malerapaso/E+ through Getty Photographs

Is now a superb time to purchase shares?

The temper surrounding the inventory market underwent a elementary shift lately. Discuss of recessions, inflation, and debt ceilings turned on a dime to synthetic intelligence (AI) and goals of recent market highs. Some at the moment are saying we are going to keep away from a recession altogether (though I’ve my doubts).

Firms like NVIDIA (NVDA) are Palantir (PLTR) are hovering, up 205% and 191% in 2023, respectively. Many shares which were lifted by AI enthusiasm are buying and selling at unprecedented valuations.

However the financial system nonetheless faces challenges because the speedy rise of rates of interest and the anticipated exhaustion of stimulus financial savings have but to hit full drive. It’s important for buyers to pay attention to valuations.

So when Alphabet (NASDAQ:GOOG)(NASDAQ:GOOGL) launched Q2 earnings on July 25th, all eyes appeared centered on AI. However I used to be trying elsewhere.

A false dilemma

Alphabet doesn’t have to decide on between a high-margin mannequin and investments sooner or later.

The battle over margins at Google has raged for years. In actual fact, when Google modified its moniker to Alphabet, it was as a result of the corporate wished to raised mirror its initiatives past promoting. The promise on the time was that the corporate would spend money on moonshots however be fiscally accountable on the identical time. However margins suffered.

Most of the firm’s “different bets,” like fiber web, smart-home merchandise, well being sciences, and supply drones, have not moved the needle. However others, like YouTube, paid off splendidly.

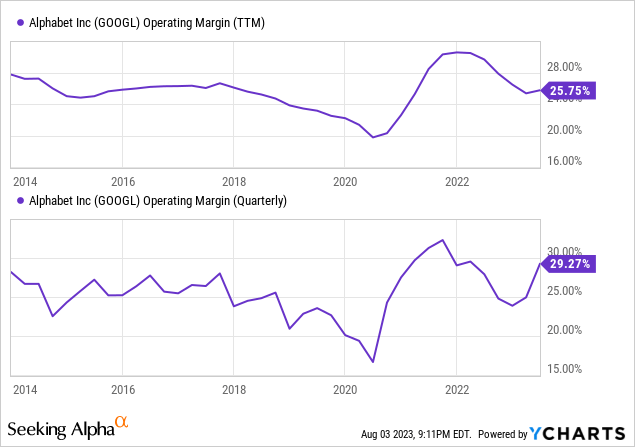

Nonetheless, Alphabet’s working margins had been in a downward-moving channel for a number of years earlier than the pandemic, as depicted under.

Google’s working margin exploded throughout the pandemic growth because the financial system was flush with stimulus money, and gross sales rose 55% from $183 billion in 2020 to $283 billion in 2022. Then inflation and a few over-exuberant spending threatened to steer the corporate proper again to declining margins.

The working margin dipped to 24% in This fall 2022 as CEO Sundar Pichai vowed to make the corporate 20% extra environment friendly.

To this point, so good.

Let’s be clear: Different Bets are crucial to Alphabet’s future. The corporate’s AI analysis hub Google DeepMind is arguably its most vital long-term funding now. However each every now and then it is necessary to prune again a number of the lifeless leaves.

AI initiatives are going to price cash – a LOT of cash. So trimming the fats in different areas is significant to the success of the inventory.

Alphabet took $2.6 billion in restructuring costs in Q1 because it started to make adjustments. Working bills rose 9% year-over-year (YOY) however would have been capped at a 4% with out the costs. It is a large win contemplating rising prices economy-wide.

Then in Q2 the working margin jumped to an impressive 29%, exceeding the prior 12 months. Analysis and improvement bills rose 8%, however common and administrative prices declined. This proves that Alphabet can make investments closely sooner or later and produce great worth for shareholders.

CFO Ruth Porat’s feedback additional cement this purpose:

We proceed investing for development, whereas prioritizing our efforts to durably reengineer our price base company-wide and create capability to ship sustainable worth for the long run.” – Q2 earnings launch.

Money is flowing…to shareholders.

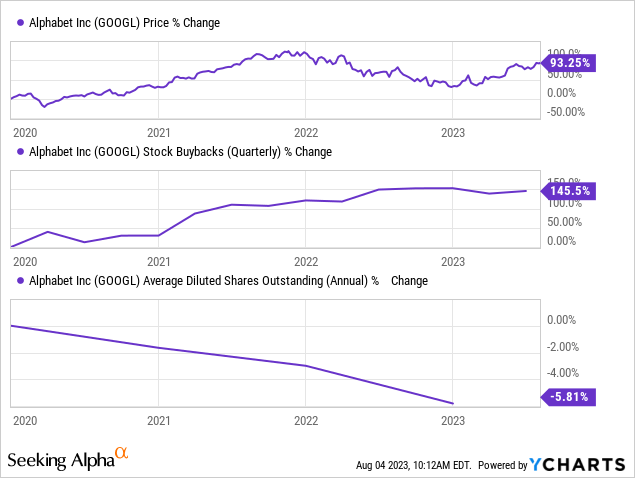

The give attention to effectivity pushed money from operations up 17% to this point this 12 months, leaping from $44.5 billion to $52.2 billion. Alphabet spent $29.5 billion shopping for again inventory by Q2. The buyback program has been terrific for shareholders, reducing the share rely (which raises earnings per share) and supporting them out there, as proven under.

Is Google inventory a purchase?

Many see Alphabet as behind within the race to develop and monetize AI. This is not the case. The corporate might have been caught napping when OpenAI launched ChatGPT, nevertheless it has been investing closely in AI for years. For instance, folks can attempt Google’s chatbot Bard right here. The corporate is integrating machine studying (ML) into Search, Google Lens (search from an image), Google Translate, and Google Workspace.

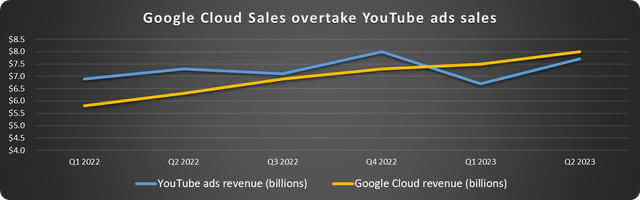

Google Cloud shall be a right away beneficiary. The platform gives the infrastructure and instruments for firms to construct and deploy AI functions. This could maintain the cloud section booming as firms experiment with and undertake options.

The cloud section has turned worthwhile this 12 months for the primary time (with a bit of assist from an accounting change), grew income by 28% in Q2, and has an extended runway.

Google Cloud income has overtaken its YouTube adverts income, as proven under, and can doubtless proceed to tug away on the energy of AI.

Information supply: Alphabet. Chart by creator.

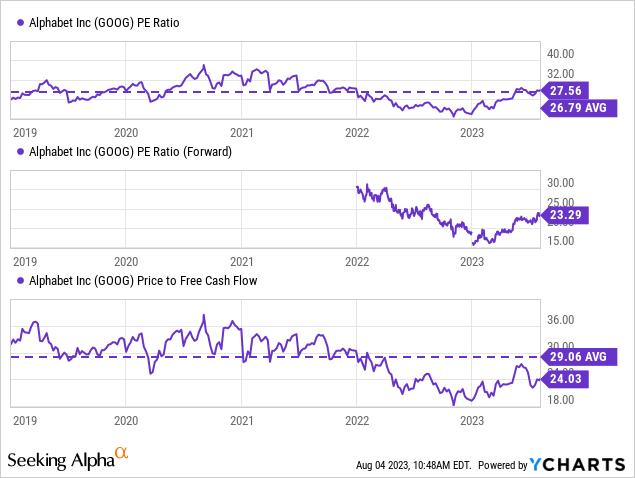

Alphabet inventory is up 47% in 2023 however solely 10% during the last 12 months. The worth-to-earnings (P/E) ratio recovered however remains to be enticing on a ahead foundation. The inventory is 21% undervalued traditionally primarily based on free money move, as proven under.

Alphabet has exceeded expectations in 2023, defying the promoting slowdown to develop revenues and EPS and, most significantly, money move. The terrific efficiency and investments in “what’s subsequent” make the inventory a superb long-term funding.

Can Alphabet make investments sooner or later and bolster margins for shareholders? Sure, and Q2 exhibits that the executives seem totally dedicated to the endeavor.