wildpixel/iStock by way of Getty Photos

Did I miss something whereas I used to be climbing?

That is a joke, after all. The peace, tranquility, and quiet of the cool mountain air I’ve loved over the previous couple of weeks contrasts sharply with the chaos taking place in the remaining of the world.

As traders, there are elements of this chaos that must be addressed.

Anytime I focus on the financial results of presidency coverage (or proposed coverage adjustments), some readers remark that I ought to keep away from “politics.”

However to write down about macroeconomics each week as I do and not point out the US election and its potential financial results would, in my estimation, be political. To fake that it’ll haven’t any impact could be doing a disservice to anybody studying.

So I’ll focus on the possible financial results of a possible Republican sweep (which at the moment seems probably) in the identical approach that CNBC and different monetary media shops do: By specializing in the economics and funding implications.

I am going to focus totally on Trump’s three marquee insurance policies: (1) protectionism, (2) immigration restrictionism, and (3) free fiscal coverage.

This is the desk of contents:

- A lot is going on proper now.

- Ratcheting up the commerce warfare.

- Immigration restrictions and deportation’s impact on the labor market.

- The potential penalties of free fiscal coverage: Spiraling inflation or Japanification?

- My contrarian purchase listing proper now.

Let’s start.

All the pieces, In all places, All At As soon as

A lot is going on proper now, each on the political and financial facet, that issues to traders.

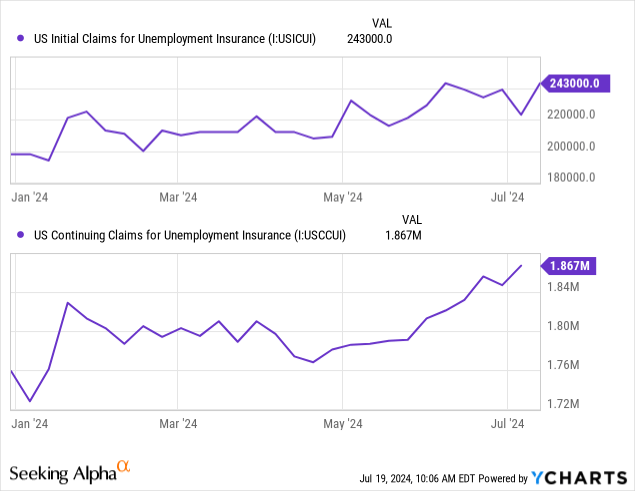

All of the noise taking place in politics could have obscured the rising development in unemployment claims reported this previous week, which concurrently brought about a market selloff in addition to rising Fed charge lower possibilities.

It is as if the market is saying: “Wait a minute. We have seen this earlier than. The Fed Funds Charge is at a cyclical peak. The yield curve has been inverted for a protracted whereas. Client spending is slowing. The labor market is weakening. Cyclical sectors are collapsing. And the main shares could have priced in an excessive amount of euphoria. May we be on our technique to a recession?”

Good query.

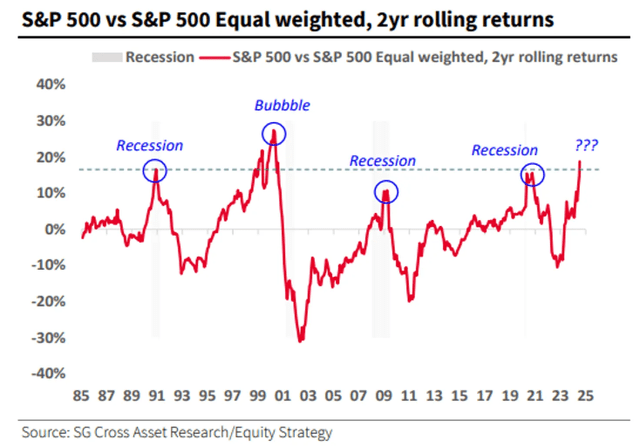

The chart under is admittedly extra correlation than causation, nevertheless it does reveal a correlation between peaks within the ratio of cap-weighted to equal-weighted S&P 500 indices and the prevalence of recessions.

SocGen

Will the historic sample maintain? Or is that this time totally different?

I believe the burden of proof is all the time on those that say this time is totally different.

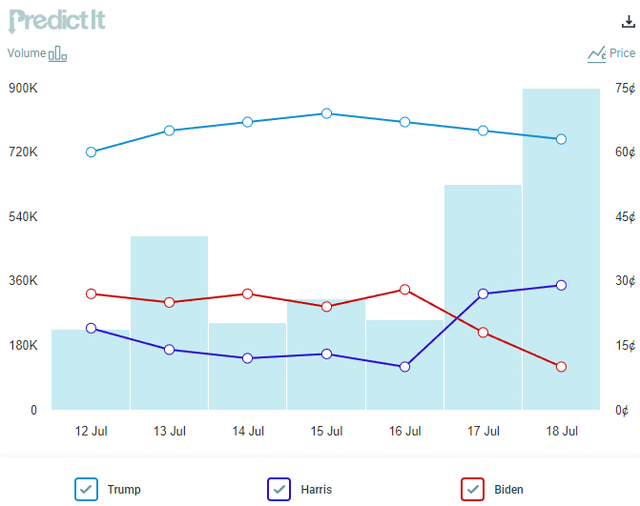

In the meantime, within the electoral realm, the pace with which momentous issues (e.g. an assassination try, requires a presumed presidential nominee to drop out, and so forth.) are taking place is extraordinary.

As issues stand right this moment, the prediction markets anticipate Donald Trump to win in November by overwhelming odds.

PredictIt Presidential Election Odds

Whereas many US elections have solely comparatively minor results on the funding outlook, there’s a case to be made {that a} second Trump time period may convey with it vital financial adjustments of which traders must bear in mind.

Return Of The Commerce Battle

The 2 largest producers on the earth look like getting ready to an expanded commerce warfare.

China is the most important producer on the earth as measured by actual (inflation-adjusted) output, and the US is the second-largest producer on the earth.

(This contrasts with the oft-repeated line that “we do not make issues in America anymore.”)

Trump seems to be fairly severe about ratcheting up the commerce warfare once more if he turns into president, and it must be famous that the ability to set tariff coverage is on the sole discretion of the president. Not like different tax coverage, Trump wouldn’t must undergo Congress or go any legal guidelines to boost tariffs. He may elevate tariffs by way of government motion.

Earlier than the Civil Battle and lengthy earlier than the introduction of the non-public earnings tax within the early 1900s, tariffs performed a key position in each gathering federal authorities tax revenues and defending American manufacturing. However the financial system was very totally different again then, because the overwhelming majority of the workforce and of GDP have been tied to agriculture or some form of industrial manufacturing.

Within the trendy financial system, the removing of tariffs led to dramatic reductions within the costs of all kinds of client items whereas facilitating an evolution towards a principally services-based financial system.

And but, protectionism appears to be renascent.

Maybe that is due to the widespread false impression that international importers are those who pay for the tariffs. In actuality, US shoppers and companies find yourself paying for the overwhelming majority of the import taxes.

To date, Trump’s proposed tariffs embody a 10% across-the-board tax on all imports, no matter origin nation, in addition to 60-100% tariffs on items from China.

For context, these proposed tariff charges on Chinese language imports vary from 3x to 5x increased than the tariffs imposed in 2018-2019. And a 10% across-the-board tariff charge could be 3.3x increased than the present common charge for non-China import origins.

However how nicely did these 2018-2019 tariffs on Chinese language items work at stimulating the US manufacturing sector?

Reply: By no means. They really seem to have had a unfavourable impact on US manufacturing.

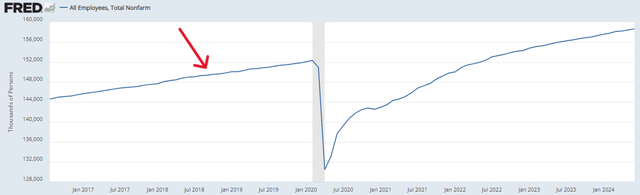

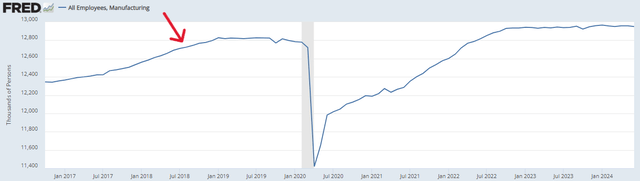

Think about this. The preliminary spherical of tariffs on Chinese language imports have been imposed in September 2018. From September 2018 to June 2024, complete US employment has elevated by 9.28 million jobs, or 6.2%.

Whole US Nonfarm Employment:

St. Louis Fed

As you may see, complete employment saved on rising proper up till the COVID-19 crash and has grown steadily within the post-COVID restoration.

In the meantime, throughout that very same time interval, manufacturing employment within the US has elevated by 206,000 jobs, or 1.6%. In different phrases, manufacturing jobs account for a mere 2.2% of complete jobs gained within the US between September 2018 and June 2024.

US Manufacturing Employment:

St. Louis Fed

As you may see, manufacturing employment flatlined for a few 12 months in 2019 just some months after the tariff regime started. Tariff charges continued rising till their peak in round mid-2019. Somewhat than seeing a rise within the development of US manufacturing employment after the tariffs took impact, the expansion of employment on this sector of the financial system halted.

And after recovering from COVID-19, manufacturing employment has principally flatlined since October 2022.

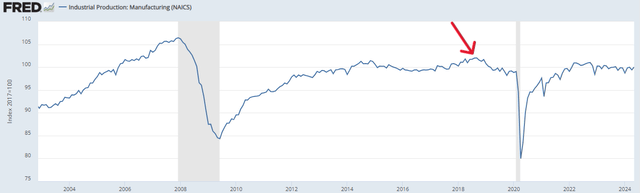

Furthermore, apparently, US manufacturing output peaked in September 2018, the month that Trump’s tariffs started taking impact. Since then, manufacturing output has been flat to down.

US Manufacturing Output:

St. Louis Fed

As of the most recent studying in Could 2024, manufacturing output is down about 2% from its peak.

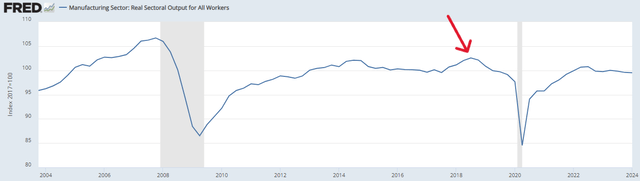

This is one other approach of measuring US manufacturing output that reveals the identical peak occurring in Q3 2018.

Actual Manufacturing Output For All Employees:

St. Louis Fed

There are just a few the explanation why US manufacturing declined following the implementation of the tariffs.

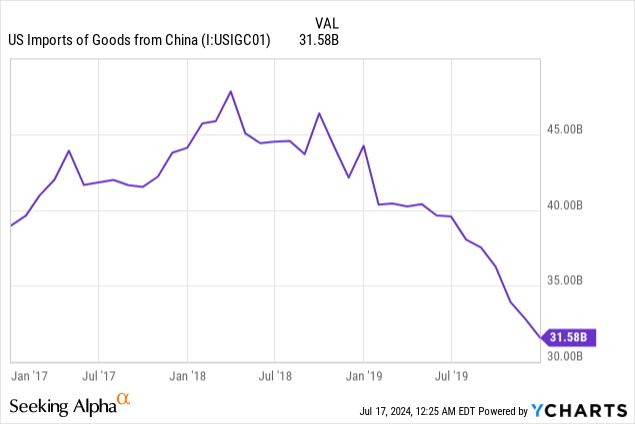

First, US producers rely considerably on uncooked supplies and/or intermediate items from China to supply their very own remaining items. About 25% of all imports into the US are industrial provides that help US manufacturing jobs and output.

The spike in US manufacturing output within the first three quarters of 2018 most likely got here from a surge of enter provides from China that instantly went into producing remaining merchandise within the US. You’ll be able to see the surge in imports from China in 2017 and into 2018 to front-run the tariffs, after which the falloff of imports from China after the tariffs’ implementation.

As I’ve written in a earlier article, the lack of imports from China did not lead to a corresponding improve in US manufacturing output however relatively merely a reshuffling of provide traces to different international nations.

The second motive why US manufacturing declined or stagnated after the implementation of the tariffs is that China positioned retaliatory tariffs on the US.

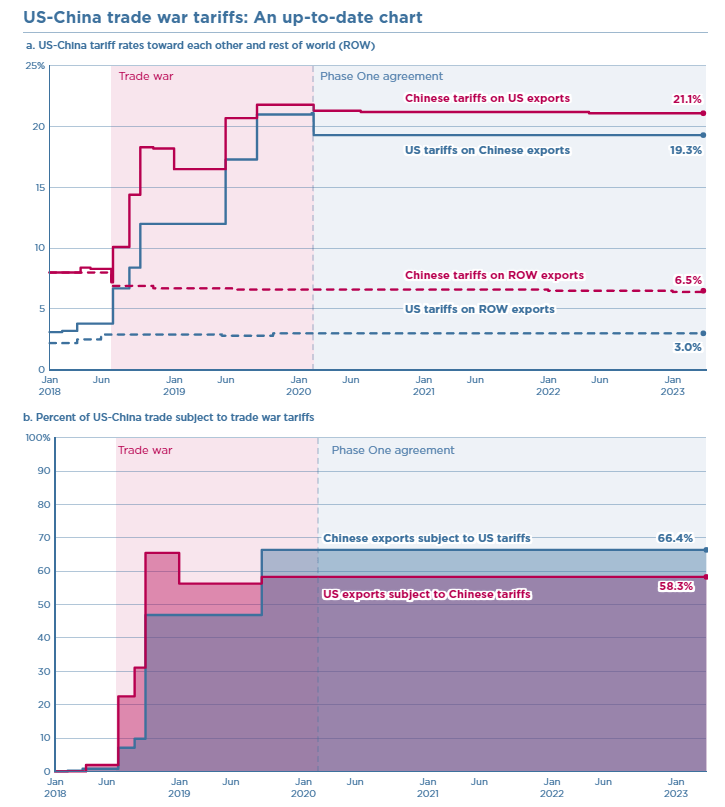

This is a chart I shared in “Eight Shares I am Shopping for As A Resurgent Commerce Battle Looms” exhibiting the tit-for-tat tariff partitions going up on either side of the US-China commerce warfare:

Peterson Institute for Worldwide Economics

(This chart throws water on the concept that Trump’s tariffs are mere short-term measures that act as negotiating chips in figuring out new, higher commerce offers. The “Part One” settlement reached with China in early 2020 solely lowered tariffs on Chinese language imports from 21% to 19% and Chinese language tariffs on US items from 22% to 21%.)

As you may anticipate, US producers do not simply produce items for US consumption but additionally for exportation to different nations. China is the third-largest vacation spot nation for US-produced items.

Naturally, with these retaliatory tariffs in place, Chinese language imports of products from the US sharply declined — not less than till COVID-19 hit.

As I’ve argued prior to now, the concept that Trump’s tariff technique is merely to extract higher commerce phrases with different nations has little advantage. The Republican Occasion has come to embrace tariffs each as a everlasting methodology of elevating tax income and as a way to guard US manufacturing from international competitors.

Trump’s proposals for his second time period replicate this.

As I defined in “7 Shares & 1 ETF I am Shopping for The Second Week Of July,” the implementation of Trump’s proposed tariffs would extremely probably result in significant inflation within the US.

Why?

Think about that the associated fee differential between US and international suppliers is normally nicely in extra of 10%. Due to this fact, 10% across-the-board tariffs would usually stream immediately into increased costs for US shoppers and companies.

Somewhat than construct costly new factories within the US and rent comparatively high-cost American laborers, it would normally be more economical for US companies to easily pay the import tax on foreign-made items and go that value onto American shoppers and/or eat a portion of it within the type of decrease margins.

Absolutely in some circumstances during which there are already American producers of a sure good, it would make extra sense to modify from a international provider to a US one. However in these circumstances, too, further prices to the enterprise will both be handed on to shoppers or will compress companies’ margins, or each.

In fact, it have to be stated that offsetting the probably unfavourable financial results of upper tariffs could be deregulations, an extension of tax cuts, and a possible decreasing of the company tax charge to 15%, that are extensively anticipated to be helpful to US companies.

Even so, I believe the unfavourable results of tariffs (increased inflation, decrease actual GDP development, disruptions to provide chains) could be essentially the most pronounced and influential a part of Trump’s financial agenda.

The Financial Penalties of Immigration Restriction and Mass Deportation

Trump has promised to convey again the restrictionist immigration insurance policies from his first time period in addition to to implement “the most important deportation operation within the historical past of our nation.”

One intention of limiting immigration and deporting those that reside within the US illegally is to profit native-born staff. The thought is that fewer immigrant staff shall be current to compete with native-born staff and thus wages must rise.

On the floor, this too is an inflationary coverage, as a result of companies have a tendency to boost costs to offset increased wages. (See this latest examine from the grocery trade in addition to this analysis from the UK exhibiting worth hikes in response to wage will increase.)

This is called the “wage-price spiral.” It’s a technique that inflation can turn into entrenched in an financial system.

An financial system is very weak to a wage-price spiral taking off when it’s experiencing a structural labor scarcity.

If not for immigration, america could be affected by an indefinite labor scarcity.

Do not consider me? Simply have a look at some information on employment within the US.

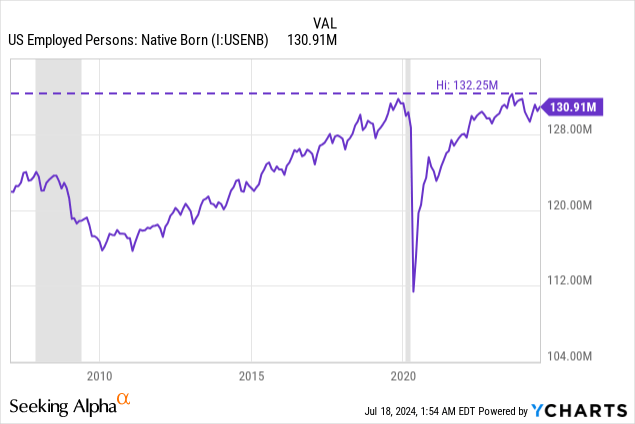

At present, the variety of native-born Individuals within the workforce is barely decrease than its pre-COVID peak in October 2019.

How may this be doable once we know that there are over 5 million extra jobs within the US right this moment than earlier than COVID-19 struck?

Two causes:

- Over 8.Three million Individuals are a number of jobholders, which is close to its document excessive

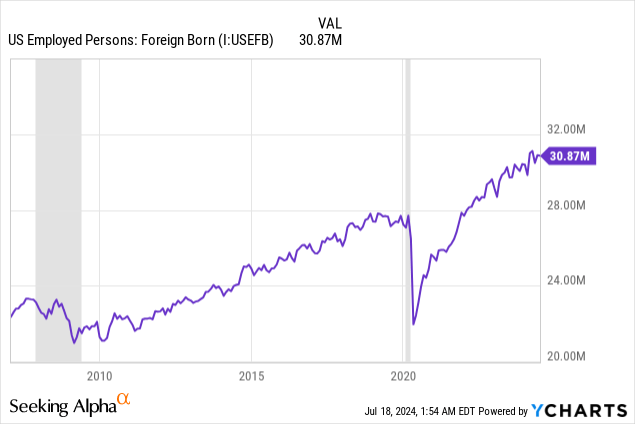

- International-born (immigrant) staff have been coming into the labor power in excessive numbers

The foreign-born section of the US labor power is sort of Three million individuals bigger right this moment than earlier than COVID-19.

The principle motive why the native-born workforce is not rising is growing older demographics. There are extra native-born staff retiring and leaving the workforce than youthful staff coming into it.

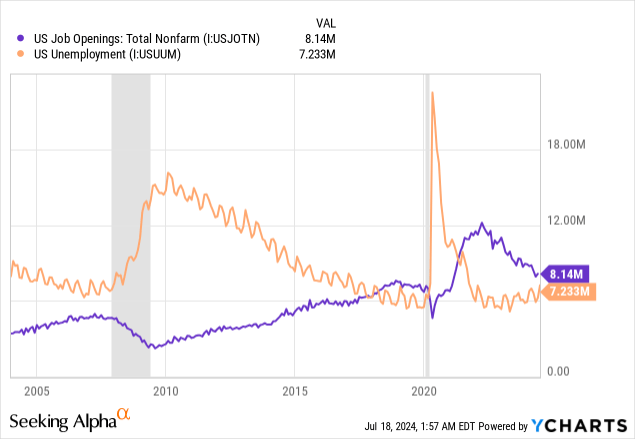

We are able to see growing older demographics slowly altering the construction of the labor market on this chart:

As you may see, for a really very long time, job openings remained nicely under the variety of unemployed Individuals, implying a labor surplus.

However because the variety of retirements outpace the variety of entrants into the workforce, job openings have steadily grown over time to the purpose the place openings outnumbered unemployment even earlier than the pandemic started.

This can be a signal of the structural labor scarcity current within the US financial system.

Immigrants have been plugging that hole and bringing down the entire variety of job openings, however in the event you lower off the stream of immigration into the US (or considerably curtail it), the labor scarcity will reassert itself, probably resulting in a wage-price spiral.

Mass deportation would have much more extreme results, as a result of relatively than leaving job openings unfilled, it will create extra job openings.

To not point out the unfavourable results {that a} lack of total inhabitants would have on combination demand and complete consumption. In any case, fewer individuals within the nation interprets to much less client spending, which in flip interprets into much less income for companies.

This text from the Miami Herald particulars extra of the probably financial results of mass deportation.

In my estimation, mass deportation would probably set off not less than a short lived bout of inflation because of a wage-price spiral. It may become a longer-running inflationary stress.

Unfastened Fiscal Coverage & Deficit Spending

To be clear, each Trump and Biden have put the pedal to the steel in the case of fiscal coverage and deficit spending.

The widespread perception (false impression, for my part) is that deficit spending all the time promotes GDP development and inflation. However in actuality, it is determined by the form of spending that the federal government is doing.

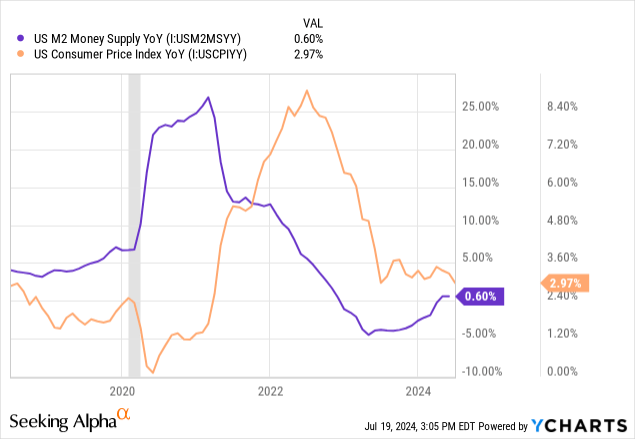

In relation to inflation, do not forget that inflation is principally attributable to an excessive amount of cash chasing too few items.

Since authorities spending tends to not produce new items, the important thing metric to observe isn’t the deficit itself however relatively the cash provide.

There is no such thing as a correlation between the extent of the deficit and inflation, however there’s a robust correlation between the expansion of the cash provide and inflation.

As we noticed throughout and after COVID-19, the large surge in cash circulating within the financial system (by way of stimulus checks, enhanced unemployment advantages, PPP loans, and so forth.) translated into an enormous spike in inflation a few 12 months later.

Deficit spending throughout COVID generated inflation as a result of it created cash and immediately gave it to shoppers to spend on the similar time that manufacturing and provide chains collapsed for pandemic-related causes.

Even when manufacturing had continued apace and provide traces remained intact, although, it’s probably that such an enormous and sudden surge of cash nonetheless would have generated inflation.

Alternatively, distinction the massive deficit spending of about $1.Three trillion within the first three quarters of fiscal 2024 (~6% of GDP annualized) with the falling charge of inflation.

Why does right this moment’s deficit spending not generate inflation?

It’s as a result of right this moment, not like 2020-2021, the sorts of issues the federal government is spending cash on will not be meaningfully rising the cash provide.

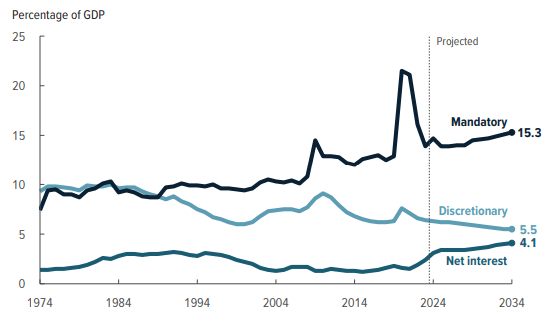

At present, development in authorities spending is generally coming from curiosity expense, Social Safety, Medicare, Medicaid, protection, and subsidies for inexperienced vitality and infrastructure funding.

As of the most recent CBO projection, just about all development in authorities spending over the following decade is anticipated to come back from obligatory sources (Social Safety & healthcare packages) and curiosity expense.

CBO Finances And Financial Outlook

This assumes no adjustments to the regulation or further spending handed by Congress.

Social Safety isn’t inflationary, as a result of (1) SS advantages are normally a fraction of retirees’ earlier labor earnings, and (2) retirees usually spend 20-40% much less in retirement than they did after they have been employed.

Healthcare packages probably do contribute to inflation within the healthcare area however nowhere else.

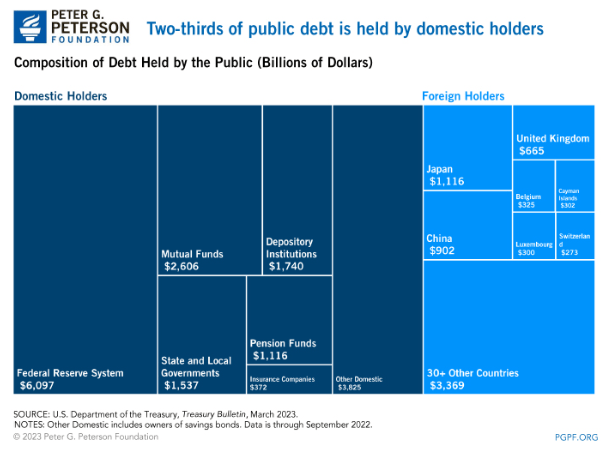

Do rising authorities curiosity funds spur inflation? Most likely not, or not less than not very a lot. The overwhelming majority of Treasury debt homeowners are numerous elements of the federal government, foreigners, US mutual funds, depository establishments, pensions, and insurance coverage corporations.

Peter G. Peterson Basis

Solely about 10% of federal debt is owned by non-public, non-institutional homeowners. Whereas some portion of that most likely will get spent, most of it stays within the monetary system and/or will get reinvested in different property.

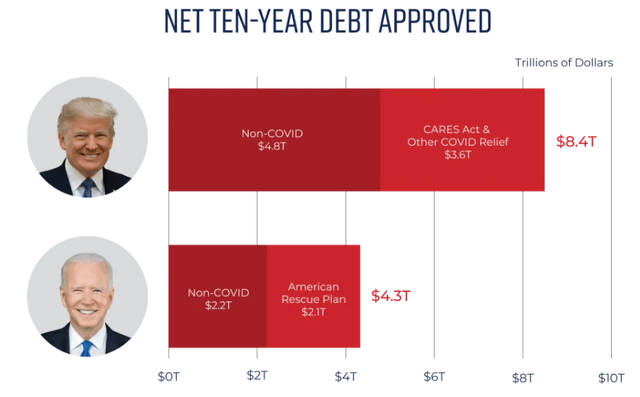

For these , the non-partisan Committee For A Accountable Federal Finances carried out evaluation on the quantity of recent debt (deficit spending) permitted through the first phrases of each Trump and Biden.

This chart reveals the quantity of incremental debt every president permitted over a 10-year interval:

Committee For A Accountable Federal Finances

The chart contains not solely new spending but additionally spending cuts in addition to the income facet — tax cuts/hikes.

Exterior of “helicopter cash” sort authorities spending that immediately grows the cash provide and will increase client spending energy, extra authorities debt accumulation tends as a substitute to overwhelm financial development.

A 2020 meta-analysis of 10 years’ value of financial research discovered that, for excessively indebted nations with debt-to-GDP ratios above a sure threshold, extra debt normally resulted in slower financial development.

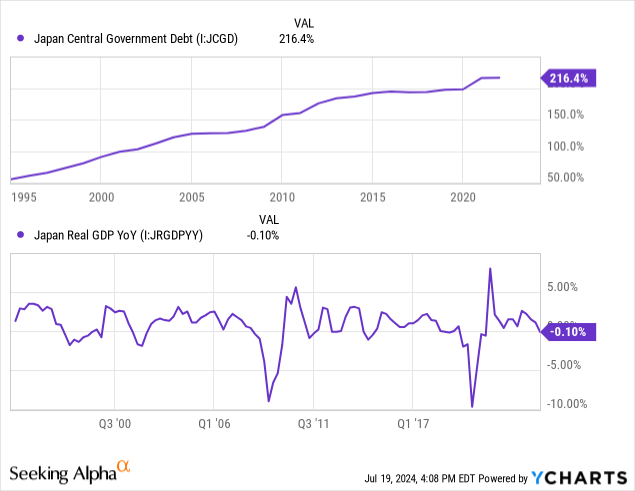

That is the “Japanification” thesis.

For many years now, Japan’s authorities debt to GDP has risen and risen, whereas actual GDP development has been persistently meager.

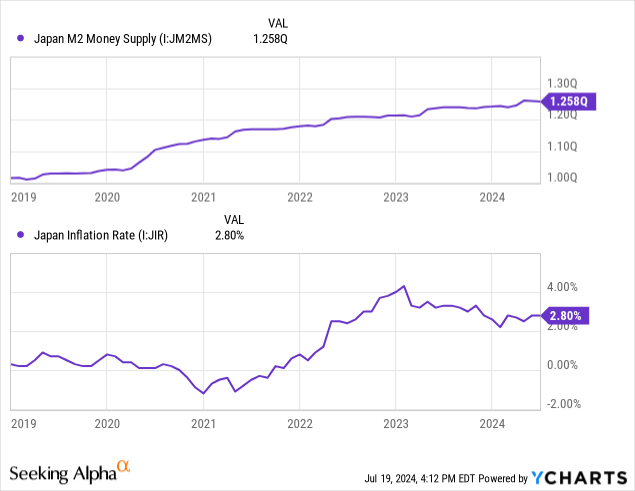

Likewise, up till a burst within the cash provide beginning in 2020, Japan’s inflation charge has lengthy been anemic as nicely.

From the start of 2019 to right this moment, Japan’s cash provide has grown 24%, considerably sooner than its earlier historic charge. That translated right into a peak inflation charge of just a little over 4%.

In lieu of one other burst within the cash provide, the US financial system will probably slip again into the low development, low inflation surroundings that characterised it earlier than COVID-19 started — the identical low development, low inflation surroundings that characterised Japan’s financial system from round 1990 to 2020.

My Purchase Record

I am taking a little bit of a contrarian stance with the shares on my purchase listing proper now.

| Dividend Yield | Projected Ahead Dividend Progress (Guesstime) | |

| American Houses Four Hire 6.25% Most popular Collection H (AMH.PR.H) | 6.5% | N/A |

| Brookfield Renewable (BEP, BEPC) | 5.9% | Mid-Single-Digit |

| Clearway Power Inc. (CWEN, CWEN.A) | 7.1% | Mid-Single-Digit |

| Rexford Industrial (REXR) | 3.4% | Excessive-Single-Digit to Low-Double-Digit |

Trump has acknowledged his intention to repeal the “Inflation Discount Act,” a legislative bundle that promotes clear vitality however does nothing specifically to truly cut back inflation.

Current evaluation put out by Columbia Threadneedle Investments argues that whereas a full repeal of the IRA is unlikely, a partial repeal is feasible.

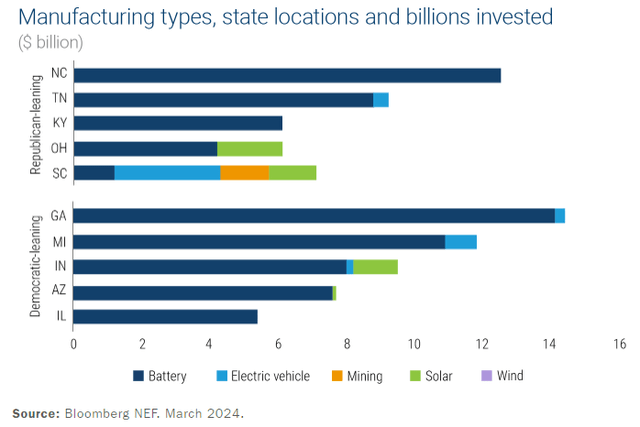

The explanation why an IRA repeal is unlikely is that a lot of its subsidies stream into Republican and swing states. This is an illustration of inexperienced manufacturing subsidies by state:

Columbia Threadneedle

Whereas this picture reveals Indiana as “democratic-leaning,” the state reliably votes Republican, and Georgia, Michigan, and Arizona are all swing states.

It appears unlikely that Republicans in these states will vote to defund their states of this subsidy earnings.

To a lesser extent, the identical holds true of renewable vitality tax credit for set up and manufacturing. Many of those renewable vitality tasks are concentrated in Republican states like Texas, Florida, North Carolina, and Arizona.

Nonetheless, Columbia Threadneedle asserts that provisions like EV tax credit, charging station tax credit, emissions and vitality effectivity requirements, and sure particular clear vitality funding is at excessive threat of being repealed in a Republican sweep.

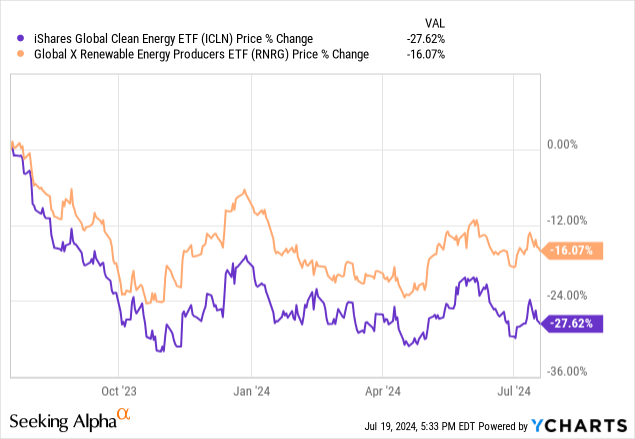

In fact, it’s doable that renewable vitality tax credit do get repealed, which might make operational tasks much less worthwhile and would gradual the speed of growth of recent tasks.

If that occurs, anticipate even worse efficiency from the likes of the iShares World Clear Power ETF (ICLN) and renewable energy asset homeowners equivalent to these within the World X Renewable Power Producers ETF (RNRG).

However evaluation from MIT Know-how Evaluate attests that behind the scenes, renewable energy tax credit are rather more standard with Republican lawmakers than they’re publicly.

Morgan Stanley analysts echo this sentiment, arguing that subsidies for home manufacturing, wind & photo voltaic, and nuclear energy get pleasure from bipartisan help and are unlikely to be repealed.

That is why I’m shopping for the dip on BEP and CWEN.A, which each personal massive portfolios of renewable vitality property.

In the meantime, whereas the 6.5% yield of American Houses Four Hire’s (AMH) sequence H most well-liked inventory isn’t the best yield you may discover within the preferreds area, I consider it’s extremely more likely to return to its par stage of $25.

In truth, AMH.PR.H traded above $25 as not too long ago as March 2024.

Whereas the pref solely has upside of about 5%, I consider that upside is very more likely to manifest within the comparatively close to future, which can give me a possibility to promote the pref for a small achieve and reinvest elsewhere.

Lastly, be aware that REXR simply reported Q2 2024 earnings, and so they have been fairly stable:

- Similar-property NOI development of 6.0% on a GAAP foundation and 9.1% on a money foundation

- Similar-property lease charges up 67.7% on a GAAP foundation (inclusive of future lease escalations) and 49.0% on a money foundation

- Q2 core FFO per share development of 11.1% YoY

- 1H core FFO per share development of 10.4% YoY

- Occupancy of 96.9%

I proceed to anticipate high-single-digit to low-double-digit development from REXR regardless of the overall slowdown in industrial actual property, largely due to REXR’s high-quality places and constructing performance.

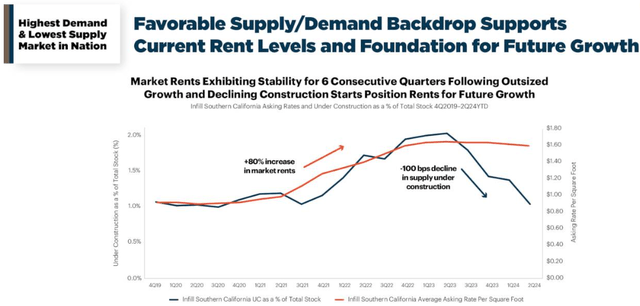

Furthermore, the pipeline of business actual property underneath development in Southern California has now fully reverted again to its earlier stage and continues to drop.

REXR Q2 2024 Presentation

This as asking rents proceed to remain regular. Infill industrial actual property in SoCal continues to get pleasure from among the lowest emptiness charges within the nation, averaging 3.9% in Q2, in line with REXR.

An alternative choice to REXR for individuals who like the true property however would like the next yield is the REIT’s 5.875% Collection B most well-liked inventory (REXR.PR.B), which at the moment has about 15% upside to par worth and presents a 6.7% yield. REXR’s two most well-liked inventory sequence collectively account for under about 1% of its complete capitalization, making them terribly secure sources of high-yielding earnings coming from an funding grade (BBB+ and equal credit score scores) issuer.

REXR may be a stunning decide due to its unique concentrate on Southern California, by way of which a lot of the imports from Asia stream by way of the Port of Los Angeles. However take into account that REXR’s portfolio is overwhelmingly geared towards the native financial system, not importers. Its common area measurement is 26,000 sq. toes, and its places are higher fitted to last-mile deliveries than warehousing enormous batches of products for distribution throughout the nation.