Robert Means

Chinese language electrical car big BYD (OTCPK:BYDDF) reported file month-to-month gross sales in its new electrical car division for the month of August a couple of days in the past. BYD leads the Chinese language market by way of deliveries and has centered aggressively on exporting its EVs to different nations all over the world, together with the European Union. BYD generated spectacular gross sales progress for plenty of months now, which is spectacular contemplating the growing challenges available in the market so far as demand and margins are involved. BYD has the second-largest gross margins in its business group, after Li Auto (LI), and I consider BYD continues to symbolize wonderful worth for progress buyers within the Chinese language EV business.

Earlier ranking

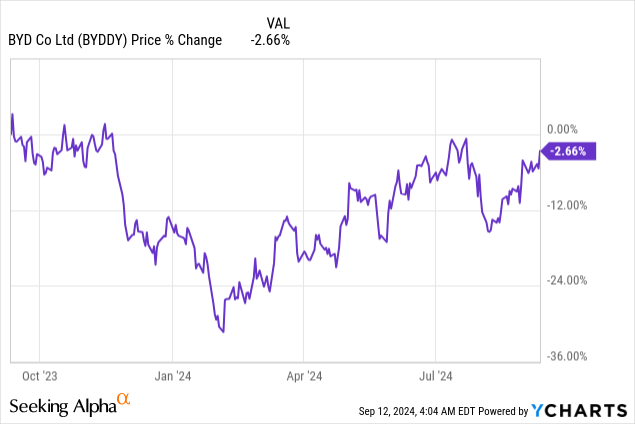

I rated shares of BYD a powerful purchase in June — A Worthwhile EV Progress Play —as a result of the electrical car firm executed very nicely on its progress technique. Additional, BYD distinguished itself by being a solidly worthwhile EV firm which in my view lowered funding dangers for buyers. BYD lately reported file gross sales, in an general weak market setting, and I consider that BYD is undeservedly low-cost, based mostly off of earnings. I proceed to see the EV big as top-of-the-line EV funding choices available in the market.

Report gross sales, export momentum spectacular margins

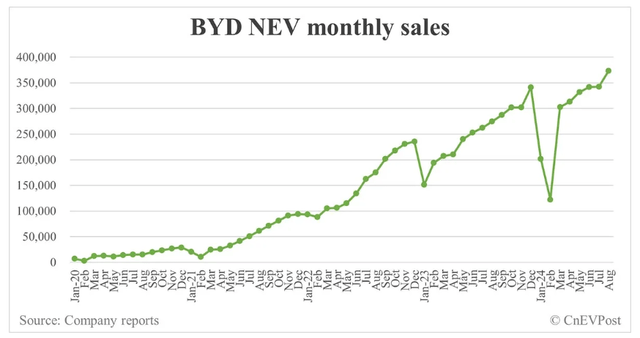

Regardless of its giant measurement, BYD remains to be placing up some very spectacular progress numbers. Within the month of August, BYD offered 373,083 new electrical automobiles, exhibiting a year-over-year progress fee of 36%. The corporate additionally exceeded its earlier gross sales file from July by greater than 30ok items.

BYD’s new power car gross sales have been in a constant and wholesome uptrend since March, which is when EV gross sales sometimes recuperate from a stoop as a result of Chinese language Lunar New Yr. Throughout this era, manufacturing crops sometimes shut as staff head residence for holidays, resulting in a seasonal gross sales dip that impacts all EV producers equally. The rebound in new electrical car gross sales since March exhibits that the EV big remains to be doing a wonderful job in scaling its manufacturing, nonetheless, and new gross sales information going ahead are possible.

BYD

NIO (NIO), did additionally moderately nicely with its deliveries in August: NIO delivered 20,176 automobiles final month. It was the fourth month by which NIO delivered greater than 20ok EVs to its prospects, however the Y/Y progress fee in August was a way more average 4%. XPeng (XPEV) delivered 14,036 Sensible EVs in August, exhibiting 3% year-over-year progress. Li Auto (LI), which is an EV start-up that provides by far the very best car margins in extra of 18%, delivered 48,122 automobiles in August, exhibiting 38% progress year-over-year.

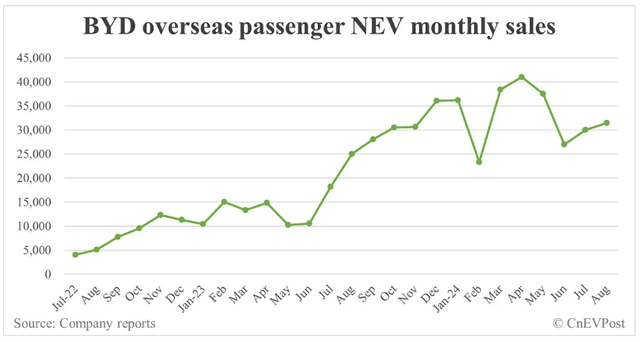

BYD can be fairly profitable in abroad markets, particularly with fashions such because the BYD Atto Three or the BYD Seagull. The Chinese language EV agency offered 31,451 automobiles outdoors of China in August, exhibiting a year-over-year progress fee of 26%.

BYD

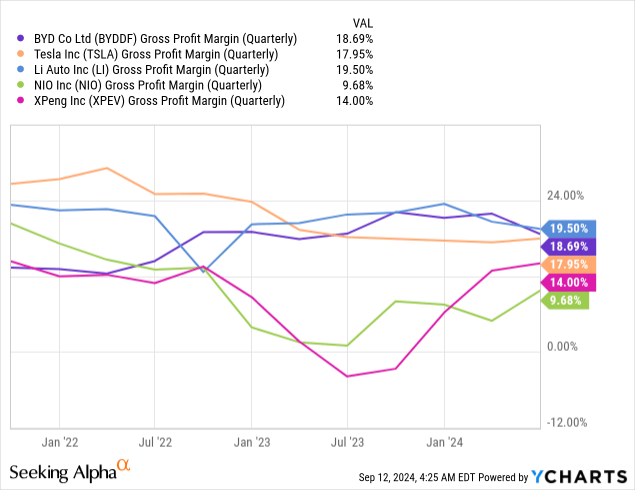

The margin image for BYD can be fairly spectacular: the EV maker had the second-highest gross margins in Q2’24 after Li Auto… which I’ve beforehand highlighted as a prime margin play for EV buyers. BYD achieved gross revenue margins of 19% within the second-quarter, which is about 1 PP increased than what Tesla (TSLA) achieved.

BYD’s valuation

BYD is at present valued at a ahead price-to-earnings ratio of 16.0X, however its rivals within the EV start-up business aren’t but worthwhile on a broad-scale foundation (Li Auto is the exception). For that reason, I’m evaluating BYD to different Chinese language EV producers based mostly off of a price-to-revenue ratio.

BYD is at present valued at a P/S ratio of 0.73X, which is means under the business group common P/S ratio of 1.92X. Tesla is by far the costliest EV firm, largely as a result of it’s centered on the U.S. market, which provides buyers increased ranges of transparency. With out Tesla, the business group common price-to-revenue ratio is 0.83X. Tesla is by far the costliest firm within the business group with a P/S ratio of 6.3X, however the EV firm has a ton of catalysts which might assist, in my view, a fair increased valuation multiplier.

In the long term, I consider BYD may commerce at a considerably increased P/S ratio as nicely, largely as a result of the corporate is seeing large supply momentum and is already worthwhile. The truth that BYD is already producing actual earnings is one thing that lowers dangers for buyers and makes shares particularly engaging contemplating that the majority EV start-ups, each in China and the U.S., are dropping cash on their EV operations.

BYD can be anticipated to attain a better complete income quantity than Tesla subsequent 12 months, which might make the corporate the largest EV firm on this planet. As I said in my final work on BYD, I see a good worth P/S ratio of two.0X for BYD, largely as a result of the EV maker is already worthwhile and has the biggest EV supply quantity. Based mostly off of a FY 2025 income estimate of $123.4B (see desk under), a 2.0X honest worth P/S ratio interprets into a good worth goal of $85 per-share.

| Firm | Income FY 2025 ($B) | Y/Y Progress | Ahead P/S |

| BYD | $123.42 | 16% | 0.73X |

| Tesla | $116.32 | 17% | 6.27X |

| Li Auto | $27.56 | 35% | 0.75X |

| NIO | $13.47 | 37% | 0.86X |

| XPeng | $8.91 | 56% | 0.97X |

| Common: | 1.92X | ||

| Common ex-TSLA: | 0.83X |

(Supply: Writer)

Dangers with BYD

One huge danger that I see with BYD pertains to tariffs that different nations impose with a purpose to defend their home EV manufacturing industries. The European Union, for instance, lately added tariffs of as much as 38% on Chinese language EV imports in a bid to counter the dumping of low-cost electrical automobiles. Larger costs clearly make BYD’s automobiles costlier and fewer aggressive, probably affecting its export potential negatively. What would change my thoughts about BYD is that if the corporate had been to see decrease margins in its EV enterprise or slowing supply progress in China, which remains to be BYD’s core market.

Remaining ideas

BYD simply reached a brand new gross sales file for its new electrical car gross sales in August, which is a decent achievement in a market that’s seeing slowing supply progress general and rising margin stress as a result of growing competitors. BYD continued to develop at spectacular charges in August and nearly achieved the identical progress as Li Auto, which is the quickest rising EV participant within the start-up business group. BYD’s exports are additionally wanting sturdy, however EU tariffs symbolize a short-term danger. I proceed to love BYD right here as the corporate executes very nicely on its progress technique, stays extremely aggressive by way of margins and its shares are nonetheless massively undervalued.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.