ALLVISIONN/iStock by way of Getty Photographs

Earlier this week, we posted an article that defined our ideas concerning Blackstone Inc.’s (NYSE:BX) transfer to restrict the redemptions of its public non-listed REIT, Blackstone Actual Property Earnings Belief (“BREIT”).

Briefly, we expect that the market overreacted to the information, and that is largely as a consequence of all of the scary headlines put out by numerous media retailers.

Its REIT is doing simply wonderful and so is Blackstone itself. Each have robust steadiness sheets, get pleasure from quickly rising money circulation, and are not dealing with any type of misery, regardless of this turning into an more and more widespread narrative.

Simply take a look at a few of these current headlines: the primary one makes it appear as if Blackstone was struggling a “financial institution run,” which is a extreme exaggeration of what is actually taking place, and the second makes it appear as if BREIT was dealing with a “stoop in efficiency” when in actuality, its web working revenue is up by 13% over the previous yr:

At present, I’m scripting this follow-up as a result of Blackstone’s co-founder, Steve Schwarzman, simply spoke on this subject at a convention and it deserves your consideration.

Speaking at The Goldman Sachs (GS) convention, Schwarzman famous that he’s “baffled” by all the troubles about BREIT:

“I watch on tv someday and persons are involved about it, I discover it a bit baffling… The concept that there’s something going fallacious with this product as a result of some persons are redeeming, is conflating utterly incorrect assumptions, utterly incorrect assumptions.”

Blackstone

He goes on to clarify that the basics of BREIT are literally very robust and that the longer term is brilliant even regardless of the difficult surroundings:

“What we did with BREIT is we concentrated it in warehouses and residences and we averted virtually all the opposite asset lessons. We have now 80% of the fund in these terrific performing asset lessons…. One other factor that’s necessary is the place is that this actual property? These 70% in BREIT is within the Sunbelt… it’s 5x the inhabitants development in the remainder of the nation… So we’ve bought excellent places with terrific belongings.

Our NOI went up this yr at 13%. The typical REIT went up 8%. So we’re out-earning that by like 65%. BREIT, as a result of it was so profitable, its returns have averaged 13% a yr for the final 6 years. That’s 3x the return of the REIT index.

… We personal actual property that’s a minimum of 20% beneath market costs. So the marketplace for warehouses and multifamily continues to be going up. Inexperienced Avenue, which is a giant adviser, mentioned that they assume these two asset lessons will probably be up someplace within the 8% to 9% zone this yr. And we have now this huge portfolio that rolls off its leases. Leases terminate fairly shortly on this space within the three to 4-year zone. And if you happen to simply mark that as much as present market with out the appreciation, you’ll be able to see this will probably be a really optimistic expertise for traders.”

So clearly, BREIT is doing very properly from a basic perspective. It owns extremely fascinating belongings which have a robust monitor document and are anticipated to continue to grow rents at a speedy tempo. That is largely as a result of they’re positioned in rising markets, but in addition as a result of their present rents are beneath market.

So why are there so many traders making an attempt to get out of BREIT?

Schwartzman supplies an attention-grabbing clarification. It has little to do with fundamentals and much more with the liquidity of sure particular Asian traders:

“We set it up initially 6 years in the past in order that we might not allow redemptions past 5% 1 / 4… and what occurred is we went over that 5% final month. So what occurred? We began asking ourselves, what’s occurring? And we discovered the best way to fasten something that these redemptions had been preponderantly coming from Asia. The identical product is in the US. It’s U.S. actual property. What was occurring in Asia? And it didn’t take lengthy to determine that the Grasp Seng Index went down 40% and the Asians have a tendency to make use of extra leverage, extra margin debt. So if you’re an investor who has bought margin debt and your market goes down 40%, you’ll be able to think about what it was prefer to be a kind of into the swimming pools. You’re below excruciating monetary strain, and they also had been simply searching for liquidity.”

I believe that many Blackstone shareholders will cease right here and really feel reassured that the redemptions are restricted to Asian traders, which seemingly aren’t even a giant a part of the REIT. If that is the case, then the redemptions would seemingly be extra restricted than what some might need predicted. After a couple of months of detrimental development, the inflows may quickly surpass the outflows once more, resulting in a speedy restoration in Blackstone’s share worth.

However I concern that this idea is fallacious.

Sure, Asian traders might need been the primary ones to ask for redemptions, however they aren’t alone.

Asian traders had been first in-line as a result of their inventory market has dropped probably the most and it triggered many to rethink their allocation to BREIT.

In case your shares are down 40% over the previous yr, however BREIT is up 10%, then it turns into very tempting to get out of BREIT to reinvest in shares at a lot better valuations. Comparatively talking, BREIT has develop into loads much less engaging relative to the shares as a result of the efficiency disparity has been so exceptionally massive.

This utilized first to Asian traders, but it surely additionally applies to U.S. and European traders, and plenty of of them will need out as properly.

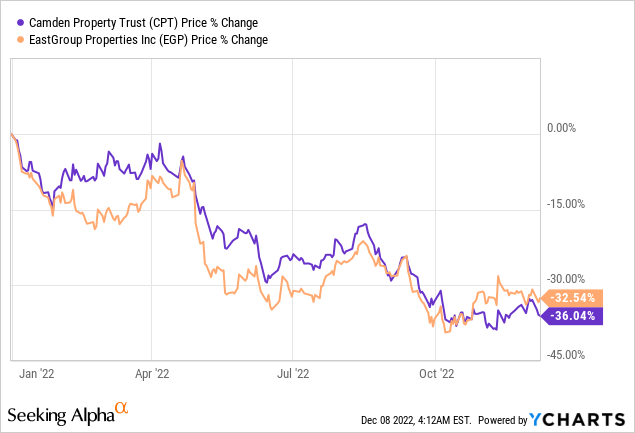

The listed REIT (VNQ) market is down 25% year-to-date within the U.S., at the same time as BREIT is up 10%. That is an enormous disparity! There are a lot of high-quality listed REITs like Camden Properties (CPT) and EastGroup Properties, Inc. (EGP) that personal comparable belongings as BREIT, however they’re down 35%:

YCHARTS

These listed REITs at the moment are priced at a 20-30% low cost to their web asset worth, however BREIT means that you can redeem at par with its web asset worth.

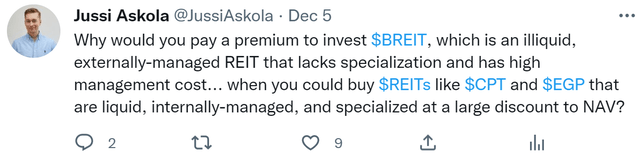

And naturally, traders at the moment are cashing out of non-listed REITs to spend money on listed REITs as an alternative. I just lately posted the next tweet about this:

Twitter Jussi Askola

Listed REITs have loads much less to lose and much more to realize as a result of they’re priced at a steep low cost to NAV at the same time as BREIT is priced at an all-time excessive.

That is for a similar belongings!

And so there’s a vital arbitrage in promoting the illiquid asset to purchase the liquid one, and that is what’s driving all these redemptions. So long as this stays true, I anticipate to see extra outflows than inflows into not simply BREIT, but in addition different non-listed REITs.

Actually, Starwood, one other main asset supervisor, additionally simply restricted the redemptions of its non-listed REIT.

It exhibits you that this isn’t about Blackstone. It’s merely that listed actual property affords a greater deal, and so it’s pure for BREIT traders to need out.

Takeaway #1:

The primary takeaway right here is that the headwind of redemptions may final for lots longer than lots of the bullish shareholders might need wished for.

BREIT is a vital payment generator and development driver for Blackstone’s enterprise, so that is vital information, and Blackstone deserves to commerce at a considerably decrease valuation.

Did it drop an excessive amount of?

Maybe, however you can’t deny that this can be a detrimental improvement in its enterprise.

I truly assume that Blackstone is a Purchase at as we speak’s valuation, however I additionally assume that there are higher alternatives on the market, and for this reason I’m not investing in it. There are different asset managers which are much less uncovered to such dangers as a result of they’ve extra everlasting capital (no redemption threat), and but, they’re priced at decrease valuations in lots of instances. Examples that I desire embody KKR & Co. Inc. (KKR), Blue Owl Capital Inc. (OWL), and Patria Investments Restricted (PAX).

Twitter Jussi Askola

Takeaway #2:

Listed REITs are as we speak deeply undervalued, and I believe that it’s a nice time to be investing in them.

They’re down so closely due to fears of rates of interest, however what the market seems to have missed is that REIT steadiness sheets are the strongest ever, with simply 35% debt and lengthy maturities at practically 10 years. So the impression will not be vital on the fee facet, however the inflation has pushed rents loads decrease.

BREIT has grown its similar property NOI by 13% this yr, and that is nothing unusual. Earlier, we talked about CPT and EGP, and each have additionally grown their same-property NOI this yr by 10%+ – and but, they’re down 35%.

This basically signifies that their valuation has been minimize in half and so they now commerce at massive reductions to truthful worth. If I used to be invested in BREIT, I might attempt to exit to purchase such undervalued REITs as an alternative.