Basic Electrical (NYSE:GE) is a extremely cyclical industrial conglomerate with important revenue danger throughout an financial downturn, which isn’t mirrored within the firm’s FCF/earnings a number of.

Even if Basic Electrical reported robust earnings within the fourth quarter attributable to a restoration within the Aerospace section, I imagine the inventory has risen too far.

On condition that Basic Electrical’s enterprise is very cyclical, and that the free money move forecast for 2023 is lower than spectacular, I imagine that the valuation a number of doesn’t adequately replicate Basic Electrical’s cyclical revenue dangers in a down economic system.

Higher-Than-Anticipated Fourth Quarter Earnings

Basic Electrical reported 4Q-22 (adjusted) earnings per share of $1.24 versus $1.15 anticipated, so GE delivered a pleasant revenue beat for its fourth quarter amid, primarily, a rise in demand from the airline business. It was Basic Electrical’s third revenue beat within the final 4 quarters.

Earnings (Basic Electrical)

GE Aerospace Earnings From A Restoration In The Airline Business

Basic Electrical’s fourth-quarter earnings have been bolstered primarily by the Aerospace section, which benefited from recovering journey business demand following Covid-19.

By way of gross sales progress, Basic Electrical’s Aerospace section carried out greatest within the fourth quarter, whereas the Renewable section continued to battle. Aerospace noticed 22% YoY natural order progress and 23% YoY gross sales progress because the business recovered from the worst downturn since November 9, 2001.

Renewables continued to underperform, with gross sales falling 13% YoY to $13.zero billion. Energy had an honest (however not spectacular) fourth quarter, with gross sales growing by 2% YoY to $16.Three billion. GE Healthcare was spun off in January and now trades as a stand-alone entity.

2022 Working Segments Outcomes (Basic Electrical)

GE Aerospace Is Driving The Firm’s Free Money Move Development

The airline business’s restoration and the resumption of air journey have resulted in a big enhance in Basic Electrical’s free money move in 2022. The conglomerate earned $4.Three billion in free money move within the fourth quarter, which was greater than it earned within the earlier three quarters mixed.

Basic Electrical’s free money move in 2022 totaled $4.eight billion, representing a 152% enhance YoY. The Aerospace section of Basic Electrical was crucial supply of this free money move, as proven within the section breakdown under.

2022 Free Money Move (Basic Electrical)

Extreme Valuation A number of For A Cyclically Weak Conglomerate

On the time of writing, Basic Electrical’s inventory is buying and selling at $81 per share. With the market anticipating $2.32 per share in earnings this 12 months, GE trades at a P/E ratio of 34x, which is somewhat excessive provided that Basic Electrical is a extremely cyclical conglomerate enterprise.

Earnings Estimate (Yahoo Finance)

Basic Electrical can be dear by way of free money move, with the conglomerate anticipating $3.Four billion to $4.2 billion in free money move in 2022.

GE is valued at 23x free money move primarily based on the midpoint of steering, $3.eight billion, and a market worth of $87 billion. That is costly for a cyclical conglomerate.

Along with the valuation concern that I see for Basic Electrical, I imagine the chart profile is troubling. In keeping with the Relative Energy Index, which at present stands at 73.84, Basic Electrical’s inventory is now overbought.

A worth for the RSI above 70 is usually thought to be a contrarian promote sign, indicating that the market has grow to be overly optimistic about GE within the quick time period, and that optimism could have gone too far. The technical state of affairs means that traders train warning and hedge their draw back danger.

Relative Energy Index (Stockcharts.com)

Why Basic Electrical May See A Greater Valuation

Aversion to a U.S. recession and continued power within the Aerospace section have the potential to spice up Basic Electrical’s inventory value. Persistently excessive demand for jet engines and energy generators could help Basic Electrical’s enterprise for some time longer, however valuation multiples will ultimately attain a restrict.

As I said all through the article, Basic Electrical’s free money move and earnings in 2023 are already costly, making the danger/reward relationship unappealing.

My Conclusion

Basic Electrical had a great fourth quarter, thanks primarily to the Aerospace section. Recovering jet engine demand in a depressed market resulted in robust order and gross sales progress for GE in 4Q-22, in addition to greater free money move. With that mentioned, I imagine traders ought to proceed with warning for a wide range of causes.

First, the Relative Energy Index signifies that Basic Electrical’s inventory is overbought. Second, I imagine GE is overvalued, with a P/E ratio of 34x and a P/FCF ratio of 23x. Third, GE stays a cyclically uncovered conglomerate with important revenue danger in a downmarket.

All issues thought of, I imagine Basic Electrical is due for a draw back correction, and traders needs to be cautious to not overpay for GE’s progress.

Shares on Friday seemed able to retreat a smidgeon as Wall Road closes out the week.

That’s OK, the S&P 500 SPX is already up 5.75% in 2023, helped by the assumption that slowing financial system and softening inflation will enable the Federal Reserve to be much less aggressive in elevating borrowing prices.

This has meant that considerably poor financial knowledge is usually effectively acquired by fairness traders. (Catastrophically unhealthy financial information could also be a distinct matter!).

That correlation could also be put to the take a look at once more subsequent week when the Fed is predicted to ship a 25 foundation level charge hike, adopted by a press convention with Chairman Jay Powell.

However inventory bulls who hope to search out alerts the central financial institution will quickly cease tightening coverage might want to suppose once more. That’s the warning from Citi’s quantitative international macro strategist Alex Saunders, who says traders should brace for a shift in market responses.

“U.S. fairness market response to financial surprises proper now could be that unhealthy information is sweet for markets. This is likely one of the finest regimes for U.S. equities. This correlation between information circulation and fairness markets is typical throughout mountain climbing cycles,” he says.

Saunders studied Citi’s financial shock index and its relationship to inventory market motion, and overlaid that with the financial coverage cycle.

The chart beneath reveals the imply returns in 4 regimes. The perfect regime, says Saunders, is with optimistic financial surprises, and a optimistic fairness/shock correlation, which occurs 34% of the time.

Supply: Citi.

The worst end result is when the market will get good financial information and fairness/bond correlations are adverse, which occurs 18% of the time.

Nevertheless: “The present studying on Citi’s financial surprises index is -15 and the correlation between surprises and returns is adverse – markets have tended to react positively to a weaker shock index.”

The seemingly motive is equities search aid from the top of mountain climbing cycles.

However this relation tends to flip as soon as the Fed goes on maintain, “Because the mountain climbing cycle matures, the correlation between financial surprises and U.S. fairness market efficiency may flip optimistic. On this case, weak financial knowledge from a possible 2H U.S. recession would weigh on markets”.

Supply: Citi.

Such a transition to a regime the place unhealthy information is unhealthy information “might be the signal that the bear market rally is fading -– for instance, the sell-off after weak retail gross sales numbers earlier this month”.

The truth is, Saunders can see the market portray itself right into a nook.

“Moreover, a string of optimistic financial releases would additionally give us pause in equities, because the Fed may see this as a inexperienced mild to tighten monetary circumstances additional,” he says.

“The slender path for equities is both to proceed buying and selling unhealthy information in hope of a Fed pivot, or for recession fears to fully recede, inflation to proceed falling, and good financial information to turn into good market information once more,” he concludes.

(For extra on how telling financial surprises will be see The Chart, beneath).

Markets

Inventory futures ES00 YM00 are tilting south, led by Nasdaq-100 futures NQ00 after poorly-received outcomes from Intel. The 10-year Treasury yield BX:TMUBMUSD10Y is up 5 foundation factors to three.547%, whereas the greenback DXY is flat, gold GC00 is softer and crude CL is perkier, up 1.2% to $81.98 a barrel.

For extra market updates plus actionable commerce concepts for shares, choices and crypto, subscribe to MarketDiem by Investor’s Enterprise Day by day.

The thrill

Intel INTC shares are down practically 10% in premarket motion after the chip maker late Thursday reported– a giant fourth-quarter miss, and a dark forecast.

Be careful at 8:30 a.m. Jap for the PCE value index report. It’s the Fed’s most well-liked inflation measure and is prone to have an effect on the central financial institution’s considering because it prepares to ship its financial coverage resolution subsequent Wednesday.

Additionally to return on Friday: actual disposable incomes and actual client spending for December might be launched at 8:30 a.m., adopted at 10 a.m. by the College of Michigan client sentiment index alongside 1-year and 5-year inflation expectations, all for January. December pending residence gross sales are due at 10 a.m. All instances Jap.

The sell-off in shares of corporations linked to Gautam Adani, Asia’s richest man, continued on Friday after hedge fund titan Invoice Ackman lent his assist to Hindenburg Analysis, the quick vendor who this week revealed a important report into the Adani empire’s actions.

American Categorical AXP inventory is up 5% premarket after delivering better-than-expected outcomes and boosting the dividend.

Shares in Hasbro HAS are down practically 4% after the toy maker mentioned it plans to put off about 15% of its workforce and warned Wall Road of a loss and income drop after a disappointing vacation season.

Chevron’s inventory CVX is down 1% after the oil and gasoline large missed fourth-quarter revenue expectations, whereas income rose above forecasts.

Better of the online

How Russia’s warfare on Ukraine modified the worldwide oil commerce.

Addressing the “Smoothie Delusion”: huge tech slashes workplace perks.

Meet the newest housing-crisis scapegoat.

The chart

German shares have been doing effectively of late. The DAX 40 was up 14.6% over the previous three months at Thursday’s shut, whereas the S&P 500 has gained 6.6%.. The chart beneath from Deutsche Financial institution partly explains the distinction. Sliding vitality prices in Europe over the winter, and extra not too long ago the opening up of China’s financial system, have made German enterprise leaders extra optimistic, feeding into financial knowledge.

It’s surprises that the majority transfer markets. And the Eurozone knowledge has been extra positively stunning than these within the U.S.

“The massive query for 2023 is whether or not the momentum in Europe and China and the current loosening of world monetary circumstances might help offset some very worrying current U.S. knowledge. It’s potential that the worldwide financial system is normalising from the shock of the Ukraine warfare and China’s zero COVID coverage and that this may assist the U.S. within the close to time period,” mentioned Deutsche strategist Jim Reid.

Supply: Deutsche Financial institution.

Prime tickers

Right here had been essentially the most energetic stock-market tickers on MarketWatch as of 6 a.m. Jap.

Random reads

Gold coated mummy.

Bear takes 400 selfies.

Lottery winner blew $50 million in simply Eight years.

Have to Know begins early and is up to date till the opening bell, however enroll right here to get it delivered as soon as to your e mail field. The emailed model might be despatched out at about 7:30 a.m. Jap.

Take heed to the Greatest New Concepts in Cash podcast with MarketWatch reporter Charles Passy and economist Stephanie Kelton

In search of Alpha’s transcripts workforce is liable for the event of all of our transcript-related tasks. We at the moment publish hundreds of quarterly earnings calls per quarter on our web site and are persevering with to develop and broaden our protection. The aim of this profile is to permit us to share with our readers new transcript-related developments. Thanks, SA Transcripts Workforce

The mass capturing in Monterey Park, Calif., shocked the Asian-American neighborhood.

Not solely as a result of the capturing occurred on Lunar New Yr’s Eve, but in addition as a result of it occurred in Monterey Park, a predominantly Asian metropolis that holds a particular place within the Asian-American panorama.

On Saturday evening, a gunman opened hearth at a celebration contained in the…

Inventory futures are treading water forward of an essential week for earnings, with the highlight on updates from the tech house, which has been shedding 1000’s of staff.

Amongst these not anticipating excellent news within the earnings pipeline is Morgan Stanley’s chief U.S. fairness strategist Mike Wilson, who in our name of the day says buyers must watch out for the “bear market corridor of mirrors.”

A reasonably upbeat begin for shares to the 12 months — the S&P 500 SPX is up over 3% this 12 months, and the beaten-down Ark Innovation ETF ARKK has jumped 17% — just isn’t tempting him. “Suffice it to say, we’re not biting on this current rally as a result of our work and course of are so convincingly bearish on earnings,” mentioned Wilson.

He notes how the early 2023 rally has been led by “low-quality and closely shorted shares” and a powerful shift to cyclicals versus defensives. “This cyclical rotation particularly is convincing buyers that they’re lacking the underside and should reposition,” he informed shoppers in a Sunday notice.

However he warns that bear markets can idiot a lot of buyers earlier than all is claimed and completed, they usually should maintain trusting their very own processes and ignore the noise. “The ultimate phases of the bear market are at all times the trickiest and we have now been on excessive alert for such head fakes, just like the rally from October to December we anticipated and traded,” Wilson mentioned.

After a “very difficult 2022, many buyers are nonetheless bearish essentially, however query whether or not destructive fundamentals have already been priced into shares,” he says. “Our view has not modified as we count on the trail of earnings within the U.S. to disappoint each consensus expectations and present valuations.”

One space of concern for him is that the hole between the financial institution’s earnings outlook and ahead estimates is “as extensive because it’s ever been. The final two occasions our mannequin was this far under consensus the S&P 500 fell by 34% and 49%,” he mentioned.

Morgan Stanley

What Wilson expects is an “imminent” earnings recession, and with that margin erosion. That may come as prices have been rising quicker than gross sales, and income has been unexpectedly slowing down for firms, he mentioned.

And whereas we aren’t formally in a recession, the fallout for firms is already there — falling gross sales driving stock bloat and fewer productive head depend.

Saying all that, Wilson says they “welcome the sentiment and positioning over the previous few weeks as a essential situation for the final stage of this bear market to play out.”

The chief fairness strategist, who appropriately predicted the path of the 2022 stock-market selloff, warned firstly of the 12 months {that a} recession shock this 12 months might drive one other 22% drop for markets. In relation to Wall Road’s predictions for the S&P 500 this 12 months, Wilson is on the decrease finish with a name for the index to complete at 3,900.

U.S. Treasurys at ‘important level’: Shares, bonds correlation shifts as fixed-income market flashes recession warning

The markets

MarketWatch

Inventory futures ES00 YM00 NQ00 are leaning south, whereas there’s little motion forTreasury bonds BX:TMUBMUSD10Y BX:TMUBMUSD02Y both, however weak spot for the greenback DXY. A lot of Asia is shut — China markets will likely be closed all week for the Lunar New 12 months’s holidays. The Nikkei 225 index JP:NIK gained.

Bitcoin BTCUSD topped $23,00zero over the weekend, a stage it hasn’t seen since September regardless of final week’s Chapter 11 chapter submitting by Genesis World Capital.

For extra market updates plus actionable commerce concepts for shares, choices and crypto, subscribe to MarketDiem by Investor’s Enterprise Day by day. And observe MarketWatch’s stay weblog for extra market updates.

The thrill

Evoquoa inventory AQUA is up 17% in premarket buying and selling after the water therapy firm acquired a $7.5 billion supply from rival Xylem XYL, whose shares are down 9.2%.

Prepare for some massive tech names to report this week — Microsoft MSFT, 3M MMM and Texas Devices on Tuesday, Tesla TSLA and IBM IBM on Wednesday and Intel INTC on Thursday. GE GE, Johnson & Johnson JNJ, 3M MMM, Boeing BA, McDonald’s MCD, Visa V, Chevron CVX and AmEx AXP may also report.

Genius Group, the Singapore-based training expertise firm whose shares have soared 800% this 12 months, has set steering for 2023, saying it sees income 27% larger than 2022 and 30% larger scholar numbers.

Earnings Watch: Microsoft, Tesla and Intel are about to face the doubters

Spotify Know-how SPOT added to a wave of tech layoffs, with the music streamer asserting plans to chop 6% of its workforce.

And: Massive Tech layoffs usually are not as massive as they seem at first look

Main financial indicators are due at 10 a.m.

Learn: A recession is coming, economists say. Some even suppose it’s already right here

Ken Griffin’s U.S. hedge fund Citadel made a report $16 billion final 12 months (publish charges) final 12 months, in accordance with this estimate.

Better of the online

Practically rich sufficient to purchase the White Home. That’s incoming Biden chief of employees Jeffrey Zients

A 70% tax on the rich ought to even up the inequality hole, says Nobel-prize profitable economist Joseph Stiglitz.

Pandemic-era free lunches are ending for a lot of households, who nonetheless desperately want them

Brazil and Argentina are reportedly laying the groundwork for a standard forex (subscription required)

The chart

“An astounding 40% of Russell 2000 firms have been unprofitable final 12 months. It’s a must to surprise what’s going to occur to those firms in a world the place larger rates of interest could imply better rationing of capital vs the freely and cheaply out there flood of funding of many of the previous decade,” says Callum Thomas, head of analysis at Topdown Charts, offering the under chart from @MichealAArouet

@MichaelAArouet

“Throw in a potential international recession and issues might get ugly. No surprise fund managers are rotating out of U.S. equities,” he mentioned, pointing to this Financial institution of America chart:

Financial institution of America/@Callum_Thomas

The tickers

These have been the top-searched tickers on MarketWatch as of 6 a.m. Japanese:

Ticker

Safety identify

TSLA

Tesla

BBBY

Mattress Bathtub & Past

GME

GameStop

GNS

Genius Group

HLBZ

Helbiz

AMC

AMC Leisure

MULN

Mullen Automotive

AAPL

Apple

NIO

NIO

APE

AMC Leisure Holdings most popular shares

Random reads

“Mattress Mack” misplaced $2 million on the Dallas Cowboys and that’s not even his greatest guess.

Senior aide to Japan’s prime minister apologies for sticking his arms in his pockets throughout a DC journey, after getting informed off by his mother.

Scorching canine crime on the Australian Open

Must Know begins early and is up to date till the opening bell, however join right here to get it delivered as soon as to your e mail field. The emailed model will likely be despatched out at about 7:30 a.m. Japanese.

Hearken to the Greatest New Concepts in Cash podcast with MarketWatch reporter Charles Passy and economist Stephanie Kelton.

lucky-photographer/iStock through Getty Photographs

Introduction

The Weekly Breakout Forecast continues my doctoral analysis evaluation on MDA breakout picks over greater than Eight years. This excessive frequency breakout subset of the completely different portfolios I often analyze has now reached 290 weeks of public picks as a part of this ongoing dwell forward-testing analysis. The frequency of 10%+ returns in every week is averaging over 4x the broad market averages prior to now 5+ years.

In 2017, the pattern dimension started with 12 shares, then Eight shares in 2018, and at members’ request since 2020, I now generate solely Four picks every week. As well as 2 Dow 30 picks are offered utilizing the MDA methodology, however I extremely advocate the month-to-month Progress & Dividend mega cap breakout portfolios if you’re in search of bigger cap picks past solely 30 Dow shares.

As long-term buyers know, you may compound $10,00Zero into $1 million with 10% annual returns in lower than 50 years. This mannequin serves to extend the speed of 10% breakouts into 52 weekly intervals as an alternative of years. In 2022, the worst market since 2008: 113 MDA picks gained over 5%, 52 picks over 10%, 22 picks over 15%, and 13 picks over 20% in lower than week. Since weekly picks started in 2017 greater than 450 picks have gained over 10% in lower than every week from launch to members each Friday.

2023 Market Outlook

All new long-term portfolio picks for 2023 have began!! See the person inventory launch articles for extra particulars. To date the long-term portfolios are additionally beating main indices.

VMBreakouts.com

My technique for 2023 is to remain bullish on China as the biggest financial system nonetheless in QE and stimulating their markets, whereas all different main economies are in QT combating inflation. I plan to chubby US treasuries/bonds as defined within the 2023 technical forecast article whereas remaining cautious on US shares following the gauge indicators. As I wrote this week a few February market reckoning, I’ve change into extra bearish on US markets as we strategy February cyclical sample and Fed FOMC price hike on Feb. 1st.

Mid-year 2023 is the place issues could get attention-grabbing with potential for a Fed pivot. Dip-buyers will proceed to attempt to pull this anticipated pivot occasion ahead in time extending excessive market volatility whereas the Fed hikes charges. Mid-year I additionally plan to leverage sturdy outcomes from a brand new June Russell Reconstitution anomaly we discovered final 12 months that’s actively tracked on the dashboard: FTSE Russell Reconstitution Anomaly Research – Sturdy +22.7% Distinction After 5 Months

The schedule of studies and forecast articles for 2023 are right here in your profit.

Momentum Gauges® Stoplight forward of Week 4

All of the Every day Momentum Gauges proceed constructive this week after peaking on the highest ranges since August 2022 in what could have been a market prime on Jan. 17th. The weekly gauge continues constructive and month-to-month indicators stay unfavorable from early December however shifting nearer to a constructive sign.

app.VMBreakouts.com

Every day Momentum Gauges proceed constructive to the very best ranges since final August. Now we have not seen constructive gauge ranges maintain at these excessive ranges for very lengthy over the previous two years. Final 12 months we did not get an official unfavorable sign till after the market had a brief bear rally then dropped very sharply. There could also be sturdy similarities within the gauges with the August 2022 peak and excessive volatility.

app.VMBreakouts.com

Weekly Breakout Returns

The 2 weekly breakout portfolios are proven beneath with present 2023 returns. The continuing competitors between the Bounce/Lag Momentum mannequin (from Prof Grant Henning, PhD Statistics) and MDA Breakout picks (from JD Henning, PhD Finance) are proven beneath with / with out utilizing the Momentum Gauge buying and selling sign. The per-week returns equalize the comparability the place there have been solely 16 constructive buying and selling weeks final 12 months utilizing the MDA buying and selling sign (unfavorable values beneath 40).

VMBreakouts.com

For 2022, the worst market since 2008: 113 MDA picks gained over 5%, 52 picks over 10%, 22 picks over 15%, and 13 picks over 20% in lower than week. These are statistically vital excessive frequency breakout outcomes regardless of many shortened vacation weeks.

V&M Multibagger Record

Whereas not the aim of my mannequin, long run (utilizing the buying and selling video in FAQ #20) many of those picks could be part of the V&M Multibagger record now at 126 weekly picks with over 100%+ features, 54 picks over 200%+, 19 picks over 500%+ and 11 weekly picks with over 1000%+ features since January 2019 equivalent to:

Celsius Holdings (CELH) +2,025.1%

Enphase Vitality (ENPH) +1,509.1%

Northern Oil and Fuel (NOG) +1,115.7%

Trillium Therapeutics (TRIL) +1008.7%

Greater than 450 shares have gained over 10% in lower than every week since this MDA testing started in 2017. Frequency comparability charts are on the finish of this text. Readers are cautioned that these are extremely unstable shares that will not be acceptable for reaching your long run funding objectives: The way to Obtain Optimum Asset Allocation

Historic Efficiency Measurements

Historic MDA Breakout minimal purchase/maintain (worst case) returns have a compound common development price of 30.87% and cumulative minimal returns of +708.19% from 2017. The minimal cumulative returns for 2022 had been -0.21%, common cumulative returns had been +67.05%, and the most effective case cumulative returns had been +360.25%. The chart displays essentially the most conservative measurements including every 52 weekly return in an annual portfolio simulation, although every weekly choice may very well be compounded weekly as separate portfolios.

VMBreakouts.com

The Week 4 – 2023 Breakout Shares for subsequent week are:

The picks for subsequent week consist of three Client Cyclical and 1 Industrial sector shares. These shares are measured from launch to members upfront each Friday morning close to the open for the most effective features. Prior picks could also be doing properly, however for analysis functions I intentionally don’t duplicate picks from the prior week. These picks are primarily based on MDA traits from my analysis, together with sturdy cash flows, constructive sentiment, and robust fundamentals — however readers are cautioned to comply with the Momentum Gauges® for the most effective outcomes.

Baozun Inc. (BZUN) – Client Cyclical / Web Retail

CECO Environmental (CECO) – Industrials / Air pollution Remedy

Baozun Inc. – Client Cyclical / Web Retail

FinViz.com

Value Goal: $11.50/share (Analyst Consensus + Technical See my FAQ #20)

(Supply: Firm Assets)

Baozun Inc., by means of its subsidiaries, gives e-commerce options to model companions within the Folks’s Republic of China. The corporate gives IT infrastructure setup and integration, on-line retailer design and setup, on-line retailer operations, visible merchandising and advertising and marketing campaigns, buyer companies, and warehousing and order fulfilment. It serves model companions in varied classes, together with attire and equipment; home equipment; electronics; residence and furnishings; meals and well being merchandise; magnificence and cosmetics; fast paced client items, and mom and child merchandise; and vehicles.

StockRover.com

CECO Environmental – Industrials / Air pollution Remedy

FinViz.com

Value Goal: $16.00/share (Analyst Consensus + Technical See my FAQ #20)

(Supply: Firm Assets)

CECO Environmental Corp. gives industrial air high quality and fluid dealing with techniques worldwide. It operates in two segments: Engineered Programs Phase and Industrial Course of Options Phase. The corporate engineers, designs, builds, and installs techniques that seize, clear, and destroy air- and water-borne emissions from industrial amenities in addition to fluid dealing with, gasoline separation, and filtration techniques.

StockRover.com

High Dow 30 Shares to Look ahead to Week 4

First, you should definitely comply with the Momentum Gauges® when making use of the identical MDA breakout mannequin parameters to solely 30 shares on the Dow Index. Second, these picks are made with out regard to market cap or the below-average volatility typical of mega-cap shares that will produce good outcomes relative to different Dow 30 shares. The newest picks of weekly Dow picks in pairs for the final 5 weeks:

Image

Firm

Present % return from choice Week

CAT

Caterpillar, Inc.

-3.39%

(HD)

Dwelling Depot

-4.89%

(NKE)

Nike Inc.

+2.88%

(V)

Visa Inc.

+4.42%

BA

Boeing Firm

+8.54%

(JPM)

JPMorgan Chase & Co.

+0.73%

CAT

Caterpillar, Inc.

+5.31%

(CVX)

Chevron Company

+4.09%

(BA)

Boeing

+11.94%

(CAT)

Caterpillar Inc.

+7.30%

In case you are in search of a wider collection of giant cap breakout shares, I like to recommend these long-term portfolios. The brand new 2023 picks have been launched within the hyperlinks beneath to members to begin the New Yr:

New 2023 Piotroski-Graham enhanced worth –

New January portfolio +15.56% YTD

2022 January portfolio beat the S&P 500 by +32.54%

New 2023 Constructive Forensic –

New January portfolio +9.25% YTD

January 2022 Constructive Forensic beat S&P 500 by +6.59%

New 2023 Unfavourable Forensic –

New January portfolio +15.68% YTD

January 2022 Unfavourable Forensic beat S&P 500 by +22.18%

New Progress & Dividend Mega cap breakouts –

New January meg cap portfolio +3.04% YTD not together with dividends

January 2022 portfolio beat S&P 500 by +13.91%

These long-term picks are considerably outperforming many main Hedge Funds and the Barclay hedge fund averages since inception. Contemplate the actively managed ARK Innovation fund down -66.97% from final 12 months, Tiger International Administration -58% YTD.

The Dow picks for subsequent week are:

The Walt Disney Firm (DIS)

Disney is in sturdy breakout situations forward of Feb eighth earnings announcement. Establishments are internet patrons within the present quarter and internet MFI inflows are strongly constructive once more with analyst consensus worth goal round $125/share towards prior August highs.

FinViz.com

Background on Momentum Breakout Shares

As I’ve documented earlier than from my analysis over time, these MDA breakout picks had been designed as excessive frequency gainers.

These documented excessive frequency features in lower than every week proceed into 2020 at charges greater than 4 instances greater than the typical inventory market returns towards comparable shares with a minimal $2/share and $100 million market cap. The improved features from additional MDA analysis in 2020 are each bigger and extra frequent than in earlier years in each class. ~ The 2020 MDA Breakout Report Card

The frequency percentages stay similar to returns documented right here on Searching for Alpha since 2017 and at charges that tremendously exceed the features of market returns by 2x and as a lot as 5x within the case of 5% features.

VMBreakouts.com

The 2021 and 2020 breakout percentages with Four shares chosen every week.

VMBreakouts.com

MDA picks are restricted to shares above $2/share, $100M market cap, and better than 100okay avg each day quantity. Penny shares properly beneath these minimal ranges have been proven to profit tremendously from the mannequin however introduce way more threat and could also be distorted by inflows from readers choosing the identical micro-cap shares.

Conclusion

These shares proceed the dwell forward-testing of the breakout choice algorithms from my doctoral analysis with steady enhancements over prior years. These Weekly Breakout picks include the shortest period picks of seven quantitative fashions I publish from prime monetary analysis that additionally embody one-year purchase/maintain worth shares. Bear in mind to comply with the Momentum Gauges® in your investing selections for the most effective outcomes.

All of the V&M portfolio fashions beat the market indices once more final 12 months with constant outperformance of the most important indices. All new portfolios have began for 2023!!

VMBreakouts.com

The ultimate portfolio returns for 2022

VMBreakouts.com

All the perfect to you, keep secure and wholesome and have an amazing week of buying and selling!

J.B. Hunt (NASDAQ:JBHT) is experiencing a quantity decline throughout its enterprise on account of a weakening financial system and the stock destocking at its clients. Whereas the macroeconomic surroundings is hard, JBHT has a superb historical past of executing properly by the macroeconomic down cycles. This slowdown isn’t any completely different with JBHT’s intermodal enterprise poised to achieve market share as its clients look to save lots of prices throughout this recessionary surroundings by switching their freeway freight to intermodal. The development in rail velocity and the corporate’s sturdy relations with BNSF place it to profit throughout this era. I like the corporate’s long-term prospects and imagine it can emerge stronger on the opposite facet of the macroeconomic cycle. Therefore, I’ve a purchase ranking on the inventory.

JBHT’s This autumn FY22 Earnings

Just lately, JBHT reported lower-than-expected fourth-quarter FY23 monetary outcomes. The income within the quarter grew 4.4% Y/Y to $3.65 bn (vs. the consensus estimate of $3.80 bn). The diluted EPS declined 16% Y/Y to $1.92 (vs. the consensus estimate of $2.44). The income development within the quarter was primarily because of the improve in gas surcharge income, partially offset by a decline in volumes within the Interload ((JBI)) and Built-in Capability Options ((ICS)) segments. The diluted EPS declined considerably because of the $64 mn Y/Y improve in pre-tax casualty declare expense. This was partially offset by the corporate’s productiveness positive factors.

Income Drivers and Outlook

JBHT is experiencing a cyclical downturn available in the market leading to decrease volumes, which led to a 3% Y/Y decline in income (excluding gas surcharge income) in This autumn FY22. The height season exercise main as much as the vacations was absent in FY22 as retailers have been destocking stock to arrange for a softening macroeconomic surroundings. This resulted in weak demand within the Intermodal (JBI) section which noticed a quantity decline of 1% Y/Y within the quarter. The volumes in October have been up 4% Y/Y, down 3% Y/Y in November, and down 5% Y/Y in December. It was not all dangerous although, and one good factor that occurred within the intermodal enterprise was an enchancment in rail velocity because the quarter progressed.

JBHT’s historic gross sales information (Firm information, GS Analytics Analysis)

Within the Devoted Contract Providers (DCS) section, the demand for skilled outsourced non-public options remained sturdy, which led to a 4.6% Y/Y improve in volumes within the quarter and an 8.8% Y/Y improve in income per week. In Last Mile Providers (FMS) section, the demand for large and hulking merchandise, together with home equipment, furnishings, and train gear, has moderated. Within the Built-in Capability Resolution (ICS) section, the quantity declined 27% Y/Y and the income per load declined 9% Y/Y because of the weaker demand within the quarter. Transactional or spot quantity was down year-over-year however the contractual quantity was barely up Y/Y. The volumes within the Truckload (JBT) section elevated by 6% Y/Y regardless of the difficult freight surroundings. This was because of the elevated demand for JBHT’s drop trailer options, which leverage the J.B. Hunt 360° platform. The J.B. Hunt 360° platform supplies shippers and carriers higher entry and visibility to the availability chain.

Trying ahead, the weakening financial system and stock destocking at clients is a serious concern for JB Hunt which ought to influence volumes in FY2023. Nonetheless, there are some positives as properly. The bettering traits round rail velocity ought to permit JBHT to promote higher-valued and dependable companies to its clients within the intermodal enterprise. Roughly half (47%) of the corporate’s income is generated by the intermodal enterprise. Because of the recessionary surroundings and easing capability constraints, many firms are shifting their focus towards value financial savings and companies versus sourcing further capability. JBHT’s intermodal service supplies cost-saving alternatives to its clients by changing their freeway freight to intermodal. Whereas the volumes have been declining on account of stock destocking at its clients, the corporate is seeing alternatives to extend its pockets share by changing freeway freight and transloading extra worldwide freight into its home containers. The development within the rail service degree and capability enlargement investments positions JBHT properly to reap the benefits of the present bid season. Schneider (SNDR) ending its enterprise relationship with BNSF additionally supplies an awesome alternative for JBHT to extend its enterprise with BNSF.

The corporate’s second main enterprise, Devoted Contract Providers (DCS), which contributes ~16% to the whole income, is often long-term and contract based mostly in nature because it supplies specialised options to its clients. Therefore, I imagine this enterprise needs to be resilient throughout this weakening macroeconomic situation. The Freeway companies companies (ICS and JBT) are seeing weak spot on account of declining demand and spot charges. The corporate loved wholesome demand within the spot market over the past two years, nevertheless, with rising rates of interest demand began deteriorating which led to softening within the spot market. The corporate is specializing in successful contract enterprise in these segments to partially offset spot market weak spot.

Little doubt, FY23 goes to be a tricky 12 months for the corporate given the difficult macros. Nonetheless, the corporate is positioned properly to achieve market share throughout this downturn and emerge stronger on the opposite facet of the cycle. JBHT has a historical past of executing properly throughout the down cycles and the company-specific initiatives ought to restrict the draw back in FY23. Additional as soon as the stock destocking on the shopper finish (possible in direction of the top of this 12 months), we’d see quantity development resuming subsequent 12 months.

Margin Outlook

JBHT has been capable of enhance its working ratio since This autumn FY20 on account of larger volumes, cost-recovery efforts by value hikes, and investments in know-how. Nonetheless, in This autumn FY22, the working ratio elevated 170 bps sequentially and 150 bps Y/Y to 92.3% on account of larger casualty claims bills in addition to elevated investments to draw and retain skilled drivers and upkeep technicians. This was partially offset by value restoration efforts from value hikes and productiveness positive factors within the JBI, ICS, and FMS segments and a rise in income and productiveness within the DCS section. Excluding the upper casualty expense of $64 mn, the working ratio within the quarter improved by 30 bps Y/Y to 90.5%.

JBHT’s working ratio and working ratio excluding larger casualty expense (Firm information, GS Analytics Analysis)

Trying ahead, I imagine the corporate’s working ratio needs to be impacted in 2023 on account of decrease volumes from declining demand. Whereas the know-how investments JBHT has revamped the previous a number of quarters and enchancment within the labor market ought to assist partially offset this headwind, I’m not too optimistic in regards to the firm’s margin this 12 months. Nonetheless, in the long run, I imagine the advance in volumes and advantages from productiveness positive factors ought to assist enhance the working ratio.

Valuation & Conclusion

The inventory is presently buying and selling at 20.09x FY23 consensus EPS estimate of $9.20 and 18.43x FY24 consensus EPS estimate of $10.03, which is beneath its five-year common ahead P/E of 22.21x. The corporate’s income needs to be impacted because of the declining demand and stock destocking within the present 12 months. Nonetheless, I anticipate the destocking to be accomplished by the top of this 12 months, which ought to profit revenues in FY24. Moreover, the corporate’s income ought to profit from the market share positive factors in JBHT’s intermodal enterprise on account of its means to save lots of prices for its clients and supply higher service throughout this recessionary interval. JBHT is an effective multi-year compounding story and I imagine the present slowdown gives a superb shopping for alternative for long-term traders.

Transportadora de Gasoline del Sur (NYSE:TGS) is the operator of half of the Argentinian gasoline pipeline community, proprietor of a liquefaction plant within the nation, and of a remedy plant on the doorways of Vaca Muerta.

In November 2021, I advisable the corporate. The inventory has returned 120% since. On this overview, I present a brand new overview of the corporate’s segments, and what I count on from them. My opinion is that the present inventory worth already reductions most future constructive developments, and subsequently it isn’t a possibility anymore.

Notice: Until in any other case said, all info has been obtained from TGS’ filings with the SEC.

Enterprise description

Transportation phase: TGS core enterprise is the concession of half of Argentina’s high-transit gasoline pipelines. This enterprise has regulated costs and has suffered from contract insecurity. Throughout some intervals it has been unsustainably unprofitable (like now) and throughout others extraordinarily, but additionally unsustainably worthwhile (2016-2019). At present, regardless of its huge belongings (round $1 billion internet e-book worth), it’s producing losses, as a result of the federal government has solely granted a 60% worth enhance within the final three years (greater than 300% amassed inflation). The phase can’t develop in quantity phrases as a result of the pipelines are already utilized at full capability.

Liquids phase: TGS owns a plant in Bahia Blanca to provide ethane, propane, and butane from pure gasoline. The phase has been not too long ago very worthwhile and is the present profitability engine of the corporate. Its earnings are affected by worldwide gasoline costs however principally by gasoline availability in Argentina, which was restricted as much as 2016. The phase has proven very gradual actual (volumes) development because it resumed regular operations in 2016.

Midstream phase: The quickest rising phase of the corporate, it has two enterprise traces. The primary one is the operation of unregulated pipelines connecting the Vaca Muerta manufacturing with the primary pipelines and remedy vegetation of the area. Costs for these pipelines are unregulated and contracted between TGS and the upstream firms. The second phase is a remedy plant for pure gasoline in Vaca Muerta, one of many solely two accessible. Transported and handled gasoline has greater than tripled since 2020. Contracts on this phase are often denominated in {dollars}.

Low leverage: The corporate has a single $500 million bonds program paying 6.75% fastened and maturing in Might 2025. In opposition to these, the corporate has steadily amassed bonds and overseas foreign money, with liquid belongings for about $440 million.

Sophisticated monetary earnings reporting: Like many Argentinian firms, TGS’ monetary earnings reporting just isn’t straightforward. For TGS, with low peso-denominated liquid belongings, the primary drawback is the conversion of pesos to {dollars}. The corporate purchases {dollars} via the acquisition and sale of bonds. The acquisition has to occur on the monetary alternate price (presently about AR$350) however the ensuing {dollars} are recorded on the official price (presently about AR$180). The result’s an automated loss on the truthful worth of belongings. I want to disregard these points, on condition that TGS has a small internet legal responsibility publicity to overseas foreign money, and easily think about the curiosity value in {dollars}.

Current developments

Transportation is already unprofitable: For the primary time since 2016 (when charges had been adjusted), TGS’ transportation phase presents an working loss in 3Q22. It is extremely possible that the federal government will present a worth enhance to cowl inflation quickly, because the infrastructure managed by TGS is important.

Liquids phase maintains document (and unsustainable?) profitability: The liquids phase is geared to publish $230 million in working earnings (on the official price) for FY22, an identical determine to the one revealed for FY21. The issue is that pure gasoline costs are already right down to 2020 ranges when the corporate generated about $120 million in working earnings. In my view, the $120 million determine appears extra lifelike contemplating gasoline costs for the previous decade.

Midstream is rising quick and is sustainable: Transported gasoline reached 13 MMm3/day in 3Q22, up from 6.four MMm3/day in 3Q21 and three.four MMm3/day in 3Q20. Gasoline remedy contracts within the Tratayen plant reached 9.four MMm3/day from 3.Three MMm3/day in 3Q20. New pipelines had been approved in April for one more 17 MMm3/day that ought to be on-line in June 2023. Extra capability for the Tratayen plant for one more 9 million MMm3/day is predicted on-line in 2023 as nicely.

Profitability calculations

Transport phase: It is a low-risk, asset-heavy funding with regulated costs. Idea signifies that IF (an enormous if) the federal government desires to succeed in a long-term association, it ought to present a comparatively low return on belongings. In my view, with about $1 billion in internet belongings, the phase will be valued as if producing about $50 million in yearly operational earnings, ultimately.

Liquids phase: With volumes not rising considerably since 2016, and profitability principally affected by pure gasoline worth actions in 2021 and 2022, I want to return to a conservative state of affairs of $120 million in working earnings for this phase, as proven throughout the interval 2016-2020. If ultimately worldwide pure gasoline costs stay elevated, then they could possibly be revalued.

Midstream: Solely contemplating the capability that’s already contracted and the bulletins of latest capability included in 2023, this phase is predicted to ultimately double its volumes.

Profitability ought to transfer with volumes. For instance, transported gasoline grew 70% between 3Q22 and 3Q21, and handled gasoline grew 15% throughout the identical interval (contracts for remedy doubled although). Throughout that interval, revenues grew solely 15% in actual Argentinian peso phrases (30% if FX results are neutralized).

In my view, from the present $60 million (annualized from 3Q22 earnings), this phase ought to have the ability to attain $100 million in working earnings within the subsequent two years.

Monetary bills: The corporate’s bonds pay $37 million in annual curiosity, however the firm can be producing about $16 million in curiosity earnings from its $400 million in liquid belongings. This leaves an approximate internet monetary value of $20 million yearly.

Revenue taxes: As normal, I think about a 35% tax price, the statutory price in Argentina.

Then, including up $50 million from transportation in a regulated surroundings (presently producing losses), $120 million from liquids below MMBTU costs between $Three and $5, and midstream incomes $100 million within the subsequent two years, I arrive at $270 million in working earnings.

From these $270 million, I subtract $20 million of curiosity, after which 35% earnings taxes. The result’s that I count on the corporate to generate $160 million of internet earnings, in the long run.

Keep in mind that the long run means a worthwhile, albeit low return, transportation phase (right now making a loss), a liquids phase producing virtually half of what it generates right now by way of earnings, and a midstream phase virtually twice as large as it’s right now.

Nonetheless, with TGS buying and selling at $3.Three billion, I consider it’s costly, and it doesn’t characterize worth anymore.

I final wrote in regards to the SPDR Portfolio S&P 500 Excessive Dividend ETF (NYSEARCA:SPYD) again in July 2021, arguing that whereas the ETF was set to outperform the SPX, the excessive diploma of volatility meant that the returns have been not well worth the threat. Since then, valuations have fallen considerably, however so has the chance value when it comes to the risk-free charge. Whereas the SPYD will outperform US Treasuries over the long run, the fairness threat premium is at report lows. Buyers within the SPYD are accepting a really low premium over USTs to compensate for the upper threat when it comes to draw back volatility and I due to this fact favor USTs over the approaching months.

The SPYD ETF

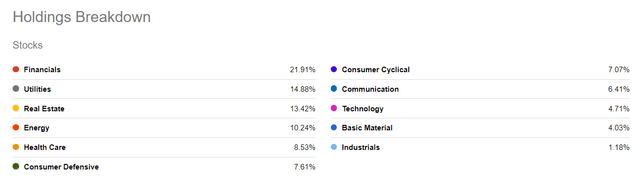

The SPYD ranks all dividend payers within the S&P 500 by indicated yield (the newest dividend, multiplied by dividend frequency, divided by share worth) and selects the highest 80. SPYD doesn’t embody any of the dividend sustainability or high quality screens which are baked into some peer ETFs. SPYD equally weights its portfolio whereas some related, income-focused funds weight by yield. Because of this, the ETF has a a lot increased weighting of financials, actual property, and vitality relative to the S&P 500. Know-how, in the meantime, represents lower than 5% of the index, as one would anticipate given the low dividend funds within the sector. The ETF has a minimal expense ratio of 0.07% and a distribution yield of 4.7%. Nonetheless, this yield will nearly actually fall, absent a decline in fairness costs, because the ahead dividend yield on the underlying S&P 500 excessive dividend yield index is simply 4.0%.

Seekingalpha.com

Actual Return Outlook Is Respectable…

The S&P 500 excessive dividend yield index has risen to 4.2% from 3.9% in mid-2021, because of rising dividend funds. This rise in dividend funds has truly underperformed different fundamentals akin to gross sales and earnings. Because of this, the dividend payout ratio sits simply above 50%, which is the bottom it has been within the knowledge accessible which is from 2016. Notably, this low payout ratio doesn’t replicate outsized revenue margins, because the rise in earnings has come from an increase in gross sales over the previous 18 months.

SPYD PE, DY, and Dividend Payout Ratio (Bloomberg)

This has led to a sizeable rise in long-term anticipated returns. The SPX has returned roughly 8% in actual phrases per yr over the long run when valuations have been on the stage of the S&P 500 excessive dividend yield index at the moment. It might be argued then that these are the returns one ought to anticipate on the SPYD. Nonetheless, these sturdy historic returns partly replicate sturdy development seen over this era, the place actual GDP averaged over 3%. The actual GDP development outlook now sits at lower than 1% based mostly on pattern charges of productiveness and labor pressure development. As excessive dividend paying shares are likely to develop extra slowly as they’re typically mature firms, dividend development is prone to be even decrease than this for the SPYD. Moreover, the long-term SPX returns have been supported by rising valuations, which has added one other 1% to annual returns. Taking these elements into consideration, actual returns look prone to be round 4% over the long run.

However The Fairness Threat Premium Is Too Low

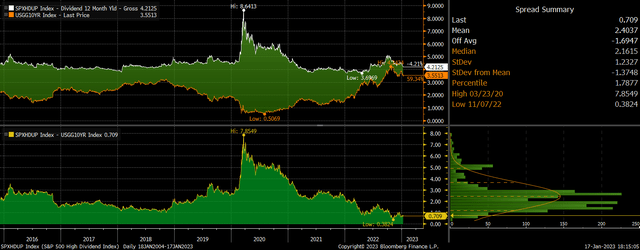

In contrast with the true return outlook for the SPX, which I estimate to be round zero, that is fairly sturdy, however within the context of present elevated bond yields this can be very low. The chart under exhibits the dividend yield on the S&P 500 excessive dividend yield index versus the 10-year US Treasury bond yield. The present unfold of 0.6% is the bottom on report and compares to a median of 1.9% since 2016.

SPYD Dividend Yield Vs UST Yield (Bloomberg)

It’s the identical story once we evaluate the dividend yield to 10-year inflation-linked bond yields, which present long-term returns after inflation. As shares are actual belongings, they need to be anticipated to rise with the rising worth stage over time, and so any comparability with bonds is healthier to be made with inflation-linked bonds quite than common Treasuries. The present unfold of two.9% might be regarded as the return of extra return on the SPYD over the subsequent decade assuming no change in valuations and assuming that dividends develop on the charge of inflation. Whereas 2.9% per yr could seem to be ample compensation for the added threat of investing in shares, it compares with a 7-year common of 4.4% and a excessive of 8.7% seen on the top of the Covid crash.

SPYD Dividend Yield Vs US Inflation-Linked Bond Yield (Bloomberg)

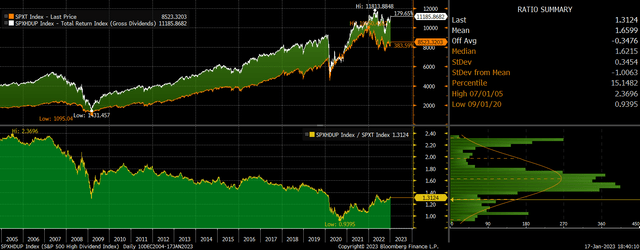

A Observe Document Of Underperformance In Bear Markets

This 2.9% fairness threat premium isn’t so engaging once we take into account the efficiency of the SPYD throughout bear markets. Within the Covid crash the ETF misplaced 47% of its worth, and losses in the course of the international monetary disaster have been a staggering 73%. The excessive weighting of economic and actual property shares, which have a 35% weighting, makes the ETF extremely vulnerable to financial weak point and credit score stress. As we noticed over the last two main downturns, US Treasury bonds truly carried out nicely as expectations of decrease rates of interest noticed yields plummet. I see a rising chance of one other rotation into bonds and away from shares because the financial development outlook continues to deteriorate.

SPYD Vs SPX (Bloomberg)

Abstract

The outlook for the SPYD has improved over the previous 18 months, and actual long-term return expectations now sit at round 4%. Whereas that is engaging relative to the SPX and is increased than the returns anticipated on US Treasuries, bonds characterize a greater risk-reward commerce within the present local weather because of the threat of sharp losses within the SPYD within the occasion of a recession.

A vacation-shortened week is trying like it’ll get off to a decrease begin, as China landed some weak development numbers and extra earnings roll out. That’s after two constructive weeks to start out 2023.

However there’s greater than a whiff of bullishness within the air, in keeping with our name of the day, from funding analysis platform Macro Ops’ founder and chief funding officer Alexander Barrow.

“The burden of the proof strongly tipped in favor of the bulls final week after numerous excessive sign breadth thrusts triggered,” writes the Macro Ops workforce in a Monday weblog put up. They see that might drive some first rate S&P 500 features earlier than “it rolls over once more.”

Market breadth refers to what number of shares are taking part in an up or down transfer. Breadth thrust indicators can decide the place markets are going, and in keeping with some, are sometimes be discovered at first of latest bull markets.

“It’s our view we’re in a broader topping course of at finest as we count on a recession close to the tip of the 12 months. However after final week now we have to be open to the potential of a run on the prior Jan highs, which might be 20% above present ranges,” says the Macro Ops workforce.

Learn: U.S. shares may fall 10% as ‘ache commerce’ takes maintain earlier than bouncing again later within the 12 months

They pointed to others who additionally seen some breadth thrust indicators final week, together with proof of an “unprecedented breadth trifecta kind Quantifiable Edges. The primary a part of that’s longtime investor Walter Deemer’s Breakaway Momentum sign that signifies “actually highly effective upside momentum,” which he tweeted about lately:

@WalterDeemer

The remainder of that triple sign got here from Wayne Whaley’s Advance Decline Thrust after which the Quantifiable Edges personal Triple 70 thrust sign.

As Quantifable Edges identified, Thursday was the primary time all three landed on the identical day. Two of three indicators triggered the identical day has occurred solely seven instances, in keeping with the chart beneath:

Quantifiable Edges

Aside from flagging a string of bullish indicators, the Macro Ops workforce affords some investing recommendation as nicely — they counsel publicity to house builders proper now (a sector they flagged in November.)

“The market is waaaay obese a recession within the 1st half of this 12 months, when financial information and financial lags behind means that’s not going to occur till nearer to 12 months’s finish. This implies Q1/Q2 earnings gained’t be as dangerous as many count on, which implies individuals are underweight threat. A reverting risk-cycle + a reopening China ought to assist compress large mortgage spreads, boosting demand in a provide constrained market, which is nice for builders,” says the workforce, who like BlueLinx Holdings BXC and Builders FirstSource BLDR.

Learn: Fund managers are ‘quite a bit much less bearish’ than the fourth quarter, says Financial institution of America

The markets

MarketWatch

Inventory futures ES00 YM00 NQ00 are decrease, whereas bond yields BX:TMUBMUSD10Y BX:TMUBMUSD02Y are headed the opposite manner, together with the greenback DXY. U.S. crude costs CL are regular — OPEC left its forecast for 2023 oil demand unchanged, however stated there are many uncertainties for the market — and gold GC00 is dropping. Bitcoin BTCUSD spiked above $21,00zero over the weekend and continues to commerce above that degree.

The thrill

On the heels of an enormous batch of Wall Road financial institution earnings final week, Goldman Sachs’ GS has reported disappointing outcomes, together with provisions for credit score losses, and shares are down in premarket. Morgan Stanley MS inventory is barely decrease as earnings topped estimates by a penny per share, and credit-loss provisions surged. Signature Financial institution SBNY additionally reported and shares are barely increased regardless of an earnings miss.

Vacationers TRV inventory is falling after the insurer’s steering fell wanting market hopes.

Netflix NFLX will report later this week.

Shares of Nationwide devices NATI are increased in premarket after Emerson Electrical EMR lifted its bid for the measurements methods maker to $7.6 billion.

Shares of Chinese language EV maker Xpeng XPEV are down after the Chinese language EV maker lower costs for many of its vehicles by round 10%, following comparable strikes by Tesla earlier this month.

China introduced its first total inhabitants decline in many years as society ages and birthrates plunge. And it reported information exhibiting its financial system grew by 3% in 2022, lower than half of the earlier 12 months’s 8.1% price, the second-lowest annual price since at the least the 1970s.

Meme-stock investor Ryan Cohen has reportedly taken a stake in China’s Alibaba BABA and launched an activist marketing campaign to get the e-commerce large to buyback extra shares. Shares are barely decrease.

The Empire State manufacturing index is forward, in per week that can carry updates on retail gross sales and the housing market, together with different information and a few Fed converse.

The founders of defunct crypto hedge fund Three Arrows Capital and crypto trade CoinFlex are pitching a brand new crypto trade that can deal with claims buying and selling.

Better of the online

Deaths of despair could also be pushed by lack of faith, new analysis paper argues

The return of El Niño will carry unprecedented warmth waves this 12 months, local weather consultants warn

400 folks informed the New York Instances how a lot cash they make.

A famed genetics professor fined $29 million after convincing pal to speculate $20 million in his “miracle” Huntington’s illness remedy.

The chart

@bondvigilantes

The most important macro choice of the week may come from the Financial institution of Japan on Wednesday, as hypothesis construct that the central financial institution may finish its ultra-easy financial coverage and yield curve management.

“The Financial institution has had to purchase a report quantity of Japanese authorities bonds to defend the coverage because it was tweaked in December, with latest shopping for far exceeding prior peaks,” factors out Gurpreet Gill, macro strategist for international mounted revenue at Goldman Sachs Asset Administration.

For now, watch the yen USDJPY and JGBs, say strategists.

The tickers

These have been the top-searched tickers on MarketWatch as of 6 a.m. Japanese Time:

Ticker

Safety title

BBBY

Mattress Tub & Past

TSLA

Tesla

GME

GameStop

AMC

AMC Leisure Holdings

MULN

Mullen Automotive

NIO

NIO

BABA

Alibaba

APE

AMC Leisure Holdings most popular shares

AAPL

Apple

DWAC

Digital World Acquisition

Random reads

Scientists steer lightning bolts with laser beams for the primary time.

Wyoming lawmakers need to ban electric-car gross sales, to guard the oil-and-gas trade.

Have to Know begins early and is up to date till the opening bell, however join right here to get it delivered as soon as to your electronic mail field. The emailed model shall be despatched out at about 7:30 a.m. Japanese.

Take heed to the Greatest New Concepts in Cash podcast with MarketWatch reporter Charles Passy and economist Stephanie Kelton.