josefkubes/iStock Editorial by way of Getty Photographs

Having survived a difficult setting final 12 months amid COVID-driven provide constraints and outsized uncooked materials inflation pressures, issues are lastly on course for Japanese auto producer Nissan Motor (OTCPK:NSANY). In its most up-to-date quarter, Nissan posted sharply larger working earnings and earnings development YoY, helped by easing constraints and continued yen depreciation. Anticipate extra of the identical by way of this fiscal 12 months as the provision/demand dynamic continues to revert, helped by resilient US auto demand and a continued manufacturing restoration.

Additionally serving to the chance/reward are the continuing United Auto Employees (UAW) strikes within the US, which threatens to skew competitiveness in its favor (together with different Asian producers like Hyundai Motor (OTCPK:HYMTF)) over the long term. In the meantime, the relative lack of China earnings contribution (vs. different producers by way of their equity-method JVs) implies restricted contagion threat ought to the financial system deteriorate.

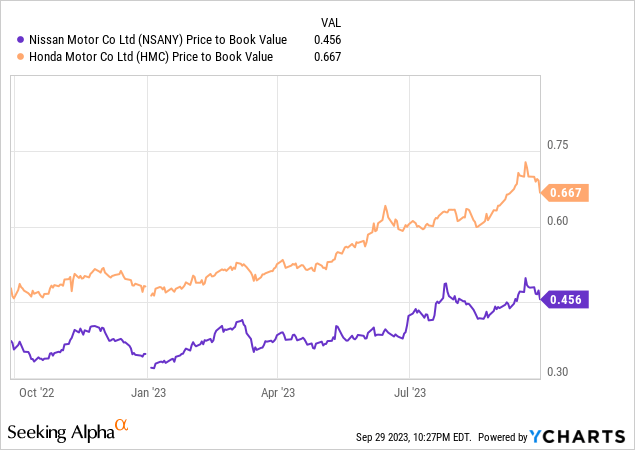

To be clear, among the positives are already within the worth – Nissan inventory is having one in every of its finest years on report at +60% year-to-date, effectively forward of the TOPIX index. But, Nissan nonetheless trades at a steep ~50% e book worth low cost (vs. key peer Honda’s ~30% low cost to e book) regardless of retaining robust money era capability. The mid-term plan later this 12 months presents a possible upside catalyst, together with upsized capital returns (dividend or buybacks) amid reform pressures from the Tokyo Inventory Trade.

Knowledge by YCharts

UAW Strikes Increase Close to-Time period Earnings Prospects

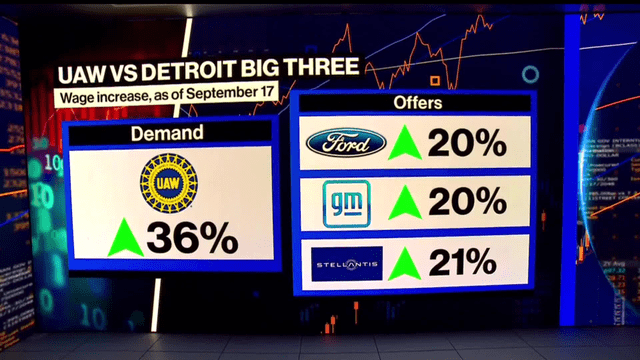

Coming off a strong begin to the fiscal 12 months, Nissan seems to be set for an additional earnings increase from the escalating UAW union dispute, masking staff of the Detroit-Three US automakers (Ford (F), Normal Motors (GM), and Stellantis (STLA)). Because the strike motion commenced earlier this month, the union has rejected a 21% pay hike from STLA (deemed a ‘no-go’ by President Shawn Fain) and appears set to rebuff the same 20% provide from Ford. Given how far aside either side are proper now, count on a drawn-out strike, maybe even longer than the final 40-day strike at GM in 2019.

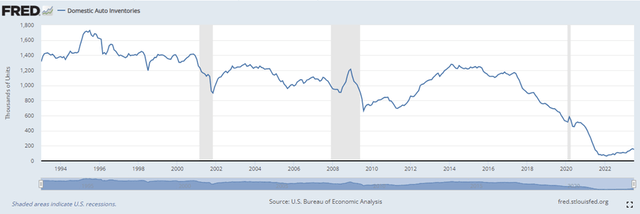

Whereas the preliminary UAW strike gained’t hit automobile output significantly exhausting, additional escalation will imply as a lot as 55-65okay of misplaced manufacturing per automaker. So, relying on the size and severity of those strikes, provide may effectively tighten by >500okay automobiles in a worst-case state of affairs (not together with post-strike disruptions). Given home auto inventories are already on the decline and vendor inventories (~2m in September) are additionally set to sluggish, this bodes effectively for firmer US auto pricing going ahead.

St Louis Fed

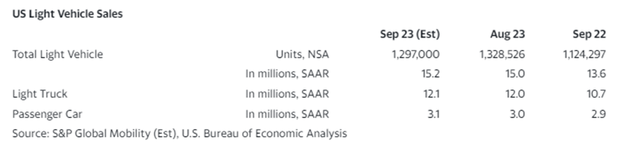

As for the demand facet, the surge of latest mild automobile gross sales within the US (+17% YoY to 1.3m items; one other ~1.3m projected for September) signifies a robust financial system regardless of the Fed’s prolonged financial tightening. Whereas improved new automobile provide post-COVID has helped to soak up some ‘pent-up’ demand, the UAW strikes ought to once more tighten the supply-demand steadiness by way of year-end. For the likes of Nissan, longer UAW strikes current a chance to seize share and increase its export earnings this fiscal 12 months. Even when a slowing financial backdrop materializes (because of the lagged affect of upper rates of interest), demand for lower-priced automobiles will acquire possible momentum on the expense of higher-end choices, benefiting Nissan’s concentrate on worth.

S&P

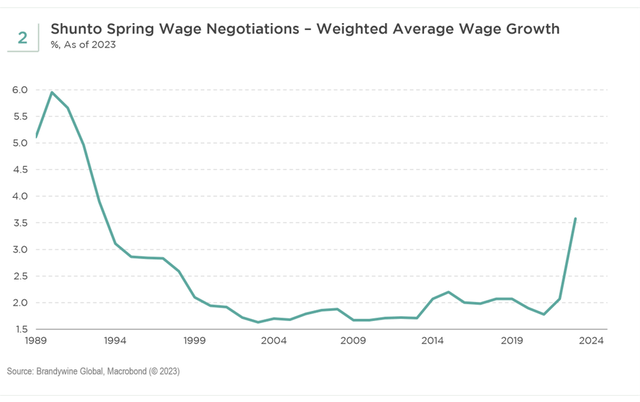

In the meantime, home auto gross sales are additionally shaping up properly – total Japan auto gross sales rose +17% YoY in August and may proceed to realize momentum as report Spring wage hikes increase client demand. Both means, the setup for Nissan seems to be nice heading into its subsequent quarterly earnings reviews.

Macrobond

Constructing on Manufacturing Benefits for the Mid to Lengthy-Time period

The largest upside to Nissan, for my part, is over the mid to long run. Managing labor pressures is vital, and going by how vital wage pressures have been on the US-based Detroit-3 (be aware the UAW is at present demanding ~36% vs. the >5% hike for Japanese autos), their incapability to take action will have an effect on their relative competitiveness going ahead. Even assuming we see the UAW settle someplace within the center (possible within the ~30% vary over the subsequent 4 years), plenty of that can nonetheless come out of margins, so it’s exhausting to see the US pricing setting not turning into extra disciplined going ahead. Nissan’s restricted US manufacturing footprint can be an enormous benefit right here – its presence in lower-cost areas like Mexico, the place it already has the dimensions, means it has a head begin on the US automakers’ ‘near-shoring’ push within the coming years.

Bloomberg

Poised to Capitalize on UAW Disruptions

Nissan’s inventory has efficiently climbed final 12 months’s wall of fear to emerge as one of many best-performing auto names this 12 months. On the one hand, the shortages that weighed on earnings final 12 months have begun to reverse. Alongside the aggressive increase from additional yen devaluation, Nissan has seen larger automotive earnings and the market has rightly rewarded the inventory. That mentioned, Nissan nonetheless trades in a steep ~50% e book worth low cost (far under its Japanese friends), so it’s not at all overvalued.

From right here, the US market will probably be key – amid a resilient demand backdrop, UAW-driven manufacturing disruptions have given international producers like Nissan a window of alternative to realize incremental market share near-term. And within the mid to long run, a wider labor price differential vs. the Detroit-3, helped by Nissan’s lower-cost manufacturing base in Mexico and Japan, bodes effectively for its earnings energy. The dearth of China publicity additionally means much less draw back potential because the area continues to see demand weak spot and protracted pricing strain, significantly on EVs. Within the meantime, buyers receives a commission an honest ~3% dividend yield (with ample room for a hike) to attend.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.

Picture Supply/DigitalVision by way of Getty Photographs

Overview

The greenback’s surge stalled yesterday, and follow-through promoting has pressed it decrease towards all of the G10 currencies as we speak. The dollar-bloc and Scandis are main the transfer. Month-end, quarter-end pressures, coupled with a probable partial shutdown of the federal government starting Monday, and after key chart ranges had been approached or violated earlier this week, serving as a little bit of a cathartic occasion.

The Swiss franc snapped a 12-day dropping streak yesterday, its longest since 1975, and is greater as we speak. Nonetheless, until the euro rises above about $1.0655, it’s going to prolong its dropping streak to 11 consecutive weeks. Rising market currencies, save the Russian ruble and Turkish lira, are additionally firmer as we speak.

Though Japanese shares traded with a decrease bias, many of the different massive fairness markets superior, led by Hong Kong and mainland shares that commerce there. The mainland’s vacation that runs all subsequent week started as we speak.

Europe’s Stoxx 600 is up over 1%, having ended a five-day slide yesterday. If sustained, it might be the biggest achieve in slightly greater than two weeks. US index futures are buying and selling round 0.4%-0.7% greater. Bonds are additionally rallying. Benchmark 10-year yields are off 7-10 bp in Europe, led by Italy, regardless of higher-than-expected September CPI. Gilts are a laggard, with yields off about 5 foundation factors.

The 10-year US Treasury yield is down round three foundation factors to 4.54%, practically unchanged on the week. Decrease yields and a softer greenback are lending gold some assist after dropping to six-month lows yesterday. It’s buying and selling inside yesterday’s vary (~$1857.7-$1879.6). November WTI reversed decrease after reaching $95 yesterday. It fell to round $91.40 and is consolidating as we speak to commerce close to $92.30 within the European morning.

Asia Pacific

China has begun a protracted vacation interval that runs by subsequent week, shutting mainland markets. Nonetheless, the September PMI will probably be reported over the weekend. Though it might not be evident in market costs, the quite a few modest steps, as a substitute of huge stimulus seems to be yielding some outcomes.

Whereas it might be true that structural challenges usually are not addressed, cyclical forces can dominate within the near-term. The manufacturing PMI, for instance, is predicted to rise above the 50 increase/bust stage for the primary time in six months. The composite PMI is more likely to rise for the second consecutive month. The Caixin composite is projected to rise for the primary time in 4 months.

Japan’s worth pressures are moderating. Tokyo’s CPI is an effective inform of the nationwide figures, that are reported with an extended lag. Tokyo’s headline CPI peaked in January at 4.4% and stands at 2.8% in September. It has not risen since April. The core price, which excludes recent meals, fell to 2.5%, its lowest stage since July 2022, from 2.8%. The BOJ’s newest forecasts has the core price again under 2% by the tip of subsequent yr. After stalling at 4.0% in July and August, the measure that excludes recent meals and power slipped to three.8%, solely the second decline because the finish of 2021.

Individually, Japan reported August employment, retail gross sales, and industrial manufacturing. Japan’s unemployment price was 2.5%-2.7% in 2022 and a pair of.4%-2.7% this yr. In August, it was regular at 2.7%, and the jobs-to-applicant ratio was regular at 1.29. The participation price was additionally regular at 63.1%. After a dramatic 2.2% rise in retail gross sales in July, it eked out a small 0.1% enhance in August, considerably weaker than anticipated.

Lastly, July’s 1.8% decline has been adopted by a flat August, which was significantly higher than the 0.8% decline projected by the median forecast in Bloomberg’s survey.

In the meantime, the “intervention watch” continues, however with US Treasury yields extending their rise, now doesn’t appear to have probably the most favorable auspices. For the primary time since easing early August, the BOJ purchased JGBS in an unscheduled operation. The quantity was considered small and the 10-year JGB yield is sort of unchanged on the day. Different long-dated yields are additionally little modified.

The greenback was provided. After peaking at JPY149.70 on Wednesday, the greenback fell to JPY149.15 yesterday, and follow-through promoting took it to virtually JPY148.50 as we speak within the Asian session. It recovered again to yesterday’s low in early European turnover, the place it seemed to be stalling. The market needs to be a bit extra involved about intervention if the seemingly partial shutdown of the US authorities, widening autoworkers’ strike, and resumption of pupil mortgage servicing weakens the economic system and pulls long-term yield again from their highs.

Japanese officers have mentioned they’re in each day contact with the US Treasury and Secretary Yellen has expressed some sympathy if the intervention was aimed toward unstable markets. But, close to 9.4%, three-month implied yen volatility is on the decrease finish of the place it has been for the previous six months. One-week vol reached 6.5% firstly of the week, the bottom of the yr and is now slightly above 8%.

The Australian greenback recovered neatly from the yr’s low set on Wednesday close to $0.6330, rallying a full cent. It closed firmly above $0.6400 and the 20-day shifting common (~$0.6420). Comply with-through shopping for has lifted the Aussie to a seven-day excessive close to $0.6485. Choices for practically A$660 mln expire as we speak at $0.6500. One other batch for round A$565 mln expires there on Monday.

The US greenback settled towards the offshore yuan close to CNH7.2960 yesterday, its lowest shut since Monday, September 18. At present, it has recorded a two-week low close to CNH7.2810.

Europe

The eurozone’s CPI rose by 0.3% in September and that makes for a 2.8% annualized price in Q3, down from 3.6% in Q2. The year-over-year price fell to 4.3% from 5.2% and one other massive decline is predicted subsequent month. Nonetheless, the weak spot of the euro and better oil costs will blunt a few of the base impact. Recall that in September and October final yr, the eurozone’s CPI rose by 1.2% and 1.5%, respectively. The core price fell from 5.3% to 4.8%, which matches the slowest tempo since August 2022.

Yesterday, Germany reported decrease than anticipated figures, whereas Spain stunned on the upside. At present France stunned on the draw back, with a 0.6% decline month-over-month, which was twice as massive because the median forecast in Bloomberg’s survey anticipated. Italy’s stunned on the upside.

The UK’s Q2 GDP was left unchanged at 0.2%, however the year-over-year price was revised to 0.6% from 0.4%. Consumption and authorities spending had been revised decrease. Capital formation and enterprise funding had been revised greater. Exports weren’t as weak as initially reported however imports had been significantly stronger.

The UK reported a dramatic widening of the Q2 present account deficit from a revised GBP15.2 bln (from GBP10.Eight bln initially) to GBP25.Three bln in Q2. The median forecast in Bloomberg’s survey sees the UK economic system rising by 0.1% enlargement in Q3 and in This autumn earlier than stagnating in Q1 24. That mentioned, the swaps market in about an 80% likelihood of a hike Q1 24. At the beginning of the week, solely barely greater than 50% discounted.

Slovakia goes to the polls tomorrow to elect its fifth prime minister in 4 years. For Slovaks, the election is essential as former Prime Minister Fico, who was compelled to resign in 2018 amid mass protests following the killing of an investigative journalist and his fiancée, is operating forward within the polls.

It will be significant as a result of since Russia’s invasion of Ukraine, Slovakia has been an essential ally. In contrast to Poland and Hungary which continued a ban on Ukrainian grain after the EU deserted its, Slovakia seems to have labored out a licensing association. Fico’s election would pressure the ties with Ukraine. Cracks within the assist for Ukraine, additionally emanating from the US finances debate, could encourage Russia (and China) to remain the course. The battle in Ukraine is about to proceed and broaden.

Brief masking helped raise the euro to virtually $1.0580 yesterday, barely greater than we had projected. There are alternatives for slightly greater than Three bln euros struck at $1.06 that expire as we speak and the follow-through shopping for as we speak lifted the euro to round $1.0615, a four-day excessive. The following chart resistance is close to $1.0640.

Sterling recovered from six-month lows on Wednesday slightly forward of $1.21 and traded to $1.2225 yesterday, a three-day excessive. It stalled shy of the $1.2230, the (38.2%) retracement of the leg down that started from round $1.2425 on September 19, however has surmounted it as we speak, rising to about $1.2255 in Europe. The following resistance space is $1.2270-$1.2300.

America

The US Q2 development was left unchanged yesterday at 2.1%, however the consumption part was slashed in half to 0.8% from 1.7%. That warns that the anticipated pullback in client has already begun. At present’s August private consumption expenditures will seemingly be lifted by greater power costs, however in actual phrases, it might be flat.

The resumption of pupil mortgage servicing is more likely to knock consumption additional subsequent month. Nonetheless, private consumption is predicted to outstrip the achieve in revenue and which means financial savings continues to be drawn down. The Federal Reserve targets the headline PCD deflator however attracts consideration to the core price, which is known as a greater gauge of worth pressures.

Rising power costs, even when the US is a internet power exporter, nonetheless acts as a headwind to consumption. The core PCE deflator has stabilized round 0.2% a month. A 0.2% rise in August places the three-month annualized price at about 2.5%.

It has been some time because the US commerce steadiness attracted a lot market consideration. Given the greenback’s energy and development differentials, it has been impressively secure and smaller than a yr in the past. Within the first seven months of 2023, the US commerce deficit has averaged $90.Four bln a month. Within the Jan-July 2022 interval, the deficit averaged about $103.9 bln a month.

That mentioned, there was a big deterioration since earlier than Covid. Within the first seven months of 2019, the US month-to-month commerce deficit averaged $72.Four bln. Furthermore, the deterioration has taken place though imports from China have been lowered. China’s mercantilism is disruptive, however the US’ chronically massive commerce deficit emerged earlier than Beijing. The supply of US imports is altering and the brand new surplus international locations, like Vietnam will fall underneath nice scrutiny.

Canada reviews July GDP as we speak. After a 0.2% contraction in June, a 0.1% enlargement is predicted. The market already seems to have taken this on board and the firmer inflation readings. The swaps market has a virtually 80% of a hike discounted for This autumn. Whereas the partial closure of the US authorities will intervene with the financial reviews, Canada sees merchandise commerce, IVEY and S&P PMIs, and September employment information subsequent week.

For its half, the central financial institution of Mexico stored its in a single day goal price at 11.25% and reiterated no cuts are anticipated anytime quickly. Subsequent week, Mexico reviews survey information and employee remittances. Home automobile gross sales for September will probably be reported too. August gross sales had been 25% above August 2022 and year-to-date automobile gross sales have elevated by barely greater than 23%. By means of August, compared, US automobile gross sales are virtually 13% above yr in the past ranges.

The US greenback reversed decrease on Wednesday after testing the 20-day shifting common close to CAD1.3540. Comply with-through promoting took it to virtually CAD1.3470 earlier than discovering new bids, which carried it again to round CAD1.3515. At present, the dollar has fallen to about CAD1.3430, a brand new low for the week. Final week’s low was nearer to CAD1.3380. A break of that space would goal CAD1.3300.

The US greenback traded inside Wednesday’s vary towards the Mexican peso. It completed close to session lows (~MXN17.55) forward of the conclusion of the central financial institution assembly. The central financial institution raised it inflation forecast for Q1 24 to 4.4% from 4.1%, driving residence the purpose that coverage is on maintain. Many now don’t assume the primary lower will probably be delivered earlier than the election across the center of subsequent yr. The dollar has been bought slightly under MXN17.42. A break of MXN17.40 might sign a transfer towards MXN17.25-35.

The dollar consolidated towards the Brazilian actual as properly, however it largely held above the 200-day shifting common close to BRL5.0230. Nonetheless, given the greenback’s heavier tone, it might return towards BRL4.97-Eight as we speak.

Unique Publish

Editor’s Notice: The abstract bullets for this text had been chosen by In search of Alpha editors.

Oil futures edged decrease early Thursday, giving up positive aspects that had seen the U.S. benchmark commerce above the $95-a-barrel threshold for the primary time in a yr as buyers weighed tightening U.S. crude inventories.

Value motion

West Texas Intermediate crude for November supply CL00, -0.22% CL.1, -0.22% CLX23, -0.22% fell 18 cents to $93.50 a barrel, after buying and selling as excessive as $95.03.

November Brent crude BRNX23, -0.29%, the worldwide benchmark, was down 46 cents, or 0.5%, at $96.09 a barrel, after hitting a session excessive of $97.69.

Market drivers

The Power Data Administration on Wednesday reported that crude shares on the Cushing, Okla. supply hub fell to underneath 22 million barrels. Analysts at Saxo Financial institution say that’s near operational minimums and lowest for the reason that seasonal lows of 2014.

“Market focus is shifting again to the tightening within the bodily market, which outweighs a weakening danger urge for food amid broader market jitters,” mentioned UBS analysts led by Henri Patricot.

The inventories information energized a Wednesday rally that noticed the U.S. benchmark log its highest shut in almost 13 months.

The drop in U.S. inventories comes as Saudi Arabia and Russia have prolonged their manufacturing cuts till the top of the yr.

“Heading into winter, worries about provide tightness might proceed pushing costs north, however whether or not it will evolve right into a long-lasting uptrend is questionable. The challenges dealing with China and Europe, the 2 largest oil customers on the earth behind the U.S., may additional dent demand, one thing which will begin being mirrored in costs sooner or later sooner or later,” mentioned Charalampos Pissouros, senior funding analyst at XM.

Coverage makers and researchers have been fretting that the share of older Individuals with debt has risen from 38% to 63% since 1990.

Having debt, nevertheless, doesn’t need to be a foul factor. For instance, households that take out a low-interest mortgage to purchase a house, which usually appreciates, are probably making a savvy selection. In distinction, households that carry unpaid credit-card balances may see their debt snowball, resulting in monetary misery.

In a latest research, my colleagues and I attempted to kind out what share of households with debt have been at “excessive threat” and “low threat” of economic hardship and whether or not these at excessive threat usually seemed the identical or fell into distinct teams.

Learn: I’m in my 60s with virtually $1 million. My house is paid off. I’d like to maneuver however am afraid of the excessive costs elsewhere: ‘Will I be OK?’

Step one was figuring out what number of of those households have been at excessive threat. The elements—secured vs. unsecured debt, debt payment-to-income ratio, and debt-to-assets ratio — are generally utilized by lenders and different researchers (see Desk 1). Households with any revolving credit-card debt are categorized as “excessive threat” since many of those debtors may expertise dangerous outcomes, despite the fact that the opposite debt measures wouldn’t seize them.

The outcomes of the classification train present that general progress is pushed by high-risk households (see Determine 1).

In eager about coverage options, it’s important to determine how these high-risk households acquired in bother. To do this, we used a way that exposed 4 clear subgroups of high-risk debtors.

The biggest group (33%) consists of “financially constrained” households, which have low ranges of wealth, are sometimes overleveraged, and wrestle with the necessities. This group is borrowing simply to get by.

The second subgroup (26%) consists of “credit-card debtors,” which incorporates middle-wealth households with no obvious have to borrow.

The third subgroup (19%) is low/middle-wealth households whose housing debt funds eat over 40% of their revenue. This group can be disproportionately nonwhite.

The final group (23%) is “rich spenders.” Regardless of being within the high third of the wealth distribution, a couple of quarter of their revenue goes to debt funds, about 80% have credit-card debt, and over a 3rd have second houses.

What may be accomplished to cut back the monetary vulnerability of high-risk debtors? Given their numerous traits, no one-size-fits-all answer exists.

Debt counseling and consolidation could assist the “financially constrained” households, however many wrestle to fulfill primary wants, so that they want extra assets.

“Credit score-card debtors” may benefit from conventional monetary counseling and laws requiring credit-card issuers to supply higher data to shoppers.

Households with “an excessive amount of home” would finest be served by applications that cut back their housing burden, akin to refinancing or downsizing.

Lastly, since many “rich spenders” have a second house, promoting it’s one solution to handle their debt.

The important thing takeaways from this research are: 1) the rising debt amongst older households just isn’t a benign phenomenon; and a pair of) the various traits of high-risk debtors require quite a lot of coverage responses.

Learn extra from MarketWatch Retirement:

‘What I wasn’t ready for was actuality.’ How do retirees survive on Social Safety alone?

Methods to use a ‘spend down’ to qualify for Medicaid

It’s time for Medicare’s open enrollment. Don’t miss this necessary step.

“ Going from zero to 2% was virtually no enhance. Going from zero to five% caught some individuals off guard, however nobody would have taken 5% out of the realm of risk. I’m not positive if the world is ready for 7%. ”

— Jamie Dimon

That’s JPMorgan JPM, +0.49% Chairman and CEO Jamie Dimon, speaking to the Instances of India, per week after the Federal Reserve saved rates of interest regular in a spread between 5.25% and 5.5% and flagged one final fee hike for this financial cycle.

That makes Dimon significantly extra hawkish than his personal economists — who simply count on yet one more fee hike — or the markets basically.

Whereas monetary markets don’t essentially envision a world with 7% rates of interest, they’re adjusting to a higher-for-longer stance on the Fed.

The yield on the 10-year Treasury BX:TMUBMUSD10Y jumped one other 10 foundation factors on Monday to the best degree in almost 16 years. The yield on the 30-year BX:TMUBMUSD30Y has surged as properly, reaching its highest degree in additional than 12 years. The S&P 500 SPX did handle to advance on Monday regardless of lengthy yields rising, however the index is 5% under its late July highs.

Within the interview, Dimon stated the worst case could be 7% rates of interest with stagflation. “If they will have decrease volumes and better charges, there shall be stress within the system. We urge our shoppers to be ready for that type of stress,” he stated.

One fear Dimon doesn’t share, nonetheless, is the mixture of social media and digital banking. “Social media and on-line banking existed in the course of the nice monetary disaster. Solely a handful of banks had the issue — Silicon Valley Financial institution, First Republic Financial institution and Signature. Different banks didn’t have an issue,” he stated. “The issue of rate of interest publicity was recognized to everybody. I don’t assume we would like a system the place no financial institution ever fails.”

Dimon was chatting with the newspaper after JPMorgan’s choice so as to add India to its emerging-market authorities bond index. “It’s a superb factor for India to be a part of the index as a result of it has different ramifications and implications about transparency and the nation’s development. So, it would assist fairness flows into India,” he stated.

AerCap Holdings N.V. (NYSE:AER) is an airplane, engine, and helicopter lessor led by CEO Aengus “Gus” Kelly. AerCap underwent a transformative acquisition when it acquired GECAS (GE Capital Aviation Providers) in This fall 2021. A number of disruptions over the previous three years, together with Covid and the Russia-Ukraine Battle, challenged the enterprise as air journey stopped and airplanes leased to Russian airways couldn’t be seized. Whereas these challenges are comparatively behind the corporate, a big overhang stays. GE owned 14.5% of AER inventory as of 9/21/23, which they may proceed to promote down, making a near-term overhang. As soon as GE exits its stake, AER is way extra compelling. The short-term promoting stress caps near-term upside. GE made intentions identified to exit the place, which ought to occur by Q1 or Q2 of 2024. AerCap’s low cost to BV and mid-single-digit earnings valuation is compelling sufficient to go lengthy in a small starter place, growing the place measurement as GE sells the remaining stake.

Enterprise Description

AerCap is the biggest aviation leasing firm on the earth, with a portfolio of two,323 plane, engines, and helicopters owned, 718 managed, and 426 on order as of June 30, 2023. AerCap supplies a variety of belongings for lease, together with narrow-body and widebody plane, regional jets, freighters, engines, and helicopters, specializing in buying in-demand flight tools at engaging costs, funding them effectively, and hedging rates of interest when prudent. Along with their main enterprise, they’re the world’s largest engine leasing firm, with over 900 owned and managed engines.

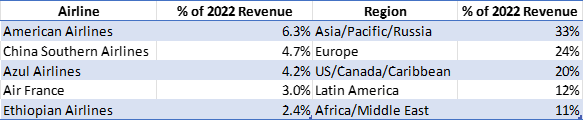

AerCap’s mannequin is an expansion enterprise. Borrowing at a less expensive price than airways because of the constant income stream and buying planes cheaper attributable to bulk purchases. The place the price of debt for American Airways in March 2023 was 7.25% for five-year notes, AerCap was in a position to challenge 5-year debt at 5.75%. The chart under depicts AerCap’s high 5 prospects and the geographic area of its income base.

AerCap Income Breakdown (AER 10-Ok)

The decrease the credit standing of an airline, the upper the price of financing, and the extra probably they’re to lease fairly than personal. Excessive debt service prices for low credit standing firms impede working a worthwhile enterprise. As an alternative, AerCap’s decrease price of financing permits them to behave as a intermediary, taking an expansion above their financing price and lending it to those riskier prospects. Airways lease a airplane fairly than personal it for just a few causes. The primary ties into the above: airways will need to have entry to capital to buy a airplane. The price of an airplane can run $100m+ (kind of relying on the physique kind); some airways are too small to afford this. Second, a lease doesn’t lock an airline right into a long-term dedication. As an alternative, they’ll lease a airplane for 5-10 years, with the one upfront capital as a safety/upkeep deposit and the primary few months of hire. The upkeep deposit might be refunded on the finish of the lease if the airline returns the airplane in good situation. The delta between a deposit and preliminary hire funds in comparison with the outright possession of a airplane is substantial, giving the airline better flexibility. Lastly, the airline doesn’t bear the residual worth threat when the airplane ends its helpful life. Technological obsolescence could lead to a scrapped airplane.

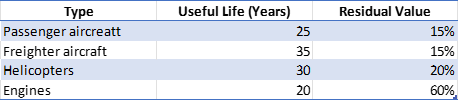

Moreover, there are dangers if the airplane producer unveils new expertise, resembling better gas effectivity, extra seating, or a greater flying expertise. Airways could change into uncompetitive attributable to a worse flying expertise or competitors providing higher costs. With a lease, as an alternative of the airline bearing this for the lifetime of the airplane, sometimes 25 years, the lessor bears this. The desk under depicts the airplane/tools depreciation schedule and the residual worth assumed. A $50m plane buy has $7.5m of residual worth. The danger of getting an outdated airplane through the early to center of life will increase for airways with little information of future demand developments. AerCap, given its broad buyer base, foresight into leasing/demand developments, and database of transactions, is way extra prone to be the primary to know when demand and expertise adjustments will happen.

Plane Depreciation Schedule (AER 10-Ok)

Constructing on the final level. Gus usually discusses the worth of the AerCap platform. In the course of the yr ended December 31, 2022, the corporate executed 895 asset transactions (sale, lease, or buy). In earlier years, they accomplished 349, 179, and 349 from 2019 – 2021. AerCap has an unmatched database concerning what airplanes are in demand, slim physique vs. vast physique, Airbus or Boeing, is unparalleled. Probably the most important threat for a lessor is buying an out-of-demand airplane that generates minimal lease income and is probably going out of demand when the lease renewal happens or on the finish of life, having no residual worth. With extra information than anybody else, the informational benefit permits them to lease planes at one of the best risk-adjusted charges, promote planes on the highest value, and buy probably the most in-demand plane.

Thesis

Whereas the above paints a constructive image for AerCap’s enterprise, the promoting stress stemming from the GE selldown has resulted in AER’s inventory declining 2% for the reason that 15-month lockup ended on February 1, 2023, in comparison with the S&P 500, up 6%. A 20% drawdown coincided with GE’s first sale announcement once they filed to promote 23m shares for $58.50, $1.50 under the inventory value. The latest sale announcement occurred on September 11, promoting ~47m shares at $59.00, $2.79 under the present buying and selling value. AerCap repurchased 15.3m, decreasing the shares coming to market. In seven months, the low cost GE is keen to tackle the shares nearly doubled in seven months. GE desires the money and never AER inventory. Under, I’ll stroll via my valuation, which makes AerCap look engaging; till this promoting stress subsides, I battle to see how the valuation hole absolutely closes.

I like to recommend constructing a place as GE continues promoting and reaches 3% or much less of an proprietor. AerCap’s historical past of repurchasing shares ought to speed up the worth realization. My expertise with a number of forms of investments, the place sometimes Personal Fairness or a big shareholder sells down, is extra vital than enterprise outcomes. If outcomes are good, the sell-down continues and will speed up. Poor outcomes trigger additional promoting stress, and a big share sell-down ends in a one-two mixture of promoting stress.

Unit Economics

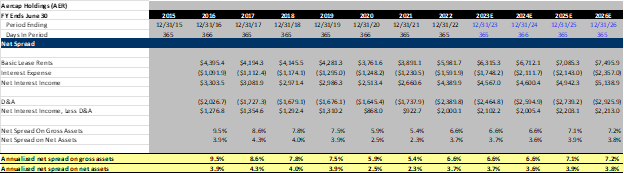

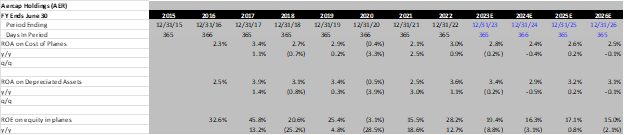

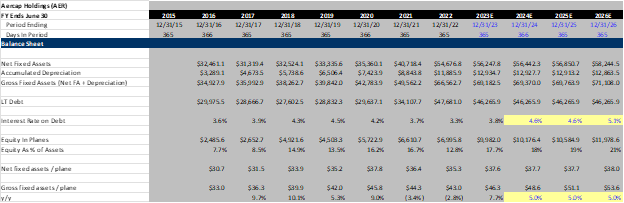

AerCap’s unfold mannequin is to challenge low-cost debt, buy plane at a sticker value (bulk buy) low cost, and cost lease rents at an expansion over borrowing prices whereas factoring within the credit standing of the top buyer. Its enterprise mannequin is just like a financial institution. Borrow at low charges and lend at larger charges, modify spreads or safety deposit (for a financial institution down cost) for credit score threat. In AerCap’s case, understanding the annualized internet unfold on belongings offers us an concept of the margin they obtain. Calculated by taking fundamental lease rents, subtracting curiosity and depreciation, and dividing by property and tools. The desk under depicts the historical past of this. My estimates for 2024-2026 are primarily based upon the corporate’s order guide, historical past of asset gross sales, and debt schedule (mentioned extra within the steadiness sheet part under)

Internet Unfold (AER 10-Ok)

Enterprise efficiency and, subsequently, the inventory is just like how a financial institution’s enterprise performs. The upper return on belongings (ROA) in AerCap’s case, larger return on plane, the higher enterprise performs. Taking it additional, like a financial institution, AerCap makes use of leverage. On the finish of Q2, that they had internet debt of $45.1B and flight tools of $55.6B. The corporate’s debt/fairness ratio stood at 2.5x, under their goal of two.7x. Using leverage considerably enhances the return on fairness of the corporate. Like a financial institution, the place ROA’s vary from 1-4%, leverage elevates the return on fairness to shareholders to 8-12% on common. AerCap follows the same playbook, with an ROA starting from (0.5%) to three.9% since 2015 and an ROE starting from (3.1%) to 45.8%. (Please notice this calculation is completed as PP&E – debt = fairness in planes).

One other calculation I run to grasp how administration costs leases is trying on the ROA on the price of planes. AerCap has constantly generated a 2.1% – 3% Return on price (excluding 2020), which is nice, in my view.

AerCap ROA/ROE (AER 10-Ok)

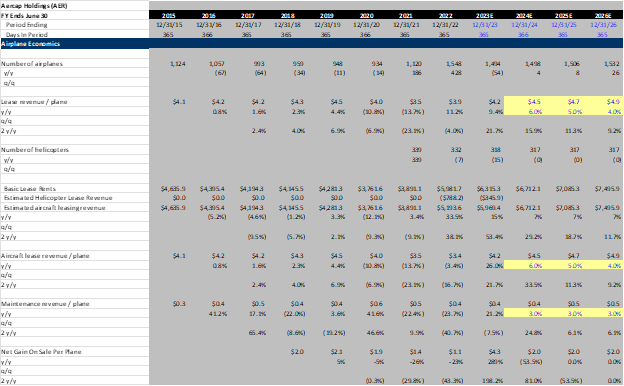

Lease rents generate 80%+ of income, the remaining coming from upkeep income (supplemental upkeep hire primarily based on plane utilization through the lease time period or end-of-life-compensation primarily based on the plane’s situation), acquire on sale when AerCap sells an plane for greater than its carrying worth, and different earnings generated from claims, curiosity, administration charges, and different miscellaneous earnings.

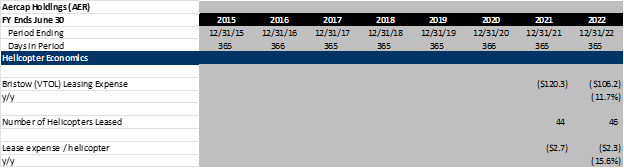

The corporate’s income per airplane exhibits how lease charges trended. 98.2% of AerCap’s rents are fastened, and the rest are floating charge tied to rates of interest. When AER acquired GECAS, they acquired a portfolio of 300+ helicopters and an engine leasing enterprise proudly owning 450+ engines. One in every of AerCap’s prospects is Bristow. Utilizing Bristow’s leasing prices and the variety of helicopters leased to calculate the leasing price per helicopter, then making use of this determine to AerCap’s helicopter enterprise to estimate the helicopter section income. I used to be unable to discover a comp for the engine leasing enterprise. Since 85% of AerCap’s belongings are plane, I consider together with the engine leasing income however not the variety of engines is sufficient to present how leasing income per airplane has trended.

Airplane Unit Economics (AER 10-Ok, VTOL 10-Ok)

VTOL Lease Expense (VTOL 10-Ok)

As proven within the spreadsheet above, within the line Plane lease income/airplane, income per airplane has not recovered to pre-pandemic ranges. As lease modifications roll off and leases signed throughout 0% charges, leasing developments ought to regain and surpass pre-pandemic ranges within the subsequent 2-Three years.

Since AerCap’s price of financing is growing, they need to move on these larger prices to prospects. Listening to Gus on the Deutsche Financial institution Plane Finance and Leasing Convention, he said that new lease charges have moved in lockstep with rates of interest. I estimate lease income/airplane return to 2019 ranges in 2024 and enhance mid-single digits in subsequent years. The rise in rental earnings will partly be offset by larger financing prices (mentioned within the steadiness sheet part).

AerCap has been a internet vendor of plane as a result of they’ve constantly been in a position to promote their planes at a premium to carrying worth whereas the inventory has sometimes traded at or under guide worth. AerCap can promote planes at a premium and purchase the inventory at a reduction. Promoting a airplane for a 10% premium to carrying worth and buying the inventory again at a 10% low cost is a 20% unfold of worth creation (assuming the plane sale and carrying worth are indicative of the remaining guide).

In 2018-2019, AerCap bought ~10% of their fleet every year. In the course of the pandemic, this determine was reduce in half to ~5%, recovering in 2022 to 13%. By means of Q2 23, AerCap bought 39 plane/engines (3.3% of fleet) at unsustainably excessive costs and margins. As proven within the chart under, in Q2, AerCap bought belongings at nearly 2x the carrying worth. Traditionally, 1.1x-1.2x has been the norm. In the course of the Q2 name, Aengus said, “On the gross sales aspect, we proceed to see robust and broad-based demand for our belongings, closing $818 million of transactions within the quarter. This resulted in our highest-ever quarterly acquire on sale of $166 million, representing a 25% margin. Encouragingly, this was not confined to plane belongings. We additionally noticed robust good points in our engine and helicopter gross sales with document volumes in every class. This additional confirms the advantages of the asset diversification AerCap now enjoys.” They acknowledge these margin ranges are unsustainable, so I’ve them returning to historic ranges.

The principle causes AerCap can promote planes at a premium are twofold. First, the price of new construct plane has elevated considerably over the previous a number of years. Plane are depreciated over a 25-year helpful life. Subsequently, if AerCap by no means refurbished or reinvested into the plane, the worth would decline 4% per yr. Over the previous few years, inflation ran north of this determine, so whereas the planes misplaced 4% in worth every year, the price to interchange them elevated at a better charge. Inflation working at 8% and planes shedding 4% of worth ends in a internet 4% enhance in resale worth. Exacerbating this drawback is the uncertainty round Boeing and Airbus deliveries, which places airways in a state of affairs the place they’re not sure what their fleet measurement will likely be in a yr. Paying the premium to have certainty of supply is price it for them, giving AerCap bargaining energy.

AerCap acquire on sale (AER 10-Ok)

Valuation

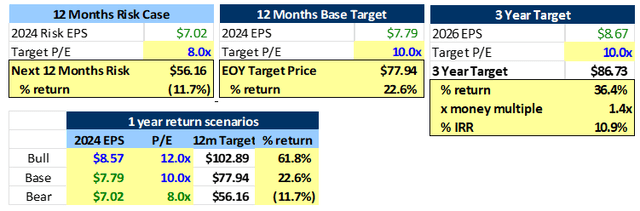

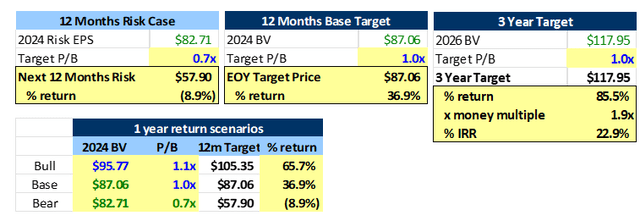

I used two valuations to develop a good worth of AerCap: a P/B and a P/E. Vital asset writedowns throughout 2020 resulted in a loss. Going ahead, I consider AerCap’s ROE will likely be ~15%, which might sometimes warrant a P/B better than 1x and a mid to excessive double-digit earnings a number of; nevertheless, again and again, like a financial institution goes via a recession and has elevated write-offs, each decade, an surprising occasion appears to happen, inflicting AerCap writedown belongings. With this the case, a 1x P/B and 10x P/E appears affordable. Moreover, given the leverage profile of the enterprise, the potential for a catastrophic occasion is at all times current.

Utilizing the P/E first and primarily based on my evaluation and estimates, my one-year value goal is ~$78 with a draw back of ~$56 for a 2/1 threat reward. If acquire sale margins stay sturdy and leasing charges speed up, I consider there could possibly be upside to estimates and the a number of. My bull case is that the corporate generates ~$8.57 in EPS and, given the robust developments, trades at 12x earnings for a 62% return. With a ~5:1 upside/draw back, the valuation is compelling.

Below both valuation methodology, the chance/reward is compelling. My common 12-month draw back case is ~$57, base case ~$82, and upside ~$104. With a $63 inventory, the risk-reward skews constructive. The draw back situation would probably take a number of elements, together with softening demand, decrease leasing revenues, decrease acquire on sale margins, and financing prices accelerating to the upside. The bull case entails accelerating lease charges, sustained acquire on sale margins, and internet unfold growth.

Traditionally, acquisitions within the house had been above guide worth, lending additional credence to the above valuation. Fly Leasing is the only real acquisition I might discover accomplished under guide worth. Nevertheless, this was attributable to Fly’s pressured steadiness sheet throughout COVID-19.

Lessor Transaction Comps (Public Filings/Google)

Stability Sheet

AerCap, like many financials, runs a levered steadiness sheet. An important objects on AER’s steadiness sheet are Internet Fastened Belongings, that are the carrying worth of plane belongings (price – collected depreciation), Lengthy-Time period debt, and guide fairness. Earlier than the GECAS acquisition, AerCap’s belongings remained comparatively secure because of the continued promoting of older plane and the following buy of latest plane. Debt was additionally comparatively secure at ~$29B. Because the chart under exhibits, AerCap’s fairness in planes (Asset Worth – Debt) elevated since 2016. Whereas this hurts the ROE, because the leverage declines (leverage magnifies returns), monetary stability, flexibility, and draw back safety enhance. Beforehand, a 10% decline in Plane values worn out fairness holders. Whereas the chance of such an occasion is minimal, black swan occasions like COVID-19 and 9/11 underscore these left-tail occasions. On the finish of 2023, I estimate AerCap may have an fairness cushion of ~18%.

Whereas the enterprise economics deteriorate with this larger fairness (i.e., decrease ROE), the catastrophic threat of the enterprise considerably declines. A trade-off of decrease returns however elevated security is one I agree with. Contemplate what might trigger plane values to say no by 18%: authorities mandates a selected gas effectivity, or all planes should be electrical, inflicting AerCap’s planes to change into out of date. A world despair causes air journey to say no, resulting in airline chapter and lease defaults. AerCap’s lack of ability to lease planes might trigger the worth of the planes to say no. A number of different occasions are potential, however contemplating what would occur to the airline trade beneath these conditions, no airline can utterly rework its fleet in a single day. Boeing and Airbus have restricted manufacturing capability. Sooner or later, one might be too pessimistic.

AER Stability Sheet Information (AER 10-Ok)

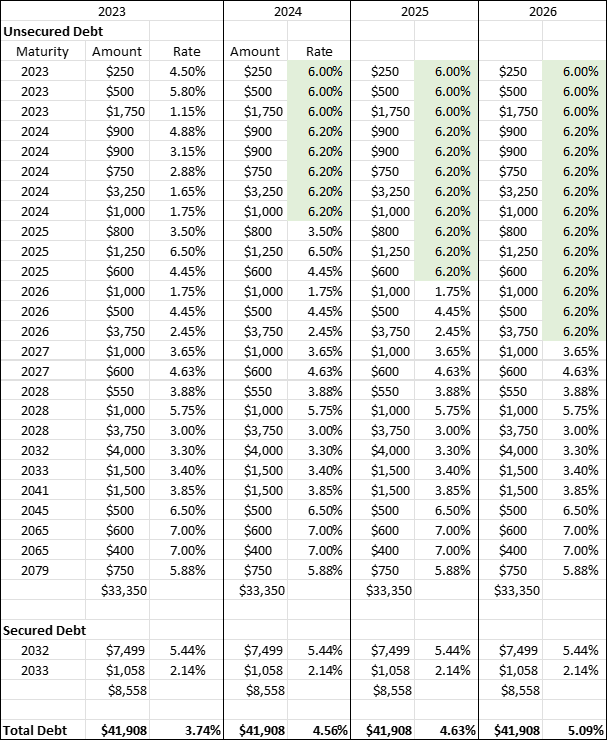

In 2023, AerCap had three bonds mature with rates of interest of 4.5%, 5.8% and 1.15%. In the present day, the corporate’s price of medium-term debt is ~6-6.5%, as mentioned within the subsequent paragraph. The chart exhibits the corporate’s maturity profile and adjustments to its weighted common rate of interest as bonds come due within the subsequent a number of years. I assume the corporate points medium-term debt at 6.2% (which could possibly be low relying on the place rates of interest go). In 2024, the corporate’s common charge goes to 4.56%. In 2025 4.63%, and in 2026 5.09%. Given the low base of three.74% in 2023, the 135 bps charge enhance is a 36% enhance in curiosity expense. Ought to charges proceed to maneuver larger, financing prices will additional enhance.

AerCap just lately issued 6.100% senior notes due in 2027 at 99.540% and $850M at 6.150% in 2030 at 99.371%. The debt issuance was one of many few instances I questioned administration’s motive. Sometimes, when an organization points shorter length debt, they pay decrease curiosity prices for it because of the upward-sloping yield curve, much less uncertainty of a credit score occasion, and decrease rate of interest threat (the chance that charges rise and the investor loses out by not having the ability to put money into the higher-yielding debt). On this case, AerCap issued 2027 2030 debt at roughly the identical rate of interest, probably because of the inverted yield curve. On this situation, firms needing to refinance debt ought to go far out on the yield curve as a result of the market fees them lower than in the event that they went shorter. Why AerCap would challenge 2027 bonds for a similar value as 2030 is puzzling, fairly than issuing all of the bonds in 2030.

Most monetary firms run a laddered bond portfolio, issuing bonds at totally different durations to not have one yr with considerably extra maturities due than one other. Once more, shorter bonds usually have decrease rates of interest than longer. In AerCap’s case, they pressured themselves to refinance debt in 2027. One can envision debt markets being closed then, but AerCap nonetheless must entry the markets by paying a better charge. AerCap might have run the laddered portfolio with these bonds, even when each had 2030 maturities, by forcing or mentally noting that the plan is to refinance a portion of the debt in 2027. If debt markets are closed in 2027, it offers them just a few extra years for markets to normalize. Optionality is commonly underappreciated.

Administration

Aengus has been CEO of AerCap for over 12 years. He grew up within the aviation leasing trade (he is solely 49). I might suggest listening to him discuss. He is trustworthy, simple, and clear. As a earlier shareholder of AER, AerCap was by no means an organization that saved me up. I belief Aengus will make the right choices.

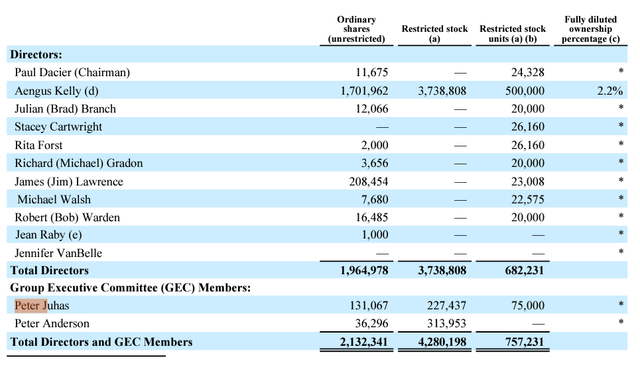

AerCap’s coverage on govt possession is that govt members should personal shares valued at a minimal of 5x their annual base wage; for the CEO, the minimal is 10x. Under particulars administration’s possession stake. The dearth of unrestricted inventory possession is regarding. Most board members personal little inventory and have most of their fairness possession granted via RSU’s.

AerCap insider possession (AER 10-Ok)

Administration’s fairness compensation bundle relies on long-term development, worth creation, and EPS development. I’ve no challenge with these efficiency metrics as a result of the corporate ought to change into extra beneficial over time via BV appreciation and growing EPS.

Dangers

Demand for plane relies upon upon the demand for air journey. The principle threat with proudly owning a lessor is that air journey demand falls, leading to much less demand for his or her plane. One of many essential dangers administration discusses is the residual worth, the remaining worth of the plane on the finish of a lease. Decrease demand for plane would lead to AerCap impairing the asset. Impairments decrease the guide worth and, due to this fact, the corporate’s truthful worth.

Alongside these strains, I’ve had the chance to fulfill Aengus and listen to him converse at a number of conferences. He’s by no means shy about sharing his opinion of Airplane producers. Boeing and Airbus care little in regards to the airplane’s worth as soon as they promote it to a lessor or airline. Aengus said a number of instances that the monetary outcomes will likely be poor if an organization buys what Boeing and Airbus wish to promote them. As an alternative, given AerCap’s database, they know what probably the most in-demand plane will probably be at any time, which is usually totally different from what the producer desires to promote. This is smart. For instance, if narrow-body planes are in excessive demand, Boeing is probably going already at max manufacturing capability; they can’t enhance manufacturing in the event that they wish to, so that they don’t have any cause to push gross sales for them. However, vast our bodies are probably in much less demand. With the surplus manufacturing capability, Boeing is out making an attempt to promote these planes to lessors. Equally, buying planes with few potential prospects could possibly be problematic. If the unique lessee doesn’t re-lease the airplane, the potential to lease it to a brand new buyer is difficult because of the lack of potential suitors.

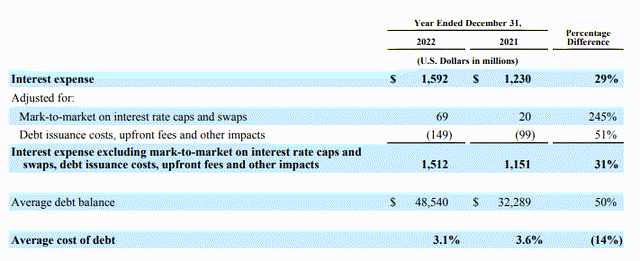

The chart under exhibits that AerCap’s common price of debt in 2022 was 3.1% (totally different from above attributable to floating charge caps and swaps). Given the dramatic rise in rates of interest over the previous yr, we all know that AerCap’s debt price will enhance.

AerCap common price of debt (AER 10-Ok)

In AerCap’s 20-F, they state, “As our leases are primarily for a number of years with fastened lease charges all through the lease, we usually can not enhance the lease charges with respect to a selected plane till the expiration of the lease, even when the market is ready to bear the elevated lease charges. Because of this, there will likely be a lag in our means to regulate and move on the prices of accelerating rates of interest.” If AerCap is unable to extend lease rents at a charge just like or better than their price of financing enhance, the corporate’s internet unfold will contract, resulting in a decline in profitability.

Lastly, ought to GE speed up the selldown of AER shares, it might enhance stress on shares within the quick time period.

Q2 Outcomes

AerCap reported robust ends in Q2, headlined by a $500m repurchase authorization, guide worth growing 14% y/y, and full-year adj. EPS steering growing to $7.50-$8.00 excluding acquire on sale from $7.00 – $7.50 ($8.50 – $9.00 together with acquire on sale) attributable to robust demand developments and sturdy acquire on sale margins. The corporate recorded its highest-ever acquire on sale in 1 / 4 of $166m, stating gross sales had been robust in all segments. They’ve $809m of belongings held on the market and are on monitor to promote $2.5B of belongings for the yr. In the course of the quarter, they repurchased $300m price of shares.

Subsequent to quarter finish, on September 5, 2023, AerCap acquired money insurance coverage settlement proceeds of $645m from insurance coverage claims because of the 17 plane and 5 spare engines on lease to a Russian service. Unsurprisingly, with the corporate’s proceeds, they elevated the buyback authorization by $650m two days later. As of 9/7, AerCap had $1.3B remaining beneath its repurchase authorization, roughly 10% of at this time’s market cap.

Abstract & Ahead-Trying Objects to Monitor

AerCap is affordable; nevertheless, the GE share sell-down is probably going capping the upside within the quick time period. One of the best sport plan is having a starter place and sizing it up as GE sells down, balancing at this time’s engaging value with the near-term headwinds offered. AerCap’s administration group may be very skilled, demand developments stay robust, and the enterprise generates mid to excessive teenagers return on fairness, which helps a better valuation than at this time’s low cost to BV.

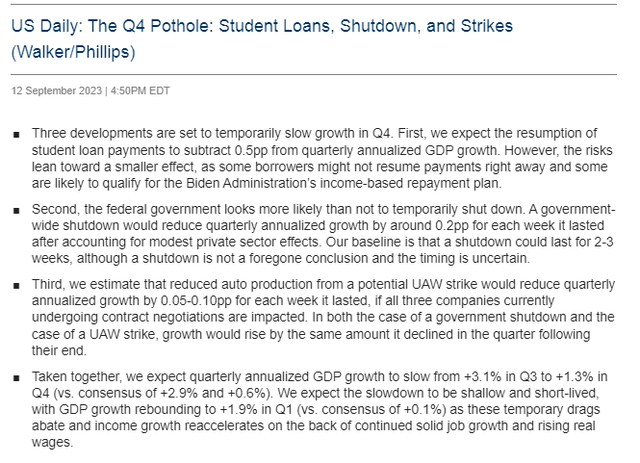

Is a This fall pothole on the street forward? That is what Goldman Sachs’ David Kostin asserts. Earlier this month, he and the remainder of the GS economics group outlined a trio of dangers that might derail what has been a 12 months of surprisingly robust home actual GDP progress.

Together with a looming authorities shutdown and the continuing UAW strikes, the resumption of scholar mortgage repayments might crimp budgets and damage discretionary spending.

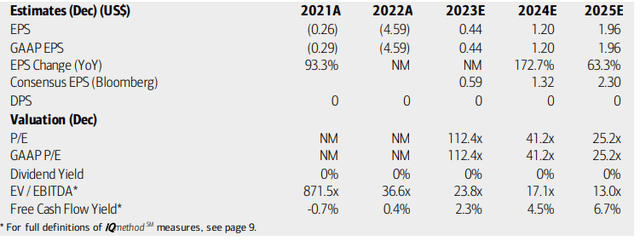

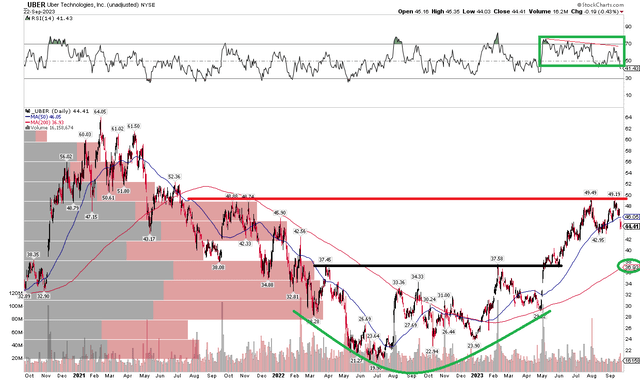

May Uber Applied sciences (NYSE:UBER) be in danger? With Uber Eats having a excessive proportion of month-to-month lively customers in the important thing 25- to 44-year-old cohort, some analysts imagine draw back dangers are on the horizon.

I reiterate my purchase ranking on Uber, nonetheless. I see a sturdy longer-term earnings story enjoying out whereas worth motion has completed the whole lot it ought to since I initiated protection on the inventory earlier this 12 months.

This fall Dangers Forward

Goldman Sachs

In response to Financial institution of America World Analysis, UBER is a mobility platform that providers 72 international locations, 750+ ridesharing markets, and 500+ Eats markets, and almost half of Core Platform Income is generated outdoors of the U.S. The corporate now has over 130 million month-to-month prospects with revenues generated from Mobility, Supply, and Freight providers.

The San Francisco-based $91.1 billion market cap Passenger Floor Transportation firm throughout the Industrials sector has unfavourable trailing 12-month GAAP earnings and doesn’t pay a dividend. Forward of earnings subsequent month, the inventory contains a reasonable implied volatility proportion of 35% whereas its quick curiosity is low at simply 2.4%.

Again in early Might, the corporate reported Q2 GAAP EPS of $0.18 which topped analysts’ estimates of a 1-cent per-share loss. Income was properly larger on a year-on-year foundation, +14%, at $9.2 billion, although that fell in need of what Wall Avenue projected. With Gross Bookings up 16% from year-ago ranges and an 18% rise on a constant-currency foundation, the general progress trajectory nonetheless seems strong.

Impressively, UBER reported file quarterly free money circulation of $1.1 billion. The agency’s increasing EBITDA margin and excessive revenue flow-through come as the buyer sees some weak point, however Uber’s earnings come largely from its stable Mobility and Promoting segments – long-form video advertisements noticed a big increase from the identical quarter final 12 months.

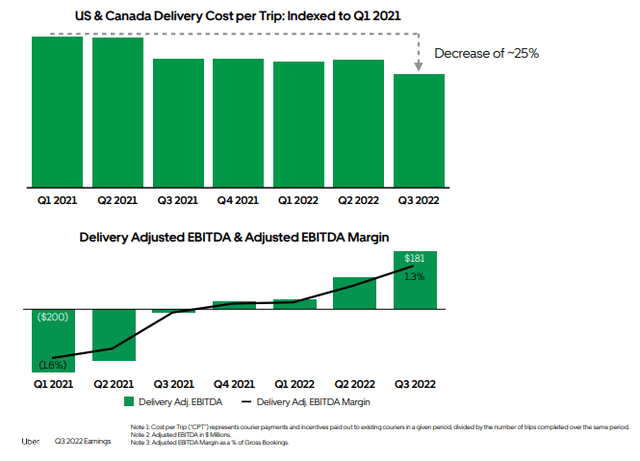

Supply Margins on the Rise

Uber IR

Key dangers embody the potential for a number of compression as a result of macro components (weaker shopper and company advert spending), slower progress in gross sales and customers from competitors, rising competitors from self-driving know-how corporations, and the hostile impacts of recent laws.

On valuation, analysts at BofA see earnings persevering with the pattern nicely into constructive territory. Out-year EPS is seen north of $1 whereas the 2025 consensus estimate, on the newest verify, is $1.79 per In search of Alpha. This fast-growing firm just isn’t anticipated to pay dividends any time quickly, however the agency is free money circulation constructive. With earnings a number of anticipated to dip into the mid-20s with bottom-line progress, the PEG ratio is engaging trying forward.

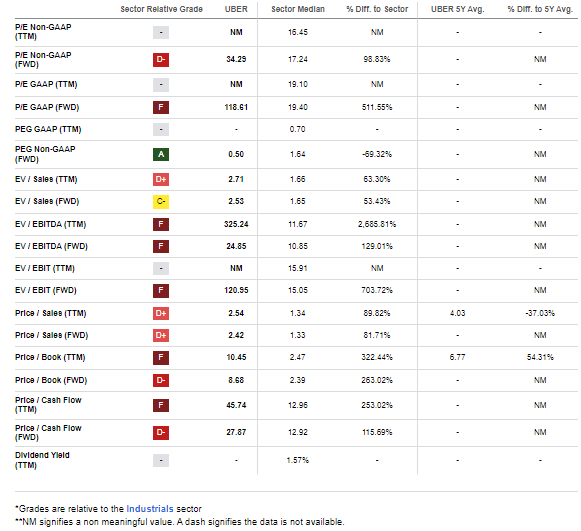

UBER’s ahead PEG ratio is presently simply 0.5, incomes it an A ranking there (although the general valuation ranking is only a D). Following the stable Q2, I proceed to say {that a} 25x P/E on $2 of future EPS is a really affordable valuation. On a ahead gross sales foundation, the inventory is only a 2.Four a number of – nicely beneath that of rival Instacart Maplebear (CART) that simply went public. The trailing 12-month price-to-sales ratio is at a 37% low cost to its 5-year common, too.

UBER: Poor Valuation Grades, However Banking on Progress

In search of Alpha

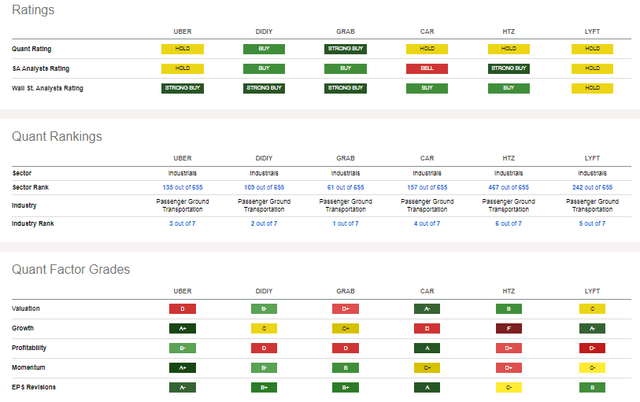

In comparison with its friends, Uber has the whole lot you need apart from worth earnings multiples. However I don’t count on this quick grower to be “worth” within the coming years. I do contend that it’s a GARP play, although, and its robust profitability and upside EPS revisions again up that narrative. Amongst its opponents, Uber additionally has the very best momentum proper now, although I’ll spotlight some near-term dangers to cost motion.

Competitor Evaluation

In search of Alpha

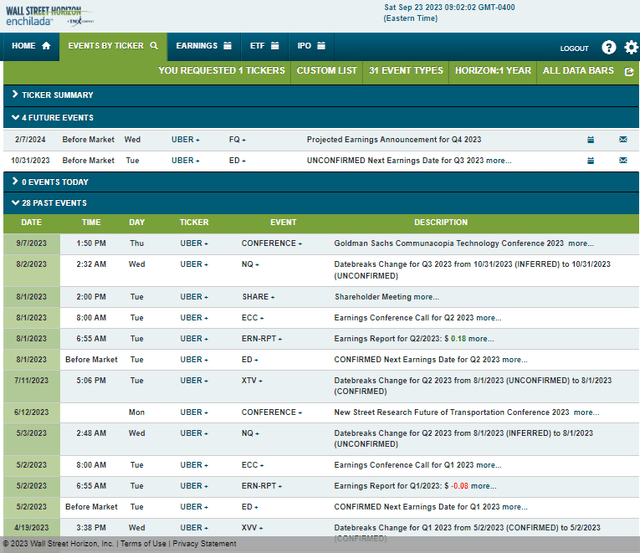

Wanting forward, company occasion knowledge offered by Wall Avenue Horizon present an unconfirmed Q3 2023 earnings date of Tuesday, October 31 BMO. No different volatility catalysts are seen on the calendar.

Company Occasion Threat Calendar

Wall Avenue Horizon

The Technical Take

As talked about earlier, UBER has completed the whole lot it has speculated to do since Q2, for my part. Discover within the chart beneath that shares almost touched $50 and have since pulled again after printing a near-term double high. Additionally check out the RSI momentum gauge on the high of the graph – whereas it stays in a bullish vary, there was some modest bearish divergence as worth rose in the summertime. I famous that in my preliminary evaluation earlier this 12 months.

I see near-term assist round $42, so that will be a very good place so as to add to the place. Longer-term assist is seen on the rounded-bottom breakout level within the $37 to $38 zone. Total, with a rising long-term 200-day shifting common and better highs & larger lows going all the best way again to June of 2022, the bulls seem in management. I proceed to see $50 as resistance, however a breakout above that degree would portent a attainable rise to $58 based mostly on this rising $eight vary that’s now a couple of months previous.

Large image, the trip just isn’t all the time easy, however I see Uber’s technical view as constructive.

UBER: $50 Stays Resistance, $42 Close to-Time period Help

Stockcharts.com

The Backside Line

It’s regular as she rides with Uber. Shares rallied to resistance and have pulled again, providing buyers an opportunity to hop in on this high-growth firm.

HighPeak Power (NASDAQ:HPK) has efficiently refinanced its debt, pushing its subsequent debt maturity (based mostly on the springing maturity of its current credit score facility) out by round three years with a brand new $1.2 billion time period mortgage.

This offers HighPeak some respiratory room, though at a value. The time period mortgage comes with an rate of interest that’s shut to three% greater than HighPeak’s current debt. As effectively, there are numerous restrictions across the variety of energetic rigs that HighPeak can have, so it would most likely see its manufacturing decline not less than a bit in early to mid 2024.

The rig restrictions do get pleasure from forcing HighPeak to spend much less on capex and concentrate on producing extra free money movement, which it ought to have the ability to do decently with $80s oil.

I consider HighPeak is roughly pretty priced for long-term $80 oil now, though I estimate its worth at round $14 per share with long-term $75 oil. That is up barely from my earlier estimate of HighPeak’s worth, on account of improved near-term oil costs plus a extra steady monetary scenario.

Debt Refinancing

HighPeak efficiently refinanced its debt by getting into right into a time period mortgage settlement with a $1.2 billion dedication capability. This time period mortgage matures in September 2026 and carries an rate of interest of SOFR + 7.5%. The time period mortgage has a first-lien safety curiosity in considerably all of HighPeak’s belongings.

With SOFR at round 5.3%, the time period mortgage’s present rate of interest could be 12.8%, which is kind of excessive for first-lien debt.

HighPeak is utilizing the proceeds from the time period mortgage to repay its 10% unsecured notes due February 2024, its 10.625% unsecured notes due November 2024 and its current credit score facility borrowings (maturing in June 2024, however with a springing maturity to October 2023).

On the finish of Q2 2023, HighPeak had $970 million in internet debt, though with no working capital deficit its internet debt could be nearer to $1.25 billion. Proforma for its July fairness providing, its internet debt with no working capital deficit could be roughly $1.1 billion.

HighPeak will doubtless proceed to hold not less than some working capital deficit and it talked about that it’s now producing constructive free money movement, so its $1.2 billion time period mortgage ought to give it enough (albeit restricted) liquidity, provided that the time period mortgage additionally imposes restrictions on what number of energetic drilling rigs it may have.

HighPeak can also be allowed to enter into a brilliant senior revolving credit score facility for as much as $100 million.

Drilling Restrictions

HighPeak talked about that it was including a 3rd drilling rig to reap the benefits of sturdy oil costs, however it would quickly (in 2024) be restricted to not more than two drilling rigs (outdoors of obligation wells) so long as its internet leverage is 1.0x or greater. If its internet leverage is between 0.75x to 1.0x, then it’s allowed to have three drilling rigs.

At present strip, HighPeak appears more likely to be restricted to 2 drilling rigs into mid-to-late 2024, however ought to get its internet leverage under 1.0x throughout 2H 2024. It could possibly get its internet leverage under 0.75x by the tip of 2024 at present strip, probably permitting it to extend its rig rely above three.

Potential 2024 Outlook

I’ve modeled a situation under the place HighPeak runs a two-rig drilling program via most of 2024 and spends $600 million on capex. On this situation HighPeak will doubtless see its manufacturing fall a bit from its 2023 exit charge (with steerage midpoint at the moment at 57,000 BOEPD).

Thus I’m at the moment modeling HighPeak’s 2024 manufacturing at 53,000 BOEPD (83% oil) with the assumption that it’s going to exit 2024 with round 50,000 BOEPD in manufacturing if it continues with a two-rig drilling program. Nonetheless, there may be vital uncertainty round HighPeak’s manufacturing ranges on account of its massive variety of latest wells and at the moment excessive base decline charge.

On the present strip of $82 WTI oil for 2024, HighPeak might generate $1.382 billion in oil and gasoline revenues earlier than hedges.

HighPeak’s 2024 hedges (from the tip of Q2 2023) have roughly adverse $14 million in worth. This does not embrace the brand new hedges that HighPeak will add quickly (if it hasn’t performed so already).

As proven above, HighPeak is now required (as a part of its time period mortgage settlement) to enter into oil hedges protecting not less than 27,000 barrels per day in oil manufacturing for the twelve month interval ending September 2024, with a ground worth that’s not less than 85% of strip.

Sort

Barrels/Mcf

$ Per Barrel/Mcf

$ Million

Oil

16,056,350

$81.50

$1,309

NGLs

1,741,050

$24.75

$43

Pure Fuel

9,285,600

$2.40

$22

Hedge Worth

-$14

Complete

$1,360

I’m modeling HighPeak’s 2024 lease working bills (together with workover expense) at $9.00 per BOE at 53,000 BOEPD in common manufacturing. HighPeak’s money curiosity prices might find yourself at round $146 million if it solely makes its $30 million per quarter in scheduled repayments. It could possibly cut back its curiosity prices with accelerated repayments.

Bills

$ Million

Lease Working Expense And Workovers

$174

Manufacturing And Advert Valorem Taxes

$76

Money G&A

$10

Money Curiosity

$146

Capital Expenditures

$600

Complete Expenditures

$1,006

This leads to a projection of $354 million in 2024 free money movement at low-$80s WTI oil and modest manufacturing declines.

HighPeak additionally has $13 million in annual dividend funds at its present quarterly dividend of $0.025 per share. It’s also required to make $120 million per 12 months in time period mortgage repayments.

Notice Refinancing And Estimated Valuation

HighPeak estimated that its proved developed reserves had a PV-10 of $2.81 billion at $80 oil. This was based mostly on estimated reserves from the start of August 2023.

HighPeak’s Reserves (highpeakenergy.com)

At $16.75 per share, HighPeak’s market cap could be roughly $2.5 billion assuming that its excellent choices and warrants had been exercised. It will have roughly 149 million shares excellent together with $850 million in internet debt. This $3.35 billion mixed complete is almost 1.2x HighPeak’s proved developed PV-10 at $80 oil. At $80s oil, HighPeak ought to have the ability to improve its proved developed reserves whereas additionally decreasing its debt.

I beforehand estimated HighPeak’s worth at $13 per share in a long-term $75 oil and $3.75 gasoline situation. I’ve elevated its estimated worth to $14 per share with long-term (after 2024) $75 WTI oil. This improve is because of greater near-term oil costs in addition to the improved stability of HighPeak’s funds.

At long-term $80 WTI oil as a substitute, I might take into account HighPeak’s present share worth of round $16.75 per share to be roughly honest. HighPeak’s insiders have lately bought shares at round its present share worth, however I are inclined to take a extra conservative view in direction of longer-term oil costs.

Conclusion

HighPeak Power efficiently refinanced its debt and it now has three years till its new $1.2 billion time period mortgage matures. It’s paying near 13% curiosity on that time period mortgage although, and can also be required to make $120 million per 12 months in time period mortgage repayments.

At $80s oil, HighPeak ought to have the ability to make vital progress in decreasing its internet debt and leverage although. It will likely be restricted by way of the variety of energetic drilling rigs it may have till it reduces its leverage under 0.75x.

I consider that HighPeak is at the moment pretty valued for a long-term $80 WTI oil situation and is value roughly $14 per share at long-term $75 WTI oil as a substitute.

Client confidence within the U.Ok. improved in September to essentially the most optimistic stage in additional than a 12 months and a half, a sign of bettering prospects for the nation’s financial system and that pressures on family spending might be easing, based on a survey revealed Friday.

Confidence amongst British shoppers rose 4 factors to minus 21 this month, the best studying since January 2022, based on an index compiled by consumer-research agency GfK.

A extra “prolonged” restoration for the patron and retail markets might imply challenges for Zebra Applied sciences Corp. shares, in accordance with Morgan Stanley.

Analyst Meta Marshall downgraded shares of Zebra ZBRA, which makes cellular computer systems, barcode scanners, machine readers and different applied sciences for the retail business, to underweight from equal weight in a Wednesday notice to shoppers.