Iryna Imago/iStock by way of Getty Pictures

Thesis

I’ve a optimistic outlook on ThredUp Inc. (NASDAQ:TDUP) as a result of I consider the corporate has ample alternatives for development and possesses a scalable enterprise mannequin that gives aggressive benefits and the potential for sustained high-profit margins in the long term. The US softlines resale market will proceed to develop at a excessive double-digit tempo, with elements like inflation and a socially aware Gen Z anticipated to drive demand. Furthermore, the acquisition of Remix has expanded TDUP’s complete addressable market (TAM) and the corporate is well-positioned to seize market share because the resale market expands. I view the inventory as a purchase and have an end-of-year value goal of $3.5 on the inventory.

Rising resale market amidst a weaking economic system

TDUP operates in a comparatively small trade, however there’s a lengthy runway for trade development, significantly within the resale sector, which I consider would be the subsequent disruptive power in retail, following e-commerce and off-price retail. This trade aligns with three key macro themes: sustainability, worth, and the shift to e-commerce. TDUP expects the US softlines resale market to develop at a CAGR of roughly 30%, reaching $70 billion by 2027, providing upside potential to the corporate’s development projections. With the acquisition of Remix, the corporate’s TAM has expanded additional.

Furthermore, elevated stress on shoppers on account of inflation and a much less promotional retail atmosphere in 2023 could strengthen ThredUp’s enchantment towards value-oriented shoppers, for my part. In March, shopper sentiment fell for the primary time in 4 months. Although stock ranges stay elevated, as manufacturers work to clear ranges and promotions gradual, ThredUp is properly positioned to seize share from price-sensitive shoppers because the resale market grows. Remix, its European enterprise, could get a lift from the weakening economic system within the area.

Remix Provides a Gateway to Europe

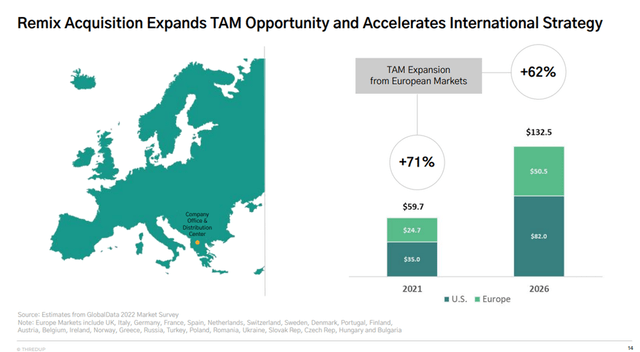

ThredUp’s enlargement into Europe via the acquisition of Remix in 2021 boosted its complete addressable market, offering entry to the $24.7 billion European secondhand and resale market, which GlobalData suggests might attain $50.5 billion by 2026. Although resale has a higher maintain within the US as we speak, $35 billion vs. Europe’s $24.7 billion, each markets are estimated to greater than double as customers worldwide more and more search reasonably priced and sustainable choices. In 2020, Remix generated $33.9 million in income, and this may occasionally develop as resale beneficial properties recognition in Europe. Leveraging ThredUp’s current advertising and marketing, infrastructure, logistics and knowledge science, coupled with shifting Remix to a consignment mannequin that mirrors the US, could enhance its gross margin, which has been dilutive because the acquisition.

Firm Presentation

Retail-as-a-Service Technique Brings Contemporary Gross sales

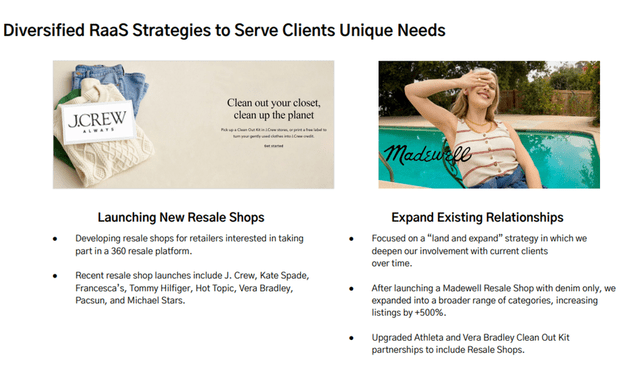

Bringing resale to model names via its Retail-as-a-Service Technique (RaaS) providing offers one other income stream to stretch ThredUp’s attain, improve product availability on its platform and enhance buyer choices. ThredUp had 42 manufacturers on its RaaS platform by the tip of 2022, after reaching 28 in 2021, together with Walmart, Adidas and Reformation. In 1Q, it launched with Kate Spade and H&M and in 2022, it expanded its Madewell resale store into 15 classes outdoors of denim, which noticed listings develop by greater than 500%. Manufacturers can distribute ThredUp’s cleanout kits and permit sellers to earn credit score on the clothes line or use ThredUp’s white-label resale retailers, a extra complete strategy the place the corporate handles clothes consumption, processing and achievement for a model’s personal online-resale platform.

Widening ThredUp’s RaaS consumer base, coupled with remodeling current partnerships from cleanout applications to branded on-line resale retailers, can enhance consignment gross sales in the long run as manufacturers change their RaaS enterprise to a consignment mannequin. ThredUp’s European and RaaS companies at the moment fall beneath product income however will quickly shift towards the consignment mannequin, which can enhance such gross sales development by double digits and support margin. As extra shoppers add resale retailers to their e-commerce websites, ThredUp can even obtain a proportion of these gross sales, vs. simply receiving a one-time integration charge, service expenses and usage-based pricing from manufacturers that solely have cleanout applications.

Firm Presentation

Gen Z to Drive Demand in Resale Market

As youthful generations (Gen Y and Z) change into a bigger proportion of US shoppers, there is a chance for secondhand-apparel retailers to achieve a higher market share. These youthful demographics are likely to prioritize environmental consciousness, resulting in elevated adoption of buying used merchandise. In accordance with a GlobalData survey, 53% of millennials and Gen Z plan to spend extra on secondhand purchases within the subsequent 5 years. Millennials, who surpassed child boomers in 2020 to change into the most important grownup group in America, have substantial spending energy exceeding $600 billion, as reported by Accenture and BLS. Gen Z, comprising 20% of the US inhabitants and influencing $600 billion in household spending, is estimated to have shopping for energy of $143 billion, in accordance with Barkley.

Monetary Outlook

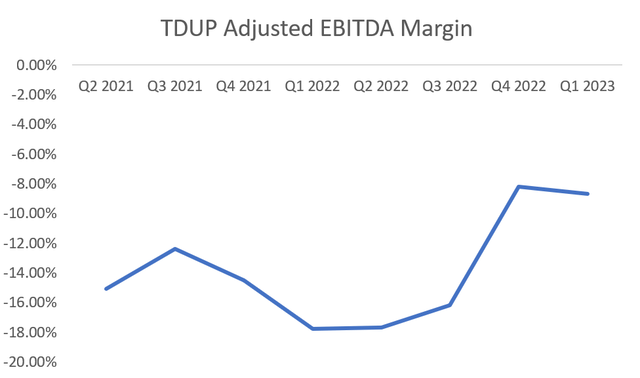

Like different newly public e-commerce firms which might be at the moment not worthwhile, an important query is when TDUP will obtain profitability. The reply to this query primarily depends upon variety of orders, per-order profitability and the mounted prices related to the enterprise. TDUP anticipates important enhancements in per-order profitability, primarily pushed by automation, and expects sturdy order development to proceed. Consequently, the administration sees the potential of attaining adjusted EBITDA profitability by FY24E, with an optimistic situation suggesting breakeven within the second half of 2023. In the long run, the corporate goals for an adjusted EBITDA margin of 20-25%.

I consider ThredUp’s gross sales could speed up in 2Q after lingering 1Q promotional challenges, and there is potential to succeed in breakeven EBITDA in 3Q forward of its 2H objective, given its skill to take share in a resale promote it tasks can develop a lot quicker vs. broader attire. It is clean-out equipment charge, new distribution facilities, development in Resale as a Service, and shopper thrift could spur high-single-digit gross sales development in 2023.

Path to Profitability

Not like many widespread shopper web firms which have skilled a decline in development and shrinking revenue margins on account of rising prices of manufacturing, labor, and different inputs, TDUP has constantly improved its unit economics lately. This has resulted in a record-high gross margin of 74.5% in the newest quarter within the US market. Though the corporate has been shifting its focus in the direction of Europe, which has briefly affected the visibility of its cost-saving efforts, administration is assured that these measures will drive profitability as purchaser and income development recuperate, particularly within the US. Regardless of the progress made thus far in bettering the associated fee construction, I consider there may be nonetheless room for additional gross margin enlargement, significantly as extra of the enterprise transitions to consignment, and the European market expands.

Furthermore, ThredUp has been testing charging a regular $14.99 clean-out charge, which can assist fight rising processing prices for used clothes. Although ThredUp has a historical past of experimenting with these charges, if it sticks with this degree throughout its platform, the corporate might see optimistic EBITDA in 2H or early subsequent 12 months. Long term, the extra charge, which flows straight to the underside line, might make it simpler for ThredUp to succeed in its targets for 75-78% gross margin and 20-25% adjusted EBITDA margin. In 2021, ThredUp processed greater than 2 million Clear Out Kits and facilitated the resale of greater than 1.7 million objects via their resale-as-a-service mannequin thus far. This, together with decrease headcount, R&D bills, and capital spending, is aiding free money stream development.

Firm Filings

Valuation

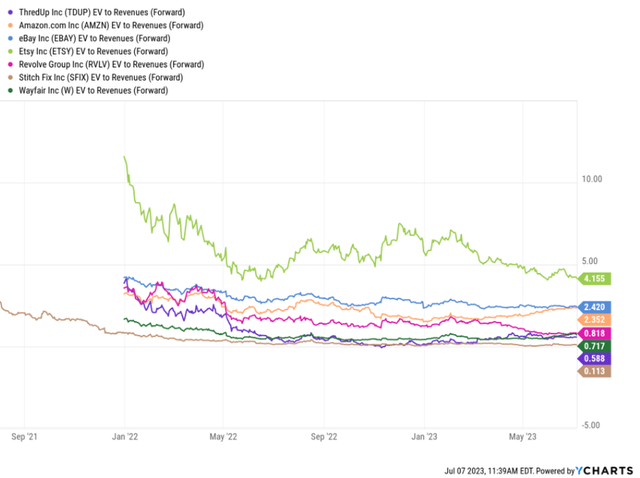

For comparable firm relative valuation functions, I separate e-commerce marketplaces and attire & retail e-commerce into two distinct buckets. The marketplaces are usually buying and selling at a big premium to retail e-comm on each ahead income and GP. A few of that is structural, given the asset-light, low/no stock threat, and usually extra engaging margin profiles (as a % of income). There’s additionally a element that displays class publicity – extra discretionary areas corresponding to attire have been significantly laborious hit from a inventory efficiency and a number of perspective, whereas marketplaces which have enough scale and/or serve a wider vary of classes have held up higher. Additionally embedded in these rev/GP multiples is a few consideration for EBITDA/FCF profitability or the dearth thereof, as most traders have been more and more migrating in the direction of extra conventional valuation metrics corresponding to FCF yield or EBITDA multiples. Within the absence of working or money stream profitability, a decrease income/GP a number of might be warranted, for my part.

As a result of TDUP is just not but worthwhile, valuation is much less straight-forward than it’s for a lot of different firms (i.e., conventional P/E and EV/EBITDA metrics aren’t relevant), thus, I believe it’s most acceptable to worth TDUP utilizing an EV/Gross sales a number of. My end-of-year value goal of $3.5 relies on 1x FY24E revenue-roughly in keeping with market friends.

In search of Alpha

Dangers to Score

There are a number of dangers related to investing in TDUP. Firstly, the corporate is at the moment unprofitable and desires to extend its revenue margin with the intention to attain breakeven or change into worthwhile. The administration has laid out a path to profitability in accordance with which the corporate is forecasted to attain EBITDA profitability by FY24. Nevertheless, any delays within the firm’s achievement of profitability would put stress on the inventory to the draw back. Furthermore, the corporate does face competitors from different sellers, which might have an effect on development. Whereas TDUP is at the moment the one managed market for mass attire, there are rivals working a peer-to-peer mannequin that might current aggressive challenges for TDUP. This might negatively affect the corporate’s development if sellers and patrons select these different platforms as an alternative.

Conclusion

I consider TDUP is well-positioned to keep up its management within the on-line resale marketplace for attire on account of its sturdy person base and a user-friendly expertise with minimal obstacles. The acquisition of Remix has expanded TDUP’s TAM, and the corporate is well-positioned to seize market share because the resale market expands. I view the inventory as a purchase and have an end-of-year value goal of $3.5 on the inventory.