PM Photographs

Written by Nick Ackerman, co-produced by Stanford Chemist.

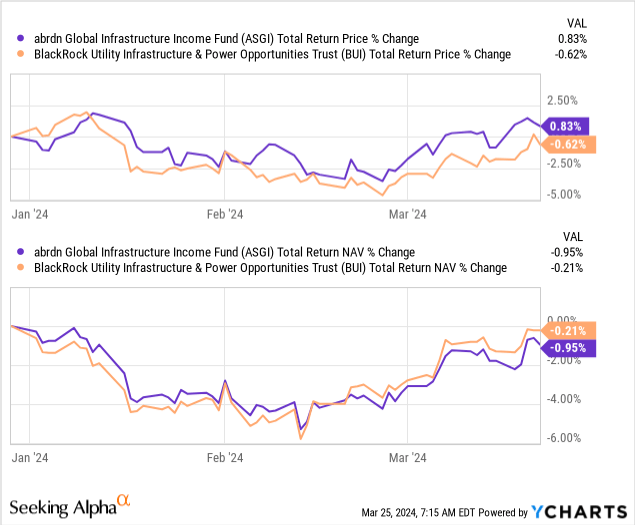

Heading into 2024, I had an article detailing why I believed that BlackRock Utilities, Infrastructure & Energy Alternatives Belief (BUI) and abrdn International Infrastructure Revenue Fund (NYSE:ASGI) had been alternatives for conservative utility/infrastructure performs. As we shut out close to the primary quarter of the yr, these performs aren’t essentially understanding as hoped.

Ycharts

At present, we’ll look at these two funds to know what is going on on and why I nonetheless take into account each of them worthwhile and conservative investments.

abrdn International Infrastructure Revenue Fund

- 1-Yr Z-score: 1.17

- Low cost: -13.50%

- Distribution Yield: 10.22%

- Expense Ratio: 1.65%

- Leverage: N/A

- Managed Property: $514 million

- Construction: Time period (anticipated liquidation date round July 28, 2035)

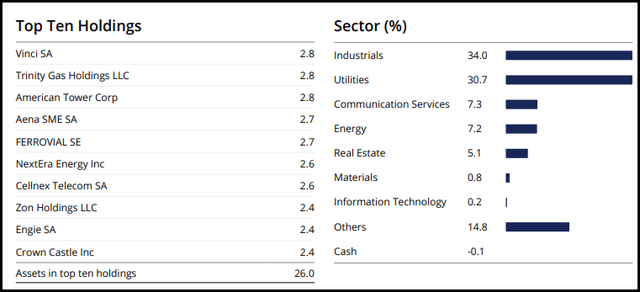

ASGI’s funding goal is “to hunt to offer a excessive stage of complete return with an emphasis on present revenue.”

To attain this goal, the funding technique is kind of easy. They’ll “put money into a portfolio of income-producing private and non-private infrastructure fairness investments from world wide.” The most important publicity for this fund stays industrials, because it has tended to be for fairly some time with this fund. Then again, utilities nonetheless make up a significant portion of this fund’s portfolio as nicely.

ASGI Prime Ten Holdings And Sector Publicity (abrdn)

BlackRock Utilities, Infrastructure & Energy Alternatives Belief

- 1-Yr Z-score: -0.65

- Low cost: -3.53%

- Distribution Yield: 6.81%

- Expense Ratio: 1.08%

- Leverage: N/A

- Managed Property: $496.7 million

- Construction: Perpetual

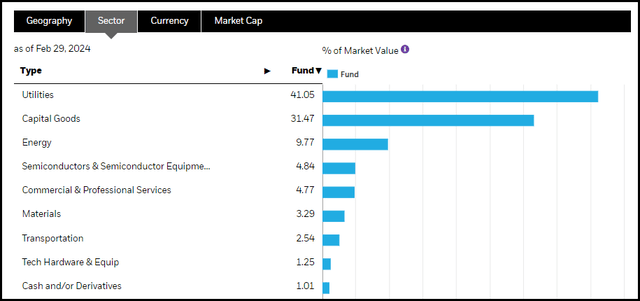

BUI’s funding goal is to “present complete return by a mix of present revenue, present positive factors and long-term capital appreciation.”

To attain this goal, they’ve fairly a little bit of flexibility. They’ll make investments “primarily in fairness securities issued by corporations which are engaged within the Utilities, Infrastructure, and Energy Alternatives enterprise segments anyplace on the earth and by using an choice writing (promoting) technique in an effort to boost present positive factors.”

Much like ASGI, BUI additionally carries publicity to not simply the utility area particularly, as each funds present loads of diversified publicity to your entire infrastructure area. For BUI, “capital items” is the second largest sector weighting, one other time period for industrials.

BUI Sector Publicity (BlackRock)

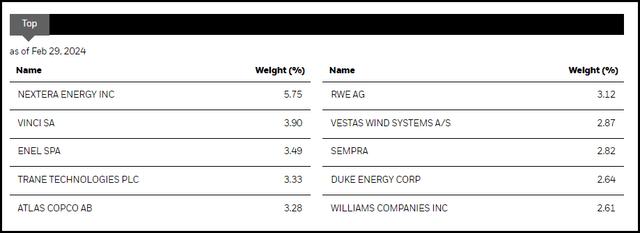

BUI Prime Ten Holdings (BlackRock)

Fee Headwinds To Tailwind Restoration Elongates

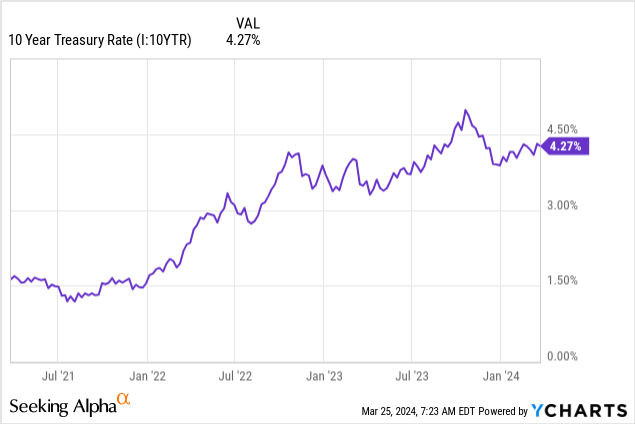

Whereas I suspected that 2024 would result in charge cuts, and that is why we noticed risk-free Treasuries falling in This autumn 2023, the timeline of such cuts has been pushed again. That is precipitated Treasuries to as soon as once more begin heading larger, with the 10-Yr now pushing again to over 4%.

Ycharts

That, in flip, pushed the utility sector to stay underneath strain as risk-free charges moved upward after taking fairly a dive from the highs final October.

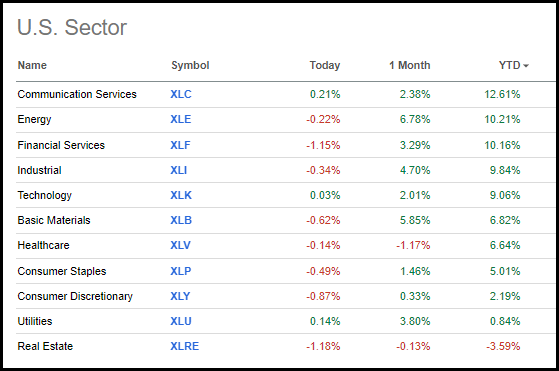

On a YTD foundation, utilities are about flat—solely topping actual property, which stays the one unfavourable sector for the yr.

U.S. Sector Efficiency as of 03/25/2024 (Searching for Alpha)

You will need to be aware that, as we laid out above, these aren’t pure utility funds. They carry some publicity to power and industrials in addition to international publicity. So, whereas we’re seeing the power and industrial sectors carry out nicely within the U.S., this does not look like taking place across the globe.

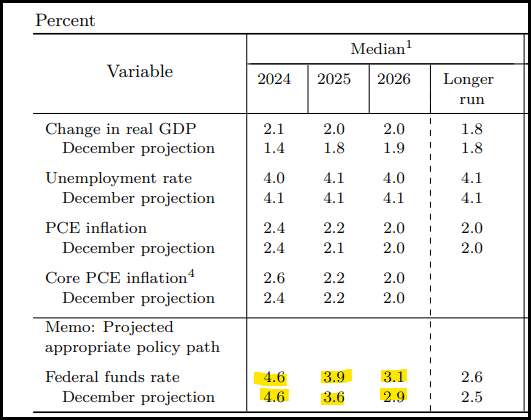

Charges had been transferring larger primarily based on the belief that the variety of charge cuts had been decreased from the place the market was initially pondering. The most recent Fed projections stay with an outlook of three cuts for 2024. Based mostly on the most recent projection materials, the projections for cuts in 2025 and 2026 did come down from earlier ranges.

Fed Fee Projections (Fed Projection Materials (highlights from creator))

After all, all of that is nonetheless depending on knowledge and the way it strikes going ahead. The most recent inflation knowledge, which was hotter than anticipated and with the labor market remaining sturdy, have stored the U.S. financial system resilient. Which means whereas the projection is for 3 cuts, that might be in the reduction of to 2 and even none for 2024.

What that would imply for ASGI and BUI is that the timeline for these funds to start out performing higher can be pushed again. With that mentioned, it’s nonetheless extremely anticipated that we’re on the peak charges for this charge cycle when it comes to the Fed’s goal. What the risk-free Treasury Charges do is as much as the market to determine. For that purpose, I imagine that these funds are nonetheless exhibiting alternative.

Enticing Valuations

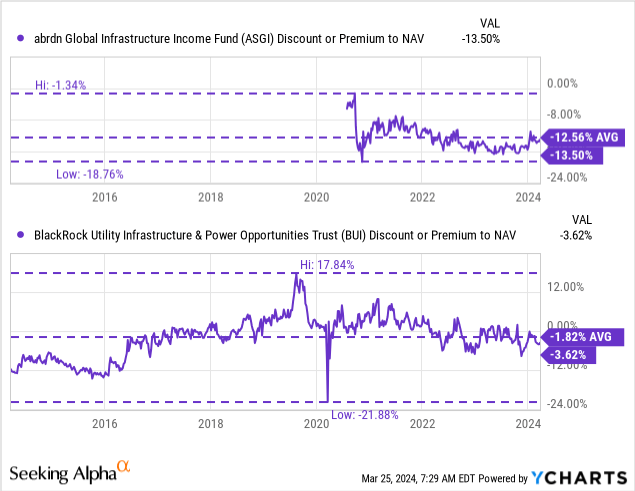

On the chance entrance, one other potential enticing function is that each of those funds are buying and selling at reductions to their internet asset worth per share.

Ycharts

On an absolute foundation, ASGI presents the higher alternative right here, however on a relative foundation to historic ranges, each have enchantment. BUI had traded at a premium fairly usually within the final a number of years. That makes a reduction right here now fairly compelling.

The conservative half right here is that each of those funds do not make use of leverage by borrowings. That is one much less transferring half that traders have to fret about, as leverage amplifies each the upside and draw back strikes of an funding.

With charges anticipated to remain a bit larger for a bit longer now, borrowing prices for the leverage being employed on a majority of closed-end funds can come underneath additional strain. A number of funds have hedges in place, however these hedges do not final without end, and decrease charges sooner will assist these funds. After all, I am not advocating for fully dumping all of your leveraged CEFs and fully altering one’s portfolio. That mentioned, it’s a good reminder simply to pay attention to what one is holding general and really feel snug with these better dangers.

Distributions

After all, these funds additionally pay out enticing distributions to traders whereas they anticipate higher instances.

They each make investments closely in equities and for that purpose, they may require capital positive factors to fund their distributions. That might be tougher in a flat market that we seem to search out ourselves in for the utility area, however then once more, these funds do carry publicity exterior of utilities. With a broader and international basket of fairness investments, they might discover alternatives elsewhere to clip positive factors to pay to traders.

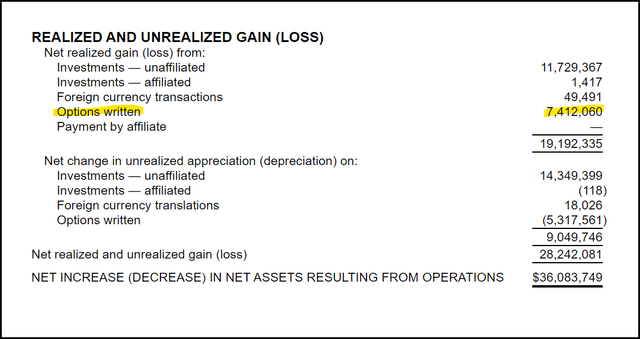

Additional, BUI has a coated call-writing technique that may additional usher in potential capital positive factors. Over 2023, that was one thing that BUI was capable of do as nicely, because the choices written introduced in simply over $7.Four million in realized positive factors for the fund.

BUI Realized/Unrealized Positive aspects/Losses (BlackRock (highlights from creator))

Each have NAVs larger than their inception – although ASGI is a comparatively newer fund, in order that needs to be stored in thoughts. Increased NAVs now recommend that traditionally, they had been capable of cowl their distributions to traders with out eroding away property.

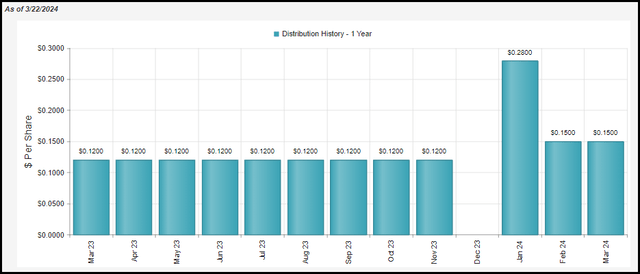

ASGI pays a managed distribution coverage that began lately. The coverage is predicated on 9% “of the common day by day NAV for the earlier month as of the month-end previous to declaration…” This coverage began in 2024, and it resulted in an preliminary bump to the distribution. Now, within the final two months, the month-to-month distribution has labored out to $0.15. Given the coverage, the distribution will change over time.

ASGI Distribution Historical past (CEFConnect)

If the NAV is transferring larger, the distribution must also be transferring larger and vice versa. I imagine that over time, the fund will start to erode its property now to help this 9% managed distribution coverage. That mentioned, that does not imply that returns cannot be respectable going ahead. One ought to simply anticipate that over time, the distribution will pattern decrease together with its NAV.

For BUI, they’ve gone with the widely extra favorable coverage of simply conserving a flat and stage distribution coverage. That does not imply that the distribution cannot change over time, however the adjustments aren’t mechanical primarily based on any particular metric. No less than not one that’s broadcasted to the general public; they might have their very own inner stage the place the Board feels they should lower.

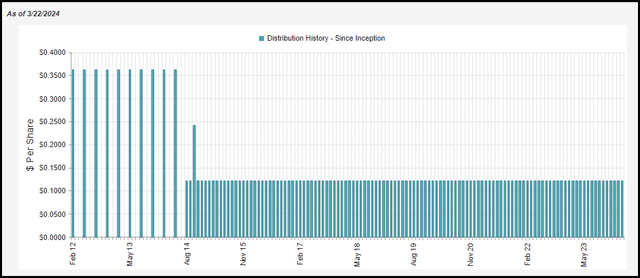

This fund has delivered the identical distribution since its inception. The caveat right here is that it was quarterly at first, however after they switched to a month-to-month schedule, they went with the month-to-month equal. With this, the fund’s newest distribution charge comes to six.81%, with a NAV charge fairly comparable at 6.57%. This could be resulting from carrying solely a shallow low cost, which implies these charges are fairly shut.

BUI Distribution Historical past (CEFConnect)

Conclusion

ASGI and BUI aren’t off to a scorching begin in 2024, like I hoped to see. That being mentioned, I nonetheless imagine their future appears brighter, however the restoration time has elongated with projections that cuts will are available in later and slower than anticipated. Over the long run, I nonetheless imagine that these two funds are fairly interesting as funding alternatives, and however, they nonetheless stay conservative choices within the utility/infrastructure area.