Kaela Lavin/iStock through Getty Photographs

Pricey Fellow Shareholders,

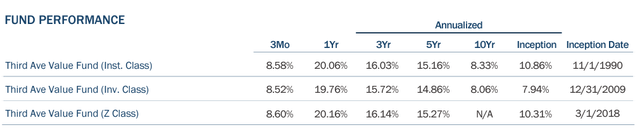

For the three months ended March 31st, 2024, the Third Avenue Worth Fund (the “Fund”) returned 8.58%, as in comparison with the MSCI World Index2, which returned 8.97%1. For additional comparability, the MSCI World Worth Index2 returned 7.65% within the first quarter. Over the trailing three- and five-year durations, the Fund has returned 16.03% and 15.16% annualized, respectively. A number of weeks in the past, our agency was grateful to be awarded the Greatest Fairness Small-Dimension Fund Household Group Over Three Years on the 2024 United States LSEG Lipper Fund Awards. These awards acknowledge “fund administration corporations which have excelled in offering persistently robust risk-adjusted efficiency relative to their friends.” This clearly didn’t occur in a single day. On the finish of 2017, our agency made a number of modifications to a few of our portfolio administration groups, together with to the group managing the Fund. The modifications had been designed to reestablish a deep dedication to our agency’s unique funding philosophy and reinvigorate an investment-centric tradition throughout the whole lot of our agency. These should not targets in themselves however, relatively, priorities and disciplines we imagine enhance the chances of manufacturing compelling returns for our agency’s shoppers, and for our personal capital, over the long run. It’s, subsequently, very gratifying to obtain this award in acknowledgement of our total agency’s efforts.

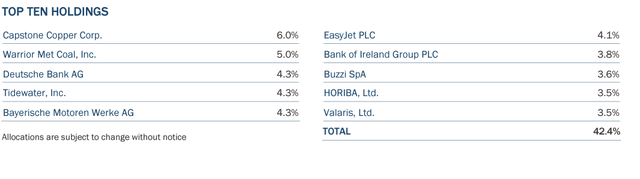

Throughout the quarter, the Fund loved robust efficiency contributions from copper mining corporations, Capstone Copper (OTCPK:CSCCF) and Lundin Mining (OTCPK:LUNMF). Lately, we now have repeatedly articulated our thesis {that a} very difficult provide scenario for copper, together with steadily growing demand for copper, was more likely to manifest in rising provide shortages, lowering international copper inventories, and better copper costs. That thesis stays unchanged and appears additional corroborated by the latest energy of copper costs, contemporaneous with giant value declines of different minerals related to vitality transition, reminiscent of lithium, cobalt, and nickel, which every have provide fundamentals far much less supportive of excessive costs. The Fund additionally benefited from robust performances by offshore vitality providers firm Tidewater (TDW), Japanese fuel flow-control and measurement firm HORIBA (OTCPK:HRIBF), and Italian-headquartered international cement firm, Buzzi (OTCPK:BZZUF)(OTCPK:BZZUY). Deutsche Financial institution (DB), seemingly amongst our extra controversial investments in recent times, additionally started the yr strongly. In the meantime, destructive efficiency contributions in the course of the first quarter had been generated by Jardine Cycle & Carriage (OTCPK:JCYCF) (OTCPK:JCYGY), Genting Singapore (OTCPK:GIGNY), Warrior Met Coal (HCC), Interfor Corp (IFP:CA), and S4 Capital (OTCPK:SCPPF). With respect to S4 Capital, a March 2024 Wall Avenue Journal article described the corporate as the topic of a number of latest takeover affords, in a single case at a proposal value showing to symbolize a a number of of the present share value. We weren’t stunned by the rumored affords, nor by Chairman Martin Sorrell allegedly rebuffing these affords as undervaluing the corporate. We, too, imagine that the corporate is probably going saleable immediately for a value nicely above the rumored supply value, though the almost certainly path ahead nonetheless seems to be for the corporate to proceed constructing a considerable quantity of future enterprise worth as an unbiased firm.

|

Efficiency is proven for the Third Avenue Worth Fund (Institutional Class). Previous efficiency isn’t any assure of future outcomes; returns embody reinvestment of all distributions. The above represents previous efficiency and present efficiency could also be decrease or increased than efficiency quoted above. Funding return and principal worth fluctuate in order that an investor’s shares, when redeemed, could also be value roughly than the unique price. For the newest month-end efficiency, please go to the Fund’s web site at www.thirdave.com. The U.S. Lipper Fund Award for Greatest Fairness Small Fund Household relies on a assessment of 185 certified fund administration corporations that had been eligible for the three-year interval ending on 11/30/23. To qualify for Lipper’s Total Small Fund Household Group Award, Small fund household teams should have no less than three fairness portfolios. The group award will likely be given to the group with the bottom common decile rating of its respective asset class outcomes primarily based on the three-year Constant Return measure of the eligible funds. |

Relating to Scalability

Common readers of our letters have not typically seen discussions about Berkshire Hathaway (BRK.A)(BRK.B) or quotes from Warren Buffett. The 2 major causes are that we do not understand there to be numerous worth in being yet another individual quoting Warren Buffett and, equally, as a result of our worth investing strategy, as was the case with our firm-founder Marty Whitman earlier than us, is essentially totally different than the one employed at Berkshire Hathaway. It’s, subsequently, value noting that the newest Berkshire Hathaway annual letter contained a strong reminder of why its capital has been managed in a selected model. Many members of the worth investing neighborhood are able to reciting Charlie Munger’s mantra of shopping for “great companies at honest costs, relatively than honest companies at great costs.” Many even deal with these phrases as a price investing Rosetta Stone of kinds. Recitations appear notably frequent amongst that phase of the worth investing neighborhood predisposed to a extra growth-focused strategy and people decided to be much less constrained by price-consciousness. It’s not an enormous psychological leap to get from “great companies at honest costs” to development at an affordable value (“GARP”).

In the meantime, the success of Berkshire Hathaway over greater than a half-century, and, individually, the resounding success of development investing methods, usually, during the last decade or so, have each inspired a palpable shift in direction of the pursuit of companies perceived to be “great” on the time of preliminary funding. One facet of the conceptual overlap stems from the truth that development can actually be an vital aspect of a beautiful enterprise. My private view is that this has left the extra conventional, price-conscious, typically contrarian, finish of the worth investing spectrum much less trafficked and considerably much less aggressive than was beforehand the case, say ten or twenty years in the past. But, on this most up-to-date letter, Buffett reminded us of the context during which Munger initially delivered his investing prescription. Again in 1965, Buffett had only recently come to manage Berkshire Hathaway. Munger believed, fairly rightly looking back, that Buffett wanted to maneuver away from the funding strategy he had been using to unimaginable success inside his funding partnership. Buffett summarized, “In different phrases, abandon every part you realized out of your hero, Ben Graham. It really works, however solely when practiced at small scale.”

That recollection touches on a number of tidal shifts coursing via the funding trade immediately. First, with out the inclusion of “It really works however solely when practiced at small scale”, Munger’s first precept of shopping for “great companies at honest costs” lacks a vital qualifier. Munger wasn’t essentially saying that purchasing “great companies at honest costs” is a essentially higher strategy to investing than shopping for “honest companies at great costs”, solely that it’s a extra possible path to success if one is charged the formidable activity of investing the large float of an insurance coverage firm. It is a essentially totally different assertion than saying it’s a superior strategy to investing in any respect scales. That these two investing deities concluded that Buffett’s partnership strategy was not sensible for investing the float of an insurance coverage firm doesn’t handle the query of which strategy is preferable for the aim of producing funding returns for a smaller pool of capital. Certainly, from time-to-time Buffett has continued to publicly lament that he would definitely be able to producing a lot bigger returns had been he not managing such a big pool of capital.

Moreover, a scalable funding technique just isn’t solely engaging to these in charge of an insurance coverage firm. It is usually extremely engaging to formidable asset administration firm executives, a lot of whom would like to preside over a big enterprise. The funding strategy employed by the Third Avenue Worth Fund is sufficiently scalable in order that it may i) be supplied to buyers at an affordable price, ii) help an skilled group, iii) make the most of a few of the trade’s highest-quality service suppliers, and iv) be an vital piece of a high-quality funding boutique. It may well’t, nevertheless, be the flagship of a giant funding agency; nor, in all probability, might it even represent a vital engine of development for such a agency? In different phrases, an awesome funding technique and an awesome funding administration enterprise are two various things, they usually occasionally overlap.

Compounding the problem, the asset administration trade has undergone wave after wave of consolidation in latest many years. An growing majority of funding {dollars} are being consolidated into corporations which might be impossible to pursue a method like Third Avenue’s, even amongst these giant corporations that stay dedicated to lively, public fairness investing methods. Our methods are simply not a scalable enterprise mannequin by trendy asset administration trade requirements. It’s, subsequently, intuitive that what stays of our aggressive peer set immediately is generally comprised of a number of different funding boutiques and a handful of value-oriented, very long-biased, non-public partnerships. In a perverse manner, all of that is excellent news. On account of an trade shift during the last decade or so in direction of approaches that emphasize investing in corporations perceived to be “great” on the time of funding, and people which seem to have favorable near-term prospects to develop, together with funding {dollars} being more and more consolidated into scalable methods, the enterprise of price-conscious, basic, worth investing does appear to have turn into lonelier and fewer aggressive of late.

Our Technique, Distilled

The essence of what we do, inside the Third Avenue Worth Fund, is to try to purchase considerably undervalued, well-financed companies which might be run by sincere and competent individuals. A possibility to purchase a considerably undervalued enterprise in public fairness markets normally derives from buyers underestimating its prospects, which often happens when one thing goes improper, investor pessimism develops, and an extreme value response happens. A darkish cloud hanging over an organization can take a number of kinds, reminiscent of a macroeconomic occasion, an industrial recession, or an idiosyncratic problem complicating life for a single firm. After all, it may be extremely tough, if not inconceivable, to foretell the timing with which such clouds will abate, and the timing can generally stretch nicely past one’s preliminary expectations. Due to this fact, we should give attention to corporations which have monetary wherewithal to hold them to higher days with out the necessity to undertake actions, reminiscent of promoting property or elevating capital at inopportune occasions, which can completely hurt the underlying worth of our funding. In difficult environments, nice steadiness sheets may also generally turn into a potent offensive weapon used to opportunistically create substantial shareholder worth. Extra on that idea seems later on this letter. In different phrases, we attempt to considerably underpay for invaluable companies whereas concurrently limiting our draw back danger, and enhancing our upside potential, via a heavy emphasis on steadiness sheet high quality and the costs we pay.

Furthermore, we have a tendency to carry about 30 positions at any given time and maintain these positions for about 5 years, on common. This portfolio construction calls for we make about 5 or 6 new investments per yr, on common, which isn’t straightforward. In the meantime, inside the universe of lively U.S. fairness mutual funds, the common fund holds nearly 100 holdings and churns these holdings at a fee of roughly 65% per yr, which implies that they make an enormous variety of new investments per yr and that the common holding interval of these investments is about 1.5 years. In spite of everything, a technique that an lively fairness technique may be made extra scalable, as mentioned above, is to personal an enormous variety of holdings, as most funds do. However that additionally calls for that the funding group give you an enormous variety of nice new funding concepts yearly, which is exceedingly tough. As an apart, if the common holding interval of 1’s technique is 1.5 years, it could be rational to keep away from companies the place the near-term outlook is difficult, even when the enterprise is clearly undervalued as a result of decision of that firm’s points could fall nicely past one’s temporary funding horizon. That is one more reason that the contrarian finish of the worth neighborhood is inherently a bit lonely.

In pursuit of undervalued bargains, we generally buy companies experiencing deep cyclical depressions, which have little or no, if any, accounting earnings on the time of our preliminary funding. These corporations would not often be described as “great” on the time of our funding. We make contrarian investments of this sort the place we understand there to be a really possible path for the trade to rebalance, permitting for improved working efficiency for the businesses capable of endure the downturn. In these conditions, we additionally take consolation when our buy value represents a reduction to our estimate of the liquidation worth of the corporate. We don’t, nevertheless, buy companies in industries we understand to be in secular decline. In different circumstances, we buy corporations which have been producing muted working efficiency in an atmosphere with some sort of headwind, however the place our buy costs are sufficiently low in order that the muted returns supply respectable earnings or money movement 6 yields, within the right here and now, and the place we imagine there to be a robust chance of enhancing working efficiency sooner or later. The excessive prevalence of this class of funding not too long ago is, in my private view, a results of the expansion and GARP fixation overwhelming fairness markets. In different phrases, there was a whole class of very wholesome and cheap, albeit slower rising, corporations, which have merely suffered from benign neglect in recent times. Lastly, we additionally buy special-situations which might be misunderstood, tough to mannequin, or altering in some vital manner. Although real special-situation alternatives may be notably tough to determine, pursuit of them has, in our view, been definitely worth the effort.

Money Flows, Low-cost Shares, And Capital Allocation

We supplied the above assessment of our technique as a result of the technique itself units the stage for the massive quantity of shareholder capital returns from Fund holdings we’re experiencing immediately. The prevalence of companies which might be concurrently i) well-capitalized and even over-capitalized, ii) performing nicely, and iii) stay cheap, has created the chance and incentives for a lot of of our corporations to supply a veritable flood of shareholder capital returns. What follows is a dialogue of how the interaction of economic place, working efficiency, and public market valuation has manifested inside one of many Fund’s present holdings, Financial institution of Eire, adopted by a number of extra abridged examples:

Financial institution of Eire (OTCPK:BKRIF)(OTCPK:BKRIY) – After we bought Financial institution of Eire in mid-2019, the financial institution was producing a return on tangible e-book worth5 of roughly 7.5%, a reasonably poor stage of profitability ensuing from a remarkably low rate of interest atmosphere and a decade of accelerating regulatory capital necessities following the World Monetary Disaster. Even then, we believed the financial institution had reached the purpose of being arguably over-capitalized, and we had been excited by the chance to purchase shares at 60% of tangible e-book worth. To this final level, the maths of paying 60% of tangible e-book worth for a corporation producing a 7.5% return on tangible fairness implies an earnings yield7, relative to our preliminary price, of about 12.5%. It is very important observe that if the corporate continued to earn a 7.5% return on fairness in perpetuity, administration illogically opted to retain all earnings inside the firm, and the corporate continued to be valued at 60% of tangible e-book worth endlessly, Financial institution of Eire would have produced a reasonably modest return for us. This risk compels our group’s emphasis on the energy of economic place, which allows the corporate to select the way it allocates capital, in addition to an appraisal of the administration group and its incentives.

As time glided by, two of Eire’s 5 largest banks determined to throw within the towel, exiting the Irish market utterly. Prospects and performing mortgage portfolios of these two banks had been largely subsumed by Financial institution of Eire and its largest peer. Business attrition of this sort is without doubt one of the ways in which industries cyclically rebalance, as talked about above. Moreover, throughout downturns, there are often alternatives for an trade’s best-capitalized rivals to construct long-term enterprise worth via counter-cyclical acquisitions or investments. The consolidation of the Irish market into three banks offered enhanced scale and an improved aggressive panorama for the remaining banks, which then loved improved returns. Equally, the unequalled steadiness sheets of each Financial institution of Eire and its largest competitor, put these two corporations in a novel place to every buy considered one of Eire’s two largest wealth administration and capital markets corporations in the course of the downturn. In doing so, they every added giant, capital-light strains of enterprise into their respective banks, producing upward step-changes in returns on fairness. After which rates of interest started to normalize, producing a tailwind for returns, relatively than a headwind, for the primary time in years.

Financial institution of Eire not too long ago reported a return on tangible fairness barely above 17% for calendar yr 2023, although it anticipates a determine nearer to 15% prospectively. Financial institution of Eire’s value to tangible e-book ratio has improved to 106%, from 60% in 2019. But, its earnings a number of has compressed over that point, to roughly 7.2x, and its earnings yield has, subsequently, elevated to roughly 14%, even after robust share value appreciation. As a result of the corporate is already overcapitalized, and its shares supply an earnings yield just like what it’s incomes on capital internally, it creates an incentive for the corporate to return a big portion of earnings, relatively than retaining them and changing into ever-more overcapitalized, which might additionally doubtless serve to depress returns on tangible e-book worth. Whereas a willingness to distribute capital could exist, as a sensible matter, a financial institution’s means to distribute capital is commonly a results of its means to acquire regulatory approval, which is a direct results of its steadiness sheet energy. If Financial institution of Eire was poorly capitalized, it might be compelled by regulators – or simply widespread sense – to retain its earnings and add them to its capital base, however that’s clearly not the scenario right here. In asserting 2023 working outcomes, Financial institution of Eire introduced a brand new capital distribution plan that successfully targets a return of 72% of 2023 earnings, as a mix of dividends and a sizeable share buyback program. These returns of capital sum to a shareholder capital return, as a share of immediately’s share value, nicely into the double-digits. The corporate arrived on the 72% distribution determine by estimating the extent of capital it anticipates needing in an effort to help continued development in lending exercise at a fee in keeping with development of the Irish financial system. Thoughts you, Eire is without doubt one of the quickest rising economies in Western Europe. All of that is to say that the financial institution anticipates that it may proceed to develop earnings, e-book worth, and enterprise worth, whereas retaining solely about 28% of earnings.

Idiosyncratic as the main points of Financial institution of Eire’s progress could also be, most of the underlying ideas are surprisingly widespread immediately. Deutsche Financial institution (“Deutsche”) shares many similarities. Its capital base and steadiness sheet have improved dramatically in recent times. Administration modifications in 2018 precipitated sweeping modifications in the way in which the financial institution is run, which, when mixed with an improved rate of interest atmosphere, have led to Deutsche Financial institution’s drastically improved working outcomes. Throughout 2023, Deutsche produced a return on tangible fairness of roughly 7%, and it presently trades at roughly 51% of tangible e-book worth, which marries with a price-to-earnings3 a number of of roughly 7x. Much like Financial institution of Eire, there may be little incentive for Deutsche Financial institution to retain a lot of its earnings and proceed to develop its capital base, except compelled by regulators to take action, so long as every Euro of retained capital is being valued at roughly 50 cents. Deutsche not too long ago introduced that it’s going to improve its dividend 5 materially in 2023, and plans to make extra, successive, 50% dividend will increase in every of the subsequent two years. The corporate additionally applied a considerable share buyback, which is extremely engaging from our long-term shareholder perspective, provided that the shares are presently valued at roughly 50% of tangible e-book worth and supply an earnings yield almost twice the financial institution’s return on fairness.

Exterior of the world of financials, Mercedes-Benz Group (OTCPK:MBGAF)(OTCPK:MBGYY) (“Mercedes”) not too long ago reported excellent working efficiency for 2023 and ended the yr with EUR 32 billion of internet money and monetary property inside its industrial enterprise (i.e., outdoors of its monetary providers enterprise). For perspective, its present market cap is roughly EUR 80 billion.

Lately, the corporate has concurrently funded giant dividends, closely invested in electrical car transition, and continued to take a position closely in its inside combustion engine autos, and nonetheless produced vital free money movement in spite of everything of that. The corporate’s steadiness sheet has advanced from being well-capitalized, to being patently over-capitalized. Administration not too long ago acknowledged as a lot when it dedicated to paying out nearly 100% of free money movement from its industrial enterprise, prospectively, within the type of dividends and buybacks. And once more, regardless that Mercedes is extremely worthwhile and presently incomes respectable returns on capital, there isn’t a have to proceed including to an already large warfare chest. On the similar time, there’s a nice alternative to purchase again shares at a big low cost to e-book worth and at roughly 5.5x trailing earnings.

Moreover, amongst our present holdings, there are numerous extra examples of corporations which might be making giant and rising shareholder distributions, and they aren’t particular to an trade or geography. An extended listing would come with Chilean holding corporations, Vapores and Quiñenco, Italian-headquartered cement firm Buzzi, auto maker BMW, U.S. insurance coverage firm Outdated Republic, and Norway-listed offshore engineering firm Subsea7.

Quarterly Exercise

Throughout the quarter ending March 31st, 2024, the Fund initiated a brand new place in Harbour Vitality plc (OTCPK:HBRIY) (“Harbour”). Harbour is an unbiased oil and fuel exploration and manufacturing firm listed on the London Inventory Change, with vital operational publicity to the U.Okay. North Sea. Based by non-public fairness agency EIG World Companions in 2014, Harbour set out with a contrarian technique to accumulate typical, producing property outdoors of North America, in the end buying offshore property within the U.Okay. North Sea from motivated sellers, together with Shell and Conoco. In 2021, the corporate was publicly listed via a reverse merger with Premier Oil.

Extra not too long ago, throughout 2023, the U.Okay. offshore oil and fuel trade suffered a significant setback by the hands of its personal authorities, which applied the U.Okay. Vitality Earnings Levy, rightly described as a windfall tax. Subsequently, European fuel costs declined considerably offering extra headwinds to the enterprise and trigger for shareholder dejectedness. In December 2023, nevertheless, Harbour introduced a transformational deal to accumulate a lot of the upstream property of Wintershall Dea AG in a fancy transaction that we imagine is more likely to create substantial worth for Harbour shareholders. Importantly, the motivating issue within the sale of Wintershall Dea’s property is that its mother or father firm, German chemical compounds large BASF (OTCQX:BASFY)(OTCQX:BFFAF), has publicly dedicated to exit the enterprise of fuel manufacturing. Nevertheless, BASF is confronted with a really restricted set of potential patrons. Anticipated to shut within the fourth quarter of 2024, the pending deal will lead to Harbour’s diversification away from the U.Okay. North Sea, in favor of Norway. Along with providing geographic diversification, the transaction may also lead to enhancements within the firm’s scale, manufacturing base, reserve life, price construction, capital depth, and credit score profile. Furthermore, as demonstrated by the pending deal, Harbour is led by an opportunistic administration group with a confirmed means to supply worth accretive acquisition alternatives, whereas sustaining a robust monetary place. Insiders retain a big fairness stake within the firm, creating alignment with outdoors shareholders.

A number of types of confusion surrounding the Wintershall Dea transaction proceed to supply a further obstacle to inventory value efficiency, albeit an obstacle we count on to be non permanent. Because of this, the Fund was capable of purchase shares at a modest a number of of our estimate of proforma money movement and a big low cost to our estimated internet asset worth.

Thanks on your confidence and belief. We sit up for writing once more subsequent quarter. Within the interim, please don’t hesitate to contact us with questions or feedback atclientservice@thirdave.com.

Sincerely,

Matthew Superb

Necessary DataThis publication doesn’t represent a proposal or solicitation of any transaction in any securities. Any advice contained herein is probably not appropriate for all buyers. Data contained on this publication has been obtained from sources we imagine to be dependable, however can’t be assured. The knowledge on this portfolio supervisor letter represents the opinions of the portfolio supervisor(s) and isn’t supposed to be a forecast of future occasions, a assure of future outcomes or funding recommendation. Views expressed are these of the portfolio supervisor(s) and will differ from these of different portfolio managers or of the agency as a complete. Additionally, please observe that any dialogue of the Fund’s holdings, the Fund’s efficiency, and the portfolio supervisor(s) views are as of March 31, 2024 (besides as in any other case said), and are topic to vary with out discover. Sure data contained on this letter constitutes “forward-looking statements,” which may be recognized by means of forward-looking terminology reminiscent of “could,” “will,” “ought to,” “count on,” “anticipate,” “challenge,” “estimate,” “intend,” “proceed” or “imagine,” or the negatives thereof (reminiscent of “could not,” “shouldn’t,” “should not anticipated to,” and so on.) or different variations thereon or comparable terminology. As a consequence of numerous dangers and uncertainties, precise occasions or outcomes or the precise efficiency of any fund could differ materially from these mirrored or contemplated in any such forward-looking assertion. Present efficiency outcomes could also be decrease or increased than efficiency numbers quoted in sure letters to shareholders. Date of first use of portfolio supervisor commentary: April 16, 2024 1 The MSCI World Index is an unmanaged, free float-adjusted market capitalization weighted index that’s designed to measure the fairness market efficiency of 23 of the world’s most developed markets. Supply: MSCI. 2 MSCI World Worth: The MSCI World Worth Index captures giant and mid-cap securities exhibiting general worth model traits throughout 23 Developed Markets (DM) nations. The worth funding model traits for index development are outlined utilizing three variables: e-book worth to cost, 12-month ahead earnings to cost and dividend yield. Supply: MSCI Three The value-to-earnings ratio is the ratio for valuing an organization that measures its present share value relative to its earnings per share (EPS). The value-to-earnings ratio can be generally often called the worth a number of or the earnings a number of. Supply: Investopedia four The dividend yield, expressed as a share, is a monetary ratio (dividend/value) that exhibits how a lot an organization pays out in dividends annually relative to its inventory value. Supply: Investopedia 5 Tangible Guide Worth – Tangible e-book worth per share (TBVPS) is a technique by which an organization’s worth is decided on a per-share foundation by measuring its fairness with out the inclusion of any intangible property. Intangible property are people who lack bodily substance, thus making their valuation a harder enterprise than the valuation of tangible property. 6 Money Move: Money movement is the web money and money equivalents transferred out and in of an organization. Money obtained represents inflows, whereas cash spent represents outflows. 7 Earnings Yield – The earnings yield refers back to the earnings per share for the newest 12-month interval divided by the present market value per share. The earnings yield (the inverse of the P/E ratio) exhibits the proportion of an organization’s earnings per share. Previous efficiency isn’t any assure of future outcomes; returns embody reinvestment of all distributions. The above represents previous efficiency and present efficiency could also be decrease or increased than efficiency quoted above. Funding return and principal worth fluctuate in order that an investor’s shares, when redeemed, could also be value roughly than the unique price. For the newest month-end efficiency, please go to the Fund’s web site at www.thirdave.com. The gross expense ratio for the Fund’s Institutional, Investor and Z share lessons is 1.20%, 1.45% and 1.11% , respectively, as of March 1, 2024. Dangers that would negatively impression returns embody: fluctuations in currencies versus the US greenback, political/social/financial instability in international nations the place the Fund invests lack of diversification, and adversarial normal market situations. The fund’s funding goals, dangers, expenses, and bills should be thought-about fastidiously earlier than investing. The prospectus comprises this and different vital details about the funding firm, and it could be obtained by calling 800-443-1021 or visiting www.thirdave.com. Learn it fastidiously earlier than investing. Distributor of Third Avenue Funds: Foreside Fund Providers, LLC. Present efficiency outcomes could also be decrease or increased than efficiency numbers quoted in sure letters to shareholders. Third Avenue affords a number of funding options with distinctive exposures and return profiles. Our core methods are at present accessible via ’40Act mutual funds and customised accounts. If you want additional data, please contact our Relationship Supervisor. |

Unique Put up

Editor’s Observe: The abstract bullets for this text had been chosen by Searching for Alpha editors.