Pour one out for the beleaguered economists, who for as soon as acquired an vital indicator, the buyer value index, proper on the nostril, after CPI fell 0.1% in December, whereas core costs rose 0.3%.

“The 2021 surge in sturdy items demand normalized, and the ensuing collapse in sturdy items value inflation was stunningly quick,” says Paul Donovan, chief economist of UBS International Wealth Administration.

“The commodity wave of inflation is fading, and that leaves the revenue margin growth in focus,” he provides. What a great time for earnings season to be upon us, and what have you learnt, it’s, kicking off with the banking sector on Friday earlier than broadening out subsequent week.

Strategists at Goldman Sachs have a brand new observe out, saying that the market is pricing in a tender touchdown despite the fact that the development of earnings revisions factors to a tough touchdown.

They’re not that optimistic — even within the soft-landing situation, the staff led by David Kostin say the S&P 500 SPX will finish the yr proper round present ranges, at 4,000. However they establish 46 shares that might profit — worthwhile, cyclical firms which can be buying and selling at price-to-earnings valuations beneath their 10-year median, amongst different elements.

One title jumps out: Tesla TSLA, which trades at 22 occasions ahead earnings versus the 10-year median of 117 occasions. However the different 45 names are much less flashy, starting from Capital One COF and Carlyle Group CG, to a bunch of industrials together with 3M MMM, Parker-Hannifan PH and Otis Worldwide OTIS. As an entire, these sometimes $10 billion firms are buying and selling at 12 occasions earnings, versus 17 occasions often.

Within the laborious touchdown situation, S&P 500 revenue margins would shrink by 125 foundation factors, to 10.9% — about consistent with the median peak-to-trough decline through the eight recessions since 1970, which has been 132 foundation factors. Consensus expectations are for a 26 basis-point margin decline.

The Goldman staff even have a 36 inventory display screen for a tough touchdown — worthwhile firms in defensive industries with a constructive dividend yield. They’re sometimes meals, beverage and tobacco firms in addition to software program and providers firms — together with Costco Wholesale COST, Kroger KR, Altria MO, Tyson Meals TSN, Microsoft MSFT, MasterCard MA and Visa V. As an entire, these $37 billion firms are buying and selling at 22 occasions earnings vs. a historic 24 occasions.

The market

After a 2.3% advance for the S&P 500 SPX over the past three classes, U.S. inventory futures ES00 NQ00 had been a bit weaker.

The yield on the Japanese 10-year bond BX:TMBMKJP-10Y exceeded 0.5%, the Financial institution of Japan’s yield cap, forward of subsequent week’s charge resolution , prompting a second day of aggressive bond purchases from the central financial institution.

For extra market updates plus actionable commerce concepts for shares, choices and crypto, subscribe to MarketDiem by Investor’s Enterprise Every day.

The thrill

Fourth-quarter earnings had been rolling out from Financial institution of America BAC, JPMorgan Chase JPM, Citigroup C and Wells Fargo WFC, and out of doors of banks, Delta Air Strains DAL, BlackRock BLK and UnitedHealth UNH.

JPMorgan shares slumped after forecast-beating earnings, although funding financial institution income got here in gentle of estimates. Delta shares additionally declined after topping earnings estimates.

Tesla TSLA minimize costs of Mannequin Three and Mannequin Y autos within the U.S. and elsewhere by as much as 20%.

Virgin Galactic SPCE surged after saying it’s on monitor to launch space-tourism flights within the second quarter.

Apple AAPL says CEO Tim Prepare dinner requested, and obtained, a pay minimize after investor criticism.

The College of Michigan’s shopper sentiment index is due at 10 a.m. Japanese, and Minneapolis Fed President Neel Kashkari and Philadelphia Fed President Patrick Harker are as a result of converse.

Tyler Winklevoss stated fees by the Securities and Alternate Fee led to Gemini Belief for allegedly providing unregistered securities had been “tremendous lame” because it seeks to unfreeze $900 million in investor property.

Better of the net

There’s a bull market in swearing on company earnings calls.

The West is now making ready to ship tanks to Ukraine in what might be one other escalation of its battle with Russia, which on Friday claimed victory within the japanese city of Soledar.

A glance again at images of Lisa Marie Presley, who died at age 54.

High tickers

Right here had been essentially the most energetic stock-market tickers as of 6 a.m. Japanese.

Ticker

Safety title

BBBY

Mattress Tub & Past

TSLA

Tesla

GME

GameStop

AMC

AMC Leisure

MULN

Mullen Automotive

NIO

Nio

APE

AMC Leisure preferreds

AAPL

Apple

SPCE

Virgin Galactic

AMZN

Amazon.com

Random reads

Like a scene out of Stranger Issues — there’s uproar after new restrictions on the Hasbro HAS sport Dungeons & Dragons.

Beginning subsequent month, Starbucks SBUX rewards can be much less beneficiant for many gadgets, although iced espresso can be simpler to get.

Must Know begins early and is up to date till the opening bell, however join right here to get it delivered as soon as to your e-mail field. The emailed model can be despatched out at about 7:30 a.m. Japanese.

Take heed to the Finest New Concepts in Cash podcast with MarketWatch reporter Charles Passy and economist Stephanie Kelton.

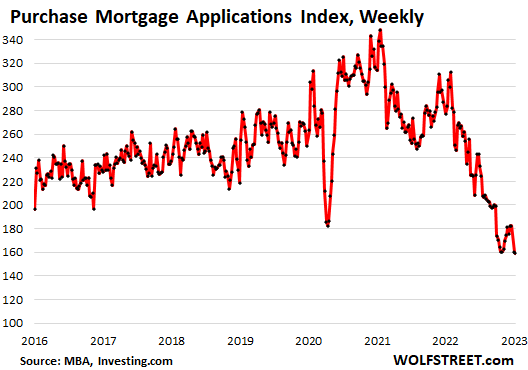

Mortgage purposes to buy a house are a forward-looking indicator of the place dwelling gross sales quantity might be. Current dwelling gross sales that closed in November already plunged by 35% year-over-year, the 16th month in a row of year-over-year declines, making for a historic plunge. And mortgage purposes went within the incorrect route from there, regardless of the dip in mortgage charges.

Purposes for mortgages to buy a house fell to the bottom degree for the reason that Christmas week of 2014, and past the lows of 2014, we have now to return all the best way to 1995, in keeping with knowledge from the Mortgage Bankers Affiliation right this moment.

In comparison with a yr in the past, buy mortgage purposes have plunged by 44%. Even throughout Housing Bust 1, mortgage purposes did not plunge that a lot yr over yr.

MBA, Investing.com

That little dip in mortgage charges had no impression. This drop in mortgage purposes got here regardless of the dip in mortgage charges that began in mid-November from the 7.1% vary and hit a low level in mid-December at 6.28%. Within the newest reporting week, the common 30-year mounted price was at 6.42%, in keeping with the Mortgage Bankers Affiliation right this moment.

The drop in mortgage purposes signifies that it would not actually matter to the quantity of dwelling purchases whether or not the 30-year mounted price is 6.3% or 7.1%. The distinction is simply beauty. The present dwelling costs – although they’ve come down in lots of markets, and have come down exhausting in some markets – are nonetheless merely means too excessive.

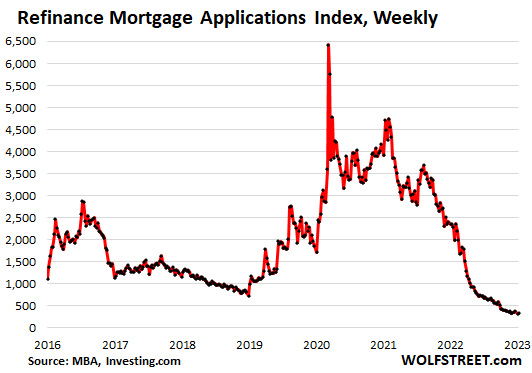

Refinance mortgage quantity has died: Purposes to refinance a mortgage have collapsed by 86% from a yr in the past, regardless of the invisibly small uptick within the newest week. Since October, refinance purposes have hovered on the lowest ranges for the reason that yr 2000. And this is sensible as a result of hardly anybody could be refinancing a 3% or 4% mortgage with a 6% or 7% mortgage, besides when underneath duress to extract money.

MBA, Investing.com

Mortgage lender woes

Mortgage lenders, whose revenues have collapsed as mortgage purposes quantity has collapsed, have spent the final 12 months shedding folks and shutting down divisions. Some smaller operations have shut down completely.

Wells Fargo (WFC), as soon as the biggest total mortgage lender after which the biggest financial institution mortgage lender, is the newest to make the information with its extra efforts to step again from the mortgage market, on prime of the steps it had taken in 2022.

CNBC reported on Tuesday that it had “realized” that the financial institution will now re-focus its mortgage enterprise solely on its current financial institution and wealth-management clients, and debtors in minority communities; that it’s shutting down its enterprise that buys mortgages that had been originated by third-party lenders; and that it’s “considerably” lowering its mortgage-servicing portfolio by asset gross sales. All this may entail a brand new spherical of layoffs, on prime of the layoffs in its mortgage enterprise that began in April final yr.

Wells Fargo solely had about 18,000 mortgages in its retail origination pipeline within the early weeks of the fourth quarter, which was down by as a lot as 90% from a yr earlier, in keeping with CNBC, citing folks with information of the corporate’s figures.

Wells Fargo shares are down 29% from their latest excessive in February 2022, and down 36% from their all-time excessive in January 2018.

The mortgage lenders that surpassed Wells Fargo a number of years in the past are non-banks – they had been aggressive in getting the mortgage enterprise through the Simple Cash period, then acquired crushed, and in 2022 made it into my pantheon of Imploded Shares. They’ve all shed giant numbers of staff, and a few have shut down whole models so as to survive.

Their shares have collapsed from their highs:

Rocket Firms (owns Quicken Loans): -81%

United Wholesale Mortgage (owns United Shore Monetary): -73%

LoanDepot: -94%

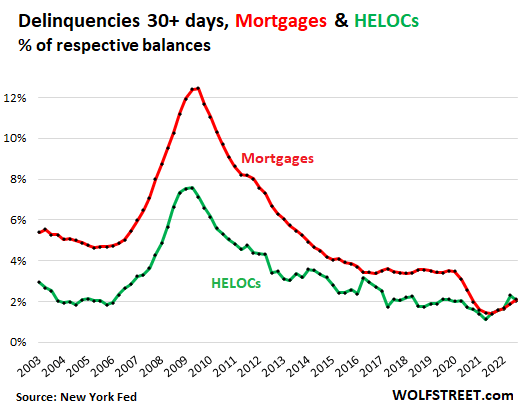

However mortgage delinquencies and foreclosures are nonetheless close to file lows.

What the true property and mortgage industries are lamenting is the plunge within the quantity of dwelling purchases and the plunge within the quantity of mortgage originations, which have brought about their revenues to break down.

The problem will not be the credit score high quality of the prevailing mortgages. Not less than not but; that part could come later if and when unemployment reaches excessive ranges, which is simply not taking place but regardless of the layoffs in tech, social media, and finance. Mortgage and HELOC delinquencies, although they’ve ticked up from file lows through the pandemic, stay very low.

The HELOC 30-day-plus delinquency price ticked right down to 2.0% in Q3, 2022, according to the lows through the Good Occasions, in keeping with knowledge from the NY Fed (inexperienced line).

The mortgage 30-day-plus delinquency price ticked as much as 2.1% (crimson line), nonetheless far decrease than earlier than the pandemic.

New York Fed

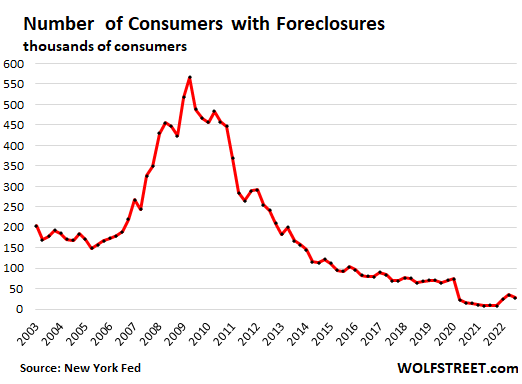

Foreclosures ticked down once more in Q3 to only 28,500 mortgages with foreclosures, and stay properly under the quantity through the Good Occasions earlier than the pandemic when there have been about 70,000 mortgages with foreclosures:

New York Fed

Authentic Submit

Editor’s Observe: The abstract bullets for this text had been chosen by In search of Alpha editors.

JD Sports activities Trend PLC stated Wednesday that it expects to report fiscal 2023 adjusted pretax revenue towards the highest finish of market expectations after it booked a robust efficiency through the Christmas interval.

The sports-and-fashion retailer JD, +4.65% stated that for the fiscal 12 months ending Jan. 28 it expects to report adjusted pretax revenue in a spread from 933 million to 985 million kilos ($1.13 billion-$1.20 billion).

Whole income development for the 22 weeks to Dec. 31 was greater than 10%, in contrast with development of 5% for the primary half, it stated. Efficiency by Christmas was significantly spectacular, it stated, with complete income development over the six-week interval to Dec. 31 of greater than 20%.

North America recovered strongly, delivering development of greater than 20% by the second half so far, it stated.

For fiscal 2024, the corporate sees adjusted pretax revenue of simply over GBP1 billion.

Targa Sources Corp. (NYSE:TRGP) is a pure gasoline liquids-focused midstream company that primarily operates within the state of Texas. The midstream sector basically has lengthy been among the many favourite areas for income-focused buyers to be attributable to the truth that most of those corporations take pleasure in remarkably secure money flows and excessive dividend yields. Targa Sources is one thing of an exception to this because it does have money movement stability nevertheless it falls considerably quick when it comes to yield. In truth, the corporate solely yields 1.92% on the present value, which is because of a dividend in the reduction of in 2020 that was then partially reversed final yr. The corporate will probably enhance its dividend at a while sooner or later, which we’ll see over the course of this text. Though Targa Sources doesn’t benefit from the excessive yield that we sometimes wish to see right here at Vitality Income in Dividends, it has prior to now and will as soon as once more. Because of this I proceed to debate this firm on my service. General, there are fairly a couple of causes to speculate on this firm at the moment because it has made nice progress in overcoming a couple of of the issues that it had in recent times and is thus positioning itself pretty nicely for the longer term.

About Targa Sources

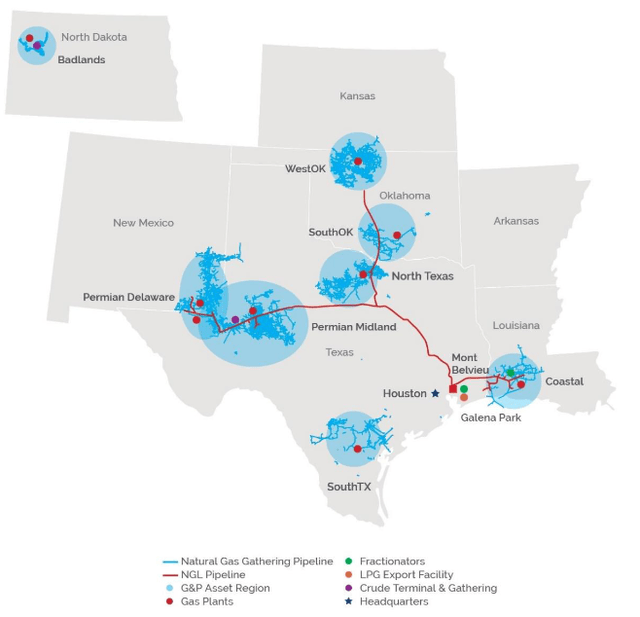

As acknowledged within the introduction, Targa Sources is a pure gasoline liquids-focused midstream company that primarily operates within the state of Texas, though it does have some operations in North Dakota’s Williston Basin:

Targa Sources

In contrast to lots of its friends, although, we will see that the corporate’s pipeline infrastructure is pretty small. This can be a bit deceptive nevertheless as Targa Sources truly has a reasonably substantial gathering and processing infrastructure community. A gathering pipeline is considerably completely different from the big long-haul pipelines that carry sources throughout a state or a rustic. Moderately, these pipelines are pretty quick and low-capacity pipelines that merely seize the sources from the nicely that extracts them from the bottom. The pipeline will then take the sources to the primary cease on their journey, which is normally both a a lot bigger long-haul pipeline or a processing facility. Targa Sources does have a reasonably substantial pure gasoline processing capability as it’s able to dealing with a complete of 11 billion cubic ft of pure gasoline per day throughout its 53 processing vegetation. The processing of pure gasoline is essential as a result of pure gasoline accommodates various impurities and pollution when it’s faraway from the bottom, comparable to water and sulfur. The processing plant removes these impurities and converts the pure gasoline right into a state that can be utilized by the tip consumer. The corporate additionally owns 960,000 barrels per day of pure gasoline liquids fractionation capability. A pure gasoline liquids fractionator splits the sources into the varied pure gasoline liquids that we use in our on a regular basis lives, comparable to propane, butane, and ethane. General, then, Targa Sources is a reasonably main participant within the midstream house, despite the fact that it doesn’t have substantial long-haul pipeline belongings.

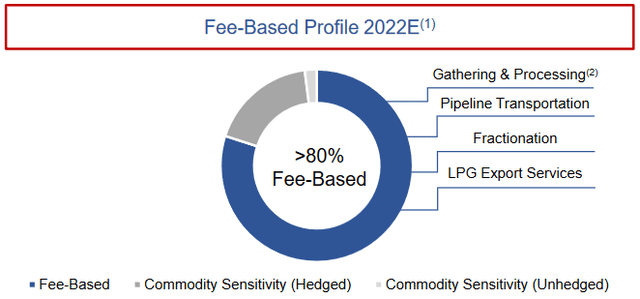

Within the introduction, I acknowledged that Targa Sources tends to take pleasure in remarkably secure money flows no matter situations within the broader economic system. That is as a result of enterprise mannequin that the corporate makes use of. Briefly, Targa Sources enters into long-term (normally 5 to 10 years in size) contracts with its clients. Underneath these contracts, the shoppers ship sources by way of Targa Sources’ infrastructure and compensate the corporate primarily based on the amount of sources dealt with. This offers the corporate with a shocking quantity of insulation in opposition to fluctuations in commodity costs. At this level, some readers may level out that upstream useful resource producers have a tendency to scale back their output when power costs lower. This occurred again in 2020 when the COVID-19 pandemic broke out and brought on the demand for crude oil to plummet. Though Targa Sources doesn’t personal any crude oil infrastructure, pure gasoline and pure gasoline liquids are sometimes produced by the identical wells so the corporate would nonetheless be affected. Thankfully, the corporate has a strategy to shield itself in opposition to this. The contracts that it has with its clients comprise what are often called minimal quantity commitments, which specify a sure minimal quantity of sources that the client should ship by way of Targa Sources’ infrastructure or pay for anyway. Thus, it has a sure portion of its money movement that’s typically unaffected by both power costs or useful resource manufacturing. In truth, 80% of the corporate’s working margin (a proxy for working revenue) comes from these recession-resistant contracts:

Targa Sources

That is one thing that’s sure to be enticing proper now as practically all economists agree that the American economic system will enter right into a recession someday in 2023. One of many traits of recessions is that the demand for power sources declines, which might affect the output of upstream producers a lot because it did again in 2020. The truth that greater than 80% of Targa Sources’ money flows are protected by this offers an excessive amount of assist for the corporate’s dividend and by extension our incomes.

We will see proof of this common stability just by wanting on the firm’s working money flows over time. Right here they’re over the previous eleven quarters:

Searching for Alpha

This offers even additional proof that the corporate ought to have the ability to deal with any imminent recession with ease. In any case, whereas its money flows did decline considerably in 2020, they nonetheless remained rather more secure than is likely to be anticipated contemplating what occurred to power costs throughout that yr. It’s all however sure that any recession that happens in 2023 won’t be practically as extreme as it is extremely unlikely that the federal government will as soon as once more try to lock us all down at dwelling and forbid us from pointless touring. Thus, power demand shouldn’t drop as a lot and we’ll probably not see practically as large of a shock to the business.

Progress Prospects

Naturally, as buyers, we wish to see greater than easy stability. We wish to see development. Thankfully, Targa Sources is sort of well-positioned to ship on this space. As midstream infrastructure comparable to pure gasoline gathering pipelines, processing vegetation, and fractionators solely have a restricted amount of sources that they deal with, and the corporate’s money movement is determined by the amount of sources that transfer by way of its infrastructure, the traditional method for Targa Sources to generate development is to assemble new infrastructure. That is precisely what the corporate is doing, though it admittedly doesn’t have as many development tasks within the works as some friends comparable to Enbridge (ENB) or Kinder Morgan (KMI). One of many firm’s main tasks is the Daytona NGL Pipeline. The Daytona NGL Pipeline was introduced in November of 2022 and has an estimated value of $650 million. This undertaking was initially envisioned as a three way partnership with Blackstone Vitality Companions, though Targa Sources purchased out Blackstone’s stake final week. The Daytona NGL Pipeline is meant as an growth to the Grand Prix NGL system that constitutes one of many largest pure gasoline liquids pipeline networks in Texas. The Grand Prix NGL system is able to carrying 550,000 barrels of pure gasoline liquids per day however the Daytona NGL Pipeline is considerably lower than that as a result of it’s not the one pipeline that’s feeding all the system. Throughout its third-quarter convention name, Targa Sources acknowledged that the Daytona NGL Pipeline can be able to carrying 400,000 barrels of pure gasoline liquids per day when it begins working, though the corporate will have the ability to increase its capability if wanted. This form of expandable capability is sort of widespread because it helps to save lots of on development prices and future-proofs the undertaking. Clearly, these are issues that we should always respect as buyers.

Targa Sources can be working to increase its pure gasoline processing capability. Additionally in November 2022, the corporate introduced that it’ll start development of a brand new pure gasoline processing plant to serve the Permian Basin. This new plant, dubbed Wildcat II, can be able to processing roughly 275 million cubic ft of pure gasoline when it begins operation in early 2024. Because the Daytona NGL Pipeline is predicted to come back on-line in late 2024, Targa Sources will thus be bringing a couple of new tasks on-line throughout that yr.

The great factor about these tasks is that Targa Sources has already obtained contracts for his or her use from its clients. This serves two functions, each of that are helpful for the corporate. The primary of those functions is clearly that we could be assured that the corporate is just not spending an infinite amount of cash to assemble infrastructure that no person desires to make use of. As well as, we could be sure that every of those tasks will start producing cash as quickly as they change into operational in 2024 so we will anticipate regular development over the course of that yr from these two tasks coming on-line. The second function is that the corporate is aware of prematurely precisely how worthwhile the tasks can be so it is aware of that every undertaking will have the ability to generate a adequate return to justify the funding. Sadly, Targa Sources has not specified precisely how worthwhile they are going to be so we can’t carry out an in-depth monetary evaluation presently. Kinder Morgan’s tasks normally pay for themselves in 4 years whereas The Williams Corporations (WMB) has a few six-year payback so it’s probably that Targa Sources’ tasks are in that very same ballpark however that is on no account sure. Regardless, we could be sure that they may present a really noticeable enhance to the corporate’s money movement.

Monetary Issues

It’s at all times essential that we have a look at the way in which that an organization is financing itself earlier than we make an funding in it. It’s because debt is a riskier strategy to finance an organization than fairness as a result of debt should be repaid at maturity. As few corporations have adequate money readily available to fully repay their debt because it matures, that is sometimes completed by issuing new debt and utilizing the proceeds to repay the maturing debt. This could trigger an organization’s curiosity bills to extend following the rollover relying on the situations available in the market. Along with this, an organization should make common funds on its debt whether it is to stay solvent. Thus, an occasion that causes an organization’s money flows to say no could push it into monetary misery if it has an excessive amount of debt. Though Targa Sources has remarkably secure money flows, we should always not ignore this danger as bankruptcies have occurred within the midstream sector.

One metric that we will use to guage an organization’s monetary construction is the online debt-to-equity ratio. This ratio tells us the diploma to which an organization is financing its operations with debt versus wholly-owned funds. As well as, the ratio tells us how nicely the corporate’s fairness will cowl its debt obligations within the occasion of a chapter or liquidation occasion, which is arguably extra vital.

As of September 30, 2022, Targa Sources had a web debt of $11.0646 billion in comparison with $4.7314 billion of shareholders’ fairness. This offers the corporate a web debt-to-equity ratio of two.34. At first look, this ratio appears extremely excessive for any firm however allow us to examine it to among the firm’s friends to get a greater thought of whether or not that is appropriate:

Firm

Web Debt-to-Fairness

Targa Sources

2.34

Kinder Morgan

0.98

The Williams Corporations

1.62

MPLX (MPLX)

1.50

Crestwood Fairness Companions (CEQP)

1.51

As we will clearly see, Targa Sources is relying significantly extra on debt to finance its operations than any of its friends. This can be a clear signal that the corporate is utilizing an excessive amount of leverage and thus could have larger dangers of monetary misery than lots of its friends. That is, actually, one of many considerations that we now have had with respect to this firm. I’ve mentioned this in lots of earlier articles right here at Vitality Income in Dividends.

In the end although, the corporate’s capacity to hold its debt is extra vital than the sheer quantity of debt. The same old method that we choose that is by wanting on the leverage ratio, which is also called the online debt-to-adjusted EBITDA ratio. This ratio basically tells us what number of years it is going to take for the corporate to fully repay its debt if it had been to commit all of its pre-tax money movement to that activity. Within the third quarter of 2022, Targa Sources reported an adjusted EBITDA of $768.6 million, which works out to $3.0744 billion yearly. This offers the corporate a leverage ratio of three.60x, which is sort of cheap. As I’ve identified in varied earlier articles, analysts typically contemplate something underneath 5.0x to be cheap however I’m extra conservative and wish to see this ratio underneath 4.0x in an effort to add a margin of security to the funding. All the really useful corporations right here at Vitality Income in Dividends are nicely underneath this 4.0x threshold however traditionally Targa Sources has not been. The corporate now seems to be, which is definitely good to see. The most important cause why Targa Sources minimize its dividend again in 2020 was to repay its debt and it has seemingly loved an excessive amount of success at this activity. That is due to this fact fairly good to see.

Dividend Evaluation

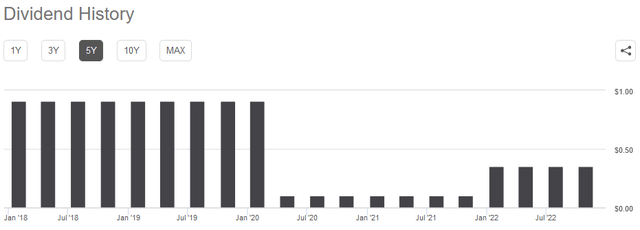

One of many largest the explanation why we spend money on midstream corporations is the excessive dividend yields that these corporations are inclined to pay out. Targa Sources is sadly a notable exception to this rule as the corporate solely yields 1.92% at its present value. It’s because the corporate minimize its dividend again in 2020 and, whereas it did enhance it in early 2022, it nonetheless stays nicely under its peak:

Searching for Alpha

Along with this, the corporate’s inventory has appreciated by 28.31% over the previous twelve months, which has additionally suppressed the yield considerably. The truth that the corporate did minimize its dividend in 2020 is more likely to be a little bit of a turn-off, particularly since there are various different midstream corporations that didn’t want to chop their payout. Nonetheless, you will need to remember that anybody buying the corporate’s shares at the moment will obtain the present dividend on the present yield and so does probably not want to fret in regards to the firm’s disappointing previous. Subsequently, the vital factor for our functions is how nicely the corporate can keep its present dividend. In any case, we don’t wish to discover ourselves the victims of one other dividend minimize since that would scale back our incomes and nearly definitely trigger the inventory value to say no.

The same old method that we choose a midstream firm’s capacity to pay its dividend is by its distributable money movement. Distributable money movement is a non-GAAP determine that theoretically tells us the amount of money that was generated by the corporate’s bizarre operations and is on the market to be distributed to the widespread stockholders. Within the third quarter of 2022, Targa Sources reported a distributable money movement of $594.9 million however solely paid $81.Zero million in dividends. This offers the corporate a distribution protection ratio of seven.34x, which is much above the 1.20x that analysts sometimes contemplate cheap and sustainable. Additionally it is nicely above the same old 1.30x that we wish to see from an organization that we’re invested in. This extremely excessive protection ratio is without doubt one of the the explanation why I prompt earlier on this article that Targa Sources could enhance its dividend in some unspecified time in the future since it could possibly clearly afford to and appears to have gotten its debt considerably underneath management. We should always total not have to fret in any respect a few minimize right here.

Conclusion

In conclusion, Targa Sources might definitely have potential regardless of now not being a high-yielding inventory. The corporate has made nice strides at addressing the debt considerations that we now have had in regards to the firm prior to now, though the debt-to-equity ratio is certainly nonetheless a bit excessive. The corporate additionally has some important development prospects which are more likely to play out over the following two years. Once we mix this with an actual probability of a dividend enhance, we will see some actual causes to buy the corporate at the moment.

Early in 2022 (Jan 3, 2022 to be actual, as you may see from the next chart), Apple (NASDAQ:AAPL) grew to become the primary firm to achieve a $3T market cap throughout intraday buying and selling. Then a variety of macroscopic headwinds introduced it again to the present $2T stage.

Supply: In search of Alpha information

The thesis right here is to clarify why I see it as solely a matter of time earlier than Apple’s market cap returns to $3T. And, very seemingly, this time it would do it with type and in addition on a extra everlasting foundation. The pullbacks had been largely brought on by macroscopic circumstances, not AAPL’s merchandise’ points. A few of the key points embrace the continuing supply-chain disruptions, the persistence of COVID-19 (particularly in China), excessive inflation, and unfavorable forex alternate charges. And I see all of those points to be solely short-term.

And the time for its market cap to climb again to $3T may be earlier than you assume. Its {hardware} stays vastly well-liked and gross sales in just about all classes set a file in FY 2022 regardless of all of the above challenges. For the 12 months, Apple set sale data for the flagship iPhone (up 9.7% YOY to $42.6 billion), its iconic Mac line of private computer systems (up 25% YOY, to $11.5 billion), and in addition wearables.

Moreover its conventional product traces, there are a minimum of two extra highly effective catalysts at work whilst we communicate: its transformation right into a service firm and its success with its personal chips. And we’ll element these instantly under.

Transformation from a {hardware} firm to a service firm

Many traders affiliate AAPL principally with {hardware} (iPhone, Mac, et al) just because it’s so vastly profitable with them. Nonetheless, the primary purpose I’m bullish on its long-term image is its transformation right into a service enterprise. Apple’s put in base of lively units set all-time highs in all of its main product divisions and geographic areas in 2022. And its services-related revenues are making up an more and more bigger portion of the entire gross sales as seen within the chart under. To wit, based on this Trefis evaluation, APPL’s Providers enterprise raked in a complete of $56B of revenues in FY 2020, which already is its second-largest section and contributed about 19.5% of its complete revenues. Trying ahead, this section is projected to nearly double to achieve gross sales of greater than $93B.

And I feel the projection is completely believable (and you may see the small print of the projection by following the hyperlink supplied above). AAPL’s immense set up base already laid the muse for the fast development in its service revenues, which get pleasure from larger margins and higher recurrence.

Supply: Trefis information

Strategic shift to its personal chips

One other very highly effective catalyst at work in my opinion entails AAPL’s strategic launch of its personal chip traces. Again in June 2022, AAPL unveiled the M2 chip, its next-generation chip following its M1 chip. The M2 chip is designed based mostly on the SOC idea (System on a Chip) and it is developed to be used in each the Macs and iPads product traces. The M2 chip design is vastly higher than its M1 chip and in addition the Intel chip it used to deploy as its CEO Tim Prepare dinner commented within the 2022 Q2 earnings report (barely edited and the emphases had been added by me):

Final month we introduced one other breakthrough with M1 Extremely, the world’s strongest chip for a private laptop. The unbelievable buyer response to our M1-powered Macs helped propel a 15% year-over-year enhance in income, regardless of provide constraints. We now have our strongest Mac lineup ever, with the addition of the solely new Mac Studio.

The M2 chip is extra energy environment friendly and computationally highly effective on the identical time. To wit, based on information from CPU Ninja, drawing the facility, the M2 integrates 25% extra transistors than the M1 (20 billion transistors in complete) and 50% quicker reminiscence velocity than M1 (as much as 100GB/s) reminiscence velocity. These developments are straight mirrored in its finish merchandise akin to battery life and spectacular multi-threaded efficiency in apps just like the Mac Studio Tim Prepare dinner talked about above. Take the battery life in an M2 Mac for instance. With M2 chips, it might probably last as long as 2x longer in comparison with earlier generations put in with Intel chips.

Supply: CPU Ninja information

Share buybacks are much more potent now

Lastly, AAPL’s aggressive share repurchases will add one other catalyst, monetary catalysts along with the above enterprise catalysts, to push its valuation again to $3T.

AAPL is a big purchaser of its personal shares lately as seen from the next chart. In 2014 when it first began its share repurchase program, its complete shares excellent stood at 23.5B shares (adjusted for its break up). And now it stands at 16.12B as seen, translating into a complete discount of virtually 1/3 (32.5% to be actual). Every AAPL shareholder now owns 1/Three extra of the corporate than in 2014.

Supply: In search of Alpha information

Trying ahead, AAPL’s tempo of repurchasing will very seemingly proceed, and its money movement definitely can assist it with no drawback. As its CFO Luca Maestri repeatedly talked about the Board’s dedication to share repurchases and AAPL’s plan to change into web money impartial over time. All instructed, in 2022, the board has approved an extra $90 billion for share repurchases within the years to return. And this large $90 billion repurchases solely grew to become stronger on the present compressed valuations as illustrated in my evaluation under.

The outcomes are my projected of the share buybacks within the subsequent few years, and my numbers are based mostly on a couple of easy assumptions as detailed in my earlier articles:

I assumed AAPL distributes the $90B as a continuing proportion of its working money movement, which seems to be 78%

I assumed that AAPL income develop at an 8% CAGR based onconsensus estimates.

Lastly, I additionally assumed a mean repurchase worth of 18.0x of its working money (which is about its present a number of as of this writing).

You may see that its complete shares rely would additional shrink by one other 19.8% within the subsequent 5 years. And every AAPL shareholder would personal ~20% of the corporate with out actually doing something. Lastly, you may see that its market cap would attain $3.0T someplace round 2026~2027.

Supply: Writer based mostly on In search of Alpha information

Dangers and remaining ideas

To reiterate, there’s certainly a variety of quick headwinds going through AAPL as aforementioned, together with supply-chain congestion, the COVID-19 pandemic, inflation, and in addition the attainable U.S. and even financial development slowdown. These headwinds may immediate companies and particular person shoppers to ease up on their discretionary spending. Nonetheless, I don’t see any long-term structural dangers to AAPL. However these headwinds are extra basic and never distinctive to AAPL. A extra distinctive and severe threat to AAPL is its giant reliance on China. And I’ve a devoted article analyzing its China publicity, entitled Apple’s China Antithesis.

By way of upside dangers to my above evaluation, I see the belief of an 18x money movement a number of as too conservative. A enterprise like AAPL ought to be simply price a minimum of 20x of its money movement. And if its valuation certainly reverts again to 20x money movement, this little reversion would hasten its climb again to $3T to a timeframe round 2025~2026 – you’ve already been warned that the time may be earlier than you assume!

Clear futuristic electrical vehicles highway site visitors

gremlin

Introduction

A number of days in the past, I analyzed ARK’s Genomic ETF (ARKG). I believe ARK Make investments do good work on specialised analysis specializing in long run transformation potentials of firms. Therefore, their ETFs are certainly a bunch of extremely promising firms with very uneven risk-reward profiles.

I consider one of the best ways to revenue from these ETFs is to take our personal possession of the macro issues to speculate solely in favorable environments. When the worldwide financial atmosphere is up-beat, I consider ARK Make investments’s funds will outperform the market handsomely.

On this article, I discover the prospects of one other certainly one of Ark’s innovation themes:

ARKQ: Publicity to Autonomous Expertise & Robotics

The ARK Autonomous Expertise & Robotics ETF (BATS:ARKQ) seeks publicity world firms whose major enterprise is in promoting competencies in areas comparable to autonomous transportation, robotics and automation, 3D printing, vitality storage and area exploration.

ARKQ ETF Publicity Combine

Diversified Sector Combine

ARKQ ETF Sector Publicity (ARKQ ETF Web site, Creator’s Evaluation)

I might say ARKQ has a broad sectoral publicity total, notably in industries that mix using know-how with {hardware}. One noteworthy distinction I spot is the stark distinction in weights within the producer manufacturing business (19% weight) and the method industries comparable to chemical compounds (0.6%). This illustrates ARKQ’s publicity to know-how spend related to discrete, device-related parts. That is in distinction to know-how spends related to software program to manage the stream of processes comparable to fluids and gases.

Most Firms in North America however Numerous Finish Markets

ARKQ ETF Geography Combine (ARKQ ETF Web site, Creator’s Evaluation)

The chart above reveals that lots of the firms in ARKQ are in North America. Nonetheless, you will need to observe that the income profile could be a lot diversified. For instance, I believe that Western Europe, which has many automotive firms would make up greater than 1% of income publicity.

Diversified High 5 Holdings Combine

ARKQ ETF High 5 Holdings Publicity (ARKQ ETF Web site, Creator’s Evaluation)

ARKQ’s prime 5 holdings embrace Trimble (TRMB), Kratos Protection & Safety (KTOS), Iridium Communications (IRDM), Tesla (TSLA), and UiPath (PATH).

Given the sector specialist focus of the ETF, I consider that is fairly a diversified publicity with the highest 5 making up 37.6% of the complete portfolio. Furthermore, the weights are much less asymmetrical than is the case in a few of ARK Make investments’s ETFs comparable to Genomics (ARKG).

Basic Drivers of ARKQ

The diversified nature of ARQ means no particular person inventory contributes disproportionately to the general efficiency of the ETF. Moderately, it’s extra helpful to contemplate the underlying drivers of buyer spends:

I observe that autonomous transportation, robotics and automation, 3D printing, vitality storage and area exploration options are sometimes capex-spend choices versus opex spend choices. Some business commentaries recommend a desire for opex-related spends, with capex spends anticipated to get better extra slowly. This might be a headwind for firms in ARKQ, holding potential room for downward shock in gross sales.

I consider capex spends might be extra energetic throughout occasions of buoyant industrial exercise. To that extent, I observe that a big a part of world industrial exercise in america, China and Japan (which make up virtually 50% of GDP) is in contraction mode. Till these nations’ respective PMIs float above the 50-line once more, I doubt there could be any real set off for bullishness in ARKQ’s constituent holdings.

Technical Evaluation

Relative Learn of ARKQ vs. S&P 500

ARKQ vs. SPX500 Technical Evaluation (TradingView, Creator’s Evaluation)

In opposition to the S&P500 (SPY), ARKQ has had it tough because it exploded to its peak in February 2021, adopted by a pointy bearish drop so far. Nonetheless, the ARKQ/SPX500 pair might need reached its backside after returning to the crucial month-to-month assist degree, as highlighted within the chart above.

I anticipate a slowdown in momentum round this degree and a gradual sideways sample alongside the month-to-month resistance and assist zones to find out the directional momentum that follows. My examine of monetary market bubbles means that recoveries after a bubble pop comparable to right here are typically sluggish and gradual moderately than sharp. To verify a change in pattern, I have to see a transparent false breakdown and a pointy rebound, trapping sellers and early patrons.

On the standalone chart, I anticipate the same value sample with ranging value motion. Nonetheless, on this case, I believe ARKQ is more likely to have a go to right down to the $35.38 month-to-month assist, as this assist degree has extra historic relevance.

Takeaway

If capex spends take longer to rebound, then a basic bullish case for ARKQ could not materialize so quickly. I’m monitoring business commentaries and the worldwide economic system’s PMIs as a proxy to evaluate the underlying spending atmosphere.

Nonetheless, this doesn’t imply the bleeding down of the ETF value will proceed. Moderately, I believe we’re forming a little bit of a neighborhood backside and I anticipate a sluggish and gradual build-up of an accumulation base earlier than any materials transfer upwards. To maximise IRR, I consider it’s best to attend a number of months and purchase once more at comparable costs.

Thus, my total evaluation is a ‘maintain’ on ARKQ.

John M. Chase/iStock Unreleased through Getty Photographs

As we enter 2023, Mr. Market has grow to be very short-term oriented. Most precise enterprise analysts which can be taking a look at Capital One Monetary (NYSE:COF), or a lot of the different greater banks, would agree that they’re deeply undervalued relative to intrinsic worth. Nonetheless, as a result of earnings may briefly decline attributable to a weakening economic system and normalizing credit score losses, few analysts are prepared to pound the desk as this one writing is likely to be. Capital One is an excellent enterprise in a powerful aggressive place. The earnings energy of the enterprise could be very strong and the corporate trades at a value implying substantial losses, versus the robust income which can be seemingly even in a recessionary situation. This brings alternative to the long-term investor prepared to abdomen short-term ache for the long-term acquire.

The final time I wrote about Capital One Monetary was in July of 2020, through the coronary heart of lockdowns and the Covid-19 pandemic-driven hysteria, which I’d encourage you to peruse because it offers some context to how delicate the present financial disaster is relative to what was transpiring then. What a nightmare it was. Nearly instantly, financial exercise plunged with nearly no warning. There was zero readability by way of when the economic system could be allowed to really get better, or what that may even seem like given the unprecedented actions of getting the worldwide economic system lockdown. The disaster occurred shortly after the essential CECL accounting change was instituted within the very starting of 2020, which required banks to order for whole anticipated losses on the lifetime of the loans, inclusive of intervals of time when the economic system is in a recession or challenged. Doing this upfront would cut back short-term earnings and frontload loss provisioning. Expectations after all can change, however by definition, future loss provisioning can be lower than it could have been beneath the prior accounting regime, resulting in much less volatility in earnings all else being even. While you take a look at the valuation’s banks commerce at although when there’s any signal of potential financial disaster, it feels as if Wall Road by no means obtained this memo. It’s one factor to commerce at low multiples at peak earnings, particularly if the corporate is prone to lose cash or make little or no in a recession attributable to elevated provisioning, however it’s a entire different factor to have the multiples decreased dramatically going into what are prone to be trough earnings, that are nonetheless going to be fairly good. I’d argue the larger banks have grow to be way more like regulated utilities in that they aren’t able to earnings the 30% ROTCE’s, however additionally they are far much less dangerous than they’ve ever been. Utilities commerce at double the valuation, if no more relying on the financial institution.

2022 noticed probably the most aggressive rate of interest expansions in U.S. historical past, which mixed with robust mortgage development, led to a big improve in preprovision web income for the banking business. This enchancment was offset by extra normalized reserve provisioning, compared to the sugar-high stimulus credit score surroundings of 2021, when credit score efficiency had by no means been higher. Normalized credit score has been anticipated for a number of years, even earlier than the pandemic, as credit score had outperformed expectations time and time once more, largely attributable to way more conservative mortgage underwriting. To be clear, we’re nonetheless far beneath even 2019 delinquencies and defaults most often, which was nonetheless an excellent credit score 12 months for the business. Not like a lot of the final 13 years for the reason that Monetary Disaster, banks have larger charges offering a tailwind to their revenues, which clearly is an enormous deal for firms that make most of their cash on web curiosity earnings, like Capital One does with its largely low-cost deposit base. These constructive attributes are fairly apparent to behold, however nonetheless the shares commerce at ridiculous costs as if we’re in one other 2008. It doesn’t make sense, so you’ll be able to both be paralyzed by concern, or make the most of the irrational pessimism.

To make the case for the attractiveness of COF, let’s check out the threerd quarter earnings assertion. Whole web income elevated 7% sequentially to $8.8B. Whole non-interest expense elevated 8% to $4.9B. Pre-provision earnings elevated 6% to $3.9B, which is the most important indicator of the underlying earnings energy of the franchise. Upon some long-expected credit score normalization, the availability for credit score losses elevated by $584MM to $1.7B, consisting of $931MM of web charge-offs and a $734MM reserve construct. The web curiosity margin elevated by 26 foundation factors to a really wholesome 6.8%. So, there you will have strong income development aided by robust spending, larger charges, and mortgage development, barely offset by inflationary prices and better mortgage loss provisioning. Web earnings was $1.7B, or $4.20 per diluted widespread share. If the economic system weakens, COF can cut back spending on issues like advertising and headcount, whereas the underside line would stay worthwhile even when mortgage loss provisions doubled in a given quarter from these at the moment robust ranges.

COF ended the threerd quarter with a Tier 1 capital ratio beneath the standardized strategy of 12.2%, which is comfortably their final goal of round 11%. Interval-end loans held for funding elevated $7.6B, or 3%, to $303.9B. Interval-end whole deposits elevated by $9.3B to $317.2B. Keep in mind, an enormous a part of my funding thesis is that the impression of CECL accounting just isn’t being given correct credit score at present valuations, so you will need to assess what varieties of reserves are at the moment on the books to have the ability to take care of that potential recessionary situation. COF ended Q3 with a whopping $12.209B allowance for credit score losses. The allowance protection ratios for Credit score Card, Client Banking, and Business Banking, are 6.87%, 2.6%, and 1.45%, respectively. To place these numbers in perspective, at 12/31/2020, the allowance protection ratios had been 10.46%, 3.94%, and a couple of.19%, respectively. The present financial surroundings is nothing like what we noticed through the lockdowns, or the uncertainty we confronted with the quickest rising unemployment charge and steepest drop in GDP we’ve seen in lots of many years. Even when COF needed to get again to these allowance protection ratios although, it may very well be completed inside just a few quarters, whereas remaining worthwhile over a 4-quarter interval. Identical to recessionary eventualities are a part of CECL reserves throughout non-recessionary instances, a restoration interval needs to be factored into reserves throughout recessionary instances. The longer the precise credit score losses are delayed, the much less they in the end will seemingly find yourself being, whereas the corporate can preserve refining its underwriting to regulate to market situations. For example, COF is decreasing its auto lending to regulate to near-term market situations upon declining used automotive costs. COF is extra of a subprime lender within the house, so they’re a bit extra prone to the place credit score degradation is being seen most clearly. They’ll now regulate whereas sustaining amply reserved and specializing in collections.

Many appear to overlook that credit score losses are perform of each defaults and recoveries. Naturally bank card lending has the very best loss reserve and the very best rates of interest related to it. There’s at the moment a number of hysteria about auto lending, however even when defaults had been to extend considerably, losses may be managed through comparatively fast repossessions and at the very least respectable recoveries upon the sale of the automobile. As well as, the banks gained priceless expertise throughout lockdowns by way of figuring out options for those that couldn’t make their funds. Definitely, these deferment packages had been bolstered by authorities stimulus, but it surely supplied very priceless information and experience to the banks that I feel may very well be leveraged in a interval of future stress. Most significantly, credit score losses are largely a perform of unemployment charges and underwriting. Underwriting has been very robust since 2008. Unemployment stays persistently low regardless of the Federal Reserve’s greatest efforts to overturn the applecart. So long as individuals have jobs, they’re unlikely to surrender the keys to their home, or automotive, and they’ll normally attempt to at the very least make the minimal funds on their bank card. It’s ironic in some methods as shares have been promoting off on good jobs information, together with the banks, but low unemployment is crucial think about decreasing credit score losses. I get that the concern is it means extra charge hikes, in the end inflicting a recession, however a recession appears to be baked into the share costs already, whereas little or no credit score is being given to the advantages of upper charges.

At a current value of $93.98, COF trades at 4.7x its TTM earnings of $20.29 and 5.8x its anticipated ahead earnings. Shares excellent have dropped from 541.8MM on the finish of 2015, to 384.6MM on the finish of Q3. COF has earned $14.84 per share simply over the past three quarters regardless of a extra normalized credit score surroundings, and mortgage loss provisioning in anticipation of a tougher financial forecast. The inventory yields roughly 2.55% and the tangible e-book worth per share of $81.38, already displays a major impression from rising charges decreasing the worth of the belongings on the stability sheet, as tangible e-book worth per share stood at $99.74 on the finish of 2021. COF has a confirmed monitor file of producing a double-digit ROTCE over the cycle and I feel it’s effectively poised to proceed doing so. Lengthy-term traders ought to make the most of the low cost at the moment being provided. For extra conservative traders, a less expensive value may be manufactured from the sale of a put choice. For example, the January 2024, $80 put choice is promoting for round $8.00 per share. If COF inventory trades above $80 at expiration, the put would yield a return of round 11%. Your worst-case situation is that if the inventory trades beneath $80 at expiration, you’d find yourself proudly owning COF at a breakeven value of $72.00 per share.

On delays at restarting the explosion-damaged Freeport LNG export terminal and on climate forecasts.

US exports of Liquefied Pure Fuel (LNG) in 2022, at 81.2 million tons, matched these of Qatar, the #1 LNG exporter on this planet, in response to ship-tracking information compiled by Bloomberg.

The US would have been #1 if an explosion in June hadn’t shut down the Freeport (FCX) pure gasoline liquefaction plant in Texas, which reduce LNG export capability by 17%.

Qatar’s LNG exports have been comparatively steady for the previous 10 years, in response to Bloomberg’s ship-tracking information. However the nation is now engaged in main enlargement tasks amid a surge in world demand for LNG.

US LNG exports started to surge in 2016 from near-nothing when the primary main LNG export terminal – initially an LNG import terminal – got here on-line. Since then, huge sums have been invested to construct and increase LNG export amenities largely in Louisiana and Texas, but additionally in Maryland and Georgia.

US LNG exports, in billion cubic toes, in response to the US EIA’s newest information by October:

As well as, 5 export terminals at the moment are underneath building within the US, and 11 export terminals have been accepted by the Federal Power Regulatory Fee however usually are not but underneath building, in response to FERC as of its newest replace on December 13.

The explosion in June on the Freeport terminal broken a part of the terminal. The reopening of the plant has been delayed a number of instances. The corporate reported publicly on December 23 that the reconstruction work essential to start out preliminary operations was “considerably full,” and that it was “submitting responses to the final remaining questions included within the Federal Power Regulatory Fee’s December 12 information request.” And it stated it delayed plans to restart the power till the second half of January.

Given the renewed delay – the data should have gotten out days earlier – the value of pure gasoline within the US plunged from $6.60 per million Btu on December 15, to $4.98 on December 23, the day of the general public announcement.

The value then continued to plunge. On Tuesday, NG futures plunged one other 11%, to $3.98 per million Btu for the time being, on climate forecasts over the weekend which predicted a milder first half in January for the US. This brings the plunge since December 15 ($6.60) to 40%! Praying for Freeport to re-start exports asap?

LNG exports supplied a brand new marketplace for the surging manufacturing of pure gasoline within the US, pushed by fracking, which had collapsed the value of pure gasoline beginning in 2009, as you’ll be able to see within the above chart. For concerning the subsequent 12 years, NG traded within the $2-Four vary per million Btu, pushing many frackers out of business – together with the large pure gasoline producer and pioneer fracker Chesapeake (CHK) in June 2020.

With surging LNG exports, pure gasoline costs broke out of the $2-Four vary in 2021, after which spiked to almost $10 with the surge in costs in Europe, demand for US LNG, now that LNG exports linked the value within the US to world costs. However the explosion on the Freeport plant, which lowered exports and eliminated some demand from the US market, introduced these costs again down. After which, over the close to time period, there’s all the time the climate.

In Europe, pure gasoline costs have unwound fully the loopy spike in 2022 and have plunged again to October 2021 ranges, amid file provide of LNG from the US and from different nations, file provide of piped pure gasoline from Norway, mixed with a light winter, and a discount in consumption.

Authentic Submit

Editor’s Word: The abstract bullets for this text had been chosen by Looking for Alpha editors.

B.A., M.A., College of Pennsylvania,; M.A., (Oxon.); Ph.D. Princeton College At present CEO of WWS Swiss Monetary Consulting SA

Disclosure:I/we’ve got no inventory, possibility or related spinoff place in any of the businesses talked about, and no plans to provoke any such positions inside the subsequent 72 hours.I wrote this text myself, and it expresses my very own opinions. I’m not receiving compensation for it (apart from from Searching for Alpha). I’ve no enterprise relationship with any firm whose inventory is talked about on this article.

Further disclosure: Information from third-party sources could have been used within the preparation of this materials and WWS Swiss Monetary Consulting SA (WWW SFC SA) has not independently verified, validated or audited such knowledge. WWS SFC SA accepts no legal responsibility in anyway for any loss arising from use of this data, and reliance upon the feedback, opinions and analyses within the materials is on the sole discretion of the person. Please seek the advice of your personal skilled adviser earlier than taking funding choices. The feedback, opinions and analyses expressed herein are for informational functions solely and shouldn’t be thought-about particular person funding recommendation or suggestions to spend money on any safety or to undertake any funding technique. As a result of market and financial situations are topic to fast change, feedback, opinions and analyses are rendered as of the date of the posting and will change with out discover. The fabric will not be supposed as an entire evaluation of each materials reality concerning any nation, area, market, trade, funding or technique.

All investments contain danger, together with doable lack of principal. Inventory costs fluctuate, generally quickly and dramatically, on account of components affecting particular person firms, explicit industries or sectors, or normal market situations. Bond costs usually transfer in the wrong way of rates of interest. Thus, as costs of bonds in an funding portfolio modify to an increase in rates of interest, the worth of the portfolio could decline. Particular dangers are related to overseas investing, together with forex fluctuations, financial instability and political developments. Information from third-party sources could have been used within the preparation of this materials and WWS Swiss Monetary Consulting SA (WWW SFC SA) has not independently verified, validated or audited such knowledge. WWS SFC SA accepts no legal responsibility in anyway for any loss arising from use of this data, and reliance upon the feedback, opinions and analyses within the materials is on the sole discretion of the person. Please seek the advice of your personal skilled adviser earlier than taking funding choices. The feedback, opinions and analyses expressed herein are for informational functions solely and shouldn’t be thought-about particular person funding recommendation or suggestions to spend money on any safety or to undertake any funding technique. As a result of market and financial situations are topic to fast change, feedback, opinions and analyses are rendered as of the date of the posting and will change with out discover. The fabric will not be supposed as an entire evaluation of each materials reality concerning any nation, area, market, trade, funding or technique.

All investments contain danger, together with doable lack of principal. Inventory costs fluctuate, generally quickly and dramatically, on account of components affecting particular person firms, explicit industries or sectors, or normal market situations. Bond costs usually transfer in the wrong way of rates of interest. Thus, as costs of bonds in an funding portfolio modify to an increase in rates of interest, the worth of the portfolio could decline. Particular dangers are related to overseas investing, together with forex fluctuations, financial instability and political developments.

With the market’s shut on Friday, buyers fortunately stated goodbye to 2022. Only a few funding classes generated a constructive return in 2022. One space inside equities that outperformed the broader market was shares that had dividends related to them. I’ve highlighted one particular technique over time, The Canine of the Dow, that’s centered solely on dividend yield. Over time, the Canine of the Dow technique has generated blended outcomes, however in a 12 months like 2022, dividends mattered. In 2022, the overall return for the Dow Canine equaled a constructive 2.2% versus the Dow Jones Industrial Common return of -7.0% and the S&P 500 Index return, down -18.2%.

The Canine of the Dow technique is one the place buyers choose the ten shares which have the very best dividend yield from the shares within the Dow Jones Industrial Index after the shut of enterprise on the final buying and selling day of the 12 months. As soon as the ten shares are decided, an investor invests an equal greenback quantity in every of the ten shares and holds them for your complete subsequent 12 months. For 2023, two of the 2022 Dow Canine might be changed, Coca-Cola (KO) and Merck (MRK). The 2 Dow Jones shares that qualify for the Dow Canine in 2023 are Cisco (CSCO) and JPMorgan Chase (JPM). The dividend yields for CSCO and JPM at 2022 year-end are 3.20% and three.00%, respectively.

Investing in shares that pay a dividend doesn’t guarantee constructive fairness returns. One profit although is the actual fact high-quality dividend-paying shares do have a tendency to carry up higher in unstable down markets like buyers skilled in 2022. Under is a chart that shows the overall return efficiency of three frequent ETFs that concentrate on dividend-paying methods together with the S&P 500 Index return for 2022. All three of the dividend methods considerably outperformed the S&P 500 Index. The dividend payers and dividend growers don’t outperform yearly; nevertheless, incorporating shares with favorable dividend traits into one’s portfolio can scale back the portfolio’s general volatility.