Funtap

Written by Nick Ackerman, co-produced by Stanford Chemist

Price cuts are right here, or virtually almost right here, as September is very anticipated to see at the least a 25 foundation level minimize. That has been fueling curiosity rate-sensitive sectors reminiscent of actual property. The Cohen & Steers High quality Revenue Realty Fund (NYSE:RQI) and the Cohen & Steers Actual Property Alternatives and Revenue Fund (NYSE:RLTY) are two funds which have been benefiting from the anticipated charge cuts.

These are leveraged closed-end funds targeted on investing in largely fairness actual property funding trusts (“REITs”) but additionally carry sleeves of most popular and different fixed-income holdings. Most popular and fixed-income investments ought to profit as effectively from a decrease charge surroundings if risk-free charges proceed to development decrease as effectively. Whereas they have been on a stable run already forward of the particular charge minimize occasion, I imagine that every of those funds has extra upside to them.

Cohen & Steers High quality Revenue Realty Fund

- 1-Yr Z-score: 0.88

- Low cost/Premium: -4.66%

- Distribution Yield: 7.21%

- Expense Ratio: 1.40%

- Leverage: 29.74%

- Managed Belongings: $2.5 billion

- Construction: Perpetual

RQI’s funding goal is to supply a “excessive present earnings.” In addition they have a secondary funding goal of “capital appreciation.” They’ll spend money on “actual property securities together with frequent shares, most popular shares and different fairness securities of any market capitalization issued by actual property corporations, together with actual property funding trusts (REITs) and related REIT-like entities.”

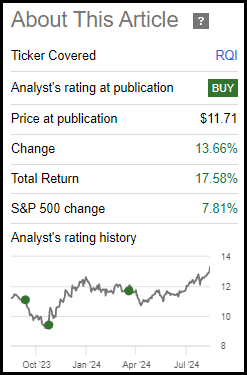

The sturdy run in REITs has seen RQI clawing again losses they skilled when the Fed raised charges. Since our final replace earlier this yr, RQI has delivered a complete return of over 17%—simply outpacing the S&P 500 Index throughout this time. Although the S&P 500 Index is not an applicable benchmark, it might nonetheless assist present some context of the general monster transfer.

RQI Efficiency Since Prior Replace (Searching for Alpha)

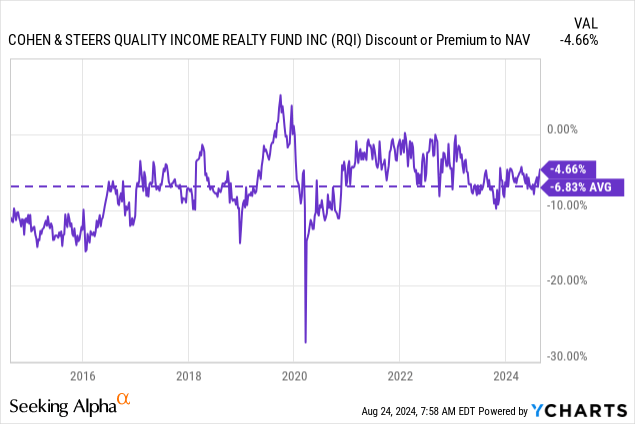

I imagine there’s nonetheless extra to go and the low cost nonetheless has some attraction right here as effectively. In reality, the low cost hadn’t narrowed an excessive amount of since our final replace, which means the returns delivered that we see above have been primarily fueled by the precise underlying efficiency of the portfolio.

Over the long run, the -4.66% low cost offered in opposition to its common nearer to -7% means that it’s not a discount. Our precise “Purchase Beneath Low cost” goal is -5%, so we’re fairly shut.

Ycharts

Additional, given the expectation that I imagine the REIT area will do effectively, this is without doubt one of the situations the place I am prepared to view it as a pretty alternative nonetheless. If the fund moved to a premium, I might be a bit extra cautious, however we aren’t essentially wildly overvalued or something on RQI.

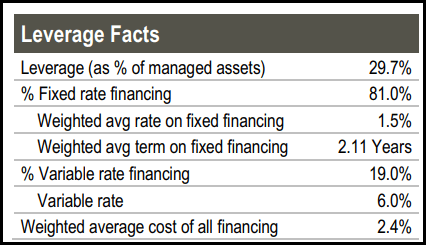

With decrease charges anticipated, that not solely helps the underlying portfolio as a result of REITs turn out to be a extra enticing earnings different but additionally will assist ease among the borrowing prices for RQI. Whereas RQI had hedged a good portion of its borrowing prices, these would not final perpetually. Charges are coming down in time for RQI to refinance under the height of the present charge cycle.

Then again, charges nonetheless aren’t anticipated to return to zero, which suggests they are going to nonetheless see larger charges, simply not as excessive as in the event that they hadn’t hedged themselves. The times of mounted financing at 1.5%, as RQI has had on a majority of its borrowings, in all probability aren’t coming again until we see a black swan occasion — which might have its personal unfavorable penalties for the REIT area.

RQI Leverage Stats (Cohen & Steers)

As we are able to see, the variable charge got here in at 6%. That is been fairly frequent from what we have seen in different funds that make the most of floating-rate borrowings. For each 25 foundation level discount from the Fed, that ought to immediately see a 25 bp drop for borrowings. It’s because they’re borrowing based mostly on SOFR plus a variety for his or her credit score facility.

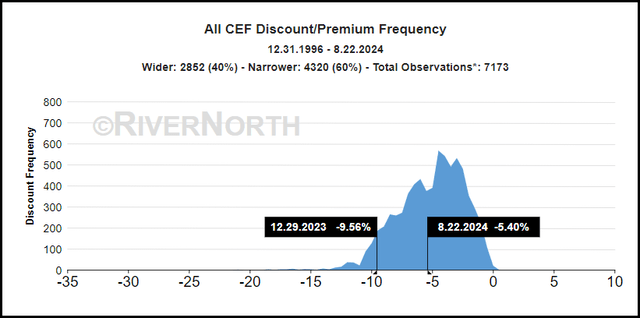

Normally, most closed-end funds are leveraged and beneath a decrease charge surroundings — not anticipated to be zero, to reiterate — that may make CEFs look comparatively extra enticing.

Total, that may very well be one of many explanation why we have been seeing reductions slender throughout the board. Then once more, since 1996, CEF reductions have been narrower 60% of the time.

CEF Low cost/Premium Historical past Vs. Present Common (RiverNorth)

REITs make use of their very own leverage as effectively, and it’s usually based mostly on mounted charges for a good portion of the borrowings; in a better charge surroundings, they nonetheless need to pay larger mounted charges relating to refinancing or seeking to develop extra by means of debt issuance. In order that’s why decrease charges profit REITS as effectively, and subsequently, profit RQI’s underlying portfolio.

Talking of the underlying portfolio, the fund invests with a tilt towards extra growth-oriented REITs, versus what may very well be thought of the high-yield REIT basket. The place they lack sizeable yields, they usually ship some dividend development.

RQI High Ten Holdings (Cohen & Steers)

In fact, there are at all times exceptions; American Tower Corp (AMT) and Crown Fort (CCI) have frozen their dividends the place they’re in the intervening time, although hopefully, that is solely a short lived freeze. AMT is on trajectory to return to dividend development in 2025, and so they’ve indicated they count on to as effectively.

So, that is sort of the way in which we give it some thought. We’d count on that the dividend development would resume in 2025 based mostly on what we’re seeing within the numbers going past 2024.

CCI, however, would not sound as assured, but it surely does include a considerably larger dividend yield at 5.57%. (Bolding added to emphasis the principle level.)

Ari Klein, BMO Capital Markets

Thanks. After which perhaps you talked somewhat bit about elevated flexibility which incorporates the steadiness sheet and perhaps bringing leverage decrease. May that in some unspecified time in the future, embody shifting the dividend technique and the way you concentrate on that?

Daniel Schlanger, Crown Fort CFO

Sure. I believe given the truth that we’re in the course of the strategic evaluate which would come with the thought round capital allocation, dividend coverage, every thing else in the end. We’re actually not in an excellent place to speak about what is going on ahead till we have now extra of a conclusion on what companies we have now and the place we’re going to be sooner or later.

The primary takeaway from taking a fast have a look at the highest ten, although, is that development is vital since RQI will gas most of its distribution to traders by means of capital features. They’ve maintained the identical $0.08 month-to-month payout for a few years now, which incorporates by means of Covid and the most recent charge mountaineering cycle.

RQI Distribution Historical past (CEFConnect)

The present distribution charge works out to 7.21%; on an NAV foundation, it is available in at 6.88%, a bit decrease due to the low cost. I imagine it is a wholesome payout degree, and we should not count on to see a distribution minimize. In fact, that comes with the same old caveat of barring any kind of important market downturn for an prolonged time frame.

Cohen & Steers Actual Property Alternatives and Revenue Fund

- 1-Yr Z-score: 0.52

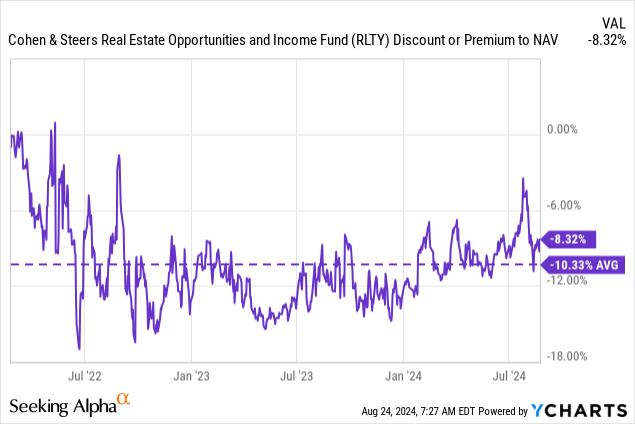

- Low cost/Premium: -8.32%

- Distribution Yield: 8.38%

- Expense Ratio: 1.74%

- Leverage: 34.93%

- Managed Belongings: $417 million

- Construction: Time period (anticipated liquidation date February 23, 2034)

RLTY’s funding goal is “excessive present earnings.” The secondary goal is for “capital appreciation.” To attain this, the fund will make investments “at the least 80% of its managed belongings in (i) actual estate-related investments, and (ii) most popular and different earnings securities.” That is fairly simple and fairly much like Cohen & Steers’ different actual estate-focused funds.

RLTY is one other fund from the identical fund household that’s benefiting equally to RQI. This is able to be largely anticipated as a result of the fund invests equally to its older and bigger sister fund. Since our final replace, RLTY has additionally been performing effectively. Extra particularly, this era is measuring from March 22, 2024. After we appeared on the RQI efficiency since our final replace above, it was from March 27, 2024.

RLTY Efficiency Since Prior Replace (Searching for Alpha)

RLTY is buying and selling at a reduction that’s wider than RQI, which may make it a extra fascinating guess. That’s the reason I wished to the touch on RLTY for traders prepared to take a little bit of an opportunity on a comparatively newer fund in comparison with the extra established RQI.

RLTY had its regular drop to a big low cost after a CEF launch, exacerbated by the unfavorable market situations for leveraged REIT CEFs. It additionally lately noticed its low cost slender considerably, solely to widen again out. Being a comparatively smaller fund, it may see some extra volatility in its low cost/premium in comparison with RQI, because it typically will not take as a lot to maneuver it.

Ycharts

One distinction between RQI and RLTY is that RLTY is a time period fund with an anticipated termination date. As we’re fairly a bit away from that anticipated liquidation, that is not an excessive amount of of a key issue at this level.

As a substitute, for now, the place the funds primarily differ is of their fairness/mounted earnings weightings. RQI is at a weighting of 80/20% between fairness and stuck earnings. RLTY is nearer to 69% invested in equities and 31% in most popular/fixed-income. There may be additionally the group’s different leveraged sister fund, Cohen & Steers REIT and Most popular and Revenue Fund (RNP), which carries a portfolio break up between 51% equities and 49% most popular and fixed-income.

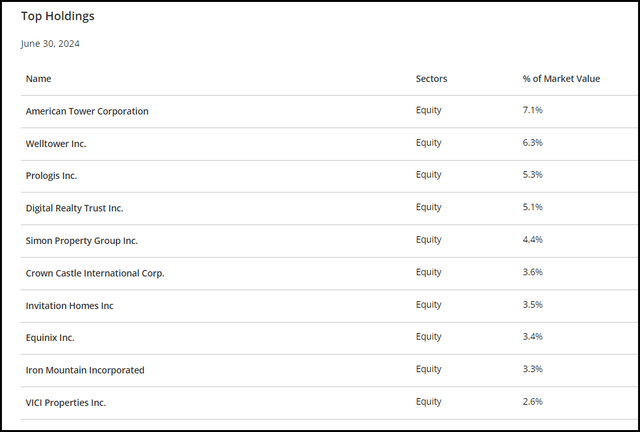

The entire high ten holdings are the identical as RQI however with some totally different proportion weighting that adjustments up the order a bit.

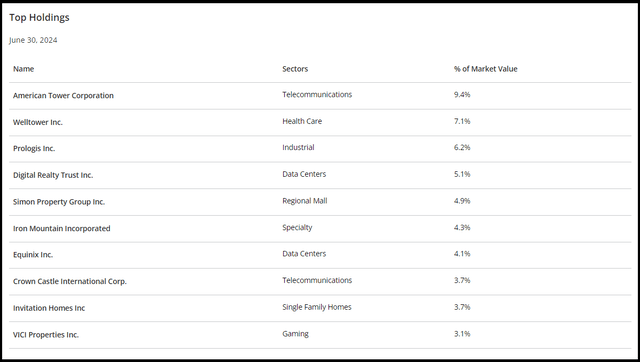

RLTY High Ten Holdings (Cohen & Steers)

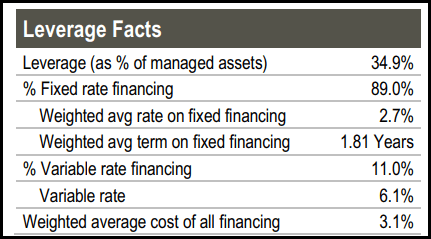

Different variations that influence efficiency are RLTY’s larger expense ratio and utilizing a bit extra leverage. The fund’s inception date was additionally early 2020, which impacted the leverage prices of the fund. Whereas they largely hedged themselves with mounted charges, it got here in at a median mounted financing of two.7% in comparison with RQI’s 1.5%.

RLTY Leverage Stats (Cohen & Steers)

Given the upper leverage and bills, and even slight variations within the portfolios, it has resulted in RLTY being a comparatively weaker performer since its inception.

Ycharts

On a complete share value return, we see that the fund delivered unfavorable outcomes because it slipped to a reduction. That is fairly regular, however the principle takeaway right here could be the overall NAV return slippage as effectively. The fund’s heavier utilization of leverage seemingly noticed higher strain to the draw back through the troublesome instances. The upper expense ratio additionally immediately takes away from complete returns as effectively.

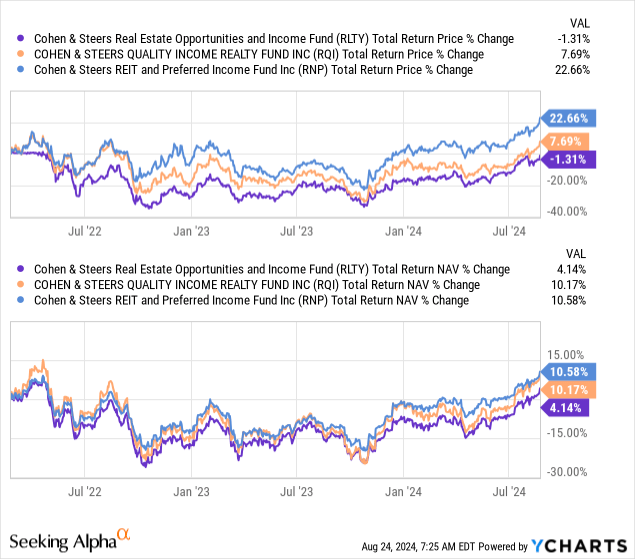

I do know most traders will have a look at that chart above after which write off RLTY and simply wish to keep on with tried and true RQI. I get it; RQI is my largest single funding throughout all my accounts, and I’ve loads of confidence over the long run within the fund.

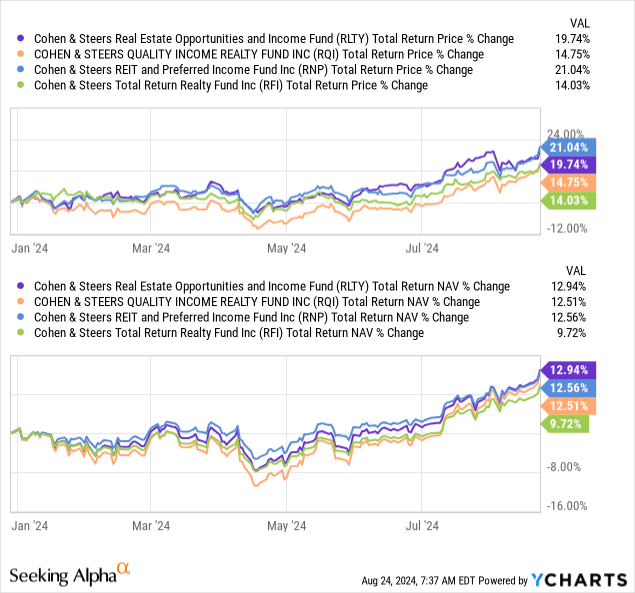

Nevertheless, I additionally maintain RLTY. It was off to a tough begin, but it surely appears to be discovering its stride extra lately. On a YTD foundation, the fund has been way more aggressive in opposition to its sister funds. RNP was the strongest performing fund by means of many of the yr, with RQI being the laggard of the trio. It was RLTY within the center earlier than having the ability to edge out its sisters on a complete NAV return foundation extra lately.

Ycharts

I’ve even included the Cohen & Steers Whole Return Realty Fund (RFI) as a result of if I did not, folks would ask why. RFI is a non-leveraged clone of RQI, principally. So naturally, we see that RFI has been the laggard as the opposite funds profit from the stronger returns boosted by their leverage utilization.

Going ahead, the upper expense ratio for RLTY in comparison with its sister funds will at all times be a slight drag. Nevertheless, with a extra enticing low cost, that minor distinction may very well be overcome doubtlessly by means of some additional low cost narrowing. The fund’s larger utilization of leverage may additionally assist the fund proceed to carry out higher in a rate-cutting surroundings.

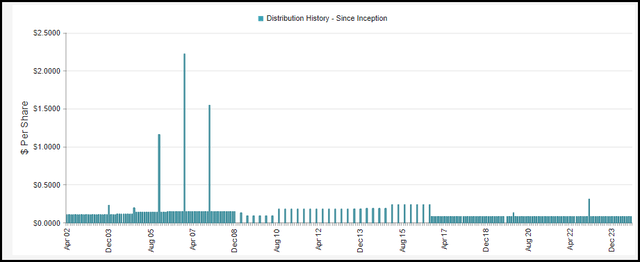

For RLTY’s month-to-month distribution, the fund had paid $0.1040, which they lifted to $0.11 per thirty days. That places the present distribution charge at 8.38%, with a NAV charge of seven.68%.

RLTY Distribution Historical past (CEFConnect)

Conclusion

With charge cuts anticipated within the close to time period, REITs have been blasting larger, and that is translated into closed-end funds reminiscent of RQI and RLTY to carry out very well. They’ve each carried out strongly since our earlier articles earlier this yr, however I imagine they nonetheless have some extra to go too.

Being leveraged funds, they will profit extra considerably in a good surroundings for REITs. In fact, that additionally comes with higher dangers and including leverage to REITs, that are already leveraged themselves, means they would not be for risk-averse traders.

Those that can deal with the volatility and elevated dangers may additionally doubtlessly see higher reward as effectively. The funds are nonetheless buying and selling at low cost ranges to their NAV per share, which is also one other approach that these CEFs may outperform. RLTY seems to be like the very best deal on this entrance, however it’s the newer fund. With RQI buying and selling above its longer-term common low cost, it would not appear to be a discount, however I am prepared to nonetheless view it favorably based mostly on the anticipated advantages of a lower-rate surroundings.