stay at a restrictive stage for the foreseeable future, to make sure shopper value inflation returns to the 1 to three% goal vary whereas supporting most sustainable employment,” the RBNZ stated in a press release.

The choice to carry rates of interest regular got here after information not too long ago confirmed that New Zealand’s financial system was in recession as excessive rates of interest and storm injury throughout the nation’s north put the brakes on exercise.

The financial system contracted 0.1% throughout the three months by March, following a 0.7% contraction within the prior quarter, in keeping with Stats NZ. That consequence was weaker than anticipated by the central financial institution, which had projected 0.3% progress within the March quarter.

The RBNZ has been among the many most hawkish of world central banks, at occasions choosing outsize rate of interest will increase whilst counterparts elsewhere on the earth took a timeout to digest the influence of earlier tightening on their financial system.

“The RBNZ is seen as a take a look at case for different central banks globally which have adopted its lead in tightening financial coverage,” stated Tony Sycamore, market analyst at IG Australia.

The pause by the RBNZ was partially on account of storm injury earlier within the yr. Cyclone Gabrielle introduced widespread flooding and killed 11 individuals in February, decreasing spending and home-building exercise within the quarter.

A cyclone restoration plan was the centerpiece of the federal government’s annual funds final month, with economists warning that the additional spending might stimulate the financial system and add to inflation.

The funds included 1.1 billion New Zealand {dollars} (US$687 million) to fund the restoration from the storm, with the entire price of the catastrophe estimated to be as excessive as NZ$14.5 billion.

New Zealand can be experiencing a surge in migration and tourism after its borders have been reopened, which is prone to help the financial system this yr.