fotostorm

Is a This fall pothole on the street forward? That is what Goldman Sachs’ David Kostin asserts. Earlier this month, he and the remainder of the GS economics group outlined a trio of dangers that might derail what has been a 12 months of surprisingly robust home actual GDP progress.

Together with a looming authorities shutdown and the continuing UAW strikes, the resumption of scholar mortgage repayments might crimp budgets and damage discretionary spending.

May Uber Applied sciences (NYSE:UBER) be in danger? With Uber Eats having a excessive proportion of month-to-month lively customers in the important thing 25- to 44-year-old cohort, some analysts imagine draw back dangers are on the horizon.

I reiterate my purchase ranking on Uber, nonetheless. I see a sturdy longer-term earnings story enjoying out whereas worth motion has completed the whole lot it ought to since I initiated protection on the inventory earlier this 12 months.

This fall Dangers Forward

Goldman Sachs

In response to Financial institution of America World Analysis, UBER is a mobility platform that providers 72 international locations, 750+ ridesharing markets, and 500+ Eats markets, and almost half of Core Platform Income is generated outdoors of the U.S. The corporate now has over 130 million month-to-month prospects with revenues generated from Mobility, Supply, and Freight providers.

The San Francisco-based $91.1 billion market cap Passenger Floor Transportation firm throughout the Industrials sector has unfavourable trailing 12-month GAAP earnings and doesn’t pay a dividend. Forward of earnings subsequent month, the inventory contains a reasonable implied volatility proportion of 35% whereas its quick curiosity is low at simply 2.4%.

Again in early Might, the corporate reported Q2 GAAP EPS of $0.18 which topped analysts’ estimates of a 1-cent per-share loss. Income was properly larger on a year-on-year foundation, +14%, at $9.2 billion, although that fell in need of what Wall Avenue projected. With Gross Bookings up 16% from year-ago ranges and an 18% rise on a constant-currency foundation, the general progress trajectory nonetheless seems strong.

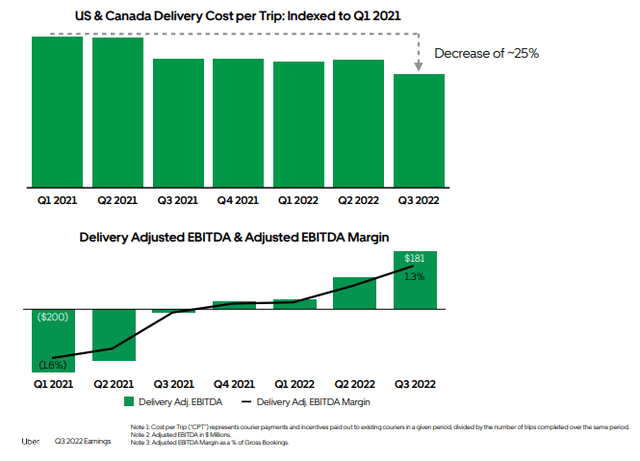

Impressively, UBER reported file quarterly free money circulation of $1.1 billion. The agency’s increasing EBITDA margin and excessive revenue flow-through come as the buyer sees some weak point, however Uber’s earnings come largely from its stable Mobility and Promoting segments – long-form video advertisements noticed a big increase from the identical quarter final 12 months.

Supply Margins on the Rise

Uber IR

Key dangers embody the potential for a number of compression as a result of macro components (weaker shopper and company advert spending), slower progress in gross sales and customers from competitors, rising competitors from self-driving know-how corporations, and the hostile impacts of recent laws.

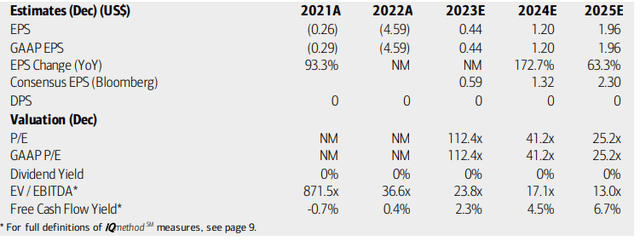

On valuation, analysts at BofA see earnings persevering with the pattern nicely into constructive territory. Out-year EPS is seen north of $1 whereas the 2025 consensus estimate, on the newest verify, is $1.79 per In search of Alpha. This fast-growing firm just isn’t anticipated to pay dividends any time quickly, however the agency is free money circulation constructive. With earnings a number of anticipated to dip into the mid-20s with bottom-line progress, the PEG ratio is engaging trying forward.

Uber: Earnings, Valuation, Free Money Stream Forecasts

BofA World Analysis

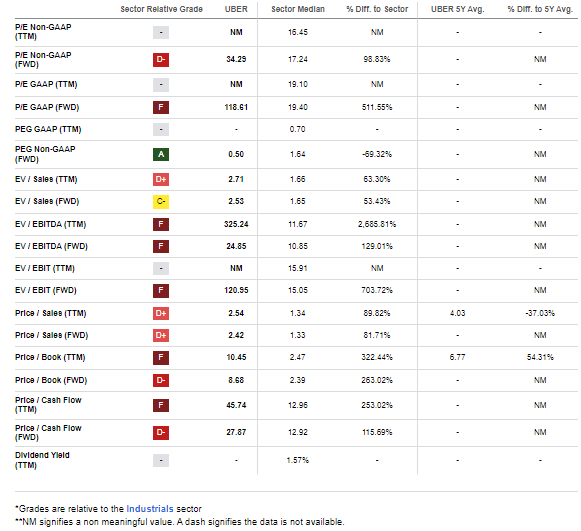

UBER’s ahead PEG ratio is presently simply 0.5, incomes it an A ranking there (although the general valuation ranking is only a D). Following the stable Q2, I proceed to say {that a} 25x P/E on $2 of future EPS is a really affordable valuation. On a ahead gross sales foundation, the inventory is only a 2.Four a number of – nicely beneath that of rival Instacart Maplebear (CART) that simply went public. The trailing 12-month price-to-sales ratio is at a 37% low cost to its 5-year common, too.

UBER: Poor Valuation Grades, However Banking on Progress

In search of Alpha

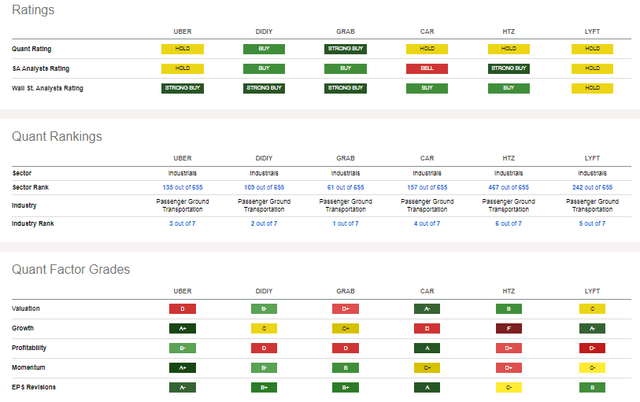

In comparison with its friends, Uber has the whole lot you need apart from worth earnings multiples. However I don’t count on this quick grower to be “worth” within the coming years. I do contend that it’s a GARP play, although, and its robust profitability and upside EPS revisions again up that narrative. Amongst its opponents, Uber additionally has the very best momentum proper now, although I’ll spotlight some near-term dangers to cost motion.

Competitor Evaluation

In search of Alpha

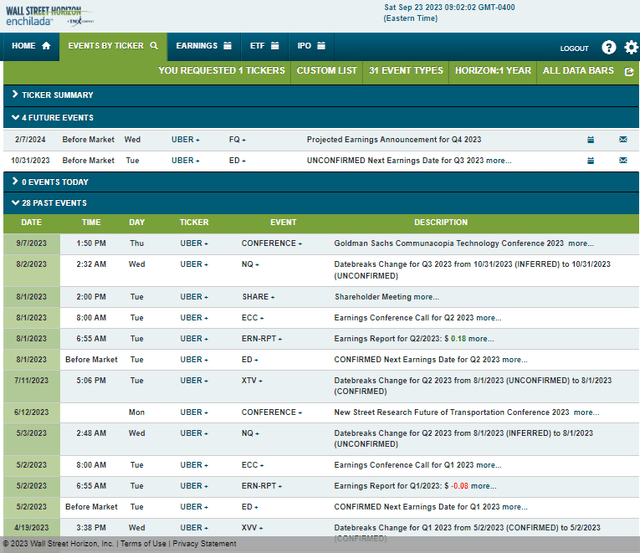

Wanting forward, company occasion knowledge offered by Wall Avenue Horizon present an unconfirmed Q3 2023 earnings date of Tuesday, October 31 BMO. No different volatility catalysts are seen on the calendar.

Company Occasion Threat Calendar

Wall Avenue Horizon

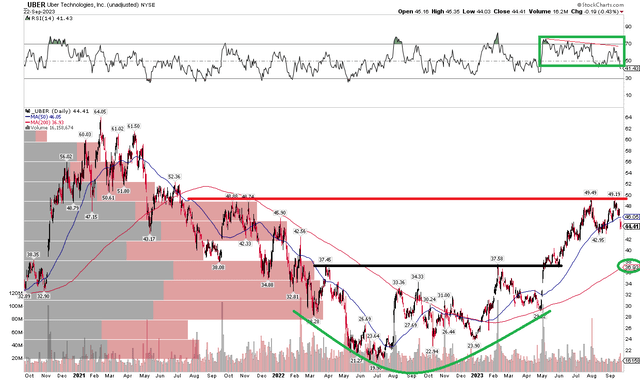

The Technical Take

As talked about earlier, UBER has completed the whole lot it has speculated to do since Q2, for my part. Discover within the chart beneath that shares almost touched $50 and have since pulled again after printing a near-term double high. Additionally check out the RSI momentum gauge on the high of the graph – whereas it stays in a bullish vary, there was some modest bearish divergence as worth rose in the summertime. I famous that in my preliminary evaluation earlier this 12 months.

I see near-term assist round $42, so that will be a very good place so as to add to the place. Longer-term assist is seen on the rounded-bottom breakout level within the $37 to $38 zone. Total, with a rising long-term 200-day shifting common and better highs & larger lows going all the best way again to June of 2022, the bulls seem in management. I proceed to see $50 as resistance, however a breakout above that degree would portent a attainable rise to $58 based mostly on this rising $eight vary that’s now a couple of months previous.

Large image, the trip just isn’t all the time easy, however I see Uber’s technical view as constructive.

UBER: $50 Stays Resistance, $42 Close to-Time period Help

Stockcharts.com

The Backside Line

It’s regular as she rides with Uber. Shares rallied to resistance and have pulled again, providing buyers an opportunity to hop in on this high-growth firm.